The AR for the year 2017-18 is out & the mgt. is distinctly bullish about the prospects going forward. The Co. is in expansion mode increasing capacities aggressively over the next couple of years & hopes to do a turnover of about 450 crores by then, an increase of about 60% from current levels. The mgt. is perhaps playing it safe when they say “on similar EBITDA margins”, though the operating margins saw improvement in each successive quarter in 17-18.

The prospects are getting better due to several plant shutdowns in the developed world, where the Co. is currently exporting. For the current year 18-19, the Co. could do an EPS of around Rs.15 and at current price of about 142 appears to be attractively valued.

Another development that has seemingly gone somewhat un-noticed is that the promoters have increased their stake in the Co. from 69.2% to 71.56% over the recent past.

Management guidance of 450 cr turnover by FY 20 looks optimistic. That is more than 50% growth from FY 18 sales. Its true that capacity is going up as much as 50% but I am skeptical if they will be able to ramp up the production that fast and more importantly sell everything they produce. going by the sales volumes for last 3 years, capacity constraints isn’t the only constraint company is facing. Offtake from customers and pricing pressure from competitors also appear to be constraints.

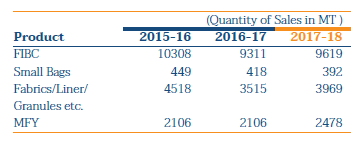

Source: Annual Report FY 18.

FIBC & fabric sales have dropped in FY 17 and only marginally improved in FY 18 and still below FY 16 level. Expecting a 50% jump in 2 years with this data is too optimistic.

Management hasn’t provided an explanation of how they are likely to achieve a turnover of 450 Cr in two years so that number should be taken with a pinch of salt.

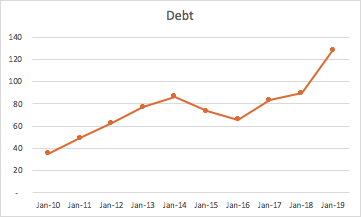

Can someone enlighten on the debt creeping up year on year (is it due to the capex?), also the debtor days seems to be on the rise as well.

Any idea on why the company is not trying to reduce the debt? Also seems like, whenever they want to do capex, they need debt (not much from internal accruals).

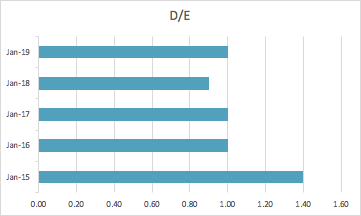

From screener, the companies D/E never went below 0.5

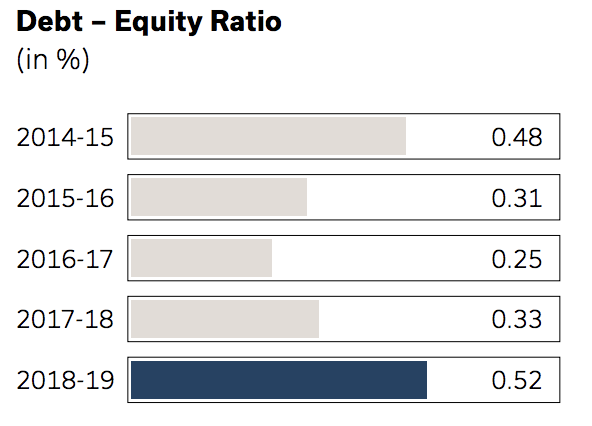

but the company’s AR claiming differently. source: AR-2018-19

Yes, company undertook a major expansion project. It is a state-of-the-art, Greenfield expansion which has increased the capacity by almost 50%. This expansion was in both FIBC and MFY. Infact MFY capacity has increased much more. The expansion was completed in July 2018 and teething problem and ramp-up started only in Q4 2018. The expansion will allow company to enter new applications and markets. The 20 acre facility has huge built up space for many more phases of expansion.The expanded capacity, once fully utilized, is expected to take company into a different orbit all together. Also, as I understand, with expansion program now completed, company is planning to reduce debt.

Company is now managed by a combination of both experienced and young energetic leadership and appears to have ambitious growth mindset. Please refer to recent Video on the company which was telecasted 10 days back on both CNBC & CNBC Awaz under the show - “incredible journeys- brands and leaders”. Hopefully, it may provide some more insight.

Acute shortage of FIBC in Europe and across globe. Statement from European FIBC association (EFIBCA) confirms this.

Vertically integrated manufacturers like Kanpur Plastipack should benefit from this. Their long term customer relationships, which have been built on pillars of high quality, timely deliveries and customized products should carry them long distance in profitability.

