Core hypothesis - Value with growth in good emerging industry with Real estate, house upgradation tailwinds. Disc : Invested and looking forward to hear other views

Stock : Airolam Industries Limited; Listed on NSE SME Platform in Sep’17 at INR 38/share (Pre-Money Mcap at IPO: INR 42cr); Raised INR 15cr new capital; Post money MCap at IPO: INR 57cr; Valuation at IPO: P/E ~22x and P/S of ~0.6x; No exit of promoters/existing shareholders during IPO and no sale of shares by promoters later; No pledge of promoter shares

Current Mcap: INR 59cr

Business : AiroLam manufactures and markets hi pressure decorative laminates primarily in India (International revenue ~15%) . Product includes laminated sheets, pre-laminated boards, and laminated floorings under brands, such as Classico, Airolam, I-Lam, Airolite, Airoline, I-Lite, Premium Airodoor, Airodoor, Airo Flexi, Airo xterior, Airo Digilam, etc.

For reference, we have listed player in the similar business (laminates) like Greenlam (market leader), Stylam, and other small ones are Rushil Decore and Deco-Mica. Apart from that there are sizable unlisted players like Sunmica, Formica, Merino, Durian etc.

| Greenlam | Stylam | Rushil Decor | AiroLam | Western India plywood | |

|---|---|---|---|---|---|

| Stock Price (Rs) | 1,369 | 1,188 | 290 | 39 | 64 |

| mCap (Cr) | 3,300 | 2,015 | 560 | 59 | 54 |

| P/E | 33 | 32 | 41 | 11 | -0.2 |

| P/S | 1.14 | 2.50 | 1.67 | 0.44 | 0.64 |

| P/B | 5.6 | 7.4 | 2.1 | 1.2 | 1.4 |

| D/E | 0.6 | 0.6 | 1.3 | 0.8 | 0.6 |

| Sales (FY 21) (Cr) | 1,200 | 476 | 335 | 133 | 85 |

| EBIDTA (FY 21) (Cr) | 173 | 95 | 35 | 12 | 4 |

| PAT (FY21) (Cr) | 75 | 55 | 14 | 5 | -1 |

| Sales CAGR (~5 yrs) | 7% | 2% | 8% | 12% | 0% |

| PAT CAGR (~5 yrs) | 30% | 19% | 17% | 23% | 0% |

| RoE | 19 | 10 | 12 | 11 | 3 |

| RoCE | 18 | 13 | 6 | 11 | 6 |

Capacity build-up : Airolam has increased operating fixed assets significantly over the time from INR 10.7cr in FY17 to INR 37.5cr in FY21. Almost INR25cr of assets became operational in FY21 (most of that were WIP at end of FY20). High growth in manufacturing capacity during the year (despite being a Covid year) resulted in revenue growth of ~25% in FY21. It is expected that full capacity utilization to flow from FY22 onwards. Assuming conservative revenue growth of 20% and normalized PAT margin of ~4.5% (not assumed benefit of operating margin), FY22E P/E comes in the range of ~7-8x.

Debt Management : Airolam has smartly managed the debt post IPO. The company has consistently reduced cost of debt through restructuring and Euro term loan. The average cost of debt reduced from 11.2% in FY17 to 6.9% in FY21. The total debt of the company only increased from INR 22.5cr in FY17 to INR 34cr in FY21 despite increase in fixed assets from INR 10.6cr to INR 37.5cr in FY21. Most of the new assets funded through capital raised during IPO, accruals from business profits etc. It is worth noting that WC has not improved significantly from IPO period, we assume Covid may be the culprit.

Management : Pravinbhai Patel is a CMD and key person running the company. As per prospectus, he is a Computer Engineer from Gujarat University and has experience in laminate manufacturing industry for more than 10 years. There is no specific info available about Pravinbhai on google or other reports etc. However, we may infer few things about the management integrity through financials/annual reports:

• No reduction in equity holding either in IPO or later;

• No pledge of shares;

• Unsecured interest free loans to company (~INR 5cr);

• Remuneration of MD (Pravinbhai Patel) for FY20 was INR 8.4 lakhs. As per company policy, max remuneration to key MD, Directors is limited to INR 25 lakhs p.a.

