Prakash Bisht: Rajesh let me take that, I think one important point is that the cash flow for FY21 is

for H1 because this has been derived from the publish results so that Rs. 350

Crores that you see is for H1 it is not for nine months that is point number one. Two

is, that now the cash flow that we are generating is capable of meeting this Capex

requirement but as Rajesh said we strive for being debt free but not at the cost of

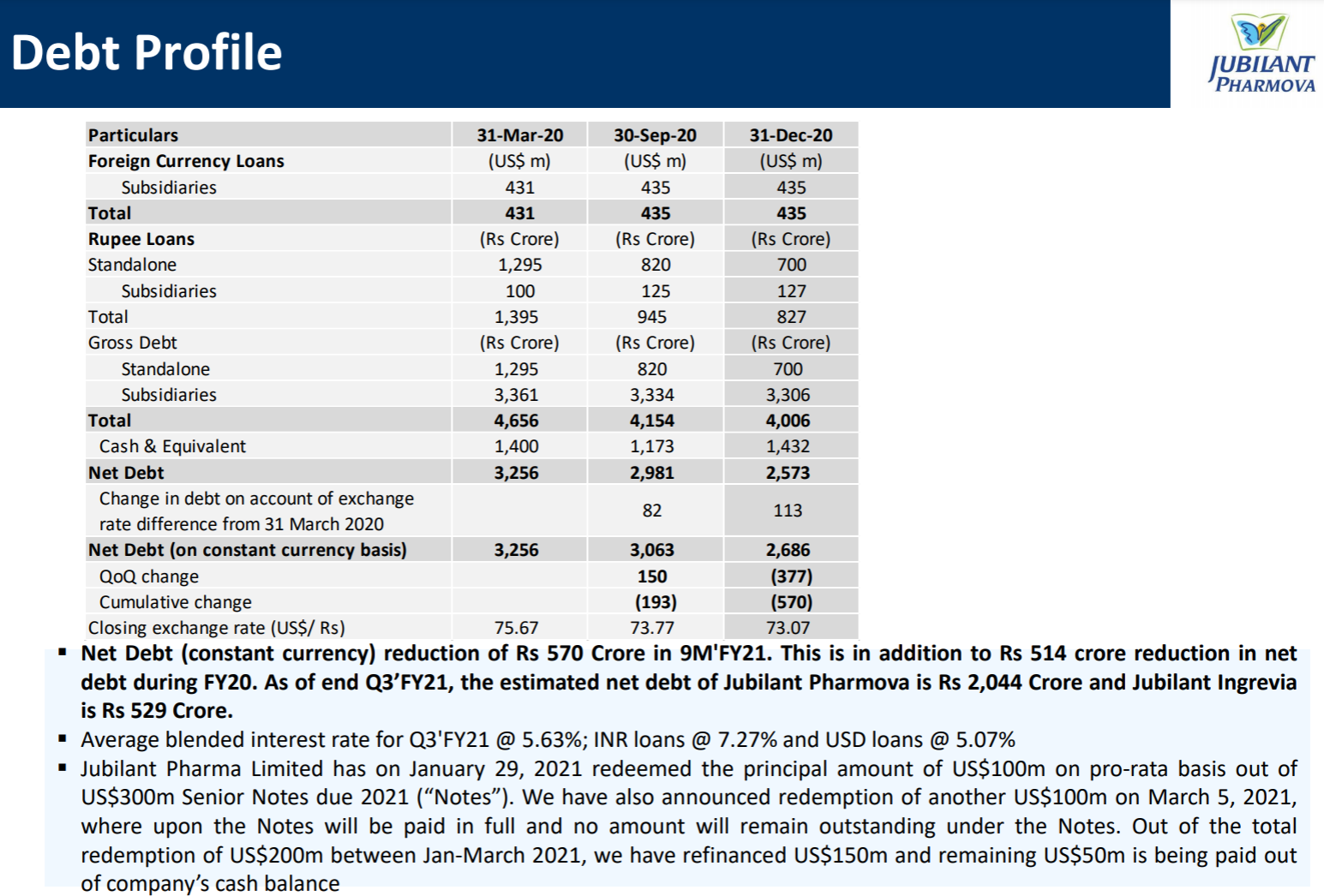

our growth. We explained you about our balance sheet, it is a very strong balance sheet, and this debt is not an issue for us so therefore you must see overall growth and the strength. We have a robust balance sheet so we are not worried 0.9X is

our EBITDA to debt so we are in a comfortable position to grow and invest.

