Just a wild guess…

Will Barbeque Nation be the one stop shop where all other brands Jubilant Foodworks will be available - pizzas, biryani, chines, burgers?

Just a wild guess…

Will Barbeque Nation be the one stop shop where all other brands Jubilant Foodworks will be available - pizzas, biryani, chines, burgers?

It’s unlikely because the management has answered a similar question in the previous quarter’s conference call.

They want to keep all the new offerings separate until they independently develop the brand.

“In addition, we generally restrict the ability of U.S. franchisees to be involved in other businesses, which we believe helps focus our franchisees’ attention on operating their stores. We believe these characteristics and standards are largely unique within the franchise industry and have resulted in qualified and focused franchisees operating Domino’s stores.” - Dominos US CY19 AR

Hi All,

Hope you are all keeping safe.

I have recently done an analysis for Jubilant Foodworks . I’m sharing the note below and attaching the detailed excel as well. Will be good to get inputs from the minds here.

Vishal

1. Industry Overview

1.1. According to the industry estimates, the Indian FSI’s market size was pegged at INR4.2t in FY20 and is expected to touch INR6.5t by FY25 (registering 9% CAGR).

1.2. The fastest growing segments have been the Chain segment and the Organized Standalone segment at ~18% and ~13% resp. The drivers of such high growth are

1.2.1. Younger demographics – building on trend to eat out / order in without any special occasion, primarily driven by millennials (~34% of India’s population)

1.2.2. Growth of online food delivery and food tech fueled by aggregators – 100% CAGR over FY16-20 for Swiggy and Zomato

1.2.3. Investment by Organized players through network expansion in Tier 2/3 cities as well as significant A&P Spends.

These segments are expected to continue grow on the back of these factors leading the (Pre-COVID) estimate for the Chain segment at ~20% and the Organized Standalone segment at 14%

1.3. Deep-dive on QSR – key segment within Chain Market where JFL plays

1.3.1. The sector is estimated to have clocked 19% CAGR over FY15-20 to INR 188 Bn and is expected to deliver 23% CAGR over FY20-25E to INR 524 bn. (Pre-COVID estimates)

1.3.2. The growth of chain QSRs is primarily driven by international brands such as Domino’s Pizza, McDonald’s, Burger King, KFC, and Subway, which combined account for ~45% of the total chain outlets in India. These chains have established their right to win in the industry through:

1.3.2.1. Global Brand: Building on the strong global brand equity through strong investment behind expansion and A&P

1.3.2.2. Scale: Higher scale leads to higher awareness as well as lower unit costs due to better deals as well as leveraging fixed assets better, Lower costs help provide margin to delivery affordable pricing

1.3.2.3. Newer cuisines in line with western lifestyles but adapted to Indian tastes (Paneer Pizza / Burger)

1.3.2.4. Multiple channels – Dine in, Home delivery, Takeaway, On-the-go, In-transit etc. which can cater to different consumer needs

1.4. Impact of COVID

1.4.1. During the pandemic, organized standalone & unorganized (Dhabas & Roadside eateries) segments have borne the brunt of the lockdown and have witnessed severe business contraction, which has pushed a lot of them out of the market. As per estimates, ~30-40% of the formats in tier I/metros have shut down, most of which belong to the organized standalone & unorganized segment. These closures have led to capacity contraction and any incremental demand therein is falling into the chain market – leading to a faster recovery

1.4.2. Furthermore, COVID has resulted in freeing up of good quality real estate as well as notable reduction in rental costs

1.4.3. Organized players have been impacted by COVID, the delivery business as well as Takeaway business has been a boon and has helped recover the losses from Dine-in business.

