@Bimal_Purohit

Thanks for writting!!!

Globaly paper industry is matured in some countries, even declining in some.

That could be the reason for stock price not appreciating in line with earnings.

Rest I don’t know much about US paper industry sir.

1 Like

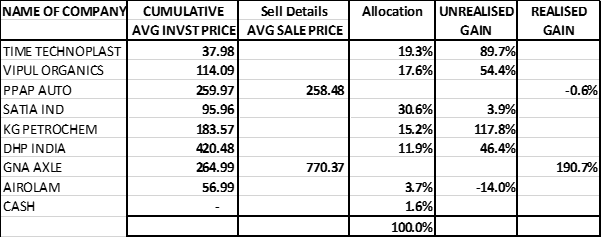

Sold most of PPAP.

Looking for other value buy opportunities,

Neuland lab, Airo Lam are on radar.

1 Like

Reason for selling PPAP -

Auto industry has a supply side issue of semiconductor shortage, which may not solve for another year or two.

Commodity prices increased over last few months, which will affect many companies over next one or two quarters.

biggest reason - such a top line was not expected.

1 Like

Airo Lam Ltd

Airolam is ranked #7 among the leading brands of the Indian laminate industry

Follows rigid international quality standards like NEMA (USA) and BS1406 (UK). For its superior design, quality, systems & environmental commitment, Airolam has been awarded ISO 9001, ISO 14001, Green Label, Green Guard & FSC certifications

Keep developing new laminates, which excel in quality & affordability

Focus on technological advancements to facilitate better production

13+ years Experience In Laminate Industry

10+ Brands

8+ Branches

Presence in 16+ Locations

69+ Distributors

170+ Employees

Rational steps by management after listing,

- High cost debt converted into low cost

- Mr Mahindrabhai Patel who had criminal/fraud cases is no longer a director

- Management remuneration is rationalised

- Many pending tax related issues seen in RHP(2017) are not seen in FY20 Annual report

- Number of permanent employees reduced even though sales has increased

Investment Rationale : -

Company don’t seem to have any competitive advantage, but industry has good tailwinds for next few years,

The industry is seeing a shift in market share from the unorganised to the organised sector,

In last 2 years many unorganised small players must have gone out of business, so we can see rapid increase in market share shift.

the changes being made in the goods and service tax in the country has resulted in lowering the price difference of plywood and laminates sector between organized and unorganized sector

Increasing urban population, rising per capita income are other key factors driving the growth of laminates industry in India

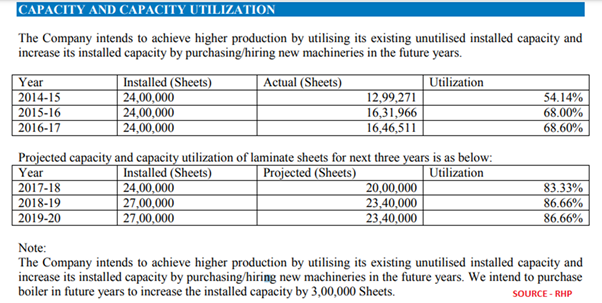

ALL is setting up a manufacturing plant of plywood and veneers adjacent to its existing location with envisaged total cost of Rs.6.30 crore and installed capacity of 67.20 lakh square feet per annum. – May be completed

ALL has expanded its installed capacity to 48 lakh sheets per annum during FY20 at its existing location considering increase in scale of operations and growing demand from the user industries. –

Seems completed (evident from March21 results - 80cr+ top line.)

It’s a big capacity expansion and from 105cr in FY20 now it can produce 350 to 400cr top line and 15 to 20 cr bottom line(5cr in FY20) , at 80cr market cap it’s no brainier opportunity.

They are sitting on expanded capacity at the right environment, may be luck.

Operating leverage can kick in as capacity utilization increases, bargaining power with suppliers may increase going forward.

Lot of scope to increase dealer/distributor network and penetrate deeper.

Risk : -

- No competitive advantage is business

- 90L bad debt written off in FY20

- Trade receivables for more than six months are consistently very high over the years

- They have to push sales through high credit period to its customers

- Many micro, small, Medium size competitors exist

- Limited to no bargaining power over suppliers from whom company imports raw material

- Cyclical Industry

Discl.:- Invested and may be biased

Not an investment advice, data sharing just for study/discussion purpose.

