Is moat of my businesses getting stronger or weaker? And what about valuations?

Let’s find out,

1) DHP India Ltd

Management realised that doing business in India have no future due to absence of any advantages against competitors, so very wisely they decided to find entire client base to western developed world, where they had some competitive advantages against local manufacturers such as,

a. Low labour cost

b. Low power cost

c. Overall low manufacturing cost

d. Over the time accumulated approval & certifications from many countries

True capitalist always try to find ways to get away from competition, they have done exactly the same, but looking at their return ratios definitely sooner or later competitors will copy them. It will happen one day, capitalism is brutal, it always happens.

For now and next few years I think they are safe, and market is big and growing, so the moat seem to be intact.

We will have to review the business at least every year, and get clues from growth rate, margin’s, credit period to customer, management guidance etc., to keep tab on the situation.

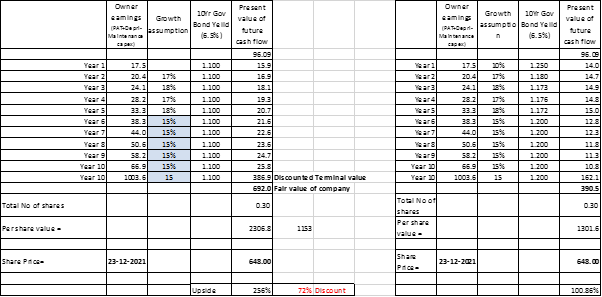

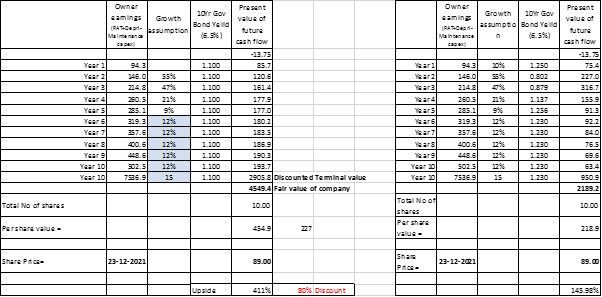

What is value of this business from my perspective –

It is generating approx. 100cr revenue and 16cr owner’s earnings from 14.90cr of plant machinery, recently plant & machinery increased by 7cr which means, at increased capacity they can produce the revenue of around 150cr and owners earnings of 30-35cr in next 3-4 years (assumption).

They will accumulate around 140 to 180cr in cash in balance sheet by then.

As per my calculations present fair value of business is around Rs. 2300 per share and as I expect at least 25% CAGR in all my investments, my entry price should be at least 20% below Rs 1300 per share i.e. Rs1040 (with margin of safety).

This company available at deep discount to its fair value.

As long as moat seems intact and business is growing I have no plans to sell, unless management do anything stupid with the pilling cash or it becomes too much overvalued.

2) Vipul Organics

This business has no real moat, as technology is freely available.

Competitive advantage comes from strict gov regulations on pollution control,

As this industry is dominated by small unorganized players, gov regulations gave tailwind to few big players who can comply with regulations due to size & scale of their business allows the feasibility.

Eventually few players present in low cost Asian and other low cost countries will gain most of the world market share over the time, so these few players will keep on growing as long as market don’t saturate, and they start competing with each other.

Vipul organics was just above the threshold of feasibility to comply with norms at the right time, so survived.

I invested in it based on sector tailwind, trading to manufacturing shift, backward integration and operating leverage.

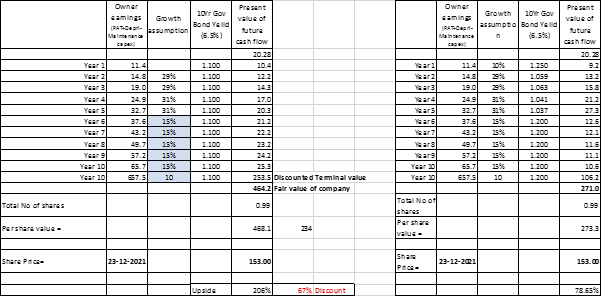

What is value of this business from my perspective –

In FY 19 their revenue was 90cr which was around 50% manufacturing & trading each, then they increased manufacturing capacity 6 time present, means now they can produce (45cr*6) 270cr revenue from manufacturing alone.

As the mix shifting from trading to manufacturing, margins will increase considerably. It is seating on huge operating leverage.