2. Business overview

2.1. Jubilant Foodworks Limited (JFL/Company) is part of Jubilant Bhartia group and is India’s largest food service Company. Its Domino’s Pizza franchise extends across a network of 1,314 restaurants in 285 cities (as of December 31, 2020). The Company has the exclusive rights to develop and operate Domino’s Pizza brand in India, Sri Lanka, Bangladesh and Nepal. At present, it operates in India, and through its subsidiary companies’ in Sri Lanka and Bangladesh. The Company also enjoys exclusive rights to develop and operate Dunkin’ Donuts restaurants in India, has in operation 27 restaurants across 8 cities in India (as of December 31, 2020). JFL has ventured into Chinese cuisine segment with its first owned restaurant brand, ‘Hong’s Kitchen’, which serves 2 cities with 7 restaurants in India (as of December 31, 2020). Recently, the Company has added Indian cuisine of biryani, kebabs, breads and more to the portfolio by launching Ekdum! With 3 restaurants in Gurugram. In accordance with shifting consumption habits, the Company has also begun offering their brand-owned ready-to-cook range of sauces, gravies and pastes, ‘ChefBoss’.

2.2. The Company has recently tied up with Popeyes – the third largest global player in the Chicken category with revenues above $ 5 bn

3. Financials, operational metrics overview

3.1. JFL has seen tremendous sales growth in FY11 – FY20 at a CAGR of 21.5%. This was driven by both new store expansion as well as a strong same store growth in most years (11% CAGR FY11 - 20)

3.2. The company has grown Gross Profits in line with sales growth (strong control on inflation for RM / PM and scale benefits), while expanding strongly from 379 to 1397 stores and 90 cities to 285 cities (exit FY20). Due to such strong expansion, the PBT and PAT have grown slightly behind topline growth at 19.1% CAGR (each – adjusted for the INDAS 116 changes for comparison)

3.3. The company has consistently delivered ROCE greater than 15% (except in FY17 when Demonetization impacted the business performance significantly)

3.4. The business has gradually expanded the share of manufactured products vis-à-vis the traded products from 89% to 94%. This has allowed the business to expand its A&P spends without impacting margins significantly

3.5. The company is debt free (the debt shown in FY20 and FY21 Balance Sheet is driven by change in Lease Accounting – INDAS 116). This has resulted in strong ROE growth as well (though below ROCE to the tune of the Tax amount)

3.6. While the company did suffer a few years of negative same store growth (mainly led by very large expansion), it has since regained its strength back in its core business and has continued to perform strongly (as evident by double digit Same store growth since then)

3.7. For its entire expansion agenda, the company has not sought external debt or equity but financed it completely from the CFO generated through strong performance across the years (21% CAGR)

3.8. However, during FY14 to FY16, the company focused very aggressively behind expansion at the cost of Same Store Growth. This led to significant slowdown in sales and margins and was rectified in FY17

3.9. The company has a strong negative working capital (ex-cash) and has continuously maintained that. However, there is a strong accumulation of cash on the balance sheet which was recently used in investments in BBQ Nation and DP Eurasia. However, going forward, the company has multiple expansion agenda across all its business lines which will utilize the cash

3.10. However, there hasn’t been much improvement in the Fixed asset turnover for the business and this is a challenge with the players who are expanding in the QSR industry as strong expansion is linked to more stores and more fixed assets.

3.11. Furthermore, the company hasn’t seen similar success from Dunkin Donuts and has had to close down several stores due to expanding before getting store unit economics correct. This has also driven significant uptick in operational costs thereby reducing margins.

3.12. Furthermore, ROA has seen severe decline from a high of 23.4% to 17.1% in FY19. This is due to PAT growing at 20% CAGR and Fixed assets also growing at ~20% CAGR. However, there has been a 30% CAGR growth in both Investments and Fixed assets which has adversely affected the ROA.

3.13. There has been a sharp decline in ROCE and ROA from FY19 to FY20. This is due to the impact of the INDAS 116 Accounting, which has included Right to Use assets and Lease Liabilities for all store leases in the Balance sheet. The effect of this is the reduction on Rent expenditure, increase of Interest expenditure and increased the balance sheet size by Including Right to use Assets (Lease liability + lease payments (advance)-lease incentives to be received if any initial + initial direct costs + cost of dismantling/ restoring etc.) and Lease liability (Present value of lease rentals + present value of expected payments at the end of lease)

3.14. FY21: In the current year, the business has been severely impacted by COVID, especially in the first half. The second half is slated to grow for the business – leading to total year sales decline of 15%. However due to strong cost control, the GM is expected to increase by ~350 bps and the operating margins are expected to increase by ~100 bps. Moreover, the JFL business is the only QSR business which has shown complete recovery by Q4 – driven by its large business salience of delivery.

