Mainly its the expansion in gross margins that seems to have contributed to profitability growth. How sustainable are these expansion in gross margins that’s the key question ??

-Dhrumesh

Disclosure - Not invested but just started study.

Mainly its the expansion in gross margins that seems to have contributed to profitability growth. How sustainable are these expansion in gross margins that’s the key question ??

-Dhrumesh

Disclosure - Not invested but just started study.

The company is in advantage position their product is superior which can clearly been seen from their working capital management.

They are able to collect the money from debtor within a period of 30 days from last 3 years. secondly they can increase the inventory level for higher period to take the advantage of lower input cost and sell it at higher rate in foreseeable future.

Employee cost includes 3 cr of commission expenses paid to director which is non recurring in nature hence going forward employee cost will be same as Q1 2020

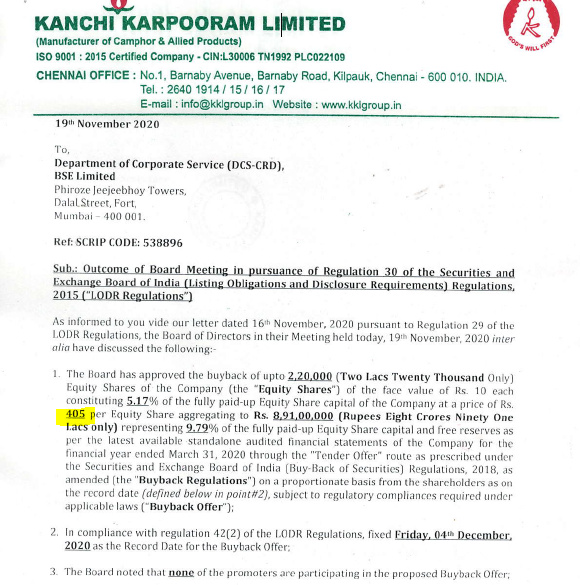

Co planing to offer buyback

Buy back at Rs.405 per share less than CMP. Company buying back 2,20,000 equity shares(5.17%). Not sure whether shareholders will tender at Rs.405. I feel promoters should have announced minimum Rs.650 per share for buy back.

@reacharjunr is recording of this webinar available ? Kindly share the link if it’s available.

Meeting recording is not available. Meeting was through Zoom platform.

Crisil has once again rated company in non cooperating category. Awaiting views from learned members.

Company having 50 cr cash in books with zero debt why will they entertain rating agency.

Lot of information gets passed on to competitor through this rating agency which may cause such small company to stay away from it.

Result of mangalam organics is out. Clear visibility of rise in camphor price in revenue.

Thinking of kanchi karpooram result will be better then mangalam organics as Q2 of kanchi was better then mangalam, company will be holding lower cost inventory and one time director commission expenses of approx 3 cr will not be reflected in Q3.

Disc-invested

Just my general Perspective, May be too optimistic

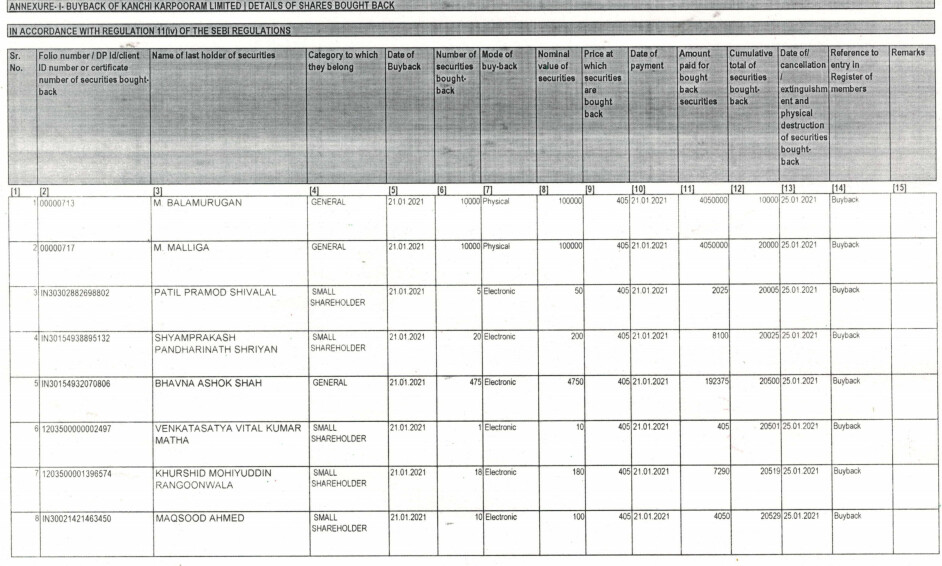

As we can see, the buyback shares pretty much flopped.

