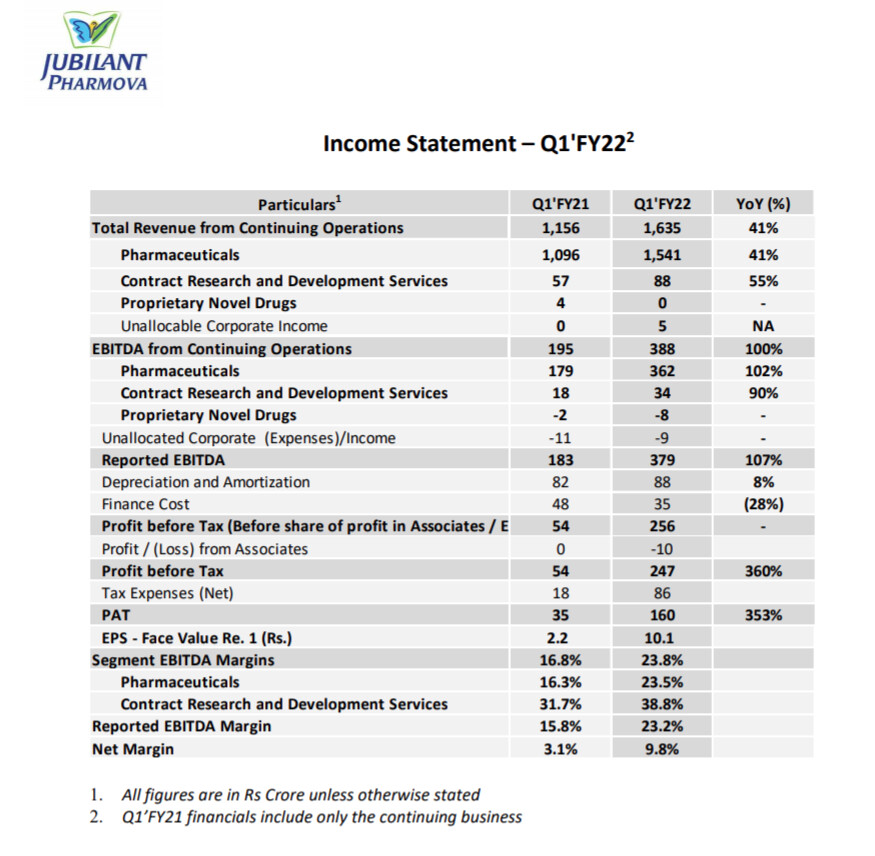

Q4 Results

3 Likes

Q4 2021 and Q4 2020 are not comparable since demerger took place in jan-Feb 2021

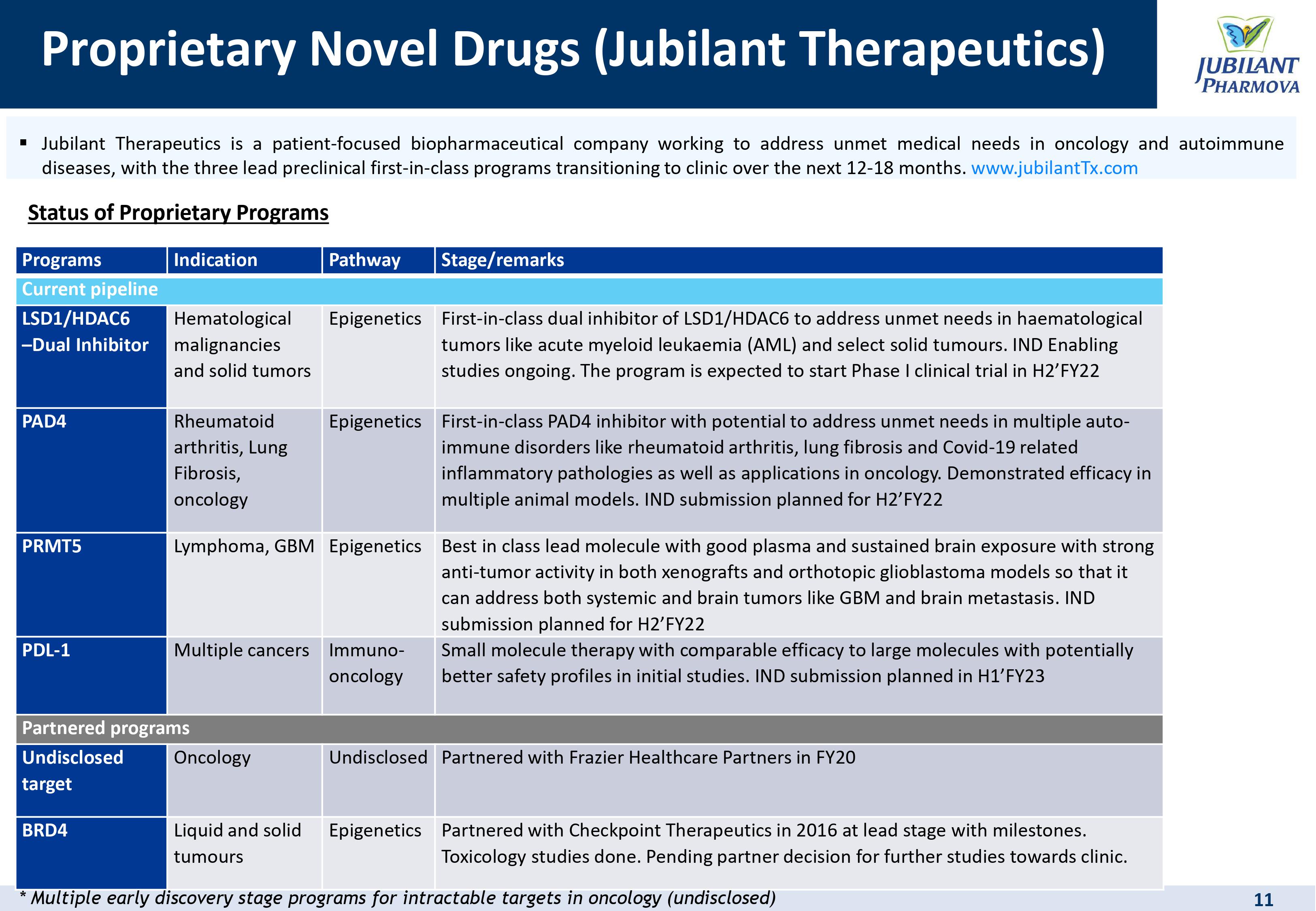

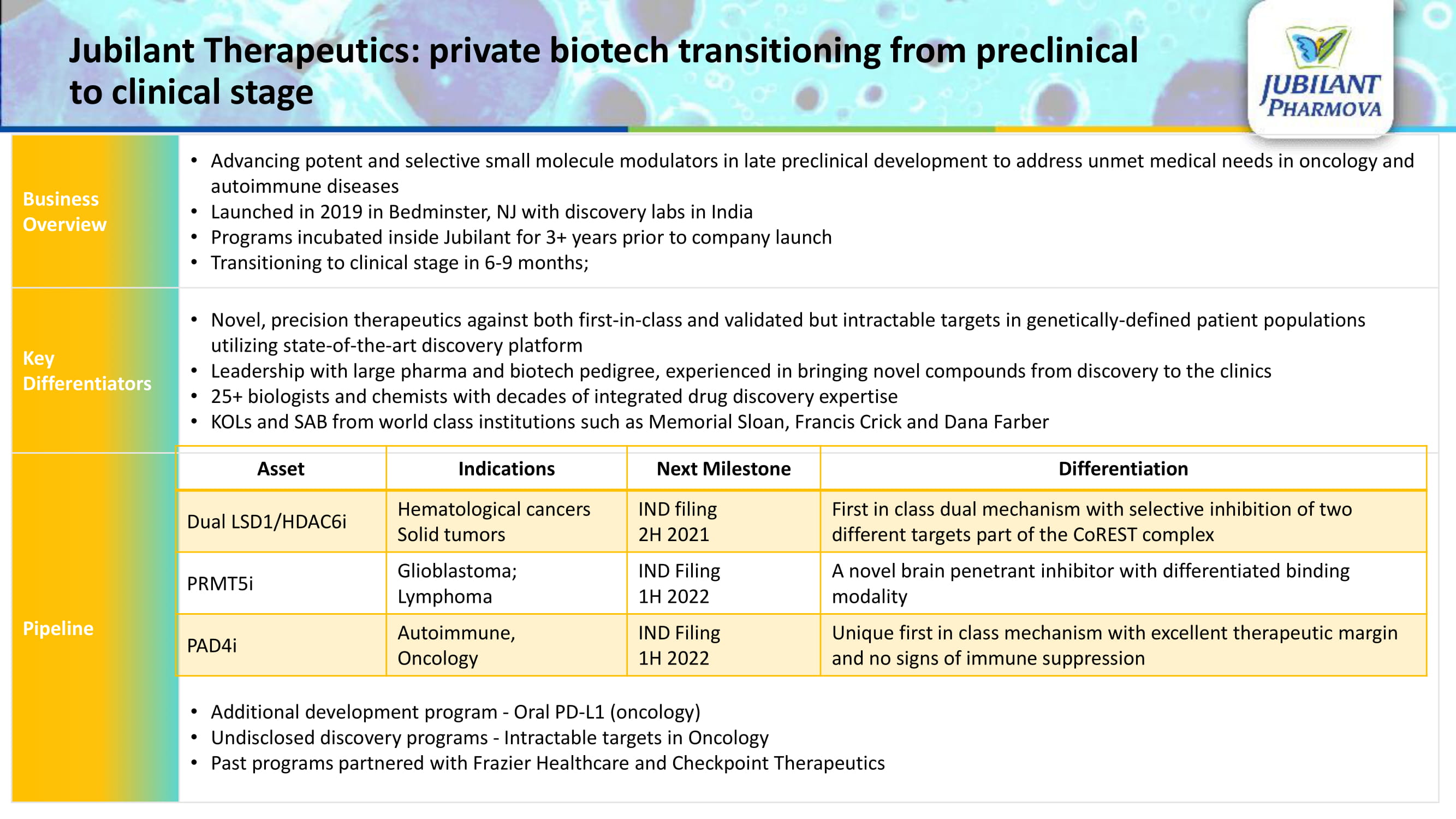

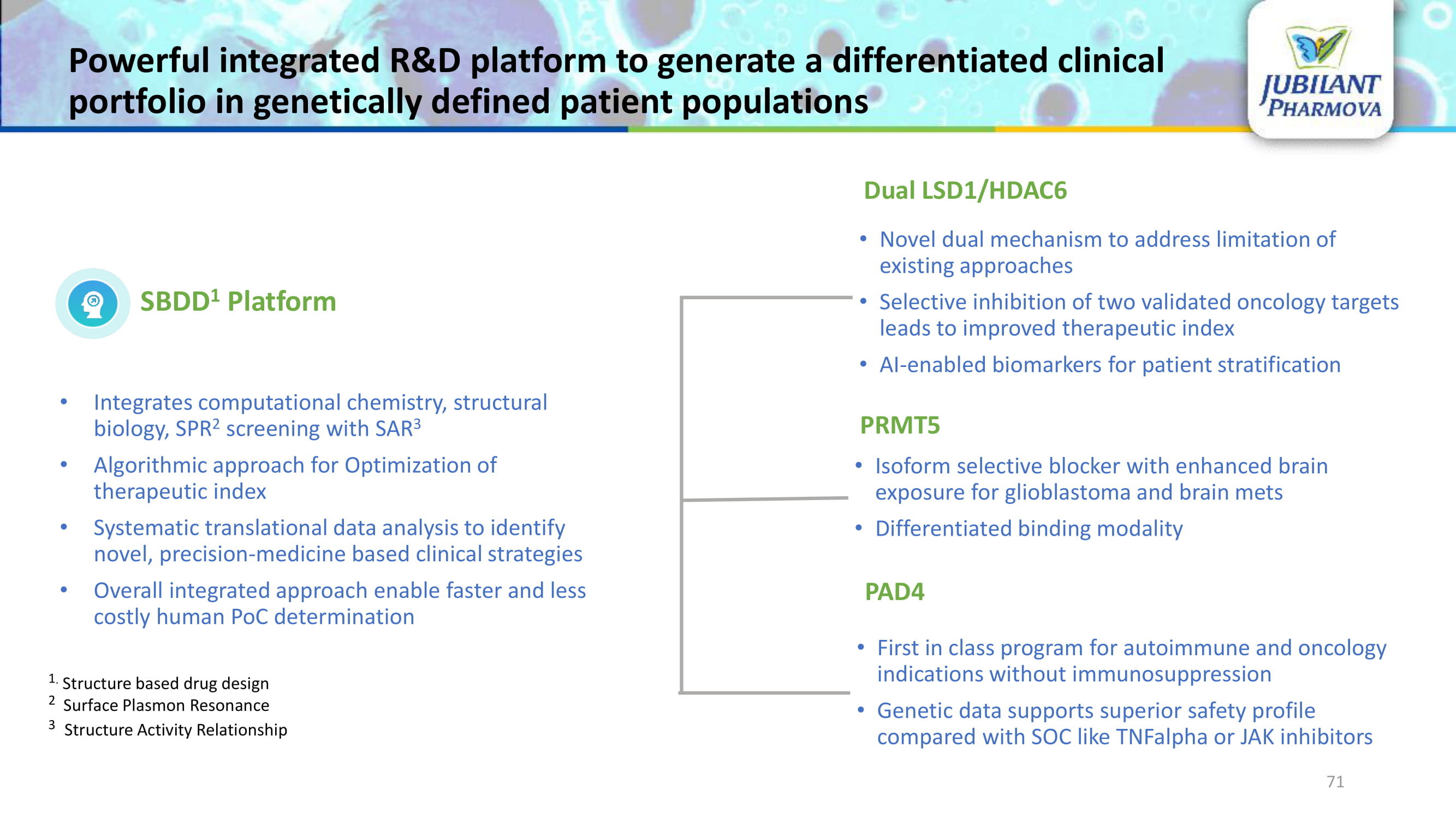

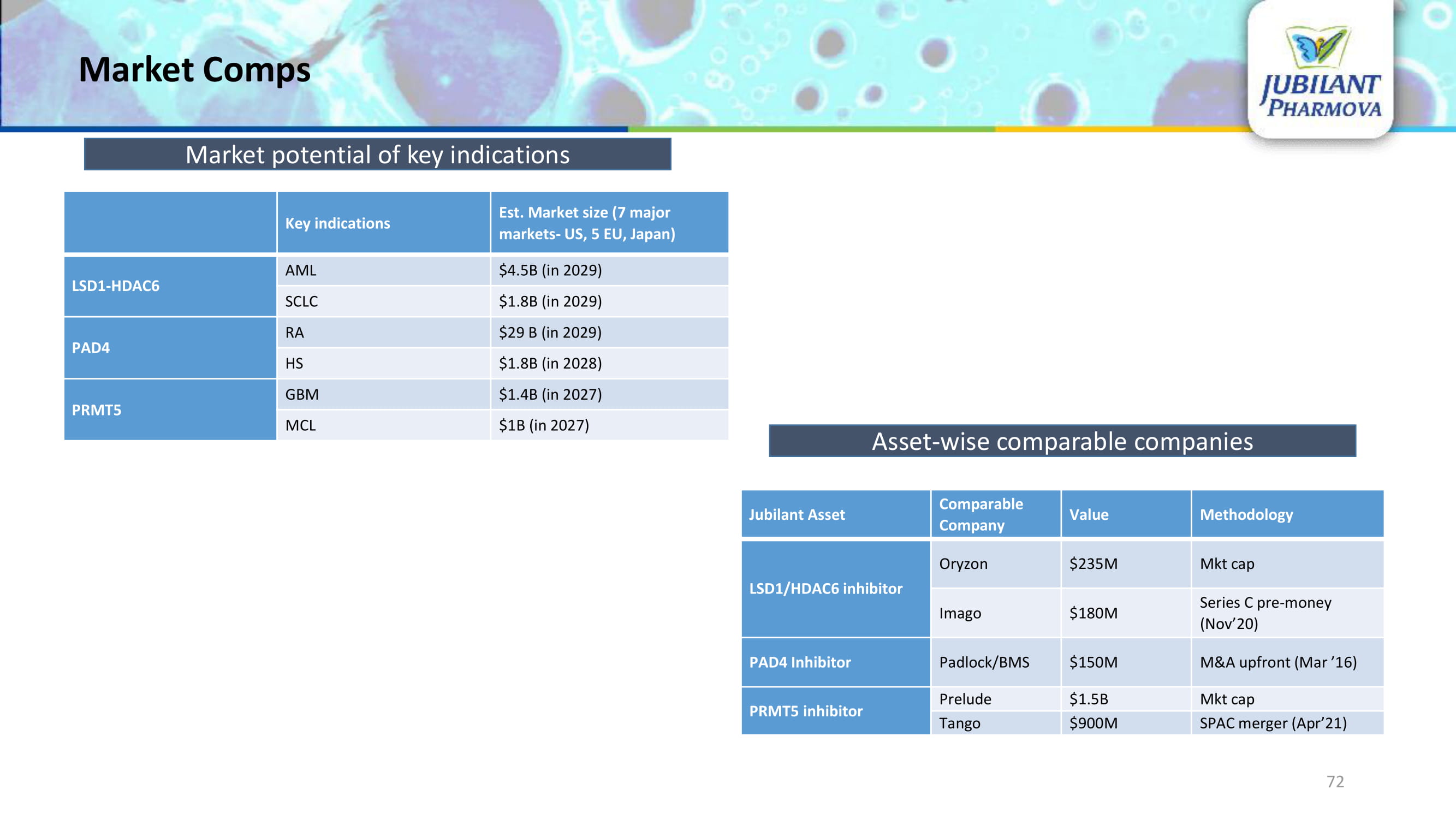

The real future value of Jubilant Pharmova lies in the success of these proprietary drugs. Jubilant has an innovator status on these drugs and would bring in a huge amount of revenue if and when they succeed.

edit:- Market Size - USD 9,143.1 Million in 2020, Market Growth - CAGR of 18.8%, Market Trends - Increasing research and development to explore novel treatment for cancer. The global epigenetic market size is expected to reach USD 36.52 Billion in 2028, and register a CAGR of 18.8% during the forecast period

Global Epigenetics Market (2020 to 2028) - Size, Share & Analysis Report - ResearchAndMarkets.com | Business Wire.

3 Likes

As per screener the sales growth (5 years) is 1.19% and as per valueresearch it is 5.68%?!

Jubilant Pharmova Analyst Day Presentation June 2021. Company seems quite bullish on Radiopharma business.

Hi, I have not yet analyzed the business model in detail but was struck by the valuation.

Does anyone know why the stock is trading at just 14x P/E on trailing earnings? A rough calculation suggests the group is generating c.1,000 cr of FCF vs. market cap of c.12,000 cr.

What is the bear thesis here? What is the market worried about?

