Hello all, current holdco discount is above 85% by my calculations. Why does screener ratio show P/B as 1.8 when it actually is 0.14 by my calculations?

3 Likes

Your calculation of 0.14 is based on share price, while book value is based on asset/investment at historical (if not revalued periodically) cost.

Had been reading different people’s comments here and have noticed a pattern, the hold co. discount has been increasing for the past many years. Everyone is investing in the hope for hold co. to catch up with reasonable discount but it is not doing so. Is the hold co. normalising(new normal) this much of discount?

disc.- invested recently

2 Likes

3 Likes

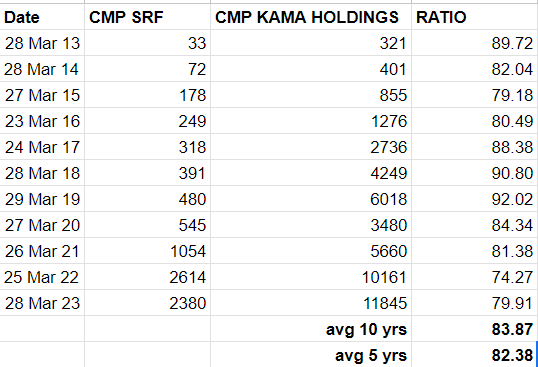

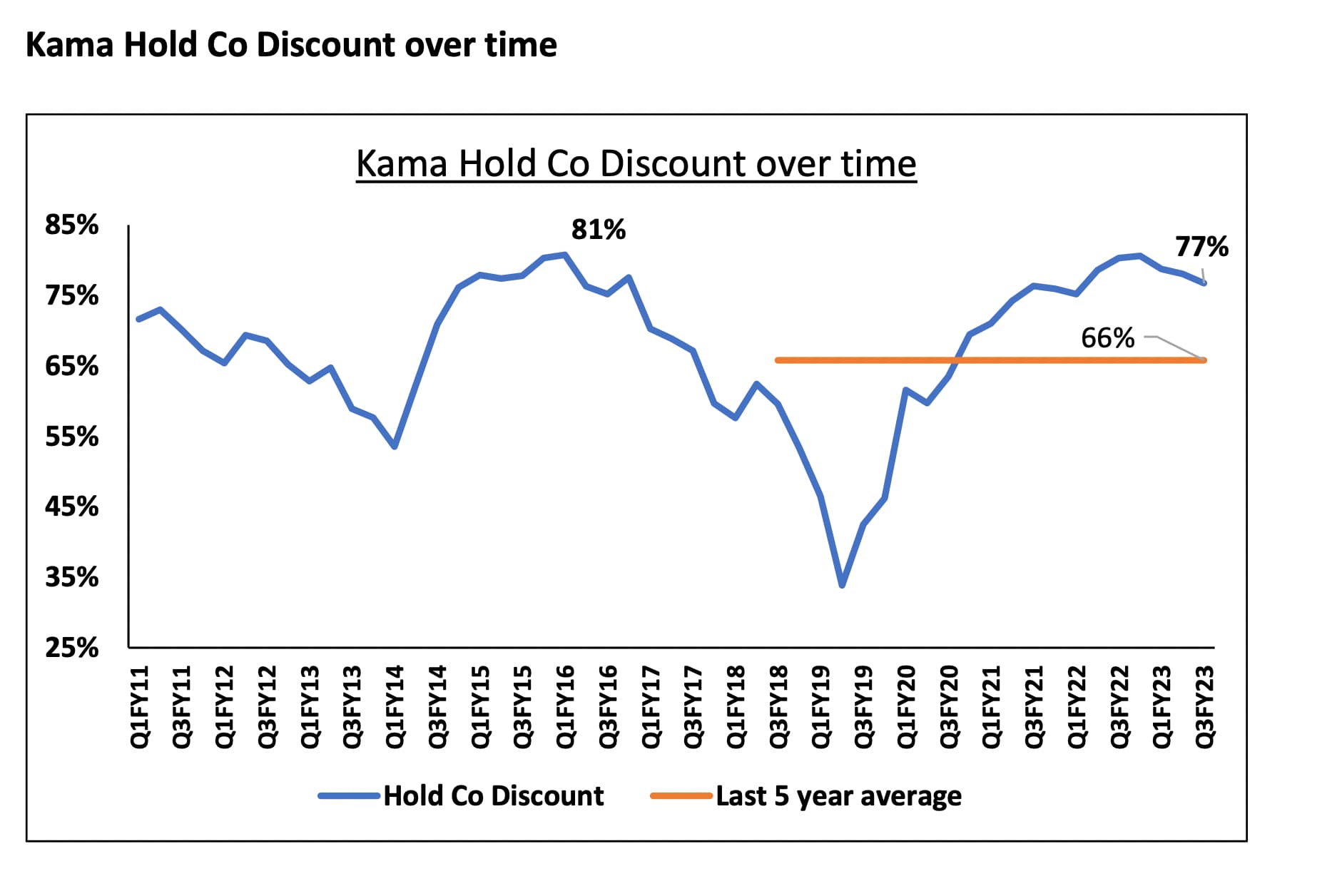

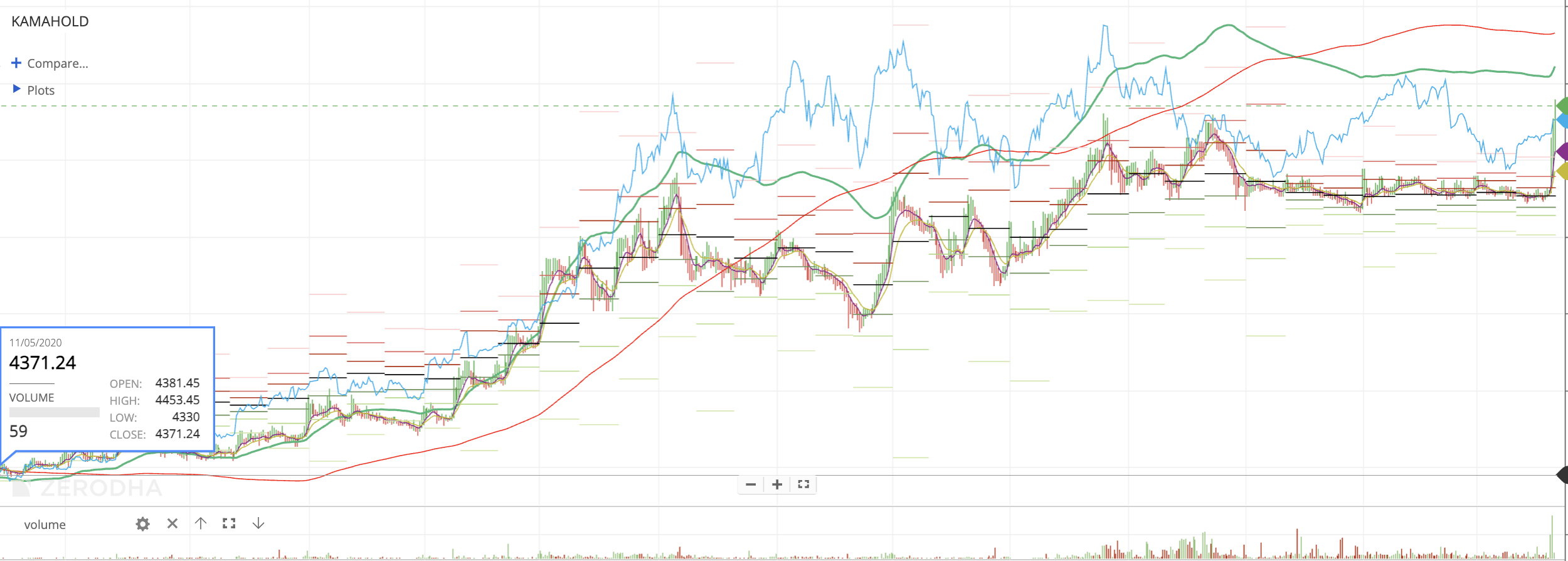

Take across time frames and then check ![]()