Now, Company is sitting with 55 cr in cash as per the Sep 2020 BS and 54 cr post buyback, since around 80 odd lakhs was used in the buyback process.

What I think would be the best next thing would be to give another buyback at 700 per share (a TTM PE of around 11 which is somewhat conservative for a company with such good profitability even in the March 20 FY where in balance sheet they have mentioned that raw materials are getting expensive and camphor selling prices are getting lower).

Now, if they use 50cr for the buyback, they can get around 7.14 lakh shares and clear them off. this will lead to a total equity base of 32 lakhs and promoter holding around 20 lakh shares which translates to 62.5% of the equity.

As we can see from Q2 results and Mangalam results and commentary, the camphor prices are at very high rates and also kanchi has expanded capacity, so a net profit of around 35-40 Cr for FY 21 is conservative and highly probable. (H1 net Profit stands at 24cr). This would lead to an EPS, If the buyback takes place, at around 100-114 rs (35-40CR PAT divided by 32 lakh shares). With a PE of 10, that translates to 1000rs per share.

If the buyback doesnt take place which is quite probable, the FY21 expected PAT of around 35-40 cr should also give a boost to both EPS expansion and PE expansion which would also lead to a good market cap of 400-500cr, a Market price of 1000 rs. Further, the company will still have the previous 50cr cash and another 10cr cash from second half. They definetly will have to either go for some aggressive capex, into another field/vertical maybe since backward integration is not useful, or declare a special dividend of maybe 100rs (40 cr).

I think these are just too optimistic views and I am just assuming one of these might happen. I have never talked to any company management, visited the plant/company or have heard any rumors/inside info regarding the co.

Disc : Invested around 8-10% of my portfolio

To my surprise , few shareholders have participated in buy back at Rs.405 which is almost 20% discount to CMP. Company has extinguished 20,529 equity shares representing 0.47% of Paid up capital. Post buy back paid up capital is Rs.4,34,38,910 (4.34 crores).

Nicely analyzed! The only bit optimistic part might be the PE multiple of ~10. These kind of commodity companies usually trade at ~7. Though, yes, it might bump up to double-digits for a while in anticipation of growth! This is my only LT holding, exactly 3 years now. It has given me CAGR of 50%  I have traded in it opportunistically, most of my initial buy was ~250 share price.

I have traded in it opportunistically, most of my initial buy was ~250 share price.

Immediate trigger will be record Camphor margins, then the 4x expansion in next few quarters (considering Camphor and also other materials as a group). The PE expansion will happen only when their exports scale up, they manage medicinal-quality supplies and eventually realize their plans to transform somewhat into Oriental Aromatics, by spending the huge reserves to get into allied streams, such as fragrances and flavors etc. This might be more than few quarters.

Overall management has shown good profitability and money-savviness even in the difficult times and tough business. Their actions do look to be trustworthy also. Can bet on them to manage well in the future for the eventual PE expansion.

One of the best quarter for Kanchi. Its party time. Cheer to all investors.

