i think Jubilant api business which is part of Jubilant Generics which comes under Jubilant Pharma ( subsidiary of Jubilant Pharmova) to come directly under Jubilant Pharmova ( Direct subsidiary) along with other 3(jubilant Pharma, Jubilant Biosys and Jubilant therapeutics)

Q3 concall

Wouldn’t be understatement to say one of the most humiliating performance and concall

- Gruesome parts( Generics, API, CMO) of biz are dragging Good performing part of biz( Radiopharma, CRDS)

- Further accentuated by lousy communications by mgmt - Q2 direction/guidance went out of window in Q3 performance

- Ususal risks of Pharma compliance already a hangover for mid term with Roorkee issue

- Nervousness on any guidance for suffering parts of biz

- CMO - This qtr no are not bottom as still has Covid share

- API - QoQ should improve, had Sartan inventory write off. Plant closure in Qtr( missing disclosures in time)

- Spec pharma- Radiopharma and Allegry holding fine and should stabilize QoQ, Pharamacy biz turn around wip - no concrete updates

- CRDS - growing well and Q3 Q4 base can be used for modeling

Learning - There is never a quick turnaround in generics Pharma, It gets worse before getting better. Best to keep a watch for signs of stability and build position size accordingly. Take mgmt words with pinch of salt esp in Generics. While valuations might look attractive relatively ( to recent past/peers) but performance might not have yet bottomed out. RJ Of the world have different risk appetite per allocation and ability to withstand opportunity cost, doesn’t make sense for retail folks.

Have tracking position - will move to watchlist now

16 Likes

Mkt Perception continues to detoriate, this one is a good example of problems spiraling, inspite of having some solid quality assets ( esp US biz), like they say turnaround seldom happens quickly, at some point it will get into value zone for patients folks.

7 Likes

Those interested in history of Pharmova , will find this article interesting , it’s a maze of acquisitions, unlike any other. Bit dated but does show that combination of opportunities & complex problems persisted much before Covid for them.

8 Likes

Jubilant Pharmova acquires 25.21 percent of Green Cure, an ayurveda company, for 8.75 cr. Green cure has a turnover of 1.87 cr, valuing the target comp at ~18x revenue.

Interestingly, sachit garg, the founder of green cure has no background in ayurveda (reference LinkedIn profile)

Disc: invested

1 Like

JUBILANT PHARMOVA : Subsidiary Jubilant Generics Limited (JGL) received a communication from the USFDA through which the latter intimated that it has decided to remove olanzapine orally disintegrating tablets, spironolactone tablets, and valsartan tablets from the list of excepted products from the Import Alert at the Roorkee facility of JGL.

.

The USFDA mentioned its review of the product supply situation in the market and company’s compliance status as the reasons for this decision. The current revenue from these three products is less than 1% of the consolidated revenues of the Company.

.

Post this currently only Risperidone orally disintegrating tablets are allowed for import into the US from the Roorkee facility.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/e50c39c1-c399-42b0-96c3-d9949e0e49d9.pdf

3 Likes

Jubilant Pharmova Limited today announced that the United States Food and Drug Administration (USFDA) has recently concluded audit of the Solid Dosage Formulations facility at Roorkee, India of Jubilant Generics, a subsidiary of its wholly owned subsidiary Jubilant Pharma Limited.

The US FDA has issued six observations pursuant to the completion of the audit. The company will submit an action plan on the observations and will engage with US FDA for next steps

5 Likes

Jubilant Pharmova’s wholly owned subsidiary Jubilant Pharma Limited, Singapore to sell its entire 25.8% equity stake in Sofie for aggregate proceeds of about USD 139.43 Million. They had purchased this stake for USD 25 Million in Nov’ 2020. The proceedings will be used to reduce leverage and for capex and other corporate purposes.

The proceedings will be received in 2 parts:

Of this, USD 113.63 Million (subject to certain customary

adjustments at closing) is expected to be received upon completion of the merger while receipt of

balance sum of USD 25.8 Million is contingent upon achievement of certain future milestones.

