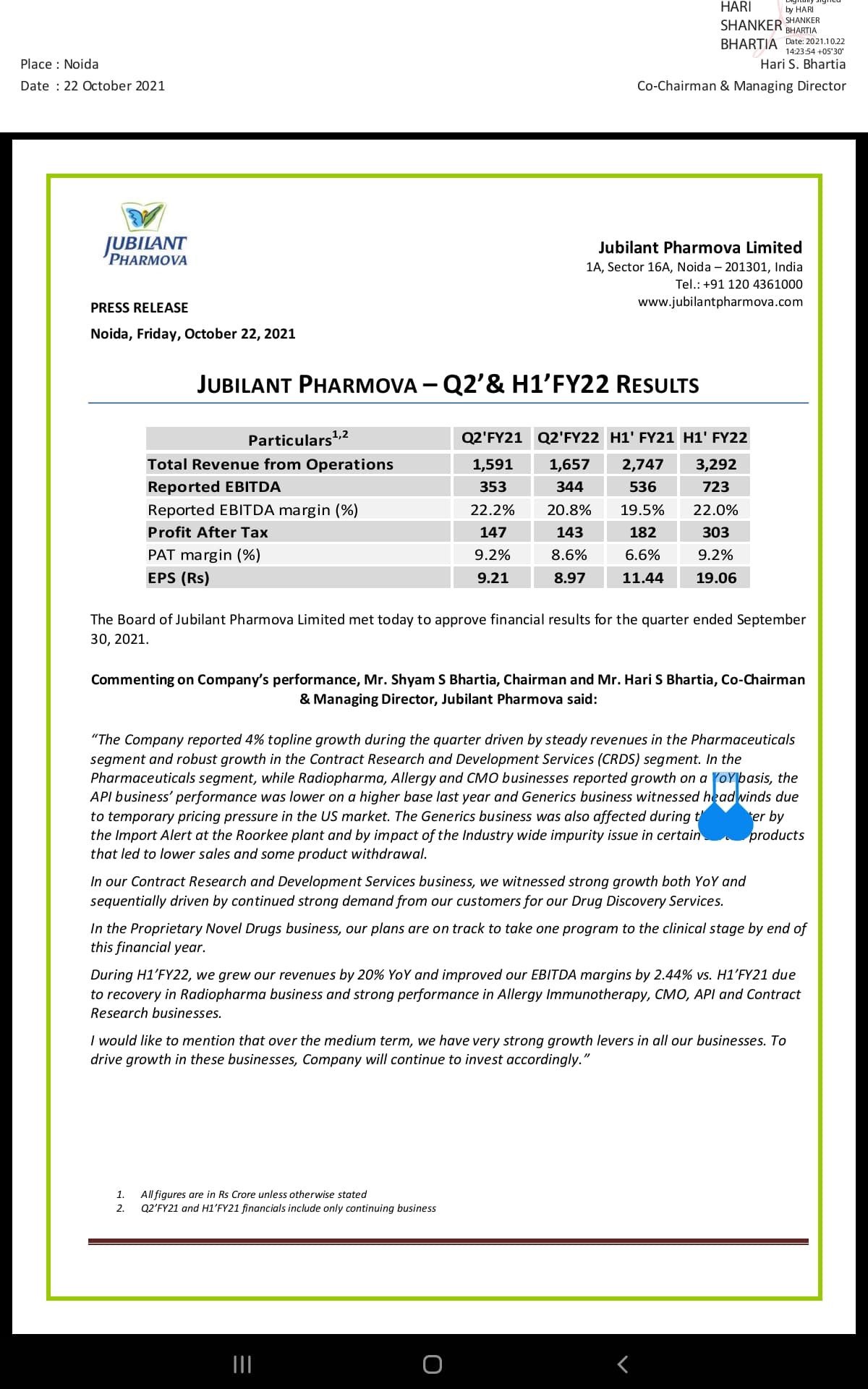

Notes from Q1 concall

- 200 cr revenue in Qtr is linked to covid, possibly 100 cr more in coming Qtrs.