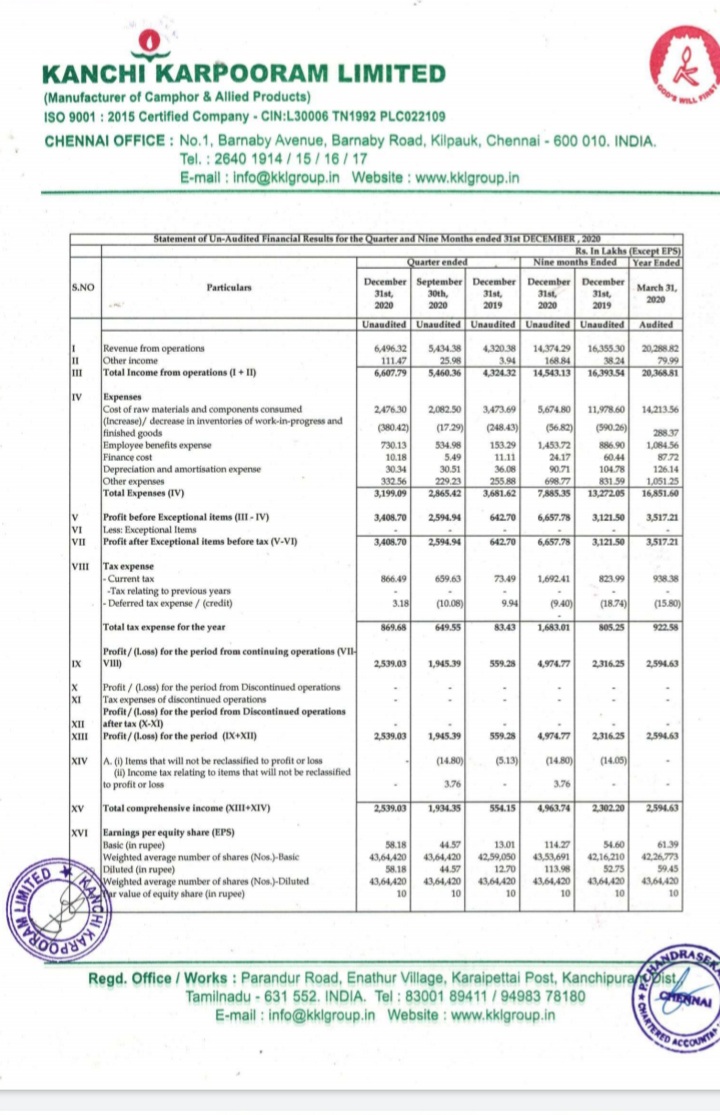

Q3 FY20-21 results summary

Revenue at INR 64.96 crores up by 50% YoY basis

PBT at INR 34.08 crores up by 430% YoY basis

PAT at INR 25.39 crores up by 353% YoY basis

EPS at INR 58.18 up by 347% YoY basis

Nine months FY 20-21 results summary (YoY comparison)

Revenue at INR 143.74 crores down by 12% may be due to camphor price increase was realised from Q2

PBT at INR 66.57 crores up by 113%

PAT at INR 49.74 crores up by 114%

EPS at INR 114.27 up by 109%

This deserves a PE of 15 times I believe since the growth is visible. Also Camphor industry in bullish mode.

Yes results are definitely eye opening. With its 5x capex kicking in this quarter I think sales will marginally increase over the next few quarters. Initially, the depreciation for the new facility will eat away the margins, maybe not so much, but the PAT margin (35% or so this quarter) should slowly come down to 22-25% and show consistency. I guess once that happens, the PE expansion might take place to 12-15 otherwise commodity chemicals/products such as camphor usually get a PE of 7-9.

Also it would be a great help if the company holds concall/ makes the Annual report more transparent as to future plans and industry outlook.

One thing I would like to know is that since the company has increased capacities of intermediates and derivatives significantly, is it planning to dive deeper into camphor derivative market since that would maybe lead to a high sales growth and margin expansion (probably not from current levels).