The greenfield capacities built in the new state-of-art plant are running at full utilisation and the additional brown field capacities in the same location are already kicking in through stage wise deployment of machines which will be fully completed in June 21.efibca_statment_on_current_supply_situation (1).pdf (172.0 KB

Attended the AGM of Kanpur plast. The Investors had asked some good questions. But the management had not given sufficient clarity during the AGM meet.

Based on the Q2 2021 investor presentation, they are outperforming on the revenue front.

Anybody knows why the fall is so drastic from 200 levels?

I feel the PE is very compelling at 7.90

The share went ex-bonus in September 21, so you need to adjust past EPS accordingly and PE would be around 10.

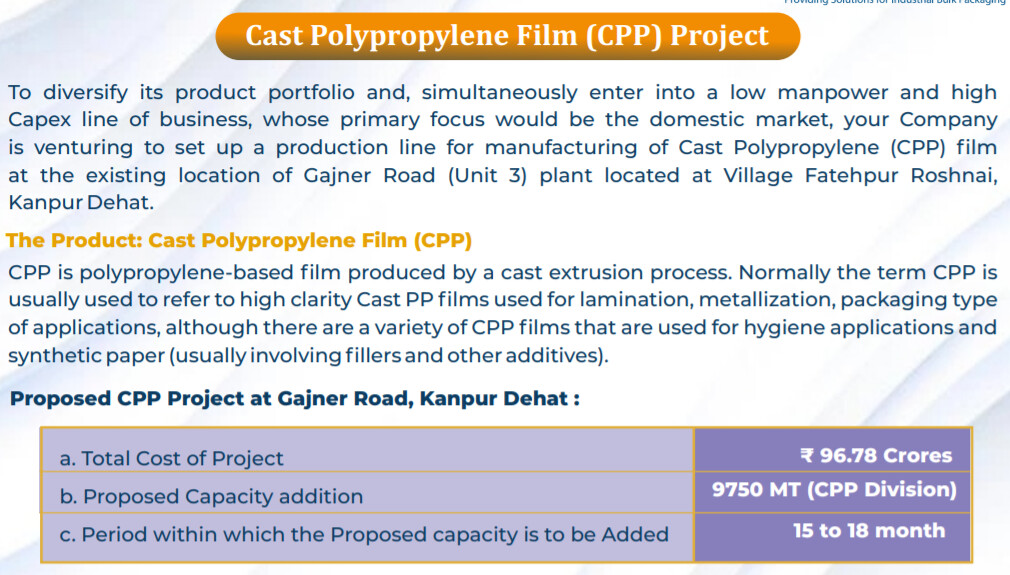

The CPP film initiative is based on the rising demand on CPP films due to its excellent recyclability and other properties.

With ban on single use plastic coming ON in June 22 along with clear “plastic waste management policy”, there is a pressure on FMCG and other industries to use CPP film which offers much superior recyclability.

I expect revenue of 150 to 200 cr, from the CPP line.

Since, CPP will be low labour product, expansion and scaling up will be relatively can be done in relatively seamless way.

In AGM I asked this Question. Being conservative management MD gave me broad range of 8-15%. However, I understand that their product will be consumed in region around Kanpur itself (Lots of Gutka and rural focussed FMCG companies are there). CPP business may generate 200 cr sales. Even with 10% margin it will contribute around 20cr to ebita.

Thanks for the reply. I have one more question. Due to fright cost reduction with the same volume they will have 20-25 cr added to ebitda this FY. Is there any chance of topline coming down due to crude price falling? Because in FY22 the revenue was 1.38x over fy21 w/o much volume growth.

So due to cpp extra 20 cr to ebitda + freight cost coming down giving additional 20-25 cr ebitda should take the ebitda to 90 cr. so it’s available at forward ev/ebitda of 4.68. Historical lowest ev/ebitda around 4. So will there be any negative impact of crude price coming down on the bottom line or the gross profit level? except this negative point the company seems to be at cheap valuation.

CPP line will be commercialised Q1 next fiscal.

As for their FIBC business, falling RM should aid their bottomline (after high cost inventory gets exhausted). But, larger issue is weakness in Europe which their major market in exports.

However, FIBC being used for packing essential commodities like food grains, Pharma, milk powder etc etc, the dip may not last long.

CPP is completely domestic business and CPP being highly recyclable, majority of FMCG and other industries will shift from BOPP to CPP to ensure tighter recyclability norms (enhanced producer responsibility - EPR guidelines) which are in place but strict enforcement is awaited.