- per Mgmt both YoY as well as QoQ there is performance improvement in core biz

- RoCE and RoE around 16% , expect FY22 end to see it much higher

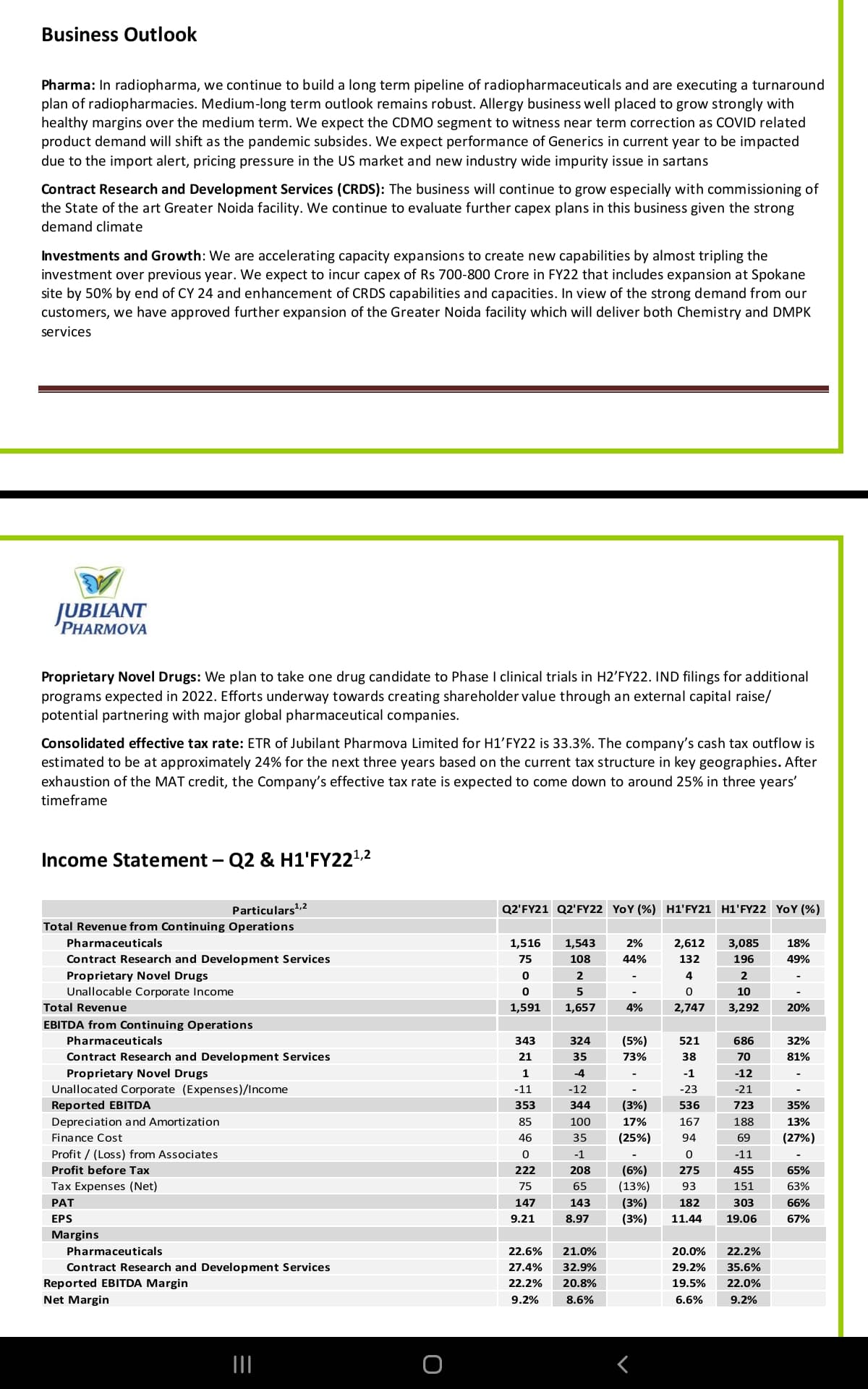

- Demerger is more of internal restructuring ( for now denied plan of spin-off in near future) to create better operations efficiency- however the restructuring gives them a high yield and high growth asset construct as well