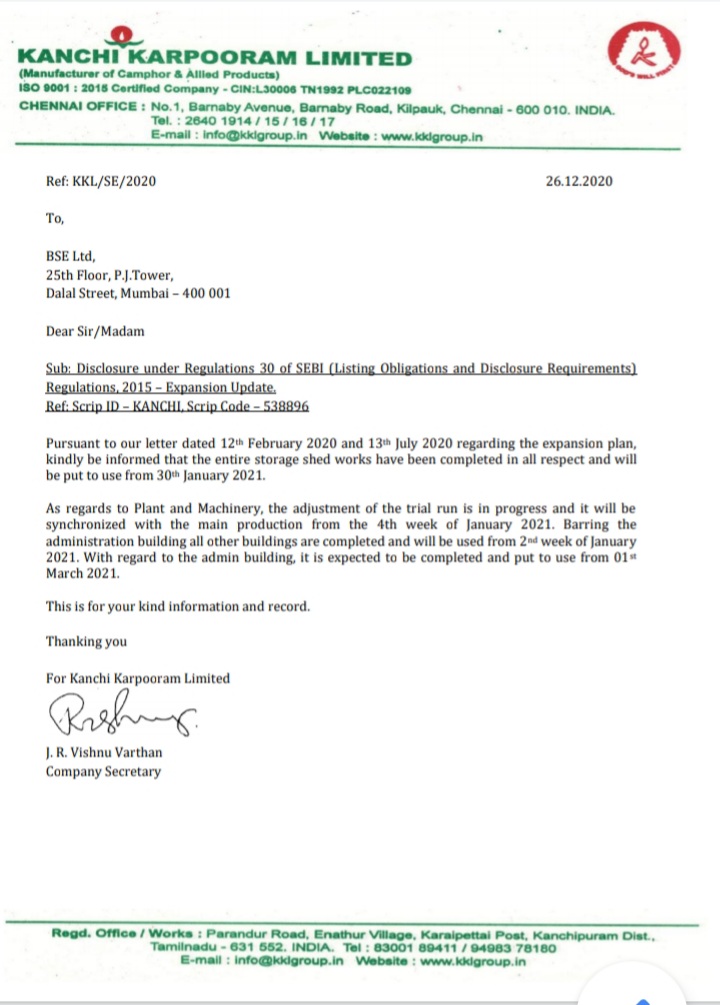

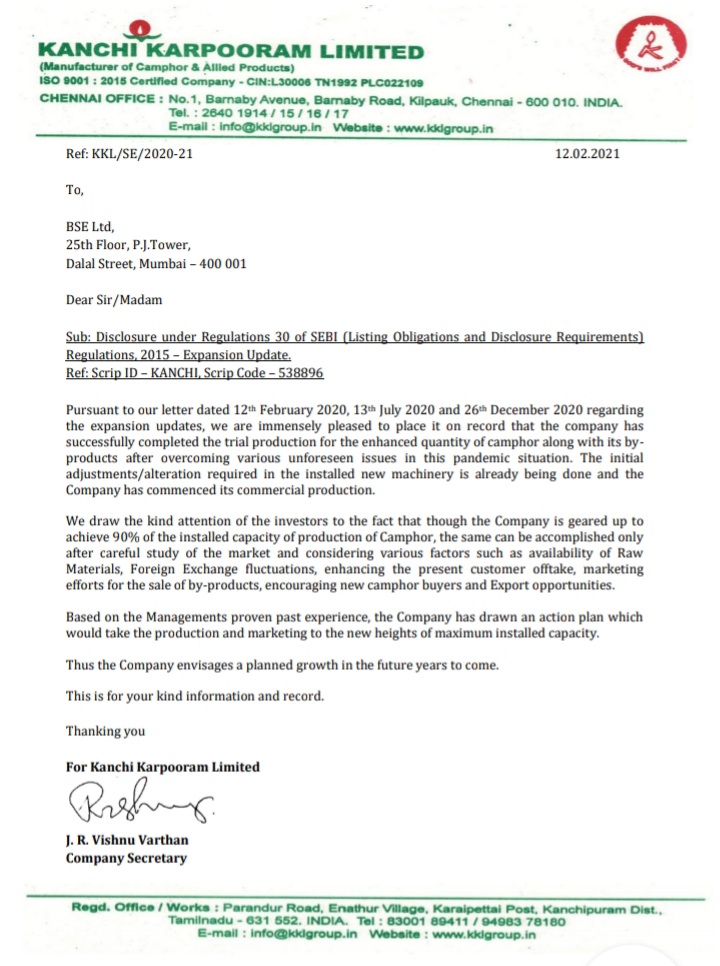

Expansion update: Good times ahead? Good to note that management has drawn an action plan. I request all investors of Kanchi to write a mail to CS to conduct earnings con call for better knowledge of investors.

Yes the company seems enthusiastic in the press release and its definitely a positive news.

A point regarding shareholding pattern that i noticed was that Ramkala Kanodia (the highest individual shareholder with 2.5% equity in dec 20 pattern) has sold off close to 0.53% equity on 7 jan 21 and 0.56% on 7 jan 21. Found it on moneycontrol under Bulk deals.

This is not a concerning/alarming news and neither should it affect our outlook of the company, it is just a point that i noticed today just while looking at SAST and bulk deals sections.

Quant Mutual Fund sold Kanchi 68,200 at Rs 676.85.

Yes. Correct. Also there were two more bulk deals in 2021. But considering the future growth of the company, this should not be considered as negative. I think best is yet to come from Kanchi.

Company is planning for a webinar on Monday, Feb 22. One needs to send an email to secretarial@kklgroup.in along with queries by Feb 19.