Data source :- RHP, Annual reports, Credit ratings etc

5 Likes

For Airo Lam Ltd business details follow company thread by @nitish

2 Likes

I revisited my thesis and I think I overestimated it

2 Likes

Nice write up Kalpesh. My estimates for top, bottomline growth are more conservative at 20,15% and listing on NSE main platform will be bigger boost (re-rating catalyst) in my opinion.

Hi Kalpesh

Very nice analysis.Noticed very thin margins like less than 10% from many years

Please let me know if there any nearest competitors on this same business

How this business earns money -

Walmart operates in very competitive environment, so they need to sell good quality products to consumers at very low rates.

so their requirement from supplier is,

- Good & consistent product quality,

- Very competitive rate

- Timely delivery

So in last few decades obviously their American & European vendors cant compete with Asian vendors in terms of competitive rates,

so KG Petrochem is one such vendor who is enjoying it location benefit in low cost country like India.

They manufacture and sell at very low margin’s and earn most of money from different gov export incentive schemes.

So their moat is being a lowest cost producer…

How strong is their moat?

- Other manufactures in low cost asian countries can have similar advantages.

- Moat is largely depend on gov incentives, so any changes in that can have big impact on their margin’s.

Moat seems weak, so what management is doing to keep the moat intact?

- to counter above point no.1 they constantly modernize the machinery to keep operating cost low - so keep competitors away by keeping operating cost lower than competitors and they may also benefit from economies of scale.

- to counter point no. 2 i.e. dependability on gov incentives for keeping good margin’s, unfortunately they cant do much and continue to depend of gov policy.,

Once they were impacted in 2014-15 when gov reduced export incentives, but somehow they managed to come to earlier margins in year or two. So they do have some pricing power with customer but we don’t know whether they will be able to do it again in future.

Last year US complained to WTO against India’s unfair export incentives, and WTO ordered India to stop those, India had to stop those and few months later come up with new export scheme (Jan 2021) which is in compliance with WTO norms, this scheme has not yet declared incentive rates until yesterday.

We have already seen its impact in last qtr along with raw material price increase, We will have to see how good or bad these new scheme for KG petrochem

Discl: Invested

3 Likes

you are right and your assumptions are realistic

2 Likes

Sir,

Have you finished buying Airo Lam & how much allocation give to it in portfolio?

I have more than 10% allocation in Airo lam but I’m planning to move some funds in debt folio so planning to sell entire stake in next 6-8 months.

Thanks sir,

Entire stake of airo will be sold off in 6 to 8 months? Or also some others too.

Will be happy if you keep updating your portfolio moves.

What are your choices for debt portfolio?

Sold GNA Axles entirely

Sold 60% position in AiroLam

@krb2709 For debt portfolio I’m thinking of Wint Wealth Platform.

2 Likes

Contemplated on the above and looked around in various sources but it still remains an elusive concept for me. Request you to share your thought process.

I will be much obliged.

Looked at wint wealth platform. Schemes looks attractive. Two queries in mind

- How to ensure safety of capital? Are they rated by any rating agencies.

- All scheme are fully subscribed & NO Room at the moment.

Kindly advise.

Yes. Maintenance capex is elusive concept unless management disclose the numbers, like in the case of Sudarshan Chemicals we know the number is around 35 cr as management said it in one of the con-call.

for companies where management has not disclose it, I calculate it with some formula(easily available on google search)+common sense.

As Warren Buffet says " It is better to be approximately right than precisely wrong"

I must disclose that I have not yet used their platform.

About safety of capital and scheme details lot of information is provided on their website, additionally they do webinar for each asset which is available on YouTube.

Each scheme is rated by rating agency, like their earlier asset was issued to U grow capital which is listed company and you can find all the details including rating report in websites like screener.in

Schemes do come and go, and their frequency will only increase from hereon.

Hope this helps

1 Like

Bought truckloads of Satia Industries

1 Like

GNA SOLD BECAUSE IT IS TRADING AT ITS FAIR VALUATION AS PER MY CALCULATIONS.

CASH EQUIVALENT TO 5.1% OF PORTFOLIO SIZE TAKEN OUT FOR TAX PAYOUTS AND OTHER PERSONAL REASONS.

4 Likes