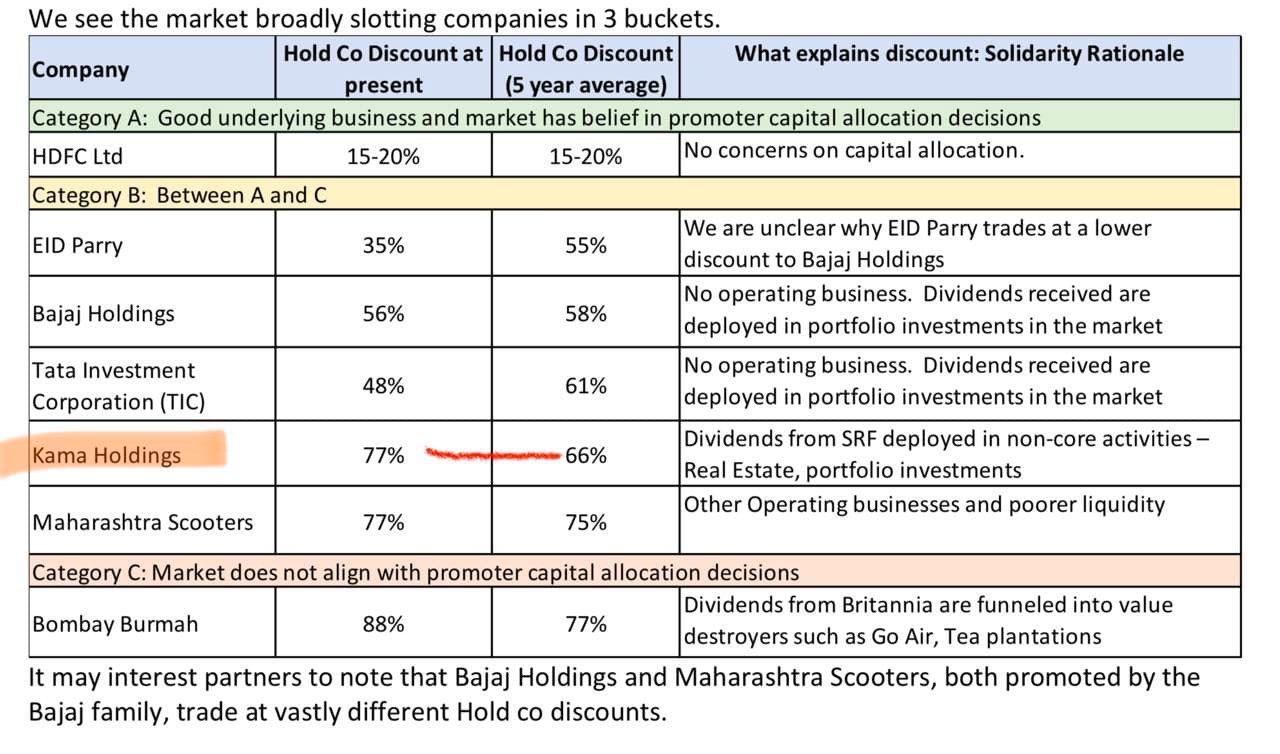

Discount in the past went to as low as 35% in Q3FY19.

Source: solidarity.

