Jyoti CNC Automation Limited is one of India’s largest CNC machine tool manufacturers.

The Company’s range of products that includes CNC Turning Centres, Turn-Mill Centers, Vertical Machining Centers (VMC), Horizontal Machining Centers (HMC), and advanced 5-axis Machining Centers, along with solutions for Industry 4.0 and Artificial Intelligence (AI).

Vertically integrated company with in-house manufacturing of machine components such as spindles, tool-changers, pallet changers, rotary tables and universal heads in-house. The company has its own R&D Centers, Foundry, Machine Shop, and Sheet Metal Unit. Also has in-house design capabilities.

Focus on R&D with dedicated R&D facilities at Rajkot and Strasbourg.

diverse customer base. Some of the marquee customers include ISRO, Brahmos, Harsha Engineers, Bosch, Tata Advanced Systems etc.

As per management, India consumed $3 billion worth of CNC machine last year (approximately 24,000 crore). of this 65% was imported while 35% was domestic over the next 5–7 years the consumption is expected to grow at 20%.

The company eyes that the proportion of imports will decrease in the next 5-7 years that is import substitution is likely to happen. Secondly, the market itself is growing at 20%.

85% of the total market is metal cutting and 15% metal forming. Jyoti CNC status metal cutting

Overall market the entry level is domesticated 80–85% is domestic while in high end machines 90% is imports. the company is focusing on this high end of the market, where competition is mainly from Germany and Japan.

The Company operates in a niche growing sector. But a good business is not always a good investment if the valuation is not in favor.

Crude Valuation:

Last Quarter EPS of 2.44. If we assume this is the run rate then full year eps comes out to be approx 10 i.e. on PE basis it is valued at 75X i.e. a lot of growth is already priced in.

The main risk in my opinion is the execution risk i.e. whether their products will find traction among manufacturers pitched against tried and tested suppliers from Japan and Germany.

Jyoti CNC Automation Ltd (updated as of 24th May/24)

Company

Jyoti CNC Automation Ltd, est. 1989, currently operates with two manufacturing facilities in Rajkot (Annual capacity of 4400 machines p.a.) and one in Strasbourg, France (121 p.a.).

Offering one of the most diverse CNC portfolios in the country, its products include CNC Turning Centers, CNC Turn Mill Centers, CNC Vertical Machining Centers (VMCs), CNC Horizontal Machining Centers (HMCs), simultaneous 3-axis and 5-axis CNC Machining Centers, as well as multi-tasking machines.

The end users are Defense, Automobile, Electronics & Aerospace co’s.

The company’s clientele includes prominent organizations such as the Indian Space Applications Center–ISRO, BrahMos Aerospace Thiruvananthapuram Limited, Turkish Aerospace, Uniparts India Limited, AVTEC Limited, Tata Advances System Limited, Tata Sikorsky Aerospace Limited, Bharat Forge Limited, C.R.I. Pumps Private Limited, Kalyani Technoforge Limited, Shakti Pumps (India) Limited, and Bosch Limited. [clientele]

3rd largest in india at 10% market share at 12th largest globally with 0.4% share. (as of 2023 & 2022 respectively)

2,538,822 sq. meter manufacturing facilities in Rajkot, India and Strasbourg, France.

Acquisition of Huron Graffenstaden in 2007. This also indicates co’s long term approach and its ability to prepare for future dynamics. (as the acq. aided Jyoti to enter into Central Europe market and gain insights into 5-axis machines which caters to defence and aerospace)