3.15. The extract from analysis is presented above

4. Competitor Benchmarking

4.1. Domino’s is the largest player in the QSR space and leads all players with regards to Store economics – highest store EBITDA and lowest payback period (except Subway)

4.2. The strong store level EBITDA is driven by high gross margins (very strong backend enabling this) as well as very high salience of delivery business which helps lower the cost at a store level (due to higher scale of orders)

4.3. Lower Royalty % compared to other players also helps improve profitability

4.4. Comparing to key players like Westlife and Burger King (listed players within QSR), the returns generated by JFL far exceeds the returns of both these players (29% ROCE for JFL vs 7.5% for Westlife vs -0.7% for BK – FY20). This is driven by the strong unit economics for JFL (consistently across the years)

4.5. Given the large scale of JFL, (~4X in terms of outlets, ~6X in cities), along with JFL being the only player to have their entire backend and delivery fleet owned (Westlife and BK use 3P players – RK Foodland and Coldex resp). This entire model allows JFL to leverage its entire supply chain better and thereby improving margins considerably vs other players

4.6. The store size of JFL is one of the smallest amongst other players (driven by their model of higher delivery focus). This reduces rental and other operating costs considerably.

4.7. JFL has also seen the highest Same store growth for a store profile of ~1300 stores. While BK has seen larger growth in few years, it is also driven by the smaller base.

4.8. The extract from analysis is presented above

5. Rationale for Investment

5.1. Industry Growth and Headroom for JFL

5.1.1. There is a large opportunity in the Organized FSI Space. The space is slated to grow at ~20% for Chain Market players and 14% for Organized Standalone players (FY20-25, Pre-COVID Estimates)

5.1.2. In terms of cities, Dominos has expanded to 285 cities already. However, the top 500 cities in India all have population greater than 1L each and an average literacy rate of >80%. Hence this provides a large headroom for Dominos to expand its outlet base further for the medium term. The current more manageable rate of Store growth will also help Dominos to maintain Same Store Growth at ~8-12% (historically there is -0.5 correlation between same store growth and new store expansion for Dominos).

5.1.3. The recent announcement of Popeyes is a great addition. Currently Chicken within the QSR market is led by KFC – which has ~70% share. While it is growing slower than other segments, the play here for JFL is to acquire market share as KFC has the task of category development and given that there is no other organized player in this space, this allows JFL a larger headroom to play its Value for Money proposition and thereby gain share. However, this potential would largely depend on restaurant opening targets; royalty & store economics; menu localization & extension plans

5.1.4. In the Burgers and Sandwiches segment (all day dining) that Dunkin Donuts plays in, the segment has grown to become the largest cuisine segment within the QSR space (~20% CAGR). This space is expected to get growth back in the longer term due to revival of dine in. However, in the short term, due to COVID continuing, the Dine in potential will be limited.

5.1.5. The Chinese segment that JFL has entered into through Hong’s Kitchen is said to be the largest cuisine segment but is dominated by Roadside stalls (mostly unorganized). The second segment that JFL has entered is the Biryani segment – another segment that has not been targeted by QSRs till now but has a large size from unorganized and organized standalone. Hence the addressable market of these segments is much higher than pizza. However, Behrouz, the largest player in the Biryani format, owned by Rebel Foods has still touched only ~INR2bn of revenues after four years of existence and that also after expanding reach to 35 cities. Similarly, Mandarin Oak, its Chinese brand, is still to clock INR1bn revenue. Hong Kitchen’s other peer, Wok Express (Lenexis Foodworks) did revenues of ~INR0.4bn in FY19 with 35 outlets.

5.1.6. Given the current salience and size of the Bangladesh and Sri Lanka Segments, while the potential exists for the space in these countries, the focus on expansion seems less likely given the number of priorities in India. Similar for Chefboss – while JFL has launched the product, due to its inexperience in the packaged food industry, it will continue to be a minor add on.

5.1.7. Overall, JFL is diversifying into 3 new segments which increases the potential headroom for the business multifold.