1 Like

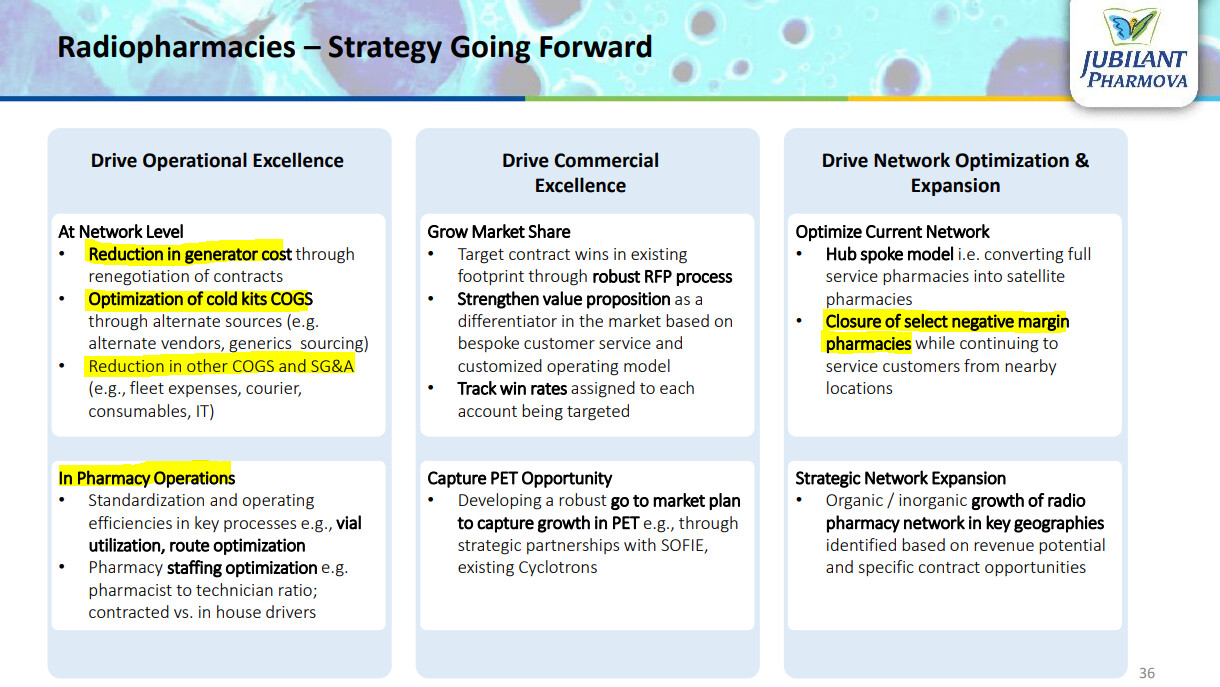

I think, a part of the reason for reasonably cheap valuations at Jub Pharmova is because their Radio Pharmacy business is loss making at present ( Radio pharmaceuticals make all the profits but the Pharmacies don’t ).

Just quoting from memory here ( i may be wrong ) - EBITDA at radio pharmaceuticals is good. However, the company clubs both pharmaceuticals and and pharmacies under the Radio Pharma business. So, the overall segment results are dragged down.

Company has a robust plan to turn around the Pharmacies in the US. And I think that its only a matter of time before it happens.

Once this is achieved, the business may get premium valuations.

Disc: invested, biased

4 Likes

Hi

For the radio pharmacies business they said this in the result

“Radiopharmacy: We are executing a detailed turnaround plan of radiopharmacies to grow top line strongly with new customer wins, expand network to service newer geographies and enhance cost and procurement efficiencies. With a detailed turnaround plan of radiopharmacy, we expect to break even in the next two-three years”

As you rightly said we can’t get the exact break up of this in the investor presentation or the results. But the AR of last FY has this data as expected. In September 2017 Jubilant Draximage Radiopharmacies acquired Triad’s business via an asset repurchase agreement.

| Jubilant Draximage Radiopharmacies Inc. | ||

|---|---|---|

| FY20 | FY19 | |

| Assets | 563.68 | 425.37 |

| Liabilities | 377.35 | 628.79 |

| Total income | 1,395.20 | 1,445.73 |

| PBT | (242.29) | (186.11) |

| PAT | (198.38) | (143.12) |

in Inr Crs

Please note in FY20 this was the largest drag amongst all the subsidiaries. On a PBT basis the worst of 49 subsidiaries. They had a slide dedicated to this in the investor deck. I don’t know what was discussed in the analyst’s call though.

Rgds

Deepak

Disc: Have transacted in last 30 days. token position

7 Likes

Thanks for bringing this out.

So…adjusted for Pharmacies, Jub Pharmova’s other businesses are doing really really well. One needs to get their hands on the latest Investor meet’s video / transcript to get some answers and management’s perspective on the turnaround plan wrt Pharmacies.

Because once that happens, the business just just get a huge re-rating !!!

Anyone having the link to the video or transcript…please do post it.

The opportunity size is huge even if a single one of Jubilant Therapeutics proprietary drug gets approved. Innovators enjoy many years of patents and have huge margins on such novel drugs, next 2-3 years would be very interesting for the company as even one approval can result in huge revenue visibilities. They have also compared Jubilant Therapeutics with other such companies and we can see the value it has just for the novel drug pipeline and its R&D work. Markets are not valuing the true potential of Jubilant Pharmova.

7 Likes

One of the biggest positive statement from management during QnA according to me is that going ahead they expect revenue from RUBY FILL to be USD $200 Million per year…Over the years, they have grown inorganically…aquiring and transforming businesses…first time they have given timeline of two years to turnaround pharmacy business…SOFIE and ISOTOPIA partnership also interesting and management sounds optimistic about more such collaborations…Rakesh Jhunjhunwala pressed hard to take a bigger risk in high margin high growth business of JUBILANT BIOSYS…Greater Noida facility launch tomorrow

Resolution of USFDA issue with two plants will be big positive…

overall good projection with first time detailed presentations about all verticals…

Discl. Substantial portion of the portfolio.

