Jyoti Resins and Adhesives Limited (JRAL) came up on my 10 year 100x multibagger screen on screener.in. It has done remarkably well on most metrics - profit growth, capital efficiency, margin expansion, low leverage. Q3-FY21 results were an absolute stunner and I got up early today, brewed some coffee and made first impression notes. This company is incredible, I wanted to share. Maybe an addendum later.

• Per the recent Investor Presentation (Slide 13 here), “The company imports raw materials from several countries”. However, Note 35 on page 92 of the Annual Report (FY20-21) discloses “Value of imports calculated on CIF basis” as Nil.

• Up until FY17, Statutory Auditors were Raman M. Jain & Co. Per Annual Report for FY17, Raman M. Jain & Co. “expressed their unwillingness to hold office from the conclusion of this Annual General Meeting till the conclusion of next Annual General Meeting”. (Emphasis mine). Suresh R Shah & Associates were appointed as the new Statutory Auditors from FY18.

• Till FY17, Auditors Raman M. Jain & Co. in their Independent Auditor’s Report stated the Auditor’s Responsibility to be:

“An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the Financial Statements. The procedures selected depend on the Auditor’s judgment, including the assessment of the risks of material misstatement of the Financial Statements, whether due to fraud or error. In making those risk assessments, the Auditor considers internal financial control relevant to the Company’s preparation of the Financial Statements, that give a true and fair view, in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on whether the Company has in place an adequate internal financial controls system over financial reporting and the operating effectiveness of such controls. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of the accounting estimates made by the Company’s Board of Directors, as well as evaluating the overall presentation of the Financial Statements.” (Emphasis, mine).

The emphasised portion (in bold) is a safety parachute and absolves the Auditors of providing any opinion on financial misreporting by management. This is typically done in cases where Auditors and Management have a differing view on representation of accounts. The fact that they eventually resigned suggests the differences were too large to be reconcilable.

The new Auditors (Suresh R Shah & Associates) merrily skipped the emphasised (bold) portion within the Auditor’s Responsibility within their Reports. Overlooking and not expressing an opinion on financial (mis)statements might have been a feature for their retention over the past 4 years.

• Earlier Auditors (Raman M. Jain & Co.) write in each of their Audit Reports:

“In our opinion and as per the information and explanations provided to us, the Company has not entered into any long term contracts including derivative contracts, requiring provisions, under the applicable law or accounting standards, for material foreseeable losses.” (Emphasis, mine).

… while the new Auditors (Suresh R Shah & Associates) write:

“The Company has made provision, as required under the applicable law or accounting standards, for material foreseeable losses, if any, on long-term contracts including derivative contracts.” (Emphasis, mine).

It is unclear what these ‘long-term contracts’ are. It is also quite a coincidence that the change in language happened with the new Auditors.

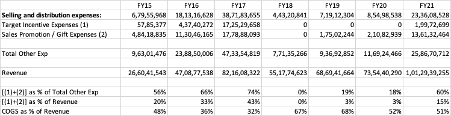

• Between F15 and FY17, incentives doled out to salespersons and distributors (Target Incentive Expenses and Sales Promotion/Gift Expense) ballooned from 20% of revenue (FY15) to 43% of revenue in FY17. To contextualise, raw material expenses as a % of revenue stood at 32% in FY17 (note that JRAL is a manufacturing company). Coinciding with the change of Auditor in FY18, FY17 P&L was restated to not include such incentives and it was netted out of revenues too. Similarly, FY18 had no disclosure of such incentives. Over FY19 and FY20, disclosure pertaining to Sales Promotion expense resumed but was very muted at 3% of revenues, but no Target Incentive Expenses. FY21 disclosed such incentives at 15% of revenue. It remains to be seen whether this is a case of underreporting or reduced incentives owing to higher brand awareness. [See Table below; FY17 numbers are before restatement]

• Provisions for (Unpaid) Expenses as reported under Current Liabilities have ballooned to INR 96.75 crore as of H1-FY22. It is not clear whether these are provisions for warranties/guarantees or for raw materials payable to suppliers. But such provisions accounted for an astonishing 71% of the total balance sheet size (excluding revaluations) for FY21. This was 6% in FY15, 24% in FY16 and grew to 55% in FY17 (the year the old Auditors resigned).

• Per the Company’s own admission to the Ministry in a letter dated April 2019, JRAL had an existing Synthetic Resin Adhesive (PVAA) capacity of 600 tons per month (TPM). In the letter, JRAL had applied for environment clearance of an additional capacity of 900 TPM. Such EC was received in July 2020. It is surprising that the latest Investor Presentation talks about existing capacity being 1000TPM (rather than 600TPM).

• Per the letter, the expansion was to be carried out on the existing land with an estimated capital cost of INR 2.80 crore. The letter stated that “No additional land will be required for the proposed expansion.” However, FY21 reports an addition of INR 15.20 crore towards purchase of land. While this purchase could be construed as an opportunistic land purchase for the envisaged capacity expansion to 2000TPM, it would take several years before the incremental 150% capacity (from 600TPM to 1500TPM) would be fully utilised. A lot can change in 4-5 years! It would be interesting to find out from whom the land was purchased ![]() .

.

• Then there are the already highlighted issues of high remuneration, three fancy cars (ostensibly for the three executive directors), etc. The Auditors have been very supportive in the enterprise, but they will conclude their term in FY22 – I believe the management would have started scouting for a friendly new auditor already. Hedge fund Ark Global Emerging Companies, LP, holds 1.25% in JRAL (per Dec-21 SHP). I was excited; unfortunately, this Ark has nothing to do with Cathy Wood’s Ark Funds ![]()

• As a fun exercise, add up the line items within the Asset side of the Balance Sheet, barring fixed assets (they do have a factory so let’s assume this to be genuine) and Other Current Assets (statutory deposits etc). Now compare this with the Provisions they have disclosed. Deduce whatever you’d like ![]()