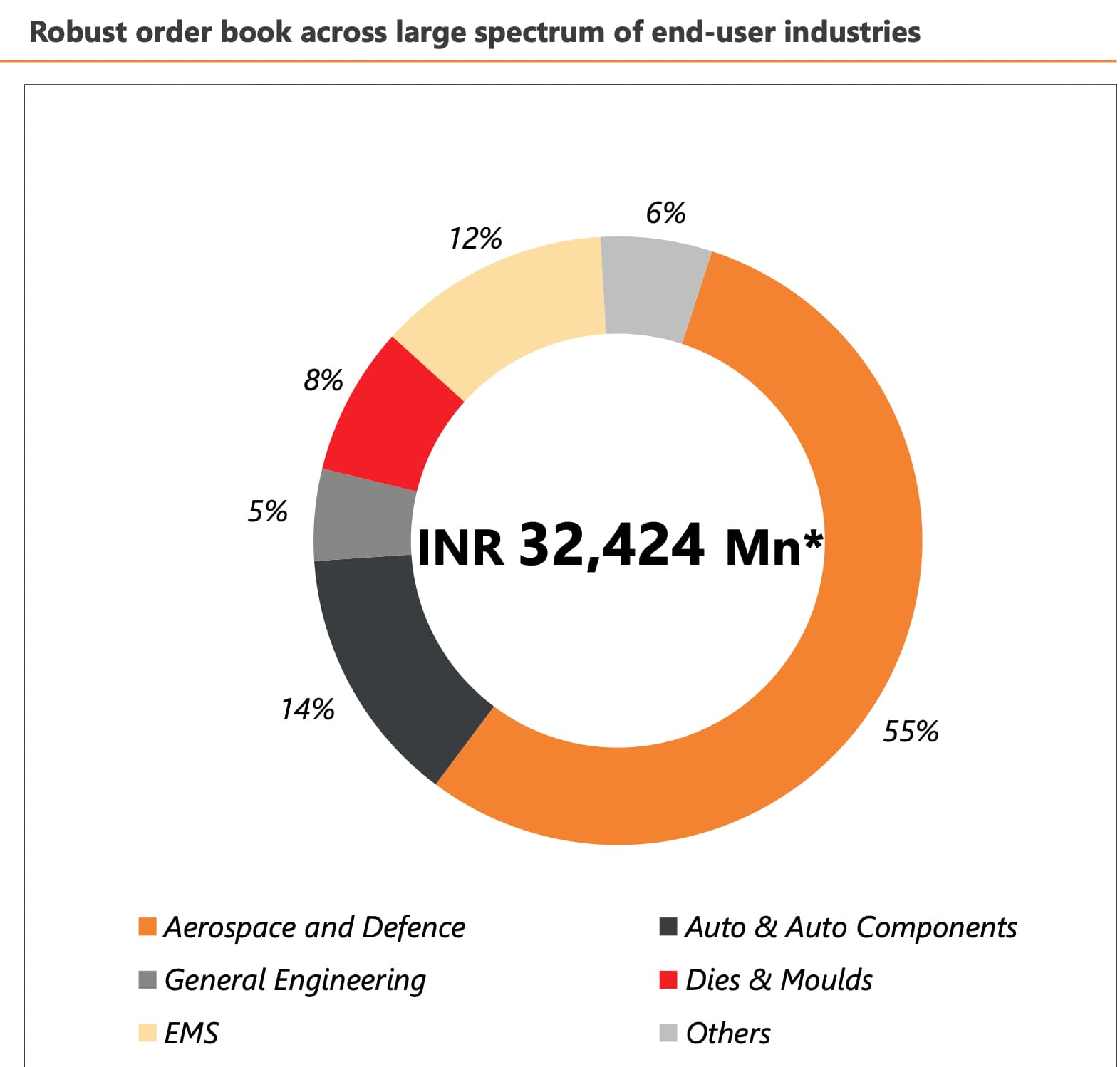

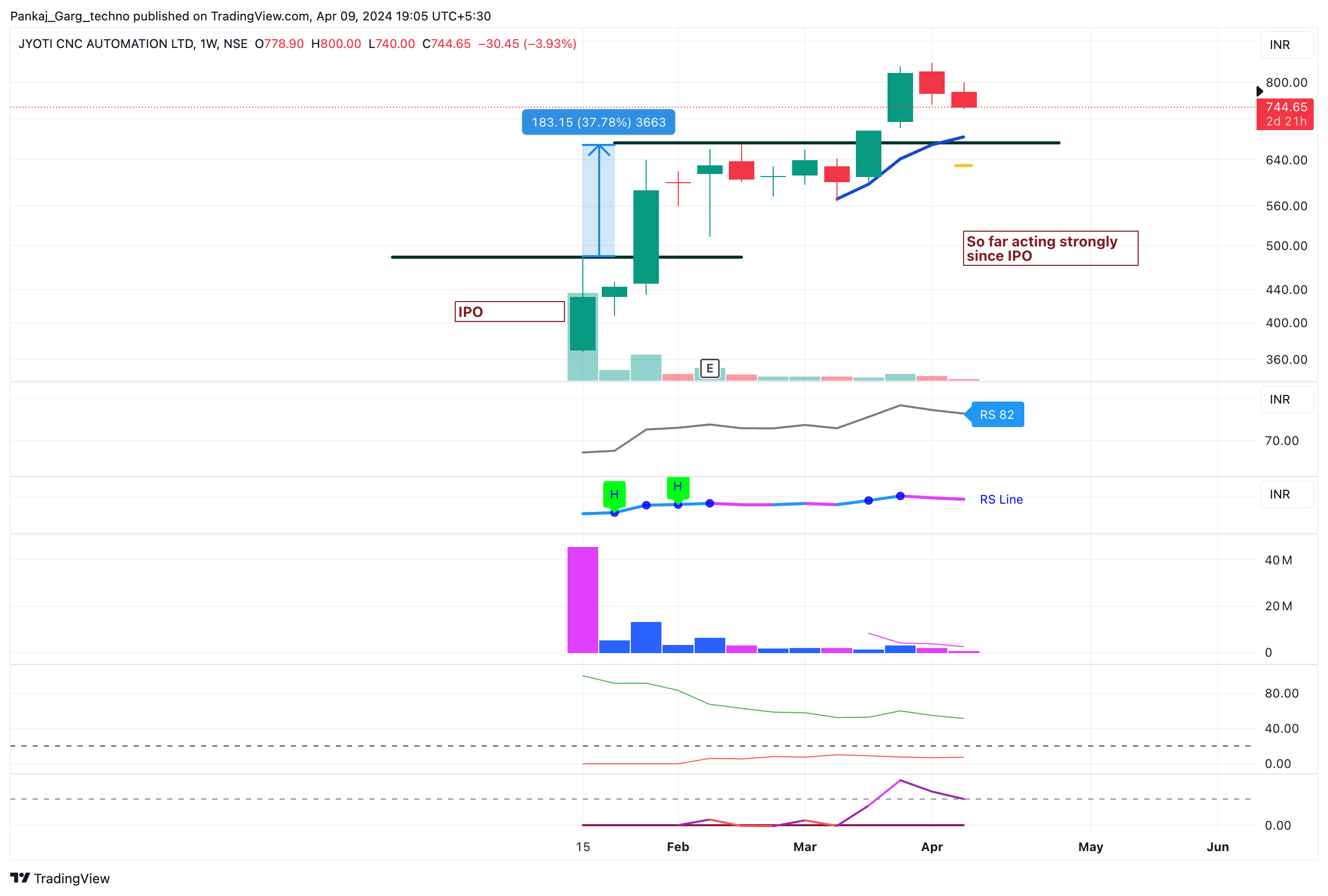

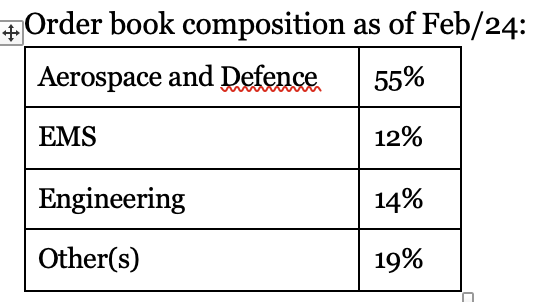

Order book at Rs. 3300Cr as of Feb/24, and delivery of Rs. 3200 is expected to be delivered in next 18 months.

Estimated base growth rate of CAGR ~20% for next few years for 5-axis CNC’s.

Capacity increased to 5000 with De-bottlenecking this year.

To be increased to 6000 by next FY.

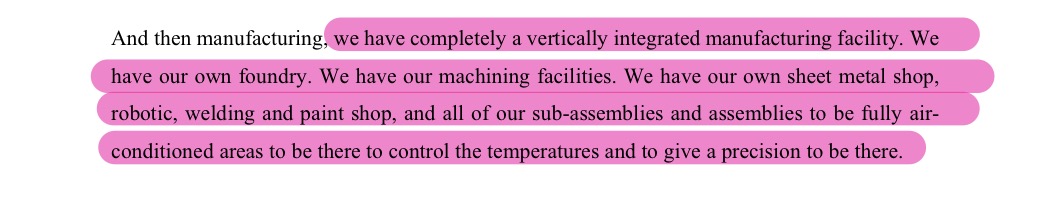

Vertically integrated; with their own foundry, machining facilities, sheet metal, robotic, welding and paints shops.

Around 140+ engineers dedicated solely on R&D.

Direct sales and marketing in case of Indian market.