4 Likes

Jubilant Pharmova in analyst call update on twitter

Management’s focus has definitely change post the demerger and they have given strong guidance for all the divisions. Last year they had guided for a 500 cr Covid related business but they have outdone themselves, I hope they continue on the same track of under promising.

Motilal oswal’s key updates from the recent analyst’s call-

7 Likes

Recording of Analyst Meet

12 Likes

Excellent Video

Super high learning value

Highlight - RJ asking questions at 02:18 onwards

Disc: invested, feeling lucky

5 Likes

Jubilant Pharmova --Press Release --15th July21.pdf (2.0 MB)

– Jubilant Pharmova Limited (JPM), an integrated global pharmaceuticals company,

has announced that in response to the US FDA inspection conducted at its dosage formulations facility at

Roorkee during March 2021, the agency has placed the facility under import alert. Earlier, the Roorkee

facility received an OAI in December 2018 and then a Warning Letter in March 2019.

4 Likes

Q1 FY22 Result

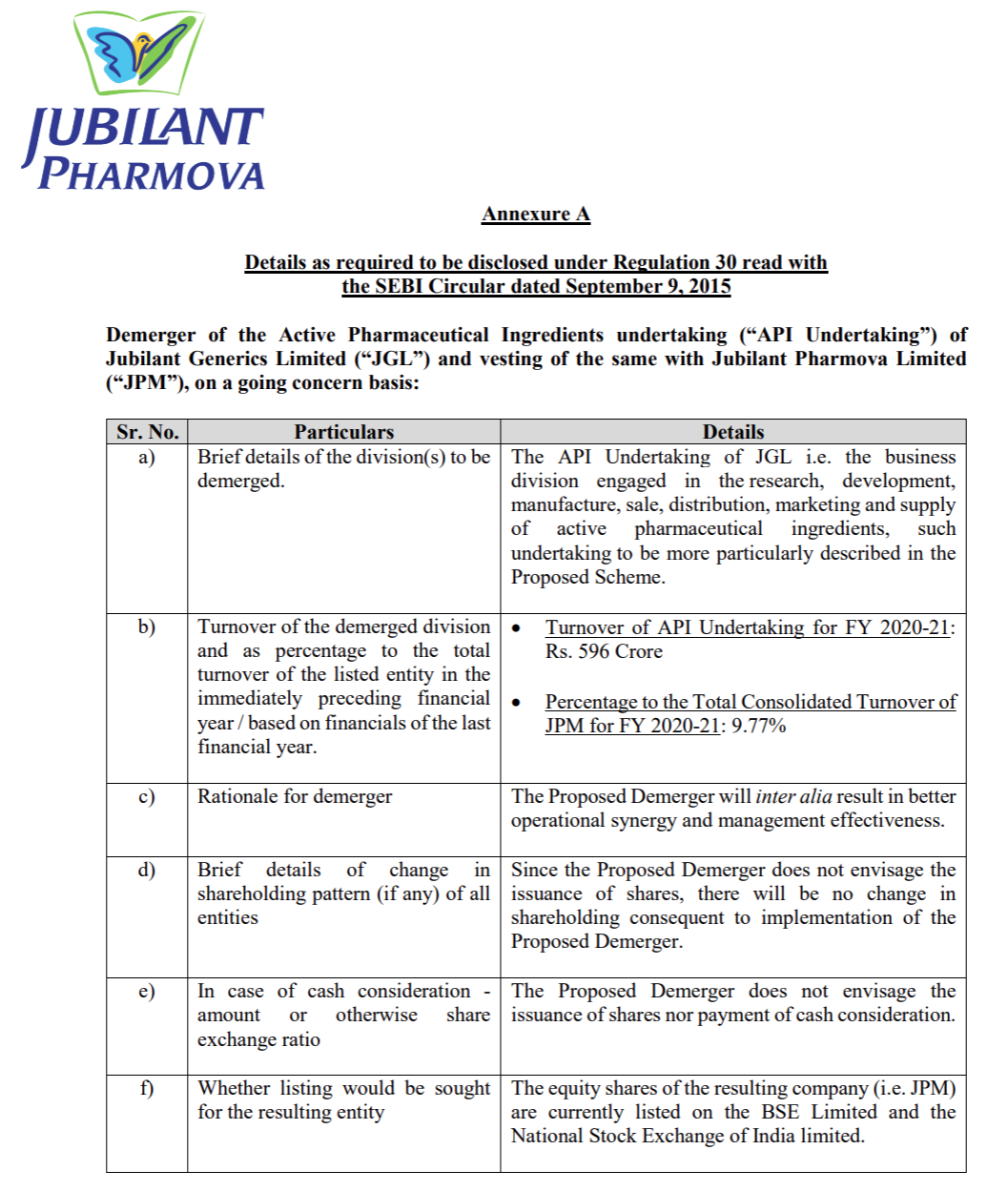

Also, The API division along with CRO & CDMO of Pharmova will be demerged as a separate entity JGL - Jubilant Generics Limited from Pharmova with same shareholding.

Disc - Invested & Biased

9 Likes

I don’t think they will list it seperately, rather the API division is being moved from Jubilant Generics to Jubilant Pharmova in order to consolidate the CRO and CDMO operations. It looks more like an internal reorganizing.