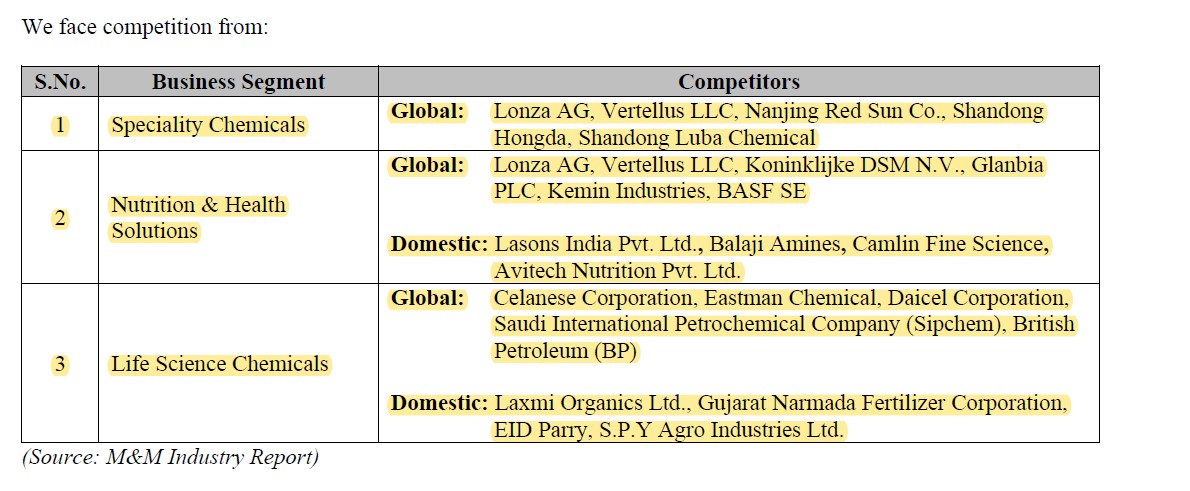

Another quote -

Prakash Bisht: And if I may chip in here Aditya, you would notice in first 9 months despite Acetic

Acid prices remaining suppressed and our revenue not growing, our profitability

has improved significantly.

Rajesh Srivastava: Right because our focus is totally on margins in that situation.

Aditya Khemka: Has there been one of cost saving in FY21, nine months which may not recur

during FY22 because of the lockdown that happened in FY21?

Mr. Khemka was trying to point out some expense cutting measures to maintain the margins which might not be recurring.

Repeated Stress on showcasing a robust balance sheet by the top management should be taken with a pinch of salt according to me.

I do not by any means want to say that the management is not honest.

