Finally got expansion clearance from EC. Now the production will be live from 1 april 2020 onwards will be able to see good jump in top and bottom line with 5x expansion plan. With August to January always remains good for camphor industry this production expansion will help them achieve new milestone.

Can’t help but recall that there used to be a time when environmental clearance of even lesser known companies used to be greeted with upper circuits. Now the markets are more cynical and wants to wait till the execution and profitability are proven. More like how we would handover our hard earned money to someone in real life - after lot of due diligence.

Searching for price trend of Camphor lead to this article on gum rosin, the raw material used for production. It appears @Jinal is quite right and I also see a cyclical trend in the margins of Kanchi. Mangalam does not show this trend that much, since maybe not directly dependent on gum rosin. Apparently harvesting in China (tapping Pine trees) happens only after the rainy season because at that time labor works on farms for sowing crops. So August to January seems to be the season of supplies coming to the market.

The trend seems to be that raw-material is getting cheaper this season and the end product is holding firm. Good for both Kanchi and Mangalam. The company in the link is an old US firm dealing in plant derived products (aromatics mainly). The article only focuses on chinese supply.

Going through the chronology of the article, it appears the reason fortunes of both Kanchi and Mangalam took off only after November 2017 because of closure of big Camphor producer in china, due to raw material issue it says.

NOTE - The link and much of this info has already been shared in the thread of Mangalam organics, a long time ago by phreakv6.

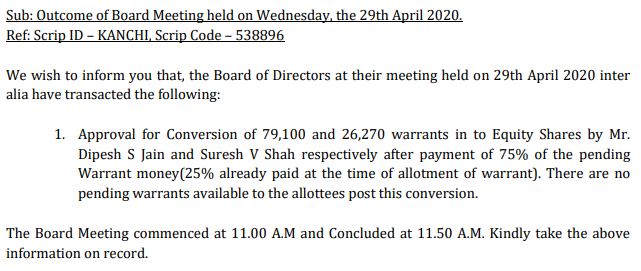

There could be oversupply issues but larger capacity means lower overall costs, important for commodity product. Though MOL is smarter to go the branding and derivatives way. Kanchi promoter is investing (in 2018) directly in the company through warrants @ 360 (for 8 Cr)

MOL promoter has recent past years increased stake by 2.3% while Kanchi promoter has increased by 1.5%.

Disc: Invested in both since 3 years, 15% of portfolio. Mangalam is 2x of Kanchi.

Hi @vikas_sinha, are you still tracking this? The price has corrected in line with the market. What caught my attention is :

(i) People are buying it because of its antibacterial properties. Observed it in last few days in two super shops.

(ii) The promoter - Mr Suresh Shah - is buying from open market, although the quantity is minuscule. He has bought 741 shares on 13th March and 4224 shares on 16th & 17th March.

Numbers wise it seems fantastic - both ROE and ROCE 50+, PE of 2.68 and 3 years sales CAGR of 49%. Its a steal…! Or am I missing something?

Do you still hold Mangalam Organics? How do you compare MOL with Kanchi? Pls do share your views.

Still holding, no change made, sold off Mangalam (promoters are focused very much on share prices, bad omen). Yes, it did occur that camphor might sell more considering it is treated as an aerial purifier in India. Kanchi I believe always commanded a premium over MOL, which most attribute to the better metrics on most counts as you observe.

They are very much into commenting on share value in interactions and buying own shares, Q3 was made worse than usual by the exceptional item accounting, I think it was for reason of easing promoter buying.

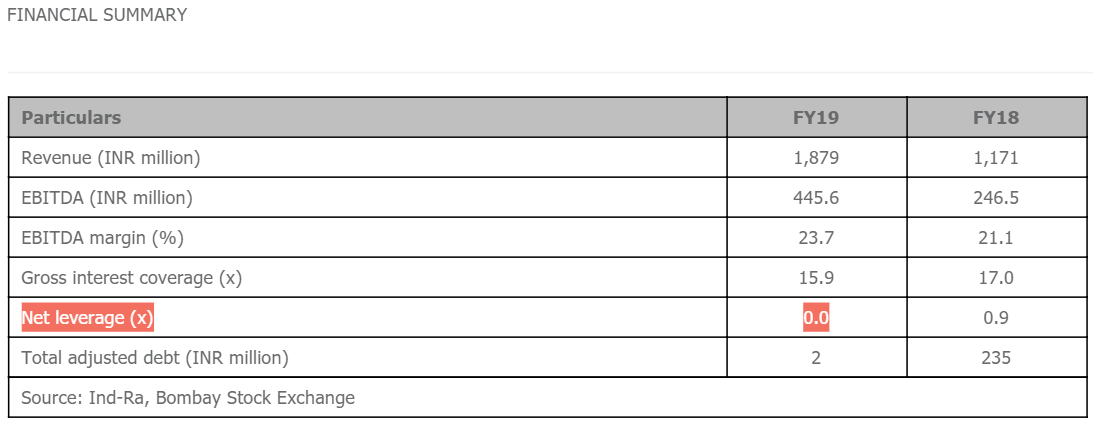

Its rating has been given not cooperating. Rating agencies have cautioned investor and lender.