6 Likes

I think API division is being moved from “subsidiary of a subsidiary” status to just “subsidiary” status …

1 Like

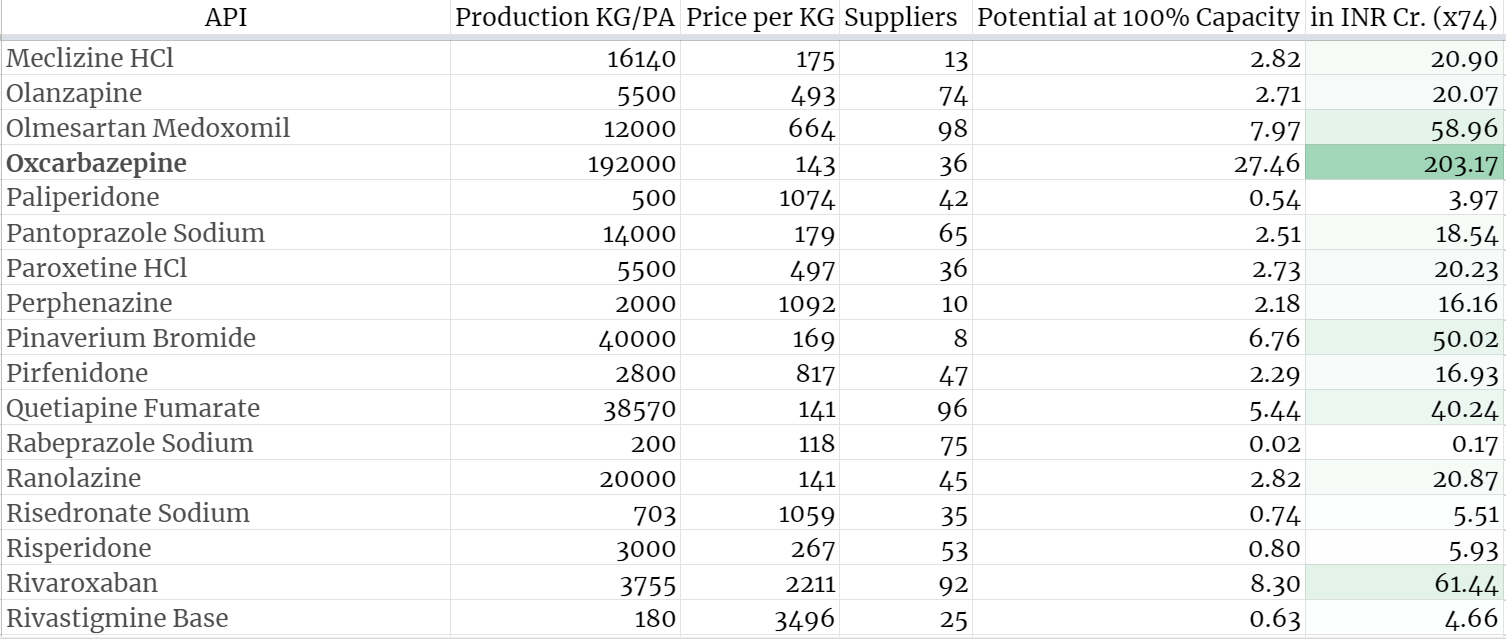

Sharing my notes from studying the generics / API business.

I’ve looked at the total production capacity per year for their API (given in the clearance report found on their website), and compared it to pharmacompass to understand key molecules, and what their potential earnings are at 100% utilisation.

The price / kg is given in dollars and potential capacity columns in million dollars. The last column gives the price in crores INR.

The strength of the green in column five tells us which drugs have the highest revenue ceiling, and I’ve highlighted them in bold.

As an exercise, assuming 100% capacity sold, the total potential revenue is Rs. 2900 crores.

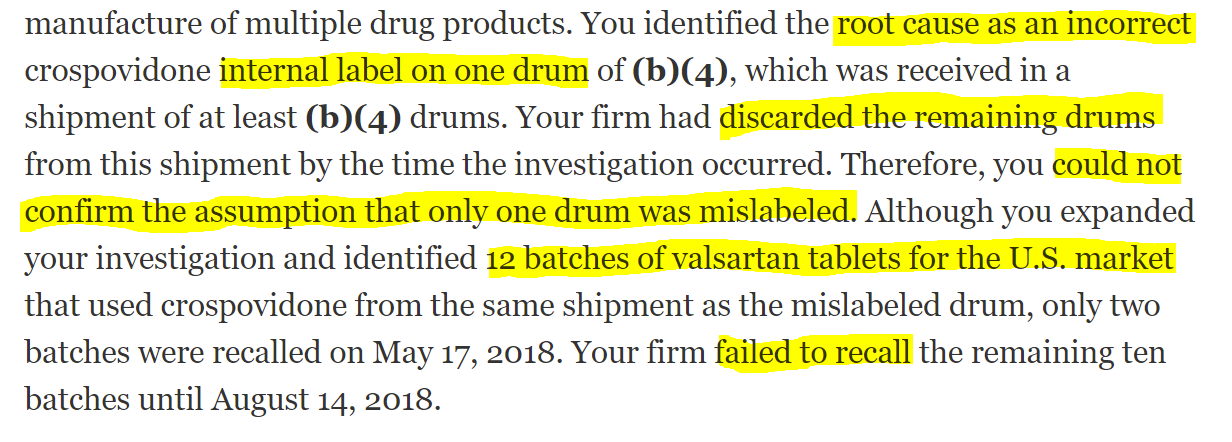

Coming to the USFDA letter:

