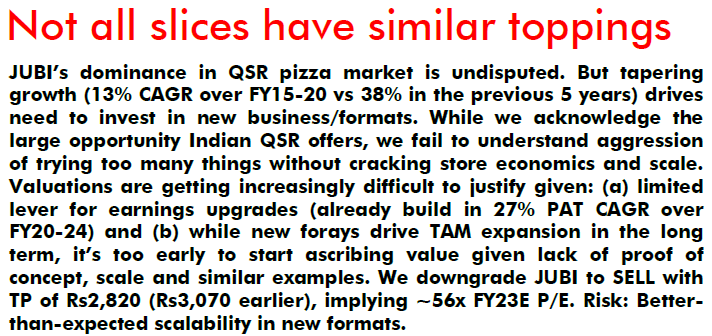

• All merits well considered; the stock seems to be significantly overvalued at current prices. A 20-year DCF with liberal assumptions of 12% sales CAGR (assumed growth tapers to 10% post FY20), steady margins and 5% terminal growth rates, one gets an implied equity value of Rs250bn or Rs1900 per share which is 40% below the current market price. The DCF does not account for the new formats or other investments but even those do not justify the current valuations.

• JUBI trades at 87x FY23 earnings which is 30-60% higher than even the leading consumer franchises such as Asian Paints and HUL. On a price to sales basis, JUBI trades at ~10x FY23 sales which is in-line with the above names. The latter also compound earnings in low double digits (albeit slower than JUBI) and have strong moats in their core segments.

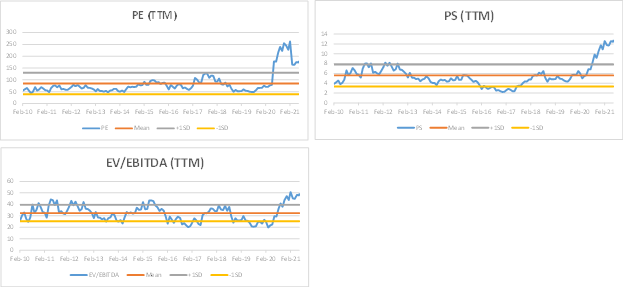

• Versus its own history, JUBI seems significantly expensive on all metrics as can be seen below. Price to sales is the best metric to use for its own history has earnings have been volatile over FY14-17 when SSSGs were weak and negative operating leverage kicked in.

• JUBI has historically traded at about ~6x sales (TTM) and in the best of times at 8x. One can fathom an 8x P/S given how the company has benefitted from COVID leading to market share gains. However, currently the stock trades at ~12x TTM sales.

• I compared the valuations of the leading listed Dominos subsidiaries globally – and there too, JUBI seems to be substantially expensive (see table below). Indian companies generally do trade at a 50-100% premium to global counterparts due to higher growth but the premium in this case seems too steep (~200%).

• At ~9-10x FY23E sales, JUBI’s current valuations are like what some of the fast growing successful starts up are commanding. For example, Nykaa is likely to be valued at US$4.5bn which is ~10-12x sales as per media articles. Similarly, the recent KKR deal with Vini Cosmetics (Fogg deos) wherein they took a 54% stake was done at a valuation of ~5x FY23E sales. These startups are in leaders in their formats and are in a hyper growth phase (40-50%) which may justify paying such a high multiple of sales. These multiples seem too steep for 15% growth business like JUBI. The Zomato IPO is valued at about ~14x FY23 sales pricing in ~40-45% sales growth. Global food delivery startups such as DoorDash and Meituan trade at 6-8x sales.