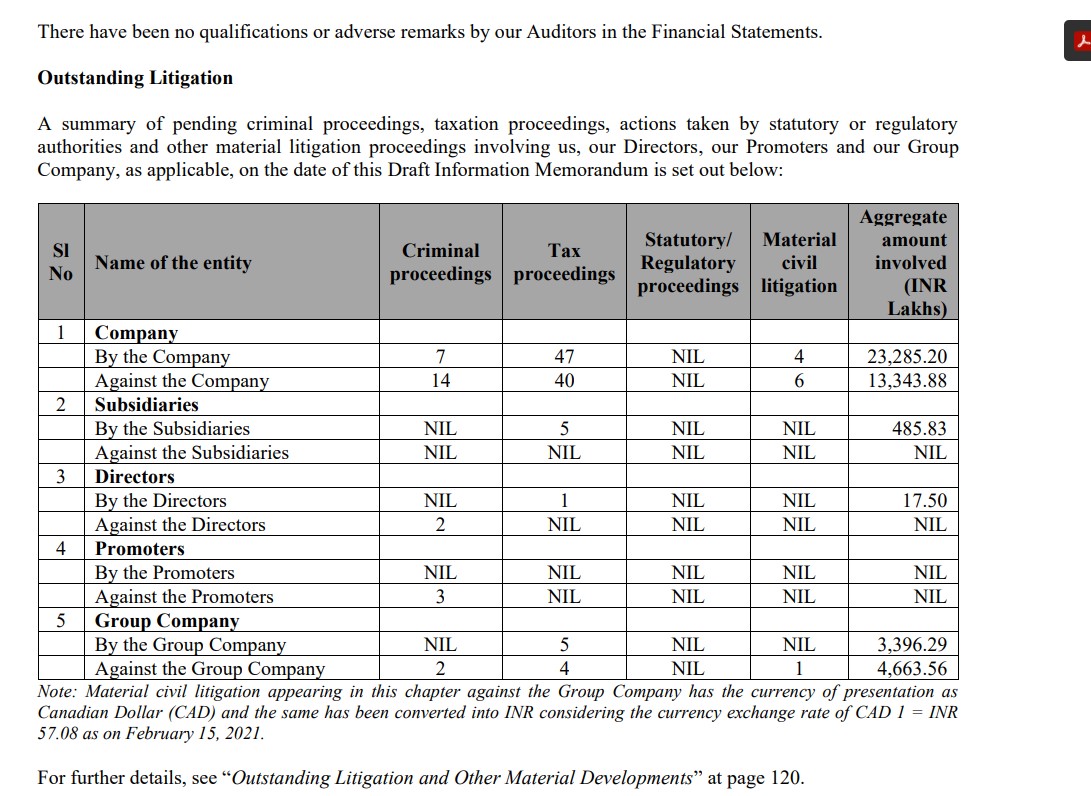

I am not sure what accounting tricks can be done in a demerger, it’s a 0-sum game as the assets & earnings will have to be either with Pharmova or Ingrevia. There seems no motive of making the picture rosy as it’s not being done to raise fresh capital for the company. This should be also taken in context of the management’s past record of good corporate governance.

Before demerger JLS was undervalued and having two separate focused business of Specialty chem & Pharma makes it much more undervalued. If you see both the sectors on a whole, they have performed well in the past many quarters which is showing in many companies & not just Ingrevia’s numbers. Both these sectors are poised to do well due to many macro factors going ahead and its up to us to research & decide which companies can do well and invest accordingly.

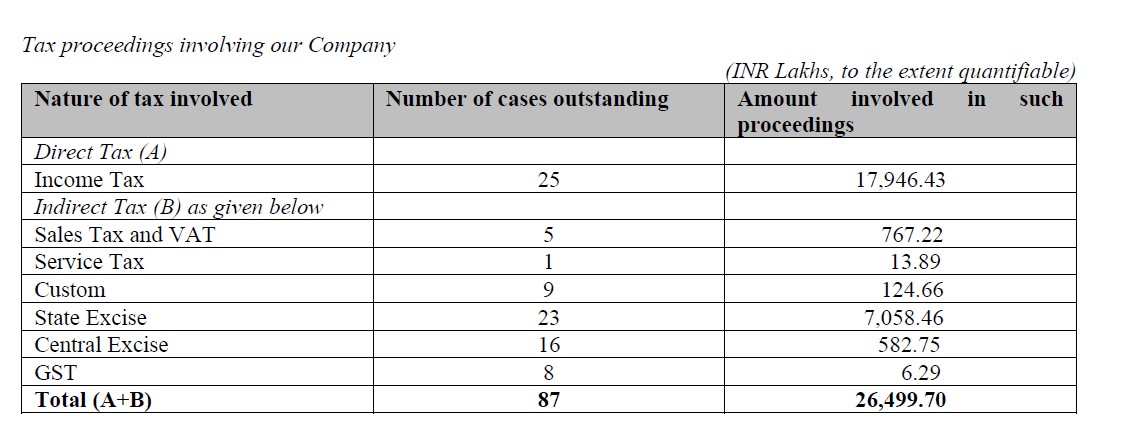

Since we do not have the official balance sheets yet, we have to take the management’s word for the balance sheet.

Also, If we look at the balance sheets for available for Dec '20 for Pharmova, they have reduced debt in this FY. They provided details in the Pharmova Q3 presentation and major part of the debt is now under Pharmova. It seems they are trying to put emphasis on having a good balance sheet after demerger as there are questions related to the existing debt & the capex plans.

Valuation is a relative term, As per my research & conviction of this business this will remain undervalued till it reaches certain value (mentioned on the first post) and I can be totally wrong about that but I am willing to risk my capital based on my conviction and research.