Disc: Top 3 allocation in family PF. No reco to buy or sell

21 Likes

Ohh. I think I was miscalculating it earlier. Thanks for the data

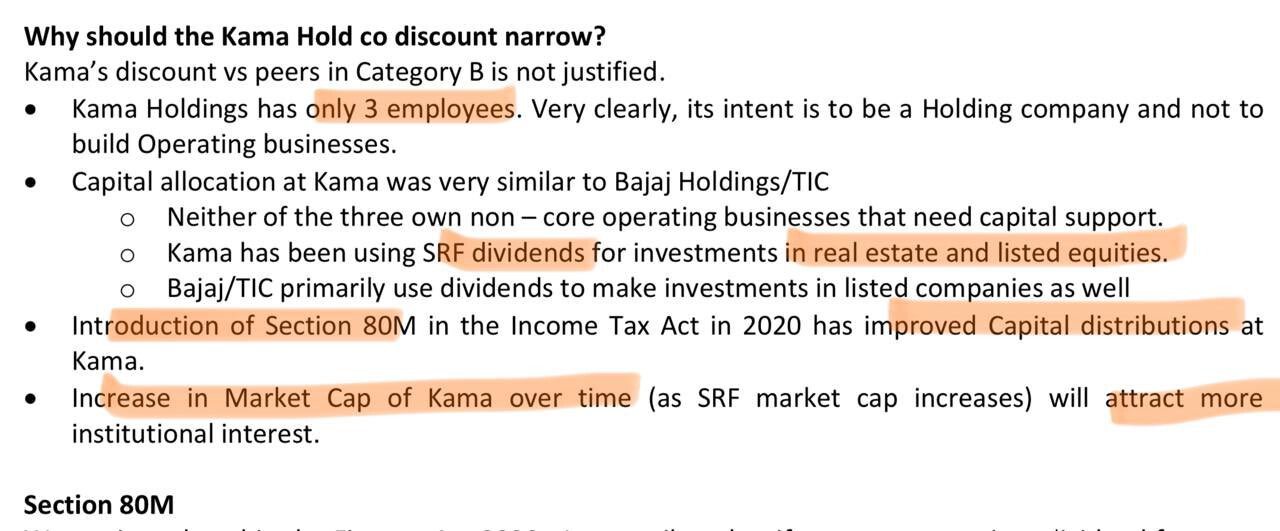

While it is true the Holdco discount is higher vs the historical discount, but I think it is also important to look at SRF’s valuation. Prior to Covid, SRF had a PE between 20-25x, while it is currently at 30x+. It is possible Kama Holdings is discounting for the risk of derating at SRF. While I haven’t studied SRF but I think would need to get a good understanding of SRF before taking a bet on Kama.