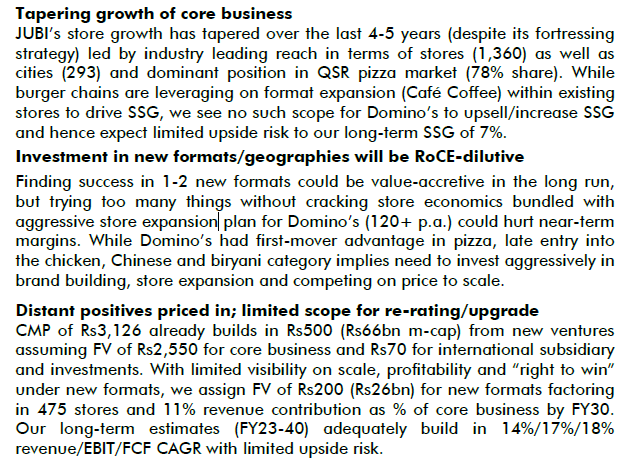

The Bhartias, like the average Indian promoters, have ‘ambitions’ beyond their core business. There has always been an intent to take the excess FCF generated by Dominos India and incubate newer franchises and formats.

JUBI secured the Dunkin Donut master franchise in 2011 and expended rapidly to 71 stores by FY16. Unit economics were ignored, and stores were aggressively added as even as store level breakeven were not achieved. There was a strategy flip flop as well – initially trying to present Dunkin as an all-day dining option with donuts & coffee for breakfast, and a burger menu for meals. Things got to a head and at its peak in FY17, the EBITDA drag on JUBI from Dunkin was almost 250-300 bps. Since the new CEO, Pratik Pota, took over in FY18, store count has been shrunk to 25 (65% cut) and the store format being downsized with menu being limited to core offerings of coffee and donuts. Dunkin has reached breakeven after nearly ten years of being in operations with 25 stores to show for it.

Over the last year or two, JUBI has launched two of its own formats – Hong’s Kitchen (Chinese Cuisine) and Ekdum (Biryani). These are JUBI’s own formats and not franchises of global formats. The narrative here is that these are large categories and don’t have a nationally scaled up QSR player. All though there might be few front-end synergies given outlets and final products are very different, JUBI can leverage its backend heft for sourcing, leverage with landlords, and apply its delivery best practices to these formats. However, there are several reasons to argue that the economics for these new formats would be inferior to the mother Dominos Franchise.

For starters, these are lower gross margin categories versus Pizza with ~60-65% gross margin versus 75% for Dominos.

These nascent brands have no customer recall in the way Dominos has and infact, there are early mover competitors who have already reached some scale. For example – in Biryani, ‘Behrouz Biryani’ from the house of Rebel Foods (Faasos fame) and ‘Biryani by Kilo’ have already reached sales of Rs1.5-2.5bn and have decent brand recall. There are few such in Chinese cuisine as well.

The new formats from JUBI would not be able to leverage their own digital assets in the way Dominos does. They might have their own mobile apps but given their weak brand equity, the only way for them to acquire customers would be via Swiggy and Zomato. The latter would thus extract higher take rates versus what they charge for Dominos. Consumers today cringe from having more than three food delivery apps on their phone. These three usually are Dominos, Swiggy and Zomato. JUBI cannot use one app to sell all cuisines as that would be a violation of their agreement with Dominos parent.

It is strange that JUBI has not exploited enough its rights to run the business in Sri Lanka, Bangladesh, and Nepal. All these three put together have just 31 Dominos stores thus far where is in population terms (~200mn) they would match a large Indian state such as Maharashtra which has ~250 Dominos stores. Given the demographics in these countries are like India, replicating and scaling up a proven model there should be have taken priority over launching completely new formats in India. Let me also add that the parent discourages their franchises from running other businesses as it risks losing focus. Seemingly, JUBI has negotiated and made an exception for themselves.

JUBI has also picked up stakes in two publicly listed companies – they picked up a 33% stake in the listed DP Eurasia for Rs2.6bn, which runs Dominos in Turkey and Russia. Likewise, JUBI invested ~Rs1bn pre-IPO for a 11% stake in Barbeque Nation, which is not even in the pizza business. There has been no clear rationale given for these except saying that these are meant to be financial investments and nothing more.

Then there is also the RTE foray via ‘Chefboss’, which is a line of gravies and sauces. This marks an entry in to the FMCG space for JUBI and they will compete here with Nestle, Tata Consumer, ITC and several other FMCG players.

I have two main issues with these diverse forays – 1) if the CEO suddenly has so many new things to take care of, he can easily lose focus from his core mandate keeping the Dominos engine firing. 2) These larger forays suggest the Bhartias drive the large capital allocation decisions in this company with the management being asked to execute them.