2 Likes

Jubilant posted it’s Q3 results today and I got couple of questions. Would be really grateful if anyone from the forum with knowledge can throw some light about the same:

-

Their Radiopharmaceuticals business is very high margin business (>50% EBITDA margins) but they are unable to scale it. Is it on account of market factors / size or Company specific inability?

-

Radiopharmacies business (highest contributor to revenue) turned from loss making segment to profitable segment (although margins are pretty thin at around 1-2%). Can there be an impact of deleveraging in this segment, which can boost the profitability of the Company, making it a turnaround candidate?

-

Reasons for continuous losses in their generics business. Is there any light at the end of the tunnel?

@phreakv6 and @ranvir I have learnt a lot about pharma companies reading your threads. Request you to share your opinion on Jubilant in case you track the company.

Disclosure: Holding small quantity, looking to increase

2 Likes

Deleveraging should certainly help bump up the consolidated results. That’s one

WRT generics - I personally think that the worst may be over. The price erosion in US mkts is down from 8-10 pc / yr to 4-5 pc / yr. Real kicker / turnaround shall happen in generics only when the Roorkee plant is able to comply with US FDA

However, I am personally happy with their de-leveraging thrust. This step alone should help save 120-130 cr kind of interest costs/yr. Hence took up a tracking position

They are currently doing an annualised PAT of say 250 cr/ yr ( going by Q2, Q3 numbers ). This 100 odd cr addition shall take it to say 350 cr. As and when generics stop making losses, radio pharmacies start making some money … PAT may well cross 400 cr levels

Disc: biased, tracking, not SEBI registered

6 Likes

Important to always focus on return on capital rather than pure marings. Radiopharmaceutical business is very capital intensive (owing to leases on both premise and equipment).

They invested in a company in Nov 2020 for $25m and are selling that same stake 3.5 years later for $113mn?! And that too through a subsidiary in a country where they have no major operations.

This doesn’t pass the smell test…

Probably the investment i’m most unhappy with myself for making

1 Like

News flow has been a mixed bag in the last 2 3 weeks.

While deleveraging and pre paying debt, renewed focus on Radiopharmaceuticals, Roorkee Generics UDFDA clearance and New Management are good ones.

USFDA adverse observations at Both Canada and USA plants don’t augur well. These plants are into CDMO sterile (most tricky from compliance POV), Allergy and Radiopharmaceuticals.

The stock is also also confused and hovering around 700 plus minus.

Not sure on the scope of revenue affected by adverse USFDA observations(Communication says Contract Manufacturing affected) . Spokane is already undergoing expansion with capacities expected to go live in FY26 and FY28.

2 Likes

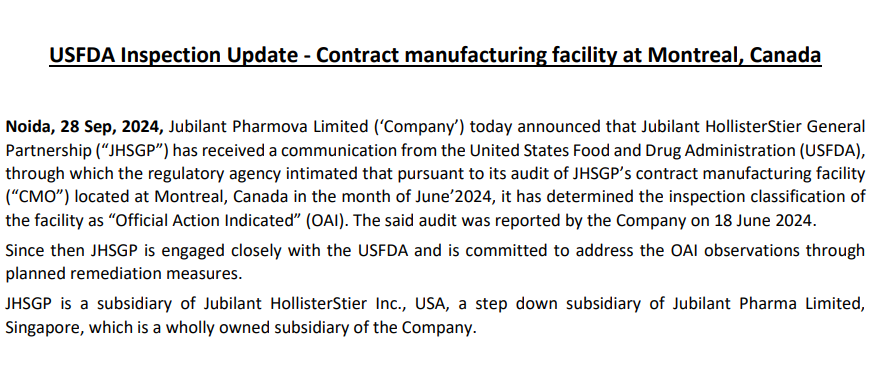

Official Action indicated for one of their core facilities in Montreal. Hope it’s not a repeat of what happened to their Roorkee plant where management failed to address audit findings flagging official action. This led to ban on the Roorkee facility and it took Jubilant 2 years to get that lifted.

Company clearly stands to benefit from several industry tailwinds (including Biosecure act) but USFDA inspection is always an overhang for the stock.

Disc- Invested

3 Likes

Latest report on Pharmova by Nuvama

I hope you find it useful

dr.vikas

1 Like