Came across the article in ET today.

Full news article download here.

Deal may Trigger Open Offer - The Economic Times - Mumbai, 7_15_2021.pdf (132.4 KB)

Not sure what it means to the outlook for the stock

Came across the article in ET today.

Full news article download here.

Deal may Trigger Open Offer - The Economic Times - Mumbai, 7_15_2021.pdf (132.4 KB)

Not sure what it means to the outlook for the stock

Clarification from the company to exchange with regards to the reliance new item on economic times - https://www.bseindia.com/xml-data/corpfiling/AttachLive/6eb4201b-5cf1-49ee-971c-0739adc8ec5a.pdf

No official confirmation from Justdial to the reliance news

It surprises me how even the most authentic news channels and websites report rumours as final news. There should be some accountability on such cases on companies which report such news

There maybe some thing brewing in background but all the news yesterday was as if deal is done and just announcement remains!

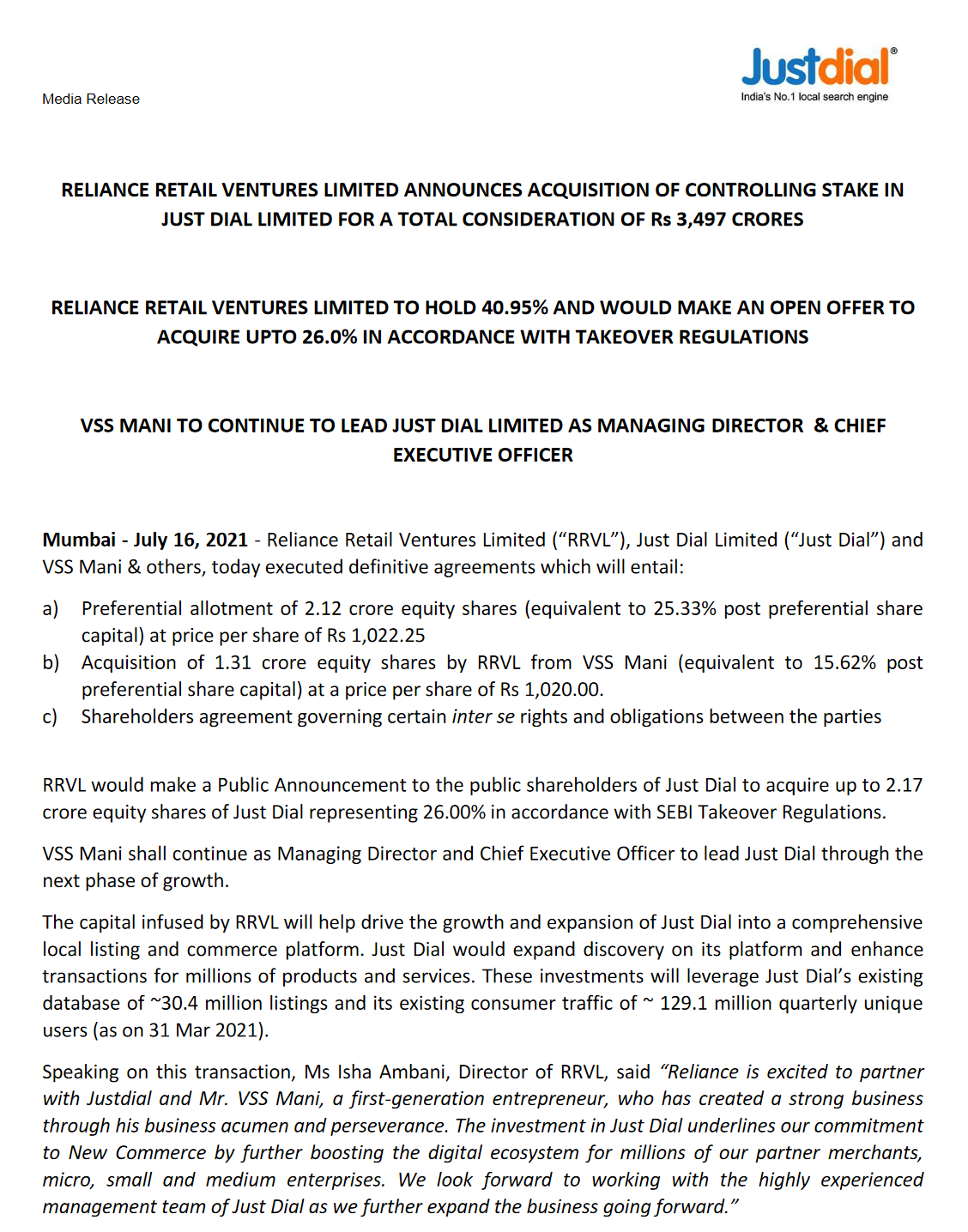

Just Dial board has approved issue of preferential shares to Reliance Retail ventures for a controlling stake.

