Have been bit too quick to reduce and then exit this. I try to maintain less no. of stocks. You have listed all the basic points very well! This can hold some promise still IMO, simply coz of capacity on hand and decent, mostly honest management. Now, camphor prices are actively tracked thanks to Rajeev Jawahar, on this forum. The unknown can be margins, though Oriental Aromatics guidance is good to follow.

Last year, it was severe lockdown and there was an MCA relaxation for Annual Financials publishing. We have something similar even this time, but June 30 is the last I think.

Even though the upcoming quarterly results are going to be record breaking as seen with mangalam organics as well.

The share price is down around 12% from its high of 1320. Currently with an EPS of 120 , stock is trading at a P/E of 9.5. An EPS of 145 after upcoming results seems very likely which can turn the P/E to around 8.0 at current levels.

Any idea , what would be a good price to take an exit?

Well I guess that since the market factors in future assumptions, there seems to be consolidation/decline due to stagnating/downward trending Camphor prices. The management has planned to enter into ther Fragrances and Flavors Vertical through Capex with the excess cash (I think they announced this in the webinar). So I guess if you are holding from lower prices such as mine (450) then i would suggest to hold for a few more quarters, look out for the results and further announcement with regards to new capex and the company’s Cash Utilization (Since the company seems to be holding a lot of cash and March quarter earnings are expected to be awesome), and keep trailing a stop loss of around 15-25% from Highs.

Any new entry at this point seems a bit risky even though the company is trading at single digit valuations in this market but I think since Camphor is a cyclical and commodity chemical, the valuations are kind of justified.

Well I guess the results were a bit below expectations but to be fair, the management did give us hints that the results might not be that great because Raw material Prices increased almost 50% and as we can see Camphor prices have corrected/stagnated. Further I think the new plant was just commissioned in this quarter so there wont be much revenue from it and fixed costs would have been added so I guess that all led to these mixed Final Quarter Results. For June Quarter Im not expecting huge results but i guess by September/December quarter, camphor demand should be at year’s high and also new plant should reach operating efficiency. Further I’m hoping for company’s entry into Flavors and Fragrances Segment leading a good and maybe a stable blended margin. I guess that would be my take on these results but i am definitely vary for 3rd wave because of this delta variant and also a but cautious for another lockdown/slowdown.

Disc. - Got a bit skeptical yesterday when the stock opened at -20% but have decided to hold this for a few more quarters.

Agree completely. From revenue perspective, results were below expectations and it has led to the LC happened yesterday. There are more positives in this company which we should not ignore.

Company’s FCF is at all time high of Rs.22.5 crore

ROCE has increased to 66% which is something commandable

3.Company is sitting with cash of Rs.63 crores

4.Dividend of 40% shows the management wants to improve the investor confidence by rewarding its shareholders.

Triggers to be watched for the next 2-3 quarters

1.Listing on NSE. In the previous con calls, management has told listing on NSE will be considered at appropriate time. In the next con call/AGM, we as investors should raise this again.

2.Aroma/Fragrances business . Need to see how the cash of Rs.63 crores will be utilised for CAPEX. I think they are considering for a land purchase.

Hi @reacharjunr , Varun here.

Tracking your views on kanchi here and on moneycontrol forum as well.

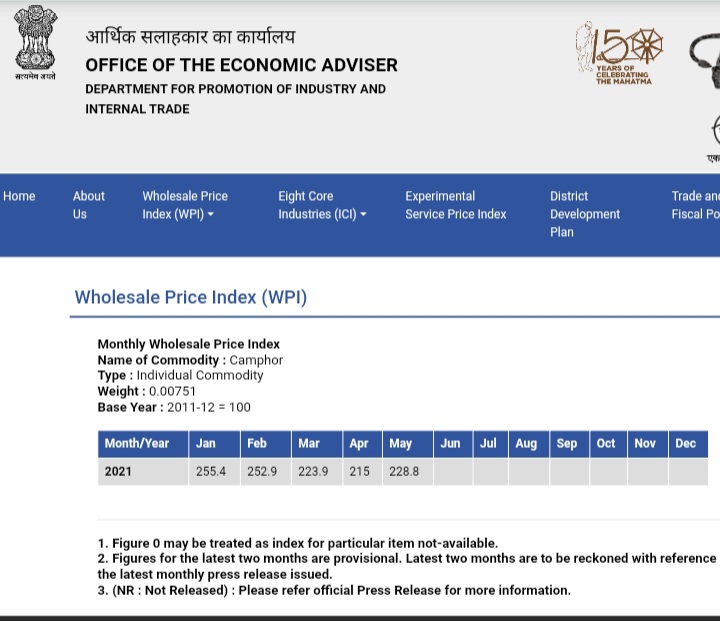

1.) I wanted to ask you about your perspective on camphor prices (on eaindustry.nic.in) with the top line figures for each quarter. Do you feel there is a strong correlation?

If yes, can we form a future outlook based on these numbers?

2.) Is there any major reason for opm and npm to fall qoq basis while mangalam improved on it? I was taken aback because kanchi has managed to always been cost efficient as compared to mangalam.

3.) Considering the Q1 2021 was completely affected due to covid, can the company post better numbers as compared to Q1 2020?

Hey Varun, Ill just share my insights to your questions,

1 - Yes I think that the data points at eaindustry are helpful in predicting results so some extent and are surely co-related. The catch here is that the prices of raw materials play a huge role in determining the bottom line.

2 - This is just my interpretation of the mangalam story. Mangalam is a B2C business whereas Kanchi is a B2B. Mangalam takes some time to process the camphor into retail products and there comes a lag effect. You can see that mangalm’s this quarter results are comparable to Kanchi’s December quarter resuts (OPM and NPM).

3 - I think the Q1 numbers will be very good YoY but will be below average since in last june quarter we faced complete lockdown whereas this jun quarter, there was still a major amount of activity going on comparatively. Sept and Dec quarters are main seasons for Kanchi so lets hope Delta covid doesnt spoil our party.

1.) I completely agree with you that raw material price is major driving factor behind opm and eventually npm as well.

As per the previous annual report also , management has stated that fluctuating raw material prices is a point of concern.

2.) This is a very deep observation which i didnt notice at all. Good one!!

3.) Hoping the same that lockdown effect wont be as severe as last time and constant fear of the next wave might be a killer blow to yoy topline and bottomline growth expectations.

• Even though margins for Q4 were not sustainable due to raw material prices…Do you find any specific reasons for average sales figures? Is the company unable to pass on the price fluctuations to the customers and hence reduced sales?

• As per the latest update on expansion , company has completed it. When do you start expecting its effects to kick in?

I am going to be quite frank here and say that I dont know. As far as I can guess, they have either done some volume growth at falling camphor prices (good), or sold lesser volume at higher prices (bad). That, only management can answer. I hope they hold a call/webinar soon.

As far as the expansion is concerned, the operating costs always start kicking in almost instantaneously, but the revenue growth (Utilization of new capacity to existing levels) takes around 2-6 quarters depending on industry, sometimes even more.