In the ICICI Direct video posted by @ysk above, the analyst says the market is pricing the stock at a growth rate of 17-18% EBIDTA for the next 10 years and a terminal rate of 6% thereafter. I used these numbers, added my assumptions on tax rate, capex etc. and solved for the discounting rate. Indeed, the current valuation balances at 9.50% discounting factor.

Now, Indian investors may find the expected return of 9.50% paltry but many foreign investors would be fine with it. Valuations for Jubilant will remain like this so long as interest rates remain low and Indian Rupee remains stable. That said, is 17-18% growth rate realistic for Jubilant? I don’t know. But excluding the new initiatives to value the company doesn’t seem right. Today’s valuation certainly includes expected cash flows from new businesses as well.

Thanks Chandra, for your feedback. Points well noted. My brief comments are as follows

cost of capital for my DCF is usually 11pcnt. I am an Indian investor so why should I be concerned with someone else’s cost of capital. I think 11pcnt is the bare minimum I’d use as even basic indexing in India has proven to generate that over long periods of time. Also, I dont intend to speak for the FII investor but their realized returns are in dollar terms so you need to adjust accordingly - so jubi is currently priced to give them a dollar return of 6% which is very poor if you go by what an S&P 500 index has returned over time.

I presume JUBI is at peak margins currently so EBITDA growth has to be in line with sales growth. A 15pcnt growth CAGR in sales is something I am comfortable with and building in 17pcnt for 10 years seems aggressive to me. It is not that they can’t do 17pcnt but just that I like to base my valuation on conservative numbers. My bull case should generate a material upside and not just help justify the current price (that to with an aggressive cost of capital assumption of 9.5pcnt)

on the new initiatives - in my view, we can’t start assigning a DCF value just because they have announced new forays. Like I have argued, the only time they venture outside Dominos, into Dunkin, they bombed poorly. Dunkin has been around for 10 years with 25 stores to show for it and yet barely EBITDA breakeven. Why should we then give any value to the new concepts even as unit economics and scalability remains unproven? I’d argue there is a serious risk that capital is misalloated and management bandwidth suffers. Don’t forget these guys are taking on too many new things too soon. Lastly, even if you assume the new concepts reach about 2500cr sales in say 10 years, value that at 5x sales, discount it back after netting back the requisite investments, per share value in todays terms does not come beyond Rs200per share.

Nice write up, agree to some company specific points but have slightly different industry specific thoughts. Could you pls suggest how you reached to 10% growth for next decade? This seems much below than US Dominoes growth rate as well.

Second thought, a Pizza, Burger, Coffee chain etc. is a 100 year plus business in India. Starbucks, McD etc. globally are 50+ years companies or older and still growing faster than most industries there…growing sustainably and providing decent visibility of multi decades ahead even in US…in India this industry is not even crossed the first hurdle after the start line…so a 20 year vision for them would never make us or anyone pay the valuation they currently command…

What this means is that market is looking way beyond 20 years…and thats when the growth rates would be much better that what it is today as more and more people adopt to this culture and eating habbits/busy, easygoing lifestyle/eating out etc.

Agree this is a very important aspect to look upon and think. Thanks for bringing in so much details and data points on this & related aspect.

Disc: Not Invested but tracking. Invested in some other QSR related stocks. Not a buy/sell recommendation

12pcnt CAGR is for a 20 year DCF in my assumptions and not 10pcnt. The 12 pcnt is broken unto 15pcnt for the first 10 years and much lower in the following 10 years so the average comes to 12ish. As companies reach a certain scale every few years, growth starts to taper off. For example, JUBI grew 40pcnt few years leading into and after the IPO but that has moderated by more than half now as they have grown larger.

Second, the global brands you have mentioned grow single digit (and not double) in their home markets and derive the major part of their growth in emerging markets. Dominos SSSG in the US is mid to low single digits for the last few years. Low penetration/ adoption does not naturally lead to faster sales growth although it does bring longevity of sales growth. Several industries have India at low adoption levels - consumer durables, liquor etc but sales CAGR last five years is way below 15pcnt. Likewise for QSR, pls look at the past five year sales CAGR of JUBI and WESTLIFE.