You should also do the research and determine if this is valued low or high. Please do not depend on anyone else’s advice for investments.

If you go through this thread, you can get most of the info. about this company and take decision yourself. If you do not understand even after reading through this thread, you should not risk your capital.

With The recent run up in stock prices of Ingrevia & Laxmi Org, the valuation gap continues to be large.

I had no knowledge of ASM before and hence, had a few additional questions i.e. criteria, life cycle and subsequent actions. In the process, I bumped into FAQ on BSE.

FYI,

Might be a trivial question but, what does this mean?

Securities shall be placed under Price Band of 5% or lower as applicable.

Also, what’s the price action to be expected because of ASM? Would prices drop because it may keep other potential investors out from buying? I know it doesnt’ change any fundamentals and hence it doesn’t change the risk profile but still curious.

For investors ASM is nothing to worry about but usually it kills the momentum of the stock as the trading volumes dry-up due to the increased margin requirements.

As far as Jubilant ingrevia is concerned, exchanges sought clarification from the company about the recent price movements and subsequently moved the stock to ASM Stage-1 however UC/LC Price Band remains at 20%. Below is the response from the company.

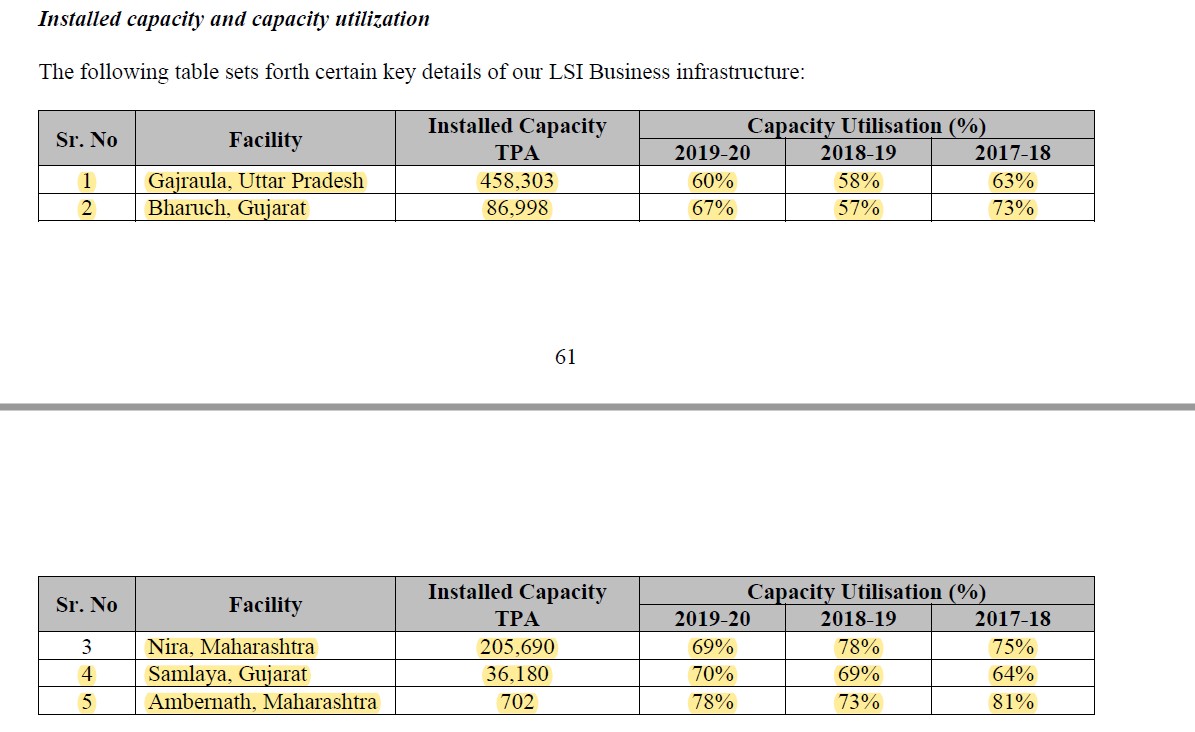

Capacity utilization of all the manufacturing units. the average capacity utilization of all units is around 70%. growth opportunity is open if CU increases gradually