1 Like

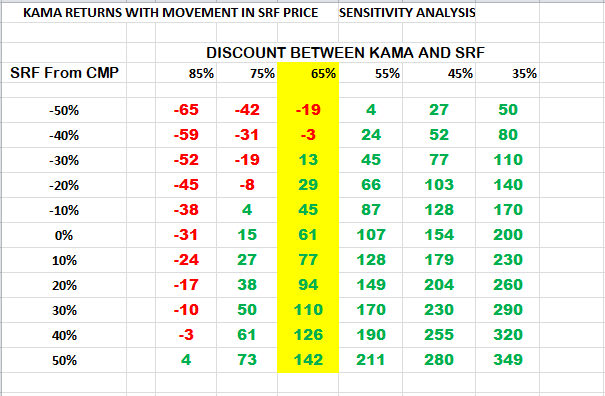

Hi Guys,

Just tried to do a sensitivity analysis on KAMA

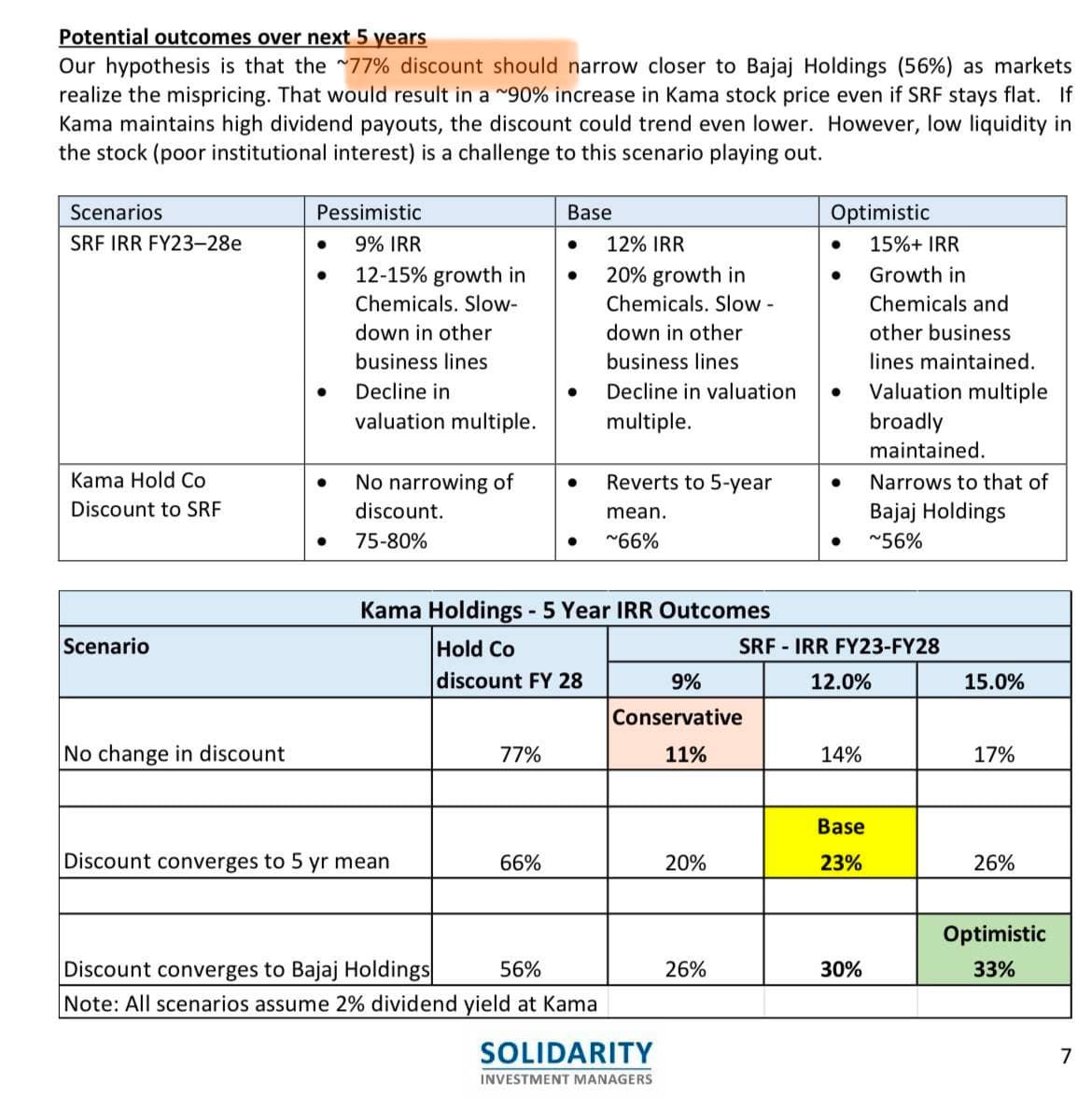

One very Important point here is even if SRF falls by a 50% and the valuation gap goes back to the mean difference of 67% then the fall is going to be between a 19% to 23%.

SRF is trading at a premium valuation than its historical mean valuations across different parameters but instead of price correction the possibility of time correction is high for earnings to catch up with valuations unless there is some business related issue.

Even with SRF giving 0% returns if the difference goes back to mean we make close to 60%

Risk reward is favorable and we also have some dividend yield 1.4% i think

Please let me know if any calculation in the above excel is wrong

2 Likes

Underlying biz has changed though. See capital employed in chemicals what % of profits is coming from chemicals now. 80% profits come from chemicals now. Even 5 years ago it was 33% from chemicals. The other two profit streams are much more volatile & cyclical. So imo past valuation is useful but an incomplete lens from which to view the company

If earning can compound 20-25% for few years then imo valuation can sustain it is not completely out of whack specially given the new verticals it is entering in like FP & new age FP