Thanks, I missed this part. What this means is that in home market, they depend only on SSGR…the store expansion/penetration is almost complete… so higher growth rates would come during periods of store expansion which would turn into better profitability subsequently… so I think maybe as you gradually taper the growth, we need to gradually increase margins & profitability?

Also, to what extent the store expansion penetration is completed in India would also be interesting and part of the valuation methodology for QSR…last couple years were blips because of pandemic so last 5 year CAGR will be battered…

I would focus on how these QSR are faring in developed economies standalone as you rightly pointed out…to understand what happens after 50-70 years of maturity… although not directly comparable but will be interesting exercise…

Thanks for info, as you are mentioning that there is sell rating on this stock, which every now and then will be for each & every stock, can you pls let us know that as long term investors…What is the time frame for this sell rating?

Your details in earlier post are very informative but not sure what would a sell rating signify for long term investors here?

Huge increase in the number of options to be granted under ESOPs. As is frequently the case, exercise price is not mentioned. However, the existing options under ESOP 2016 are being offered at Rs.10 per share, so this too is unlikely to be any different.

ESOPs have become a very non-transparent way of remunerating the employees. Better pay a liberal salary and bonus than ESOPs. I hope institutional investors start opposing such resolutions!

In hindsight, these concerns do not look significant. Well aware a bull market in progress, but at same time, there were midcaps/small caps punished in between which deserved that.

An opportunity to add/accumulate lost yet again in Jubilant Foodworks when it was consolidating at around 2800 a month back, which incidentally was the sell side target rating on the article you had shared.

40% up post the sell rating in a couple months, a leader in QSR in terms of profitability and growing vigorously digitally…

Are such sell ratings of any meaning to long term investors? I will definitely remember this as a case study for my own academic purposes.

Disc: Invested in most QSR as a small position, except Jubilant. Not easy to catch a market leader, specially if we focus on the sell side…I maybe wrong in my assessments and may prove wrong with this stock being punished in future…

i am the exact opposite of ur investment rationale…

i like the entire qsr space but invested only in jubilant foodworks…

my reasons to invest were…

good management and great capital allocation history

high growth forecast in qsr industry ( one estimate forecasts 19% cagr upto 2025)

pizza as an industry itself is higher margin than burgers or chicken…sandwiches being the next best (which is why reliance seems interested in subway)

jubilant has shown substantial growth numbers and they plan to continue the stores growth of 130-150 stores per year

With popeye…Ekdum…Dunkin and Dominos…hong’s kitchen…eventually they might foray into a super-app which caters to all cuisine deliveries under a single app

significantly high cash flows

Dominos as a brand has “creeped into our habits” which may not be true for mcdonalds or burgerking…

evidence for the same….???….two points…

a) in FY22Q1…the entire country was in lockdown and ppl were avoiding all outside food…yet…jubilant managed to do 85% of sales in comparison to previous quarter

b) Jubilant decided to charge 30-50 rupees as delivery charges…and nobody seemed to mind at all…

My 4 year old is a fan of the garlic bread…and my wife somehow doesnt seem to see it as “junk food”

(thats what lead me to believe…this brand/product has creeped into our habits)

And as Mr. Damani always says…invest in companies that become a part of your habits…these businesses are the most sustainable and last ones to be disrupted.

Disclosure: Invested in 2019…first purchase was at 1200…and have been regularly averaging up…This was one of my first equity purchases in my PF