5.2. Why JFL is poised to succeed (Moats)

5.2.1. JFL today operates one of the strongest brand under Dominos and the strength of this brand is visible from the large topline growth, large potential for further growth and a business model (High EBITDA, negative working capital) which provides a ROCE of 25% - 30% year on year. This provides a large amount of FCF for the business every year (evident from the cash buildup in the balance sheet). This cash can easily be used to expand the Dominos franchise further or invest into building other franchises (Popeyes, Dunkin, Hong’s, Ekdum). This is one of the biggest differentiator for JFL vs other players in the QSR space who have to depend on Equity or debt infusion to even finance their current business expansion (due to very low ROCEs). This allows JFL to expand without depending on external capital.

5.2.2. JFL is one of the only players of large scale in QSR to have completely owned backend supply chain (Westlife has RK Foodland and BK has Coldex as 3P partners). This entire system has helped Dominos achieve a higher Gross Margins (through leveraging scale and direct Vendor management and partnering). This ~8-10 ppts higher gross margins has helped push the Store EBITDA for Dominos to one of the highest in the Industry (below Subway in QSR). Moreover, this entire system is in place to now build multiple brands of the same system (which will truly allow JFL to leverage scale benefits manifold). Hence this will become a major differentiator for JFL when it scales up other brands as it will allow for higher margins than competing QSRs even in the same segment

5.2.3. JFL is now diversifying into multiple newer segments while keeping the entire play with QSR (except Chefboss). This allows JFL to leverage its scale and more importantly its talent and learnings across brands. This also provides a larger space for JFL to grow within. A major benefit of this diversification is also to compete with Aggregators as JFM now will have an entire Ecosystem within itself and can further reduce its dependence on aggregators as well as attract consumer directly (Potential Super App Ecosystem). However, the journey to scale in new brands will be much more difficult given the nature of the industries they are in (especially Chinese and Biryani). While in Chicken, it will depend on JFL’s aggression to garner market share from KFC. However even with a lower revenue salience, these brands are expected to add to profitability faster

5.3. Other areas that JFL has successfully done in Dominos

5.3.1. JFL has a strong history of Innovation in menu and adapting the menu to local tastes in Dominos and this will be extremely essential for other brands

5.3.2. JFL has consistently invested behind Dominos brand building exercise and this is essential going forward for all other brands to build scale for them

5.3.3. In many trends on Digital, JFL has been the leader in amongst QSRs – App, Delivery backend, CRM etc. This needs to continue going forward across brands.

5.4. In terms of valuation, the current valuation of the business comes to be around ~35K INR Crs (extract from DCF attached below). However, I would not recommend sticking to the DCF valuation over the qualitative understanding of the Moats of the business and its ability to generate returns for a long time. This is because in the model, there might be under valuation of the terminal value of a business (Terminal growth assumed at 5% vs industry has been growing double digit for the last 10 years). Given the high sensitivity of the model to such inputs, I would recommend using the DCF more as a guiding light than a strict benchmark.

6. Risks for Investment

6.1. The biggest risk for JFL is the loss of the Dominos Franchise. This is the largest business for JFL and any risk of loss of this franchise can be severe for the business

6.2. Potential for Employee costs to balloon (Swiggy – Zomato Effect) - Percentage increase in median remuneration of employees has been increasing and was 13% last year. This is driven by the fact that the store employees can easily shift to Swiggy / Zomato for higher pay.

6.3. Promoter Concerns: Reduction in stake by Jubilant Consumer Pvt Ltd, pledging of shares, and the recent brand royalty proposal and subsequent withdrawal.

6.4. JFL has historically launched and failed when they launched Dunkin (due to aggressive expansion without solving for unit economics). While JFL would have learnt its lesson and is hence expanding Hong’s and Ekdum more conservatively, however this needs to be followed continuously

6.5. Gratuity Impact of new labour code can be immense due to the very large employee base (however the law is yet to be implemented)

6.6. While Management Bandwidth on managing 5 chains prima facie seems a risk, the actual risk here however is the loss of focus on Dominos. Traditionally organizations tend to provide larger resources and attention to the newer brands at the cost of the established brands but given the Dominos is the biggest brand and the reason for the large growth, profitability, FCF of JFL, the team needs to ensure that it is given adequate resources.