disc : have a small position

8 Likes

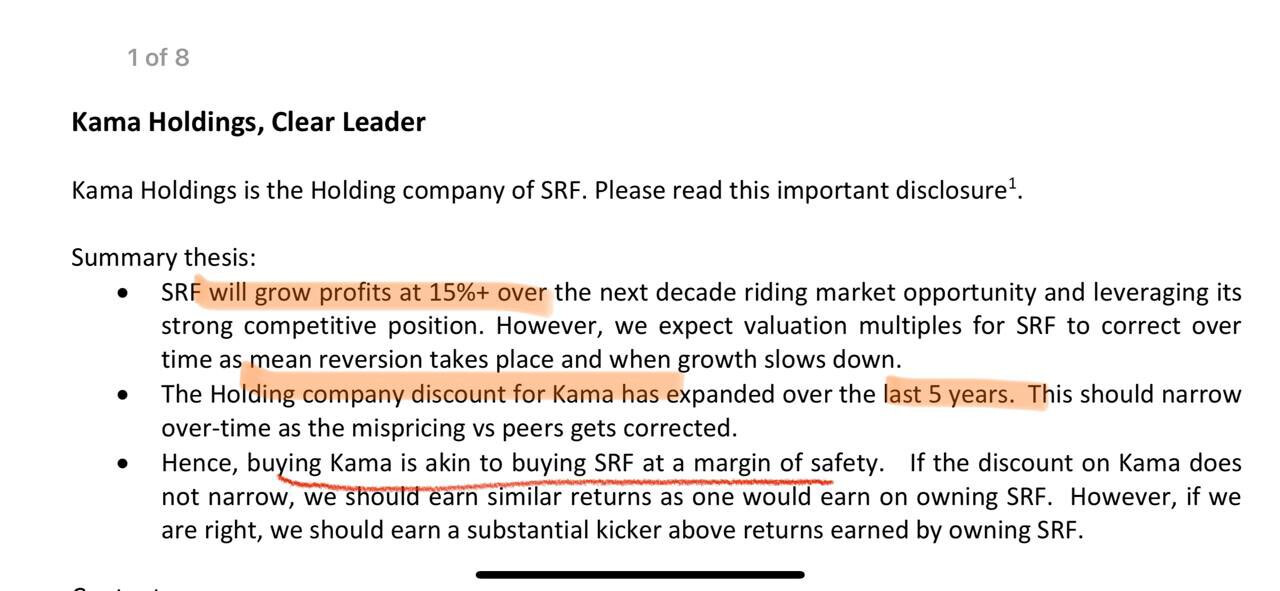

Solidarity shared some further insights on Kama Holdings -

Some pointer’s from the document I would like to highlight :

https://twitter.com/Lakshayy_99/status/1658149238436667392

Comparison with other holding companies

If anyone want’s to go through the entire document then here it is :

Disc : Invested , no reco !

17 Likes

KAMA Holdings

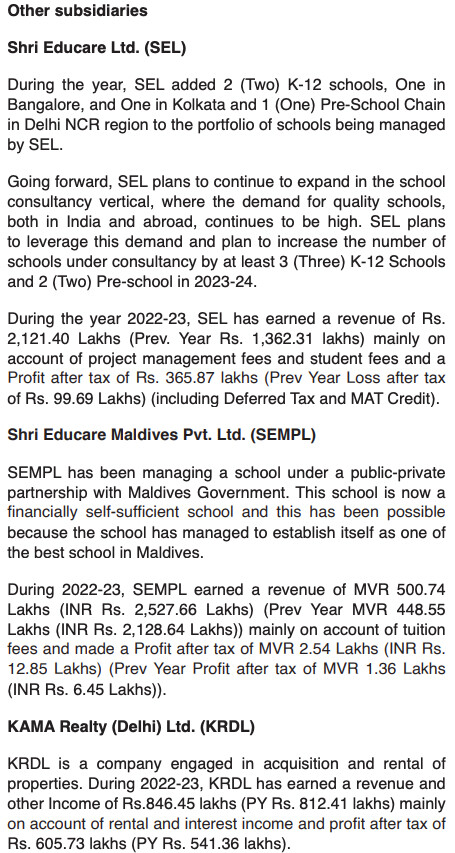

- Shri Educare

- Shri Educare Maldives

- KAMA Realty Delhi

- SRF Transnational Holdings (Nbfc)

- KAMA Real Estate Holdings LLP

Almost every other subsidiaries have made profit and incresed that number Vs Previous Years.

They have reduced stake in SRF, last year they sold about 6Lakhs shares. If they continue to reduce stake in SRF then isn’t against the thesis for which everyone is invested in Kama Holding?

4 Likes

They sold 6L shares (worth 146cr) in 2Q FY22-23 and used the amount to do a buyback (at 14500) and extinguished 34500 shares (worth 50cr). On this they paid buyback tax (10cr).

Also they redeemed non-cumulative pref shares of promoters worth 14cr to decrease subordinated liabilities. Rest they moved to reserves.

The buyback actually led to promoter holding increasing beyond 75% to 75.05% so they will have to reduce it.

My thesis is also to use KAMA as a proxy for SRF with a margin of safety. Hope this stake-sale/buyback combination will lead to discount narrowing

Disclosure - Invested (small position), not a recommendation.

4 Likes

Hi, @Worldlywiseinvestors, any specific trigger which led to the holdco discount drop to 35% in FY19? it didnt sustain and came back… not sure what would have led to it. Maybe just that Kama price appreciated faster in comparison to SRF

2 Likes

debt to equity of Kama has increased …is it an antithesis pointer or a reason to worry?

1 Like

discount has reduced significantly in last few days, any trigger? only when I got out last week ![]()

blue line - SRF

disclosure: no current holding

1 Like

I also made the same mistake. Got out at 12695 at pre market 2 days back!! Then got to know that kama holdings is declaring bonus shares!!

1 Like

As discount reduces, any views on whether one should look at exiting Kama Holdings and enter SRF. Any discount threshold to be considered?

If you like srf at current valuations, I believe kama holdings remains a better bet for long term.

The management is honest and shares rewards with shareholders, so a discount of 65 percent(reduced from 70 perc) is not warranted either.

3 Likes