Owner’s earning will be around 30cr in FY26.

As long as tailwind is present and management is executing well, I want to stay invested.

Clear sell if too much overvalued.

This is available at deep discount.

3) KG Petrochem Limited

The management of this company believes in working in value added products.

Their textile division is growing at healthy rate from long time.

As they work in value added products they have price increase pass on powers with customers. They also get gov incentives for exporting textile products.

They recently they forayed into technical textile division (Artificial leather like what Mayur Uniquoter Ltd does), initially for last 2 years they couldn’t stabilize this division, but management is capable and I believe they will do it.

As they operate in value added products and management always look to keep the moat intact, as an investor I feel safe.

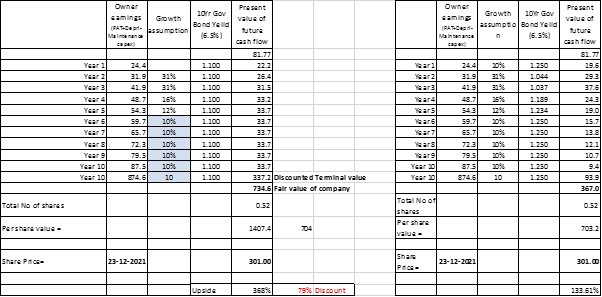

What is value of this business from my perspective –

Presently market is giving them valuation of textile division only, considering problems in stabilizing or scaling up of technical textile division.

I believe management will eventually figure out the issues and scale up the technical textile division.

Textile division at 67% capacity utilization

Technical textile division at 32% capacity utilization

BPT margin’s –

Textile div 10%

Technical textile div 10% (this is conservative)

Management has guided for 550cr revenue at full utilization and I consider it to happen in 4 to 5 years. It will throw owners earnings at around 55cr.

This company also available at deep discount.

I didn’t like the decision of management to go for big artificial leather capex without first understanding the facts, they should have started small and eventually increase capacity.

Management has also mentioned for mega capex after 2-3years, so as long as I believe management is walking the right path at right speed, I want to stay invested.

4) Time Technoplast Ltd.

Their industrial packaging business has a stable customer base and growing business, but can be clearly seen from few years under competitive pressure.

Their composite business has a great potential to grow rapidly, it also has good margins and less competition.

Moat is not that great but addition of value added products and valuations do provide me comfort.

What is value of this business from my perspective –

Management has guided to improve working capital which will improve ROCE profile in the future.

They are generating around 200cr owners earnings now and in FY26 I expect them to earn around 400cr owners earnings.

I believe 250 per share is fail value of company, and to get 25% CAGR returns I need to invest at 110 per share.

Again this is a deep value bet.

5) Satia Industries Ltd

Excellent management which can convert any adversity into opportunity, and constantly on the endeavour to improve efficiency.

Whether it is Power, water, pollution, raw material, pulping etc they didn’t just solve these problems, they make lot of money by addressing intelligent solution.

They are operating at margins of 22-23% and I believe they can go to 28% OPM at full capacity utilization.

Moat here is management itself who can sail the boat safely, another moat is they are low cost producers, even if they don’t have pricing power, market share shifting to them from weak players.

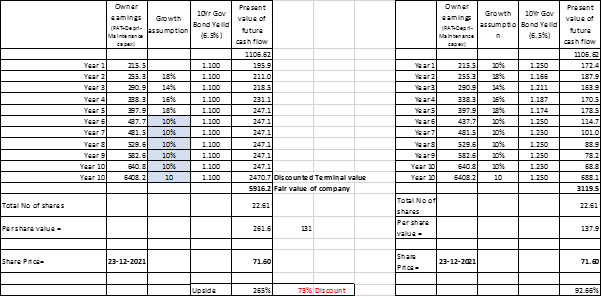

What is value of this business from my perspective –

Recently they have gone for big capex which will help them generate total revenue of around 1500cr and PAT of 250cr after 3 years.

It is available at deep discount.

I think this company will keep on growing for long long time, obviously stock price will grow non-linearly.

These all may be small companies but I think they are great investments.

I don’t expect them to give linear returns, most of them operate in cyclical industries, patience is a key here, let the management execute, and price will follow eventually.

Disc: Not a SEBI registered advisor, do not invest on my conviction, do your homework, do your own valuations and then take decision.

This data posting here for my own future reference, views & counter views invited.