7. Impact of Tech

7.1. Risk of delivery business takeover by Aggregators - Aggregators like Swiggy – Zomato currently have ~75-80% Market share of the delivery market (though it has come through deep discounting). However, this puts immense pressure on even established restaurants to build their presence on Zomato as the number of consumers on their in-house apps are much lower (limiting the market)

7.1.1. Currently JFL has a long term solution to this through becoming a multi-cuisine powerhouse itself (Pizza, Burgers & Sandwiches, Chinese, Chicken, Biryani). Once the multi-cuisine propositions are established, JFL should look at building a Super App / Ecosystem for its own restaurants.

7.1.2. Given the JFL ecosystem will still have lower consumers than Swiggy / Zomato (as they are more penetrated within cities and in more cities), JFL should look to build on the 20 min delivery promise. This can be done in multiple ways – expanding closer to existing restaurants, higher number of delivery personnel, cloud kitchens to reduce rent etc. What this will entail is that within cities that JFL has entered, it will be able to continue the fastest delivery promise of Dominos

7.2. Competition on delivery business from Cloud Kitchens – Given the large plans of Swiggy, Zomato, Ola Foods etc. there is large potential competition from these cloud kitchens on faster delivery (less than 30 mins promised by Dominos). This attacks on the key tenets of Dominos brand of 30 mins promise. However, there is low evidence to suggest that this can become a thorn immediately for Dominos as

7.2.1. The business model isn’t as profitable in reality as it looks from the outside. Cloud kitchens alone won’t be able to compete with established restaurants. So there is a low chance of a single business scaling up and providing big competition to incumbents

7.2.2. The scale of cloud kitchens will allow only to compete in small micro-markets. An entrepreneur is better off buying a franchise of an established player who has a cloud kitchen model within its business.

7.2.3. Cloud Kitchens are an all-out operations-heavy food enterprise. The food is prepared the old fashioned way—a cooking stove, a gas bank, et al. The needed skillset and path to success are fundamentally different to what Aggregators have

8. Other Callouts

8.1. JFL has recently invested in BBQ Nation and Fides Food Systems. However, these have been mentioned as Financial investments with no view of taking control as of now. Hence they have been continued to be treated accordingly

9. Final View

9.1. JFL is one of the largest and most successful players in an industry which is slated to grow strongly going forward. On top of this, JFL has a stellar record of ROCE and FCF generation. While from the DCF valuation currently the stock seems expensive, we must take into note that the growth potential for this stock is much higher and hence the DCF may not correctly capture the terminal value. Hence my recommendation would be to invest in JFL.

You say DCF may not be the correct way to value JFL. Then what method do you recommend instead to value JFL?

The loved the entire thesis by you and enjoyed it throughly.

I also feel that the opportunity are immense here onwards. Once JFL builds a super app (for all its food brands) then the actual valuation will be play out.

Also i love their app, UI/UX, recommendations, analytics.

Disc: invested.

I Don’t think Domino’s USA would like that. They would be leveraging the Domino’s brand and cross selling their own products.

hey - my view on this is quite tilted towards what two people whom i respect have been saying all long - Rakesh Jhunjhunwala and Saurabh Mukherjee (Marcellus). Their viewpoint is simple - in India, funds invested in the market is much lower than in developed countries. As the funds make their way into the markets (either directly or through funds), there are not many great avenues for investment due to either shady books of many companies or no clear Moats. Hence funds will eventually find a way to companies that are clean and have durable moats. As a retail investor, my viewpoint is more towards sustainable earnings growth >10% and sustainable ROCE >15-20%. If these converge, the market cap will continue to multiply.

Happy to hear other opinions!

Nice write up. I am long the stock, so obviously my confirmation bias is front and centre! A couple of points worth mentioning - 1. JFL is effectively a cloud kitchen, 2. It is debt free, 3. The inventory turnover and working capital cycle is extremely efficient and leads to a higher ROIC and 4. The ‘Fortressing’ model is vastly superior to the aggregator model - the unit economics for the Zomato types are poor and owning the customer relationship like JFL is doing is the MOAT. Thanks for your note.

Hey - Pretty interesting. Do you have any detailed write up on the fortressing model and how it compares to the aggregator model across different situations (given right now its superior in the case of Zomato but bringing in a Doordash comparision, i dunno if numbers will hold)??