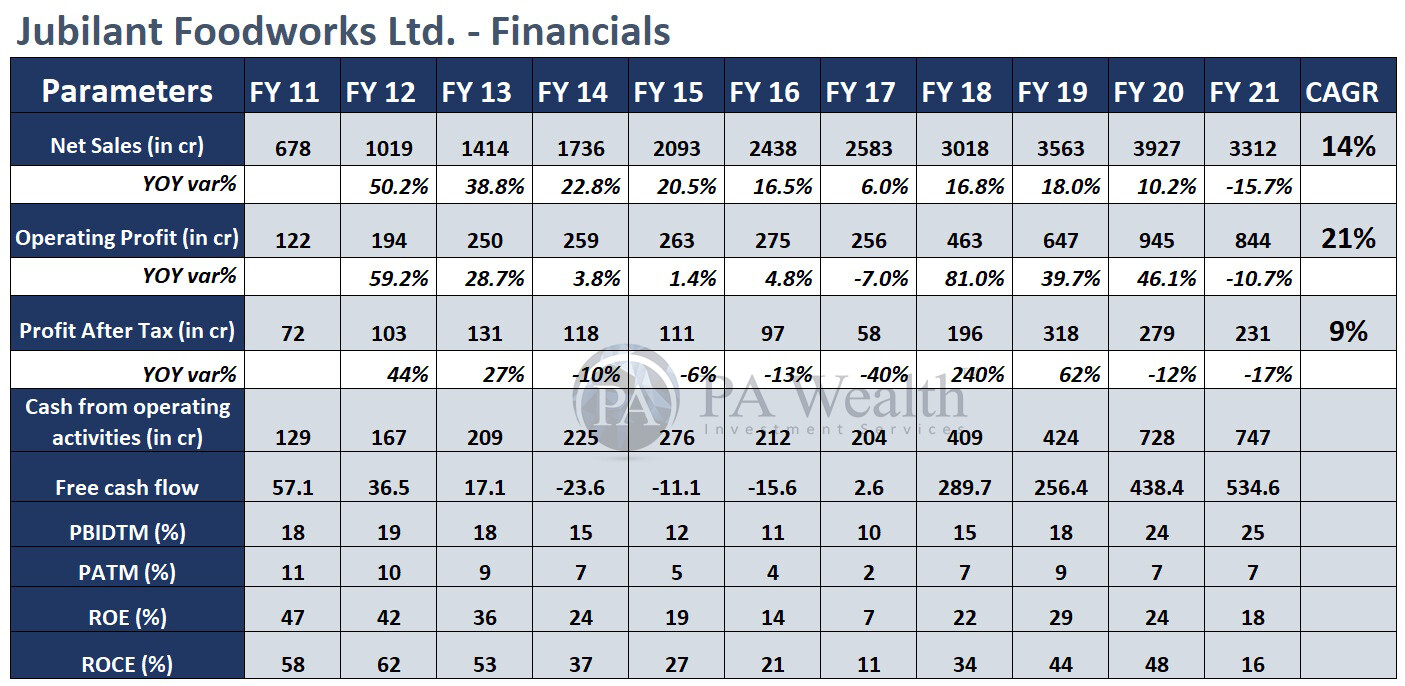

Some Inputs on Financial Performance of the Company - Jubilant FoodWorks Limited

(old to latest)

In FY17

The Profit after tax of the company decreased by 27%. The main reason behind this negative growth was the increase in total expenditure which mainly include increase in selling and distribution expenses, Raw material expenses and personal expenses. Further the restrained market situation and demonetization which happened in Nov,2016 also impacted Domino’s pizza sales. As a result same restaurant sales growth (SSG) for the year, also stood negative at -2.7%.

Further the cost of expansion affected the EBITDA margin of the company.

In FY20

The company reported negative growth in PAT margin for FY20. The reason behind this was mainly increase in expenses of the company. In FY 20 Depreciation, Finance cost and employee cost of the company has been increased.

In FY 20 the company reported amortization expenses on right to use assets. As per IndAS the nature of expenses in respect of operating leases changed from “Rent”/ “Other expenses” in previous period to “Depreciation and amortization expense” for the Right of use assets and “Finance cost” for interest accrued on lease liability.

As a result the “Rent” / “Other expenses”, “Depreciation and amortization expense” and “Finance cost” of the current period is not comparable to the earlier periods.

This also resulted in change in cash flow from operating activities and financing activities for relevant expenses.

In FY21

Due to Lockdown the restaurants temporary closed which affected the sales of the company for FY21.

Further the restriction in delivery hours also acted as an headwinds for the company and affected the profit margins. As a result the company reported negative growth in revenue and profits.

However during the end of FY21, the company managed to recover its sales level mainly driven by home delivery.

Thanks!