The drugs exempted from the imported alert have a total revenue of ~ 400 crores, and we should highlight Valsartan in this list for two reasons:

-

Out of the 400 crores, Valsartan tablets make up 85% of the potential revenue from the list of drugs cleared, as they have the highest ceiling of 340 crores.

-

The original FDA warning letter from 2019 mentioned the valsartans as a problem area, so it’s positive that they’ve cleared the valsartans manufactured at the plant, and have exempted them from the import alert.

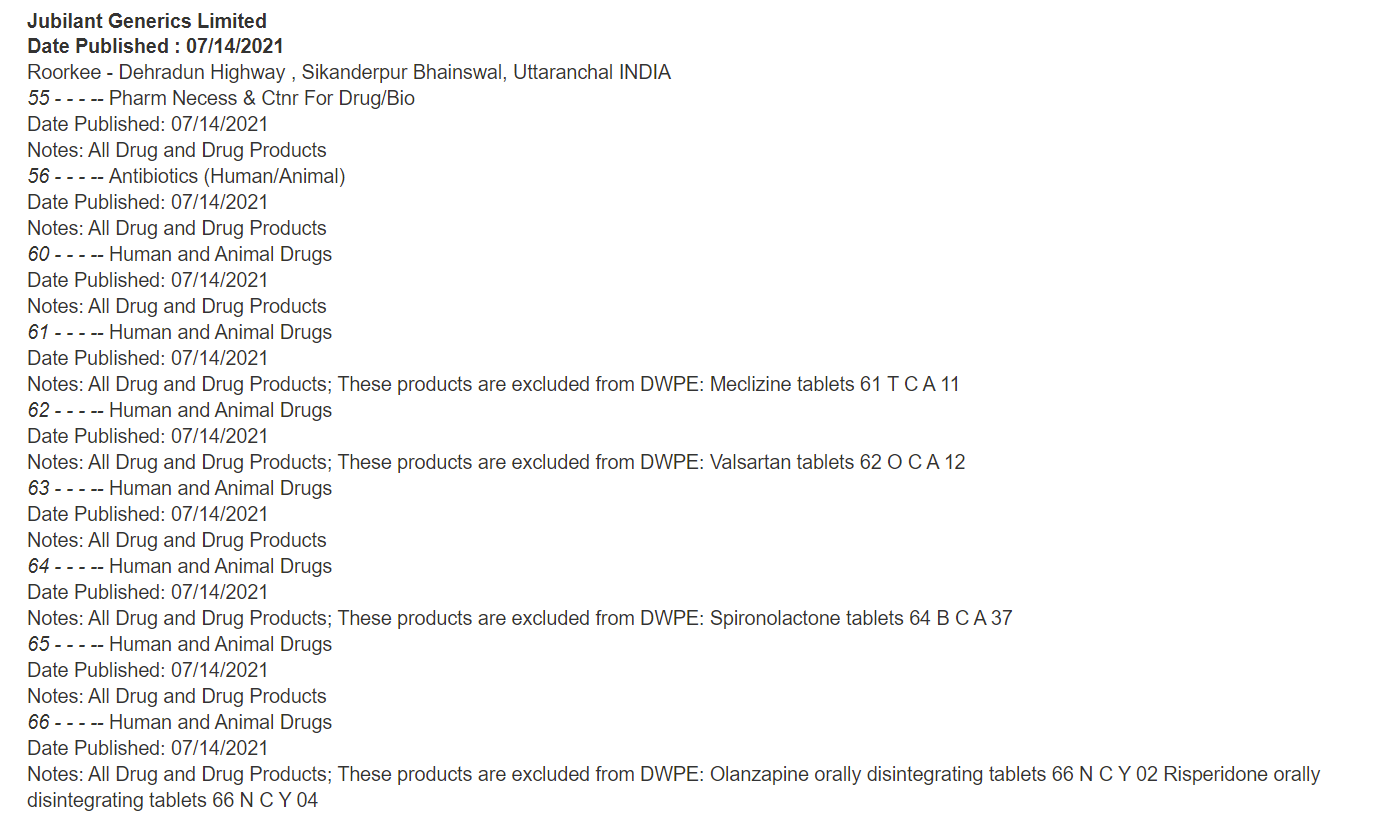

Here’s the list from the import alert. Many different countries and producers were hit on the 14th. Among the list from India were products from Shilpa Medicare, Ipca Labs, Aarti Drugs.

Here’s the full link for information:

If anyone can fill in the unknown details, please let me know. Will share workings of the radiopharma division in Canada after understanding.

Disclosure: No investments, studying.

19 Likes