IPO proceeds worth of Rs. 475Cr used to pay off debt. (Debt/Equity @ 0.22). Reduced interest cost upto 55-60 Cr.

Planning to go debt free in next 2-3 years.

Inventory turnover to decrease from 300 to 210-220 days by 2024 and 170 by 2025.

About 20-25% price competitive than ones that are imported.

Focus on gaining market share through import substitution.

N0. Of machines manufactured in FY23-24 @ 3495 units. (indicates a capacity utilization at ~80%)

Closing Order Book of ₹3438 Cr.

Expecting INR 1,500 to INR 2,000 crores of orders in FY’25.

Industry

India consumed $3 Billion worth of CNC machines, whereas global consumption is around $80 Billion annually.

Of which 65% is imported and 35% manufactured domestically.

Majority of imports from Germany (around 30% of global output from Central Europe) and Japan.

Industry divided into Metal Cutting (85%) and Metal Forming (15%).

Jyoti, focuses on Metal Cutting, and has been awarded “Best Metal Cutting Brand in India” multiple times.

Prominent player in 5-axis CNC machine.

Offers solutions suited for transitioning towards ‘Industry 4.0’, including their flagship multifunctional solutions package viz. ‘7 th Sense’ – which is geared towards automating sophisticated diagnostic and analytical functions enabling seamless management of productivity, health and tool life of the CNC machine.

The 4 Stallions that Jyoti CNC bets on :

The Global Aerospace and Defence market size is expected to reach as ~US$ 1388 B (@ 8.2% CAGR) by 2030.

The potential CNC Machine demand for EMS industry in India is over 1,00,000 machines within the span of next 5 years.

The Electric Car market in India is expected to grow at a 56.0% CAGR during 2024–2030.

The Indian semiconductor industry is expected to grow at a CAGR of 19.7% from 2022-23 FY to 2026-27 FY.

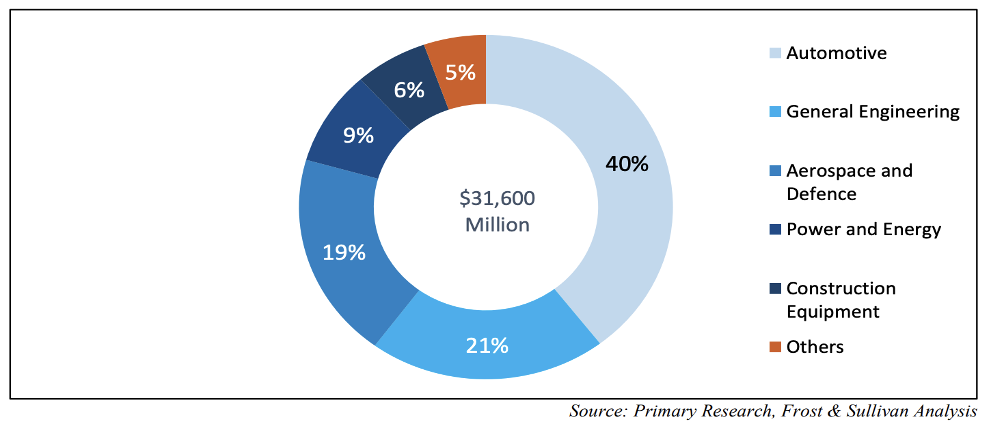

CNC Machining Center Production Share by End User CY22 (%)

Industry 4.0 is changing the CNC machining (excerpt from DRHP)

Industry 4.0 is the latest in industrial revolution and it is changing how CNC machine shops run on a day-to-day basis. With all the smart technology and integrated software available, quicker turnaround times and decreased downtime all result in increased productivity. Data collection and analysis from sensors and other instruments help CNC shops test out new products or study product use. With the application of Industry 4.0, Data helps inform CNC machine shops and manufacturers to make better products and allows business owners to examine their supply chain management process and delegate tedious tasks to the machines.

Industry 4.0 basically refers to a more complex manufacturing setup that includes IloT (Industrial Internet of Things) that monitors and measures manufacturing processes and reacts autonomously to errors. This ability helps CNC machines self-diagnose problems and correct errors in the manufacturing process faster than employees can detect and respond to errors or diagnose the reason for machine malfunction.

For the industry specific example, the medical products industry demands perfection in manufacturing processes because life depends on fail-safe components. CNC machines and Industry 4.0 technology together ensure the production of high-quality components for medical devices. CNC and CAM (Computer Aided Manufacturing) machines are a combination that produces top quality, flawless products, regardless of the industry a manufacturer serves.