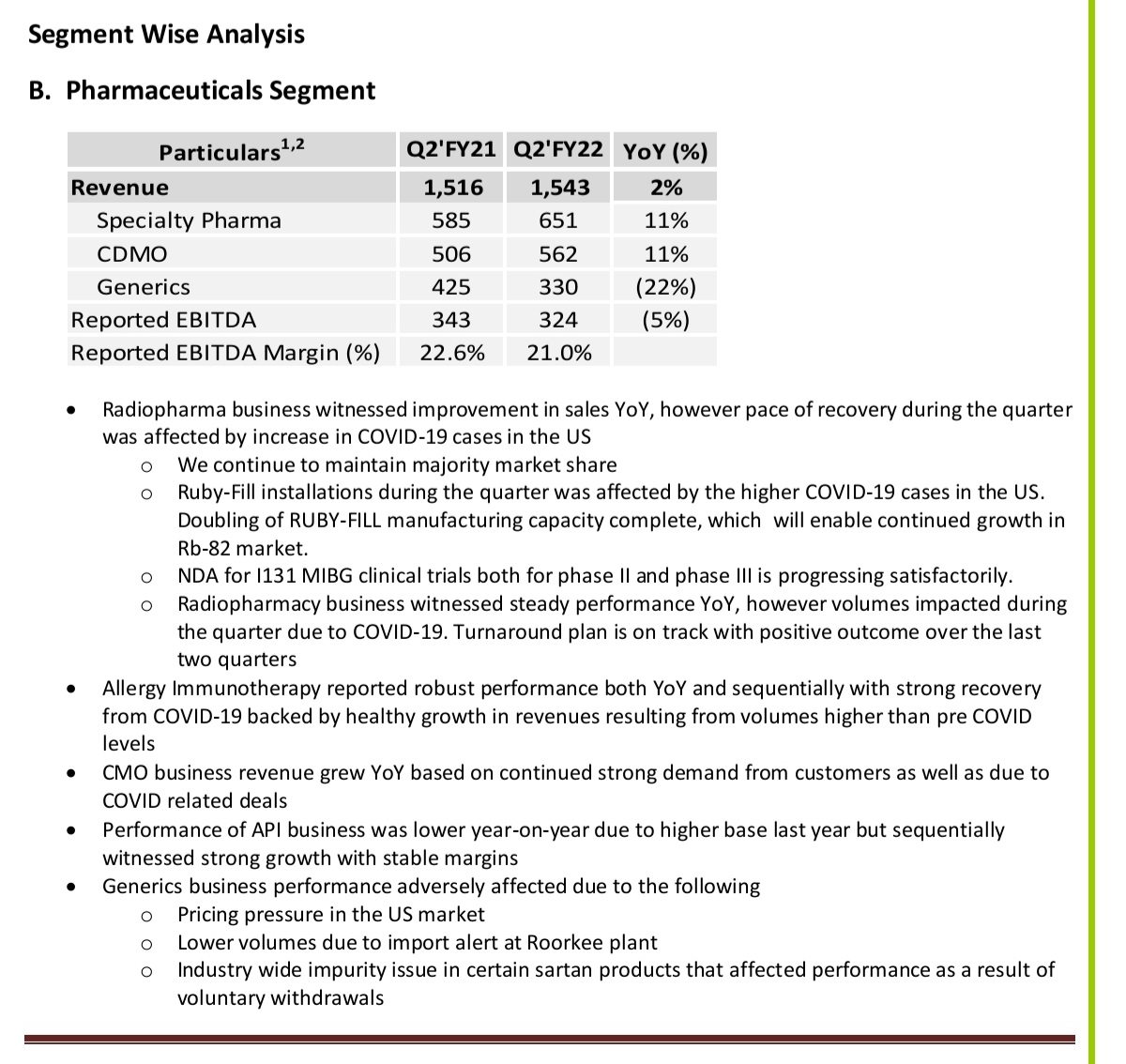

- Demand environment is good ( except Liver tests in us) - as covid related one offs go down, other biz areas which are slow will pickup thus growth continues