From 2017 or 2018 rating agencies are cautioning investors and lenders and from that time onwards its inventories as well as trade receivables have almost doubled or more.

Please read carefully, the caution is while using the rating (since it is based on insufficient info) and not for the company, and you are then using the rating to form an opinion of the company! They have almost zero debt and this is normal when they do not have plans to get more debt. This is from the most recent published rating report, typical boiler-plate wording, very often used. This is normal when company does not want to spend time on something it has no use of.

Sales have increased 4x since 2017 and fixed-assets 10x since 2016, I too find all this very troubling indeed! Will try to find out more about what exactly is going wrong with this company! Thanks!

Am currently studying the camphor markets - its relevance in air pollution control and other medical factors

I just had a question regarding the camphor industry : since Kanchi Karpooram | Oriental Aromatica | Mangalam Organics are kinda on a same boat with Managalam Organics having a retail brand play. What are your views on Kanchi? if possible Oriental too? I feel Kanchi is cyclical due to its diversification and have to target multiple range of stream that leads them to only be a partial player isn’t it? or is my understanding wrong here?

I have been following Oriental aromatics since 2019 and due to good results - it has shown some push.

Would like to know your views about the industry & relatively comparison between Kanchi & Mangalam & in the middle Oriental.

Thanks for your work and effort - i appreciate (kindly delete this post if its irrelevant)

If you can share me a good read about this industry - it would be great

Disc : Am studying and researching about the various factory and components of the industry & its level of affect to micro & macro economic factors.

I do not follow Oriental, it might be much more than Camphor, and also much larger than the Camphor players Kanchi and ManOrg. Camphor players have some diversity since Camphor is one of the pine/turpentine oil based derivatives (aromatics) but looks like heavy dependence of current growth is on Camphor, due to shutdown of large player in China.

I only have Kanchi now, since together with Mangalam they had grown to almost 10% of PF (while other stocks were not doing that good, perhaps!) which is too much for a single commodity, not safe without depth knowledge, so there was some pressure to sell at least one!

ManOrg retail I do not give much importance, it can have costs due to marketing/channel push issues. Kanchi I favored because of relatively steady performance and superior numbers on most metrics. Growth is supposed to be 4x in coming quarters, and we hear about exports to developed markets also (medical quality camphor may be possible, ManOrg has some plans definitely).

Looking at Oriental performance now I understand why Kanchi also saw huge jump last few days! thanks for sharing!

I really do not know much, these 2 were buys when I had almost no depth understanding, thankfully the reason for buying them i.e. performance, continued, or at least no big crash, they are very cheap anyway. And I did not raise the risk by buying too much in their bubble phase.

The share price of Kanchi has gone up by more than 50% in the last 5 days. This has resulted in its weightage going higher in my portfolio than my comfort level. I have sold half of my Kanchi share & purchased Mangalam Organics to reduce my risk. The results for 19-20 have still to come for Kanchi while Mangalam has done well. Mr. R.K. Damani has also purchased Mangalam if news item is correct.

Yes, me too, sold off 25% of holdings in Kanchi in the past week (transaction worth 1% of PF), shocked by sudden optimism when TN is a heavily affected by COVID and they have announced earlier of some weeks lost in Q1, and also even when still no result for Q4 FY20!

And a 6 months+ delay with expansion!

Maybe markets are giving marks for disclosure?

Maybe people find this a good time to get in and wait for 6-9 months for the 4x jump later.

