About the Company

JTL is engaged in the manufacturing and export of black and galvanised electric resistance welded (ERW) steel pipes and tubes through its four manufacturing units located at Derabassi (Punjab), Mangaon (Maharashtra), Mandi (Punjab), and Raipur (Chhattisgarh) with aggregate installed capacity of 600,000 MTPA as on March 31, 2023 (PY: 400,000 MTPA).

JTL has plants located at strategic locations that allow company to source raw materials at competitive prices and expand their sales and footprint in domestic and international markets.

- Derabassi (Punjab) – 1L MTPA

- Mangaon (Maharashtra) – 2L MTPA : Presence near port boosting ecports – will go up to 4L MTPA

- Mandi (Punjab) – 2L MTPA (1.86L MTPA commercialised) – 14k MTPA to commence by end of FY24

- Raipur (Chattisgarh) – 1L MTPA : 50% is dedicated to value added products – strategic location of the plant has offered an advantage of backward integration to ensure cost synergies and greater proximity to raw materials facilitating JTL to procure RM at competitive prices – will go up to 4L MTPA

Geographical Mix: 95% of the Sales is domestic; 5% is exports

Industries Catered: Agriculture, Water Distribution, Solar Projects, Energy & Engineering, Heavy Vehicles, Construction & Building Material, Core Infra

Clientele:

Industry is expected to grow at high single digits till CY30E

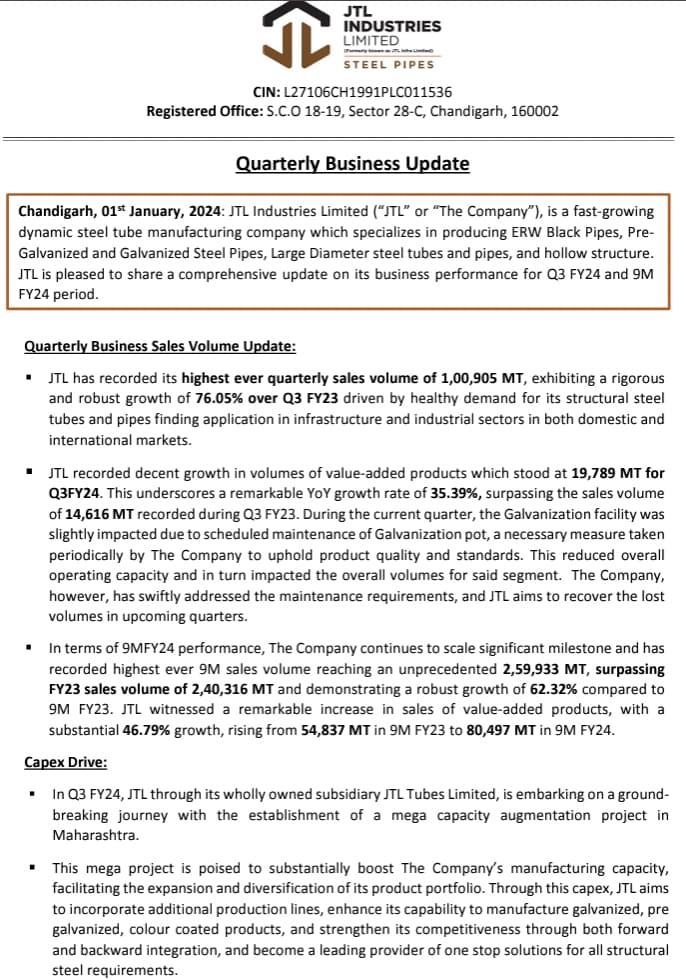

JTL is a fast-growing dynamic steel tube manufacturing company which specializes in producing ERW Black Pipes, PreGalvanized and Galvanized Steel Pipes, Large Diameter steel tubes & pipes, and hollow structure is planning to set up a mega project in Maharashtra

Growth Opportunities in various themes:

- Warehousing

- Infrastructure

- Green Growth & Water Sanitisation

- Affordable Housing

- Oil Industry

- Railways

Growth Triggers:

- Significant capacity expansion plans with a total outlay of close to ₹500-550 crore increasing the capacity from 600,000 metric tonnes per annum (MTPA) as on March 31, 2023 to 1,000,000 MTPA over a period of next three years through FY26 and addition of value-added products

- Raised Rs. 384 crores through the allotment of fully convertible warrants to fund the expansion

- During FY23, the merger of Chetan Industries Limited into JTL was completed vide NCLT order dated March 30, 2023, and has been effective from April 01, 2021. JTL is amongst the fastest growing steel tube manufacturers.

- Aims to double market share with the upcoming capacity expansion

- Target of reaching a total manufacturing capacity of 2 million tonnes in the future

- Aims to increase share of international sales to 15% from the current 9%

- Anticipates a 30% increase in volume growth for the full year FY24 compared to the previous year

- Expects third and fourth quarters to be better, with no demand slowdown foreseen

- Expects EBITDA per tonne to increase with the introduction of DFT technology and an increase in the share of value-added products.