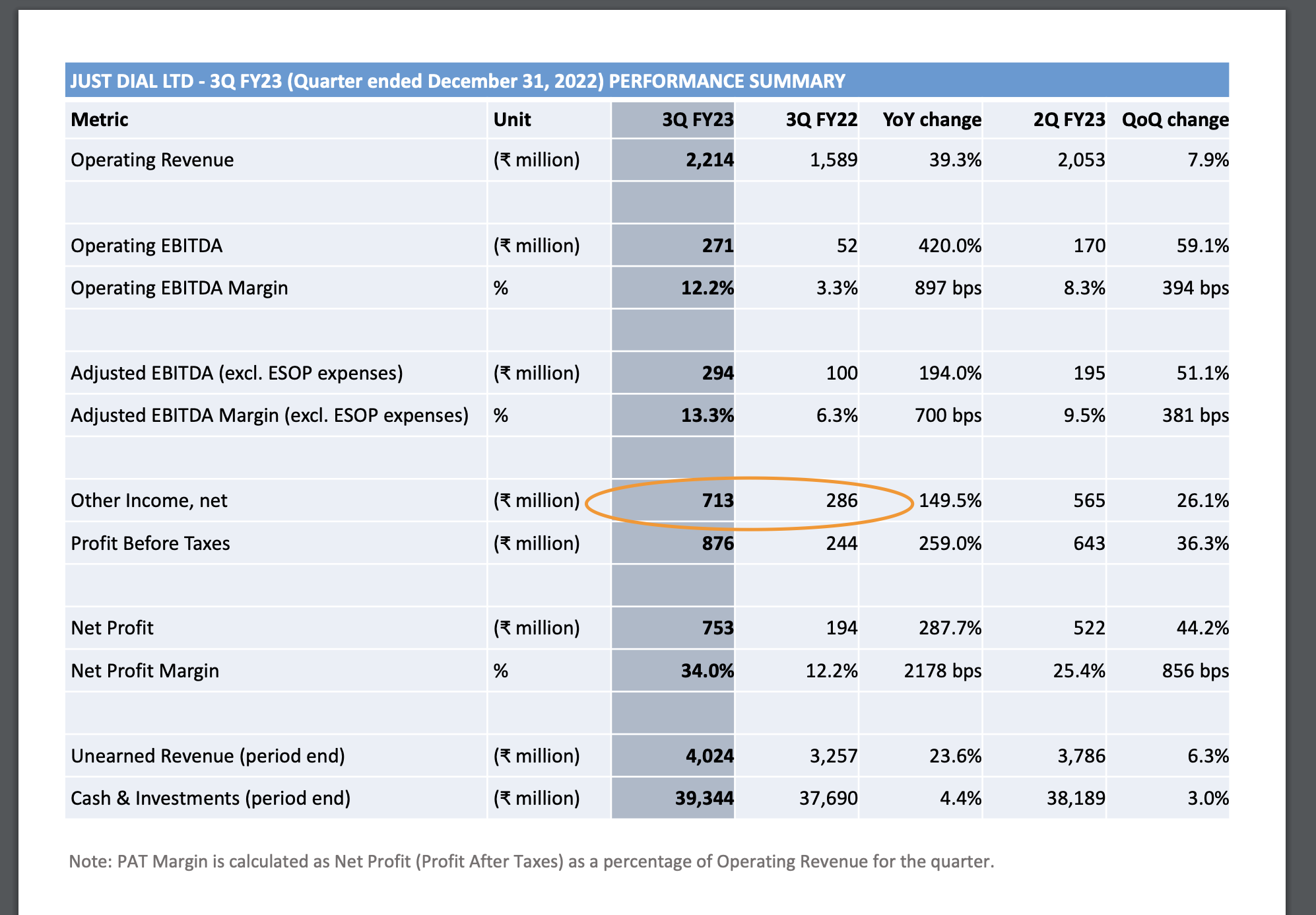

Justdial quarterly results December 2022. M.Cap ₹ 4,938 Cr

Sales ⇡39%

Operating profit ⇡421%

Net profit ⇡288%

EPS ⇡285%

Justdial, as I see, was ₹914 in April '22. Now it is ₹ 586.

Calls for a fresh look at it?

Not invested.

The Other Income line item has seen significant jump, does anyone know what it is? and is it just one time factor and hence income should be lowered down for analysis?

Other income is income from bond . They have ~4K Cr in bonds. So, it is contributing to other income.

The results were announced yesterday. I’m sharing it here.

And here is the latest Investor Presentation

https://www.bseindia.com/xml-data/corpfiling/AttachLive/09cd5f98-0718-4c06-967e-399db3d02a76.pdf

Hope you find it useful.

But this looks relatively cheaply valued considering the growth. Personal Opinion.

Few positive points

Please share your views, especially the ANTI-THESIS pointers.

NOT INVESTED as of now.

dr.vikas

Dr Vikas

I am also tracking this stock and my anti thesis for taking a position are as below:

Still above are easily manageable and any resolution of above should result in further appreciation.

P.S-Not invested till date but may take position in coming weeks.

Shankar raised a very good point of delisting scenario. Maybe the CEO wants to give dividends but Reliance is holding back and trying to pocket all cash for self use.

Disc: not invested

Just thought of sharing my 2 cents on JustDial at CMP

Thesis

Anti-Thesis

One reason the stock is so cheap is that it is the market expected “Promoter Apathy”. For Reliance, I assume a business of this size is only worth a few glances annually for Mukesh Ambani. Regardless, the business struggled to grow sales at a meaningful rate even before it was bought out by Reliance. And after the acquisition, the core business has maintained the fundamentals like OPM and mediocre (5-7%) sales growth intact.

The core business has a slow growth rate. I feel the listings space is pretty much exhausted in India. They either have to go outside India and raise the rates sequentially for faster revenue growth. Unique visitors have remained the same but listings have grown in last two years.