You can read about fortrseeing in their Annual Report. From a podcast interview about Dominos USA

thanks - super helpful

I agree with most of what you have written, except the last para where I have somewhat different views. I agree Pratik Pota has converted Domino’s into a cash machine, and you have described the flywheel effect quite well. I don’t intend to repeat Jubilant’s positives again, most of which you and the previous post by @vkediaonline has already covered. But all these positives are already in the price!

The main risk to the Jubilant story comes from capital misallocation. As a long time shareholder, I am okay with Hong’s Kitchen and the Biryani foray but quite circumspect of various other adventures the company has embarked in recent times.

There is no way Barbeque Nation as a business can give the same returns as Domino’s Pizza (ignoring the listing gains for the moment). In the last concall, I couldn’t fail notice that after an initial attempt at explaining the investment, Pota deflected all questions about Barbeque Nation to Mr. Bhartia.

Coming to Pizza, I don’t think one can assume the India pizza formula will automatically work everywhere. Turkey, Russia et al are very different from India, and what worked here may not work there. There is also the added political and currency risk. Let us not forget that Jubilant’s Sri Lanka operation has gone nowhere after a decade of existence. And it is too early to celebrate Bangladesh yet.

In the past, Jubilant burnt it’s fingers with Dunkin’ Donuts, and Pota is trying his best to turn it around by shrinking rather than growing it.

Little is known about the Chef Boss RTC / RTE foray - how much money has been poured in, how it has done and whether the company intends to grow the line or exit. Little is also known about the Popeye’s Chicken foray announced recently, and I will be keenly listening to the concall for more on this.

So while the Hong’s Kitchen, Ekdum! biryani, Chef Boss and several other initiatives are still in their infancy, throwing more and more money in newer and newer adventures is making me quite jittery of what comes next.

New Risk Factor

Yes - but this is true for most consumer facing businesses in the current digital era. i think we should look more at the potential unlock from the company using the data of consumers well to drive marketing and product decisions

Thanks for the post @Chandragupta. I too have been debating the past capital allocation track record here; especially with regards to Dunkin Donuts and some of the new brands they have launched. If you look at Jubilant’s cashflows, they can now generate about 700 cr cash in a normal year of operations. They can deploy about 150-200 cr of that in opening 150 new Dominos outlets. Lets assume they bump this number up to 300, thats approx 300 cr capex per year. That still leaves 400 cr of CFO. Is it reasonable for them to open 500-600 new Dominos outlets a year to utilize all that cash? I doubt it, we saw what happened when they got overly aggressive in earlier years. In that scenario, the way I am justifying the spends on new brands is essentially as an option value. They can try out new brand concepts, worst case they burn 100-150 cr over many years if a concept doesnt work. But in case any of them is successful, that opens up growth potential for another 2000 stores which will be worth multiples of the downside (even if ROCE is lower than a Dominos store). Do you think this is a fair way to justify the investment in new brands?

Yes, I agree that’s one way to look at it. You have put it well. Option Value of all these experiments is what is keeping the stock valuation also high. But since there is no way to really value this option value, it can be termed as speculative too. It is similar to how the Venture Capital / Private Equity markets are valuing start-ups.

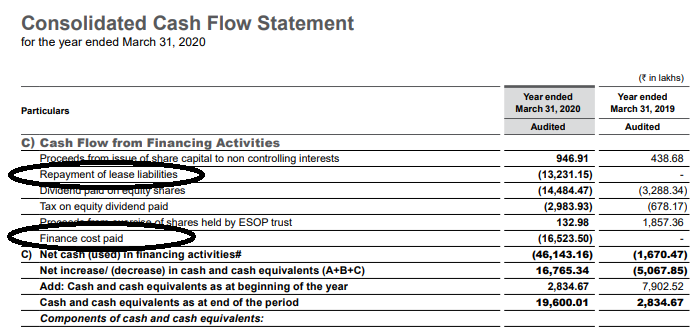

Just one point – I think Free Cash Flows should be taken as Rs.400-450 crore rather than Rs.700 crore after deducting Lease Rentals of around Rs.300 crore which are appearing in Section C of Cash Flow Statement.

Industry report.