- Within the next two years, JTL has set a goal to raise its proportion of value-added products to over 50%, as a part of its strategic plan to enhance the business and margins generated out of its product offerings

- Mega Expansion Plan announced: JTL, through its wholly owned subsidiary JTL Tubes Limited, is embarking on a groundbreaking journey with the establishment of a mega capacity augmentation project in Maharashtra.

To finance this ambitious project, JTL is set to raise Rs. 13,100 Mn through various routes, including but not limited to Qualified Institutional Placement (QIP). This infusion of funds will be orchestrated from both promoter and non-promoter groups

Of the overall fundraising, the promoter and promoter group is committed to contributing Rs. 5,400 Mn, while the public, non-promoter group will play a pivotal role with the contribution of Rs. 2,700 Mn. The remaining Rs. 5,000 Mn will be garnered through the QIP route. This strategic initiative serves as a testament to the Company’s resolute dedication to expansion and diversification, reflecting its proactive approach in shaping the future of the Company marked by dynamic growth and success

Fundamentals:

- Installed Capacity: 5,86,000 MTPA

- 100+ Acres land bank area

- 4 Manufacturing Facilities

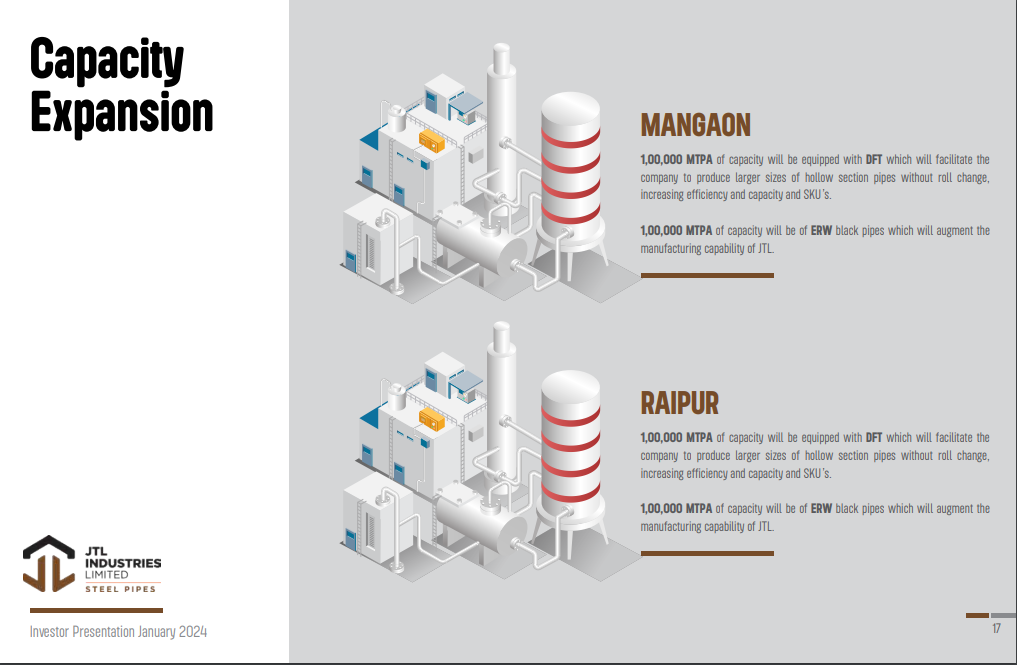

- Expanding current facility with DFT Tech, aiming for 10L MTPA

- Pan-India presence + Global Presence (5 Continents, 20+ Countries)