I initially saw some operating leverage playing out with lower employee costs when compared with FY24. But this is a business where you will need a huge sales team to stay relevant and push sales. That will hinder them from getting the kind of operating leverage certain tech companies get. So, I don’t expect a huge upward kick in the margins anytime soon.

In other verticals, it competes with players with huge moats. In B2B, it competes with IndiaMart and is nowhere near them on any important metric. JDXperts is unheard of when compared to Urban Company. Same with JD Shopping, Search and Homes. Regardless, all these are optionality’s and all of them aren’t expected to work out. Some of these competitors have a strong moat that even Reliance firepower will find it difficult to find their way into.

It has a mediocre 60% retention rate in core business. But considering how thrifty Indian SMEs are, they pay, pause and come back very frequently. So, customer churn is rarely a customer permanently lost.

ROCE is single digits because of huge cash in BS. On flip side, They have only 128 cr of fixed assets on which they generate 330 Cr of OPM, which makes it a pretty solid business.

Conclusion

I believe JustDial is a good business. Not a great compounding one (but a small potential to become one) or a mediocre one. It has a competitive advantage in the listings space. I See some intent from the Promoter to enter new verticals which is positive as the core business was a laggard before acquisition as well. The net cash and potential dividend play makes it a very safe and somewhat asymmetric bet which is hard to find in the Indian market these days. Even though it was acquired, VSS Mani still leads it with some significant (7-8%) stake.

He has the ability to try new things and be a bit more bold with the backing of Reliance.

Classic case of “Heads I win, Tails I don’t lose much”

Current Market Cap - 4900 CR and the Balance Sheet has investments worth almost 5900CR with no debt. It is gone much deep into value?