One of the leading CNC machine manufacturing companies globally as well as in India with presence across the CNC metal cutting machinery value chain.

Well diversified customer base.

Constant focus on R&D and new product development.

Vertically integrated.

Experienced promoter group.

Provides an extensive range with over 200 variants across 44 series.

Thesis

The end-user industries are growing at a faster pace.

Strong order book providing revenue visibility.

Financial Strength improvement. To be debt free in nest 2-3 years.

Addition of new customers.

Focus on EMS rising as the industry is getting groomed.

Multiple Engines of growth:

CNC sector to grow at around ~10% CAGR.

Base growth rate 20% CAGR for 5-axis CNC’s.

Capturing market share through import substitution on high-end machines.

Capturing market share in Central Europe through Huron. (turned EBITDA +ve, and expected EBITDA margin of 20% at optimal capacity)

Anti-Thesis

The growth probably is already priced in, as evident through its current valuation.

Material cost is a huge chunk of COGS, and can further increase due to underlying raw goods prices.

Business is highly dependent on skilled workers, and attrition rate was around 25% in 2023 as stated in its DRHP.

Customers (even the larger ones) don’t usually go forward with long term contracts, and it can take away a huge chunk of revenue if a price competitive player enters in the market.

Disc: Invested. DYODD. Not a Buy/Sell Recommendation.

a. 40-50% growth in FY25

b. Expect more than ₹1,600 cr+ of order inflows in FY25.

c. Capacity Last Year: 4400 machine, by september it will be: 6000 machines

d. Execution will be: 5400 machines this year, at 90% utilization

e. Last year by FY23 avg per machine throughput was 27L/machine which has touched 35L/machine, and expecting to touch 45-50L per machine

f. Margins will be conservative, 25-27%

g. Net Debt is zero, Gross debt is 0.25% of equity

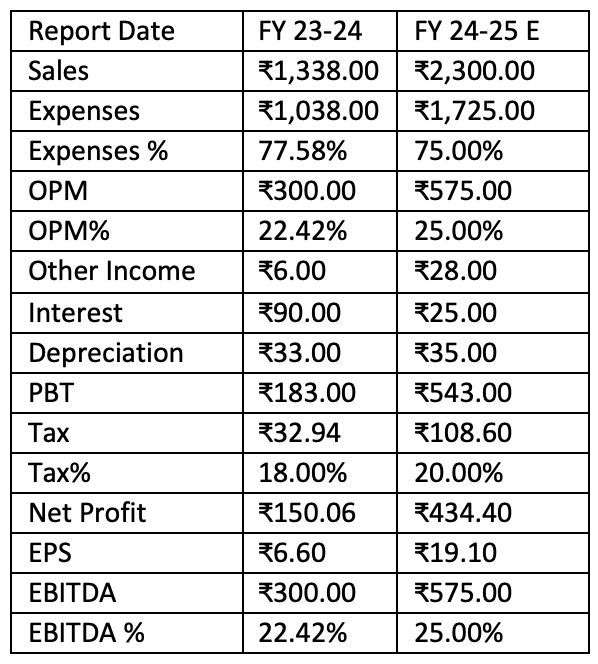

The Q3 results are very good. The 9 month NP has crossed the previous entire FY net profits . Now all eyes down for the presentation and conf call for the order book and management commentary jyoti CNC.pdf (3.0 MB)