Open questions : Despite all positives, stock price is still is at IPO price. Airolam’s revenue almost doubled and PAT almost tripled over the period. Balance sheet has become strong and manufacturing capacity has almost quadrupled. Interest cost of the company has almost halved. We believe major barrier for price movement is listing of stock on SME platform:

• Trading requirement of minimum lot size of 3000 shares. It results in minimum investment of ~INR 1.2 lakhs. Since it is a micro cap and mainly traded by small retail investors, this minimum investment criteria is a big deterrence for small investors

• Investors have apprehension on investing in SME platform of exchange due to lack of liquidity. Investors prefer to invest in Main board of exchange

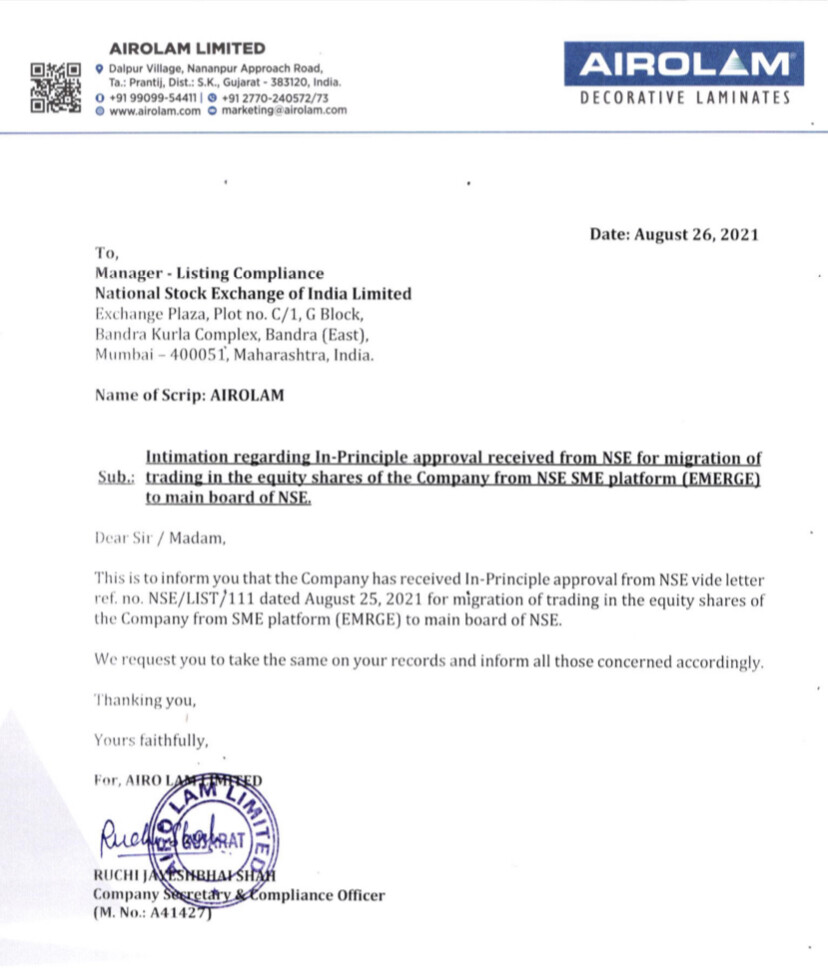

Going Forward : On 16 June 2021, Airolam has informed NSE that its board has approved the migration of listing and trading of equity shares of Airolam from SME platform to Main board of NSE. In this regard, company has already started the due process of shareholders approval and subsequent application to NSE. Company is already in compliance with and fulfil migration requirements of NSE. Shareholders approval process is completed on 24th July 2021. In our analysis of other stocks which migrated from SME platform to Main board of NSE, migration process takes close to 1 month from the date of shareholders approval. (https://archives.nseindia.com/corporate/AIROLAM_24072021153255_Combined_Voting_Results_Scrutinizers_Report.pdf) The stock has already seen run up of ~25% post this announcement in last one month. We believe once stock is migrated to Main board of NSE, it should attract more investors and enhanced liquidity should drive stock price.

Risk analysis/ Downside : -

- Competition : Laminates sector is highly fragmented with multiple players (both regional and pan india) including sizable unlisted companies. Airolam will have to face constant competition and need to differentiate in terms of quality, pricing and fluid supply chain

-

Liquidity : Presently the company is listed under NSE SME platform where liquidity and investor acceptance in low compare to listed stocks at NSE Main platform. As discussed above, since company has already started process of migration from SME platform to Main board of NSE, we see it is just a matter of time before it moves to Main board of NSE

-

Innovation : Constant innovation in products and vertical expansion of related products is quintessential for the long term growth of the company

-

Economic recovery : Overall economic recovery post covid is key for the growth of laminate sector and Airolam in particular

-

FX risk : There is Euro loan of ~9 Cr at 5% but there is currency risk associated with it.