- 600+ employees

- 800+ distributors and retailers

- 1000+ SKUs

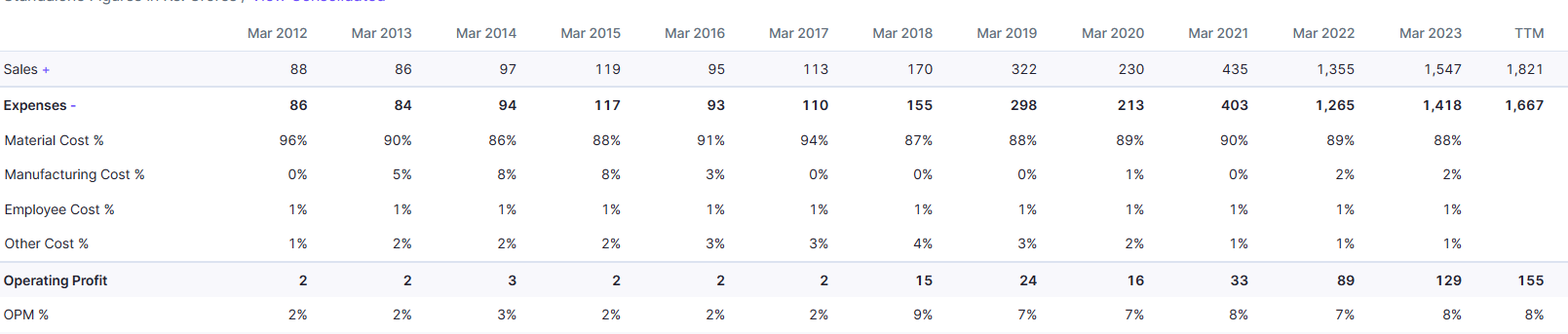

- 5 Yr Revenue Growth: 56%

- 5 Yr PAT Growth: 62%

- H1FY24: Revenues up by 37% YoY, EBITDA up 53.5% YoY and PAT up 61.6% YoY

- ROE: 30%+, ROCE: 35%

- Stable operating margins at 7-8%

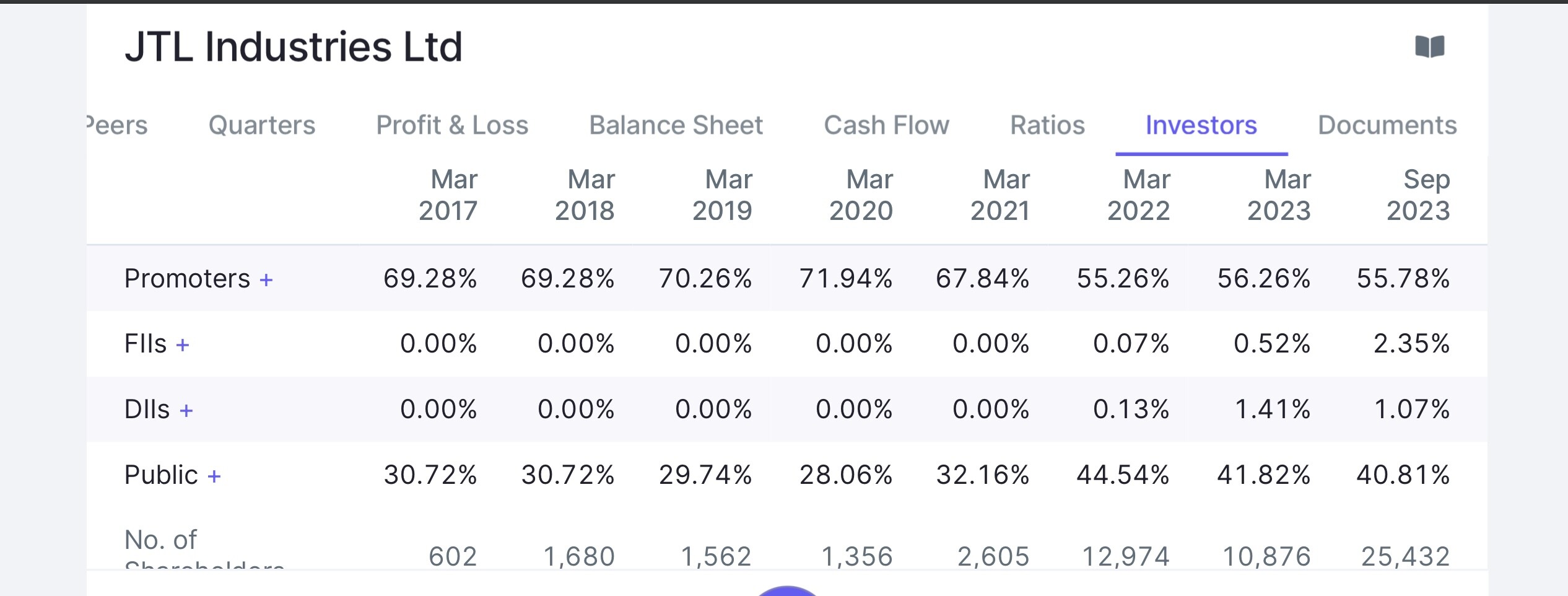

- Institutions increasing stake

- Debt going down: Negligible long term debt – D/E at 0.12

- Improving WC Cycle from 71 days in FY23 to 57 days in H1FY24

- PEG at 0.6

Quick Comparison with the giant APL Apollo

| JTL Industries Ltd | APL Apollo Tubes Ltd | |

|---|---|---|

| Market Cap | 4,234 | 44,403 |

| Current Price | 249 | 1,600 |

| Stock P/E | 38.3 | 57.9 |

| ROCE | 34.60% | 26.90% |

| ROE | 30.10% | 23.50% |

| Price to book value | 8.86 | 13.5 |

| Debt to equity | 0.12 | 0.36 |

| Profit growth 5Years | 62.50% | 32.40% |

| Sales growth 5Years | 55.60% | 24.80% |

| PEG Ratio | 0.61 | 1.79 |

| Price to Sales | 2.32 | 2.48 |

| Return on invested capital | 22.40% | 20.20% |

| Interest Coverage Ratio | 27.8 | 11.6 |

| EVEBITDA | 26.5 | 34.6 |

| OPM | 8% | 6% |

Disc: Invested and biased