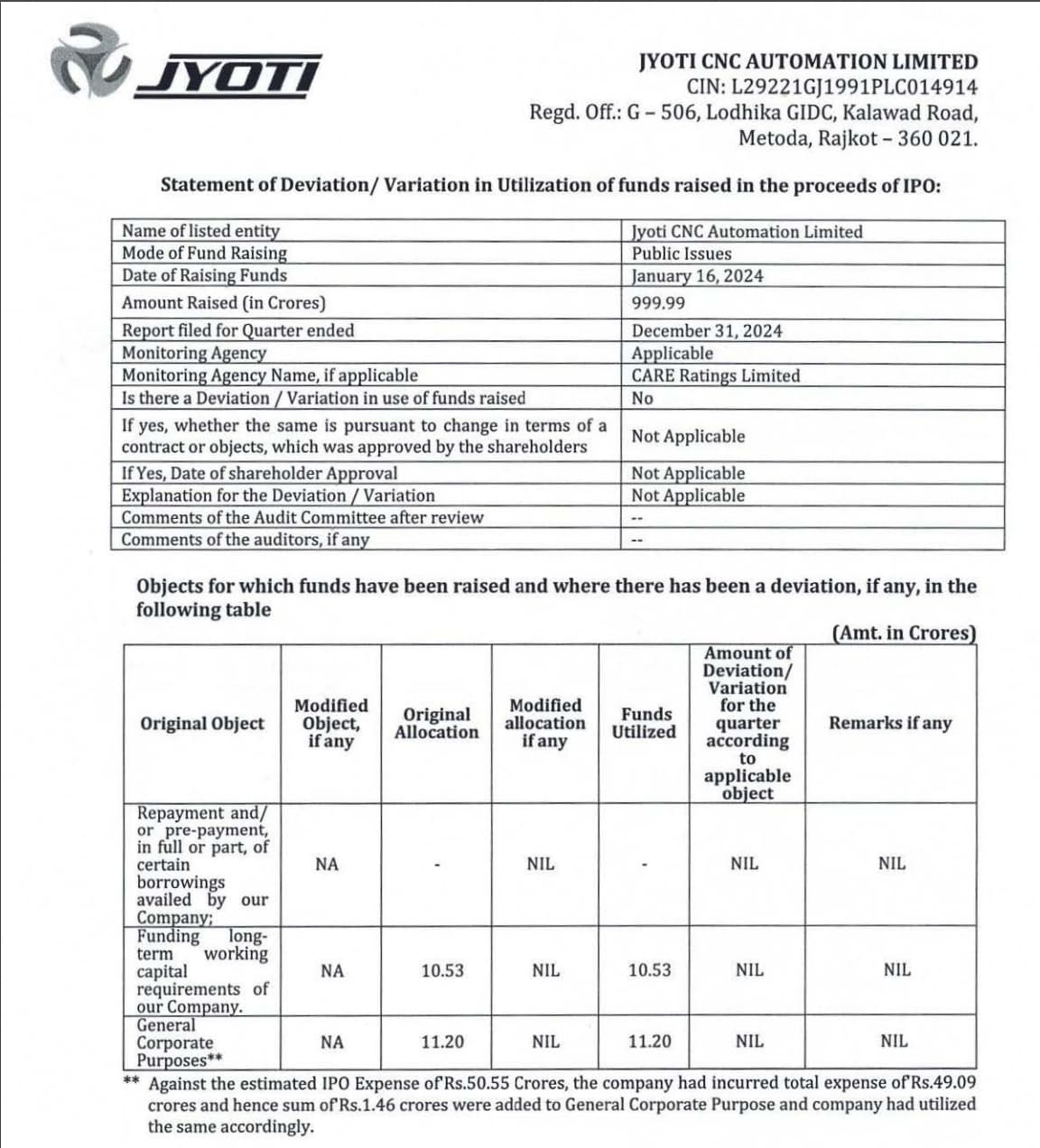

**No funds were used for debt repayment.

**₹10.53 crore was allocated and fully utilized for long-term working capital.

**₹11.20 crore was allocated for general corporate purposes and fully utilized.

**₹1.46 crore from IPO expense savings was added to general corporate purposes and used accordingly.

On co’s website it has uploaded rating certificate by Infomerics Valuation & Rating Pvt. Ltd. giving satisfactory ratings.

It is worth noting that Infomerics Valuation and Rating Private Limited (IVRPL) settled a case with the Securities and Exchange Board of India (SEBI) for alleged violations of Credit Rating Agencies (CRA) regulations, paying Rs 57.63 lakh to resolve the matter.

Question is why would a co will not cooperate will a well known rating agency and upload rating certificate of a less known rating agency. which itself has violated rules of SEBI.?

Any views on Jyoti CNC for the long term period ( 3 years), whether is buy on dips at the CMP since the Management was very bullish on the capacity expansion, revenue booking of backlog orders from EMS and the renewed defense expenditure looking at the global war scenario? Any insight whether company will benefit from iphone supply chain expansion to India especially Enclosures / casings that require CNC machining of Aluminium body ?

Results are not good, Margin falls YoY and significantly QoQ.

Revenue growth is also lower.

Company is planning to expand overseas sales & service network, with plans to set up or acquire entities in the United States and China, highlighting international growth ambitions.