- Alert for roorkee facility - clear root cause not explained even though warning was already there - explanation given was on lines of areas outside warning letter were also called out for lack of cleanliness- which mgmt didn’t think will happen.

- Mitigation of revenue impact - max 1-2 month impact on areas which were cleared from alert scope( to secure third party validation…) - this is majority revenue out of facility so didn’t seem concerned per them

- Interesting call out was that Roorkee facility capacity which gets unused till alert resolution - same will be used in RoW markets

- Radio pharma biz has been in red but strategy is to use this as distribution channel to cross sell new products as well as continue to turn around by ways of operations optimization.

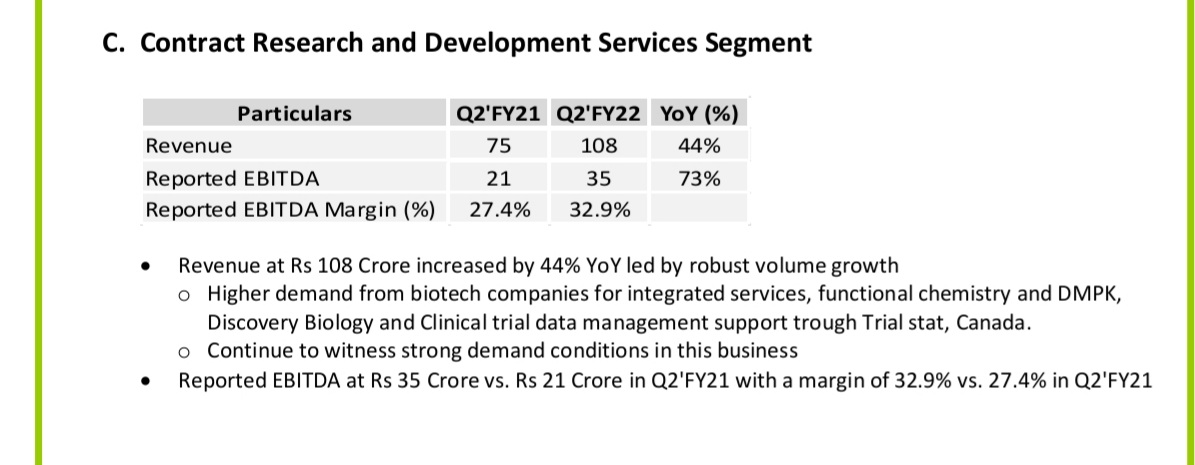

- Good demand on CDMO continues- company is keen to build and grow it.

- Novel drug biz to continue losing money - last qtr concall mgmt called out monetization in 1.5+yr, same stance continues

- Balance sheet healthier

1600 cr Qtry revenue even after taking out covid one offs should continue doing 1300-1400 cr qtrly run rate, operating leverage by higher utilization should support margin profile. Difficult to see any reasons why Annual EPS will be lesser than 30- 35 range and EBDITA at 20% conservatively( ideally As CDMO share grows this will take it up as segment margins around 40%) , after normalizing Qtrly profit runrate comes to 150 -180 cr( PAT 600-700 cr for FY22), Market cap is at 11000 cr, implying PE of 17-18 type.

Risk reward seems favorable, there is something about both Jub twins where larger market is still not giving due valuations, probably few more Qtrs to build that conviction. Ingrevia has lesser complexity and variable at play hence seems better positioned.

Invested - tracking position, looking weak on charts as of now, 660 of recent lows need to be watched for bounce back

)

)