Universal Autofoundry Ltd sounds very interesting. Would it be possible for you to share your notes or observations ?

@The_Seeker yes sure,

Universal Autofoundry Ltd

Founded by 2 friends, run the business together for many years, one of the founder family exited recently(they had disputes), now current management is in complete control & rationalizing things(at least that’s what I’m expecting)

Reason for being cheap -

- Disputes between founders

- Business/industry in down cycle

Triggers -

- Valuation wise it’s cheap,

- Rationalizing expenses

- Adding value added products/processes, capacity expansion

- Margin/RoCE expansion(in next industry up-cycle) etc.

Thankyou! much appreciated!

One of the famous investors, Ashish Kacholia, has been reducing the stake consistently in Universal Autofoundry. Anything alarming?

Mr. Kacholia bought some 10.3 Lakh shares at Rs161.59 per share.

I think he provided exit to outgoing founder.

I do not have any idea why he is selling.

Finally sold IRM ENERGY and brought INFLAME from the proceeds.

What’s your thesis on Inflame appliances?

Have you looked at Greenchef or Stove Kraft?

hi @Apurva_Dubey ,

Inflame Appliances Ltd

I don’t know much about Stove Kraft & Green chef, I don’t know much about Inflame either because publicly available information is very limited & no con-calls.

from whatever is my limited understanding, I can see that all three are different business models with different focus areas.

Stove Kraft is building a mass market brand whereas Green chef trying to build a premium brand.

whereas focus of Inflame is towards becoming supplier to all brands, and be an alternative to Chinese imports.

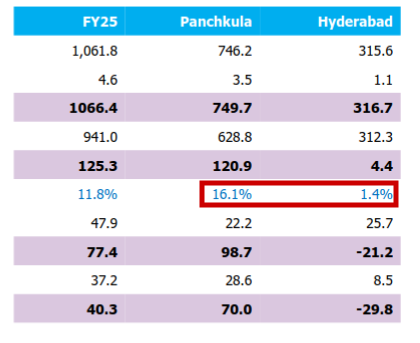

Why I’m Investing in Inflame?

If you look at above screenshot, you will realize lot of manufacturing capacity is underutilized.

As per my best estimate they can do 250Cr revenue at near full utilization. that is 135% revenue upside available.

As they are already doing OPM of 16.1% at Panchkula, that conveys that they can do same margins at Hydrabad facility too when they increase capacity utilization (Manufacture same products at both plants).

They can do NPM of 23cr or more at full capacity utilization.

Thats almost 670% upside whenever that happens.

Lots of operating leverage to play out as revenue increase in the future.

Margins can go well beyond 16% at full capacity, so its not expensive at future PE of 7.

Whether they will be able to grow? that’s the big question.

Disc:- Invested, Biased

SG Finserve & SG Mart

Management of APL Apollo realized, their dealers are so much dependent on them, and thought about leveraging this dependency to create new businesses.

They came up with two business models,

-

SG Mart

-

SG Finserve

I invested in both businesses looking at past execution track record of APL Apollo team.

Now, as more I think about these businesses more scepticle I become.

• SG Mart will do great in steel industry down cycle, but why companies will stick to them in industry upcyle, when demand for their products is high, why would they need SG Mart?

• SG Finserve has advantage of lower cost borrowing compared to its peers, that advantage primarily come from Sanjay Gupta family holdings in APL group, at some point in time lenders will find it uncomfortable to lend at such low rate when size of loan will increased to like 70% of value of SG family shares.

• May be management of SG Finserve thinks by that time they will have a good size and track record to convince banks to lend them at low rate, but still that low rate will not match what they currently have.

• That time SG Finserve will also increase their lending interest rate, so they will be at same level playing field as other Supply Chain Financing peer, their growth will slow down?

• They give very short term loans, like for 30-40 days, so if they have Rs100 to lend, they can roll it like 10 times in a year, so they can disburse Rs 1000. That looks big amount but their AUM will be Rs 100 only. Means they can make interest of whatever 13-14% on Rs 100 only in a year. Growth seems difficult for such a business compared to other financing business models. Cyclicality component will be higher.

• Suppose share price of APL group goes down, what will happen in that scenario(SG Finserv)?

• Promoter holding in both the companies are below 50%, when they have capacity to keep it at 75%, that also tells that they experimenting with these business models and not quite sure whether things will work out as anticipated.

Disc: Sold all the shares of both SG Mart & SG Finserve today, as an individual investor my job is to find LOW RISK HIGH RETURN ideas, not HIGH RISK HIGH RETURN idea, it was a mistake.