Jyoti CNC stands out as a high-growth CNC machine manufacturer with impressive financial momentum, a large addressable market, and a strong technology-mix; however, major concerns around cash flow conversion, working capital intensity, and rich valuations demand disciplined monitoring and a selective, risk-aware investment approach. The following report synthesizes all primary financial, operational, and strategic insights from your uploaded documents to deliver a thorough investment framework and recommendation.

Company Overview

Jyoti CNC Automation is a NSE/BSE-listed capital goods company specializing in metal-cutting CNC machines, with substantial presence in domestic (India) and European markets through its Huron subsidiary. It operates three plants (two in Rajkot, one in France), boasting installed capacity of 6,000 machines in India and 121 machines in France.Business-Update.docx+2

Revenue for FY25 was ₹1,817.7 crore, with PAT at ₹316.01 crore and an EBITDA margin of 27%—considerably superior to industry benchmarks. The order backlog has surged to ₹4,412 crore, supplying visibility over the next 24–30 months and indicating sustained industrial demand.

Financial Performance and Trends

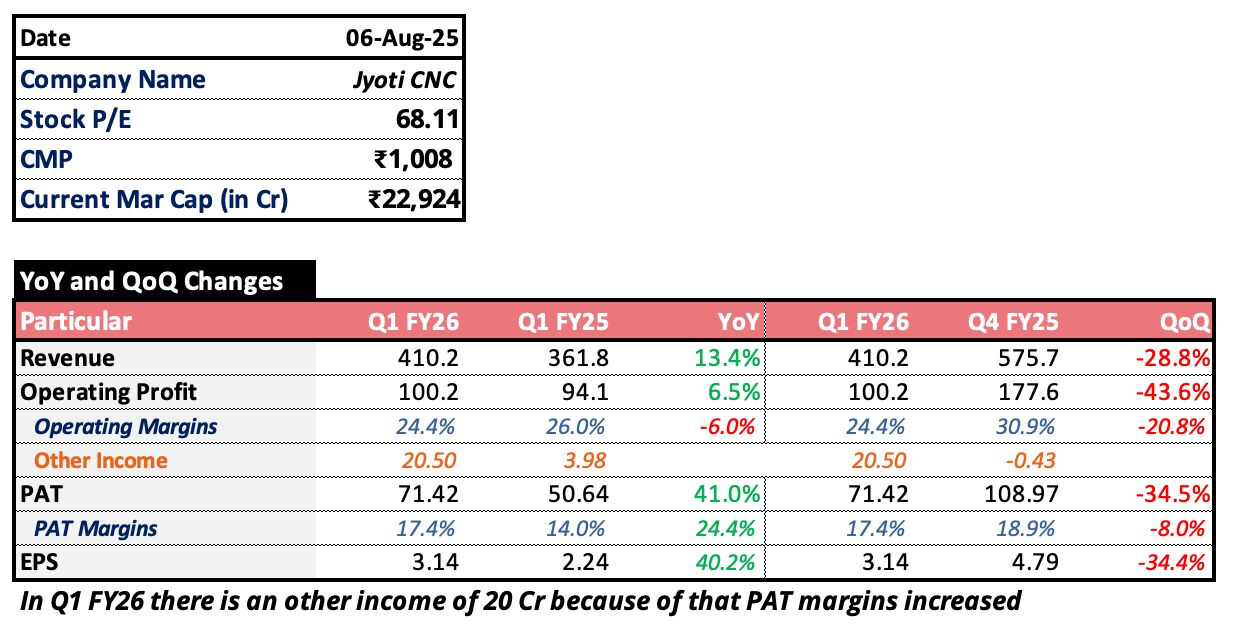

Q1FY26 revenue grew 13.4% YoY (to ₹410.2 crore), with a 40% jump in PAT and stable gross margins (56%) and EBITDA margin (24.4%).Business-Update.docx+1

FY25 revenue CAGR (FY21–FY25) stands at 33%, with FY25 PAT growth over 100%.Business-Analysis.docx

Product mix is dominated by high-end, custom machines for sectors like aerospace, defence, auto, and engineering.

Key Risks on Financials

Negative Operating Cash Flow: Despite strong PAT, CFO for FY25 was negative (₹−105.4 crore), driven by high receivables and inventory. The accrual ratio (Net Profit/Operating Cash Flow) of 15.1 is much higher than the benchmark, raising quality-of-earnings flags.Business-Analysis.docx

Working Capital Intensity: Receivable days (~98) and inventory levels are elevated. Working capital cycles have crept up to 160–170 days, requiring close tracking.