Delay from June to December for plant construction:

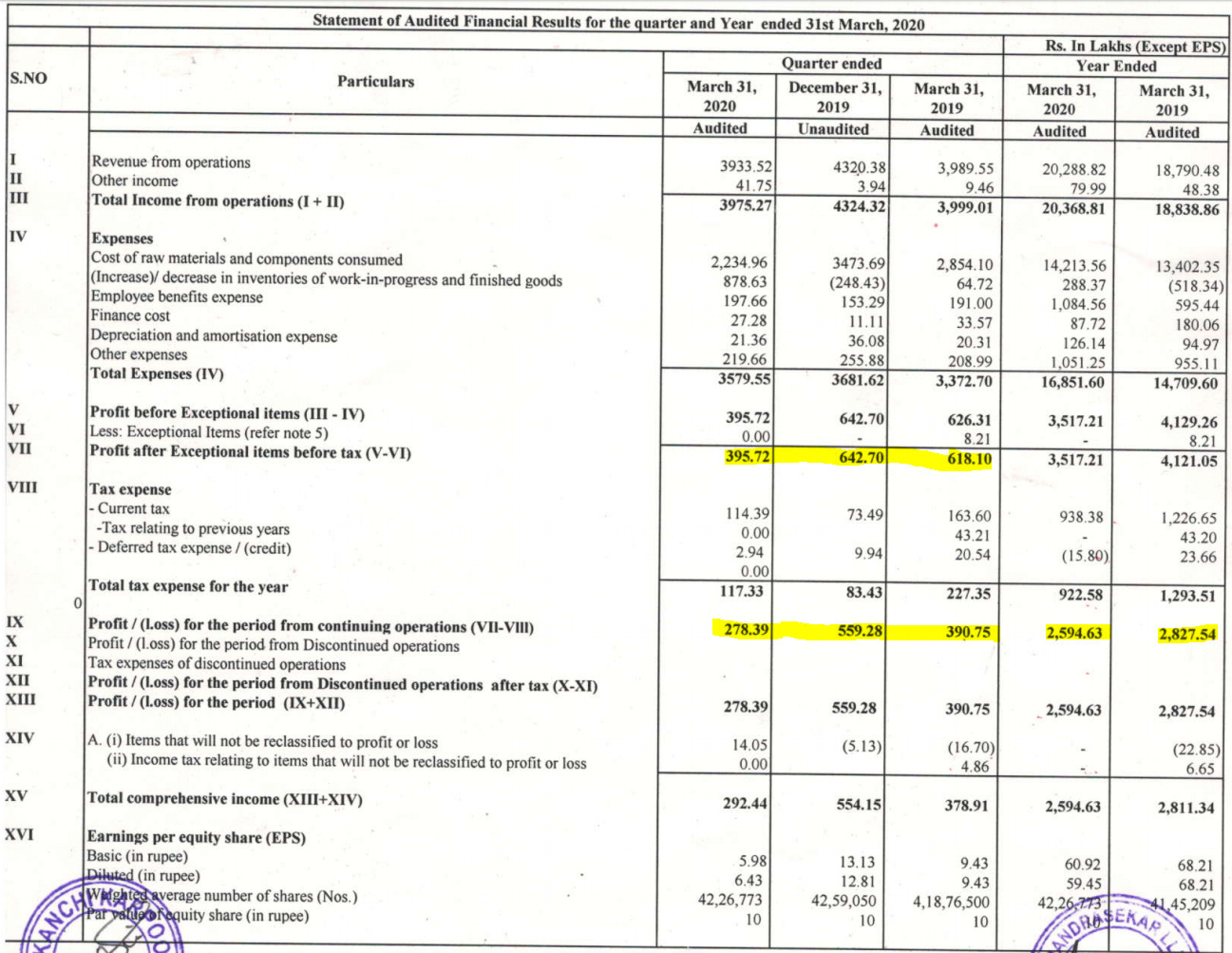

Q4 FY20 Results already announced yesterday, comparable or better than the peer ManOrg (comparing PBT performance YoY basis of both) except margins seem to have fallen much. Not much surprises. Rs 1 dividend given. The huge rally of past few weeks was the surprise.

1.Capacity will be increased to 550 mt per month after expansion

2.Company has plans for more exports after expansion.

3.Trial production in January 2021. Full production expected by April 2021 considering no second wave of Covid-19.

4.Guidance for topline after expansion for FY 2020-21 is INR 270 crores.

5.Company plans to add new products in Aromatics, Aroma

6.Company is not selling any branded camphor only bulk camphor

7.Company intends to retain its employees strength 140-160. Contract employees would be hired on need based.

8.As per management, backward integration is not economically viable.

9.CWIP for 2019-20: major investment in building, roads, sheds apart from machinery investment.

10.As per management, most of their clients are from unorganised sector since camphor is in unorganised sector

11.Company intends to supply products to flavour industry.

12.Company is concentrating currently on local market. After expansion company will concentrate on increasing exports.

13.Margins expected after expansion is 12-15%.

14.Camphor price is market driven neither cyclical or structural.

Unanswered queries

1.Major customers?

2.Current camphor price?

3.Long term contracts with customers?

4. current proportion of exports and domestic sales?

NB: Company plans to have more investor webinars in near future to update shareholders.

Other learned members who attended webinar can also add your points