Hi @pranshukh ,