Business Strategy and Operational Updates

Management is scaling capacity to 10,000 machines/year by September 2026, with new facilities and expansion both in India and France.Business-Update.docx+1

The company is pivoting product mix toward entry/mid-level machines to serve fast-growing EMS and auto sectors, anticipating improvements in sales velocity and working capital efficiency.Q1-Concall.pdf+1

Strategic land acquisition in Tumakuru, Karnataka, will facilitate proximity to EMS and electronics customers, aiding future expansion and service efficiency.Business-Update.docx+1

The Huron subsidiary’s capacity expansion opens new opportunities in high-end aerospace and European orders, with expected pronounced impact on margins as production ramps up from Q4FY26 onward.Q1-Concall.pdf+1

Board approvals are in place for sales/service entity expansion in China and USA, targeting the world’s largest CNC markets.

Management and Corporate Governance

Promoter holding is stable at 62.55%, with a minor pledge (4%) flagged for monitoring.Business-Analysis.docx

The board has ~50% independence; related-party transactions are not material, and audit reports show no immediate qualification, though ongoing vigilance is necessary.Business-Analysis.docx

Management has confirmed no need for external fundraising for planned capex through FY26; capex is to be funded internally.

Key Risks & Red Flags

Cash Flow Conversion Lag: Increased sales and reported profits are not translating into cash, largely due to working capital build-up. Sustained negative CFO would threaten debt servicing, capex, and overall financial health.Business-Analysis.docx

Execution and Orderbook Risk: With a massive backlog, any slippage in execution, especially delays in aerospace or EMS segments where long-lead machines prevail, can affect revenue realization and investor confidence.Business-Update.docx+1

High Valuation: Jyoti CNC trades at a very high PE (60–66x) and PB (12x), pricing in rapid, flawless execution and continual margin maintenance. Any slip in cash flow or working capital discipline could cause sharp valuation compression.Business-Analysis.docx

Customer Concentration: Top-5 customers accounted for 48.6% of revenue in FY25. Loss of a key customer or delayed order can materially affect growth trajectory

Supplier dependency due to payablesBusiness-Analysis.docx

Investment Thesis

Bull Case

Strong revenue growth (CAGR >30%) fueled by order backlog and market expansion.

Sustained EBITDA margin (24–27%) via high-end custom machines and Huron.

Successful scaling and capacity expansion to serve EMS/Auto with faster turnover, driving sales and improved working capital efficiency.

Positive capex/funding discipline and margin accretion as overseas expansion (Huron, China, USA) deepens.

Improvement in cash flow conversion, with DSO and DIO dropping, orderbook translating to cash-backed profit.

Bear Case

Orderbook slippage or difficult execution, especially if prolonged negative cash flow persists.

Aggressive revenue recognition or repeated accrual buildup without conversion.

Spillover of receivables, working capital squeeze, or debt stress eroding growth plans.

Sudden slowdown or loss in demand from top customers, failure in overseas expansion.

Valuation rerating if margin/cash flow targets are missed, causing severe downside.

Valuation View and Recommendations

Jyoti CNC remains a selective, conditional long-term BUY, but only for fundamentally risk-aware investors capable of disciplined, quarterly monitoring. The strong top-line growth and margin story are offset by the risk of operational and cash-flow misexecution at rich valuations.Business-Update.docx+2

Position sizing should be moderate, and staggered—consider only partial exposure if PE corrects below 35–40x or on clear signs of positive sustainable CFO and improved working capital metrics (DSO <90 days, inventory stable, accrual ratio <5).Business-Analysis.docx

DO NOT buy on P&L headline numbers alone; require clear evidence of improving cash flows and orderbook realization before building or increasing position. Any further deterioration in operating cash flow or worsening receivables must trigger an immediate review or reduction in exposure.

Key Monitoring Metrics

CFO/PAT ratio and absolute CFO each quarter: positive trend required (CFO/PAT >0.5).

Receivable ageing: no material roll-ups above 180 days.

Inventory levels (DIO) and conversion to revenue/orderbook realization.

Quarterly orderbook conversion rate.

Related-party transactions and audit language shifts.

Staggered follow-up on new facility commissioning, Huron ramp-up, execution timelines in EMS/Auto sectors.