Great result by Vaibhav Global

Sold entire position today due to unable to understand geopolitical issues and spoiled relationship between top leaders of both countries.

Largest sales of Vaibhav global happens in USA.

I had entered Indiamart during covid and by sheer luck exited at the peak making good profits. After that it started a slow downward journey. I have again started tracking Indiamart for last 4-6 quarters. Management is trying very hard to find root causes for low growth and address them to get back to higher growth they have not been very successful as yet. I understand it is cash generating business available at relatively reasonable valuations (in context of growth struggles). Would it be possible for you to share your thesis for Indiamart?

Sure,

Indiamart Intermesh Ltd

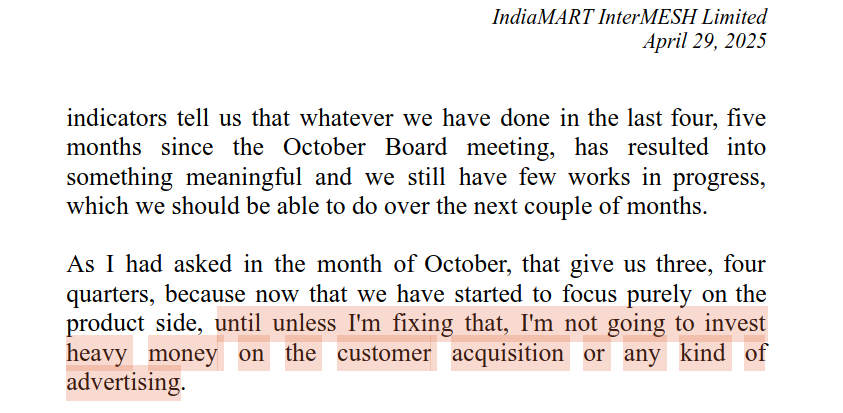

I don’t think they are facing growth issues, they were facing high churn at lower strata customer base, so they chose not to grow before solving this root cause for this problem.

I think that was wise decision from management side, because they are intentionally taking short term pain for good quality long term growth.

July 30, 2024 concall-

Jan 21,2025 concall -

April 29,2025 concall -

My investment rationale -

- This business is cash generating machine, which doesn’t consume it back much, throw it out as free cash.

- It has become big enough, so that competitors will find it difficult to enter in this space.

- It has pricing power ( You can see in last few quarters, without adding new customers it’s still able to grow by raising prices for existing customers)

- Promoters/management making rational decisions

- when they solve churn problem, business can growth easily at 20% CAGR for many years to come, If they can’t solve they can still be able to grow business.

- 30-40%ROCE with 20% CAGR growth is a great combination for future returns.

Inflame Appliances:

Any clarification given by promoters in ARs (if you have studied them) as to why they have sold their shares/ diluted their holdings?

You are right about the opportunity size if it can increase its sales through contract manufacturing (B2B) or by B2C directly.

Still it is not available at cheap valuation, compared to the 5 year sales growth. Also being a low mcap company with not clear growth visibility (read no concall/management commentary on business growth), it is expensive at 50 PE.

I may be wrong in my assumptions.

Dis. : Not invested; Studying.

SG Mart:

I was looking at SHP of APL Apollo since 2011 and the shareholding has decreased from 41% to 28%. That’s not a huge selling given the growth the company has experienced and every promoter has right to encash the hardwork they have done.

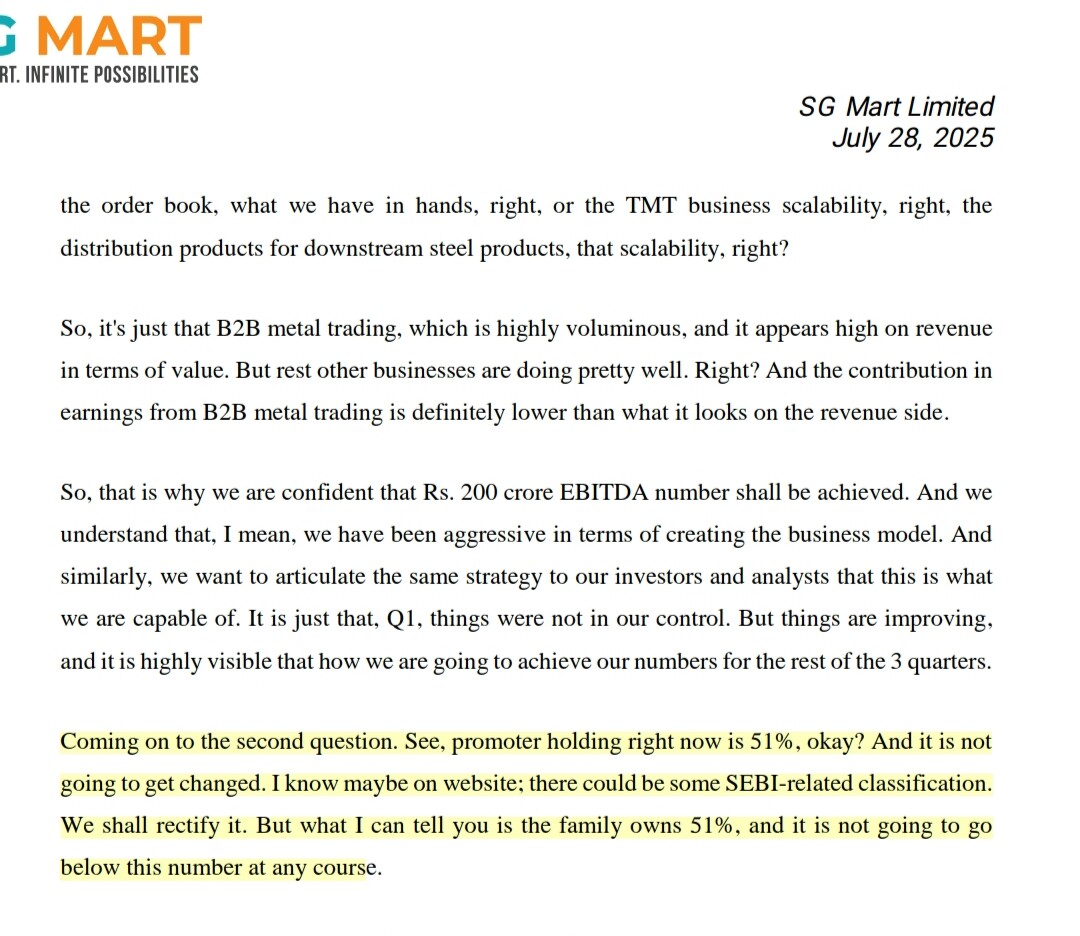

Coming to SHP of SG Mart: The Promoter Group Holding is 36% in Q1 26 SHP and no doubt it has been on a regular decrease. However if include the shares help by gupta family in the public section, the holding is above 50% and it has been committed by management that it won’t go beyond 50% (screenshot from CC attached)

Regarding your skepticism about what would happen to business when steel prices recover, I think the business is volume play and not a price play. They are just the middle men who can buy large quantities and sell to small businesses. How would that change if steel price increases? If steel manufacturers can directly sell that much volume to businesses, there would have been no business / revenues for SG Mart irrespective of steel prices but as you can see that’s not case (based on the assumptions that same channels can sell irrespective of steel prices).

Regarding the insecurity about correction in SG Mart in case of amy weakness in APL apollo business: Yes, there may be some correction as both belong to same promoters but beyond a point they are different business and will be valued depending upon their individual growth projections, profits and cash flows. Also APL apollo is matured business while SG Mart is still small, so linking them together in terms of price corrections is not wise.

Would love to hear your views.

Dis. : Invested and biased.

Brought Siddhika coating few weeks back. sold Prime Fresh entire position today.

Will put rationale for buying Siddhika coating lateron.

I always thought I bought Prime Fresh for long term, but sold very early, may enter again if price drops significantly.

Now again sitting on significant cash position.

Yesterday sold entire position of Indiamart & Krishca strapping

Krishca Strapping: Bought in the impression that company is growing fast in Value added products & services, but in last concall Promoter made it clear that he is more interested in growing commodity/semi commodity business in the future. Initially I thought of it as backward integration but he wants to grow it big.

Sold at good loss.

Indiamart : I bought it by looking at business quality and great cash generating machine, but CG issues always haunted me since my first purchase, couldnt live with such constant fear, so decided to exit at small profit.

After covid world over central banks flooded economies with money by introducing huge liquidity and reduced interest rates, result being huge inflation and big bull market, that is not going to sustain more than few years. Now many central banks absorbing liquidity and reducing interest rates as inflation and economic activities going down.

I have been in the selling mode to build cash position from last many months now, hope market will reward my efforts by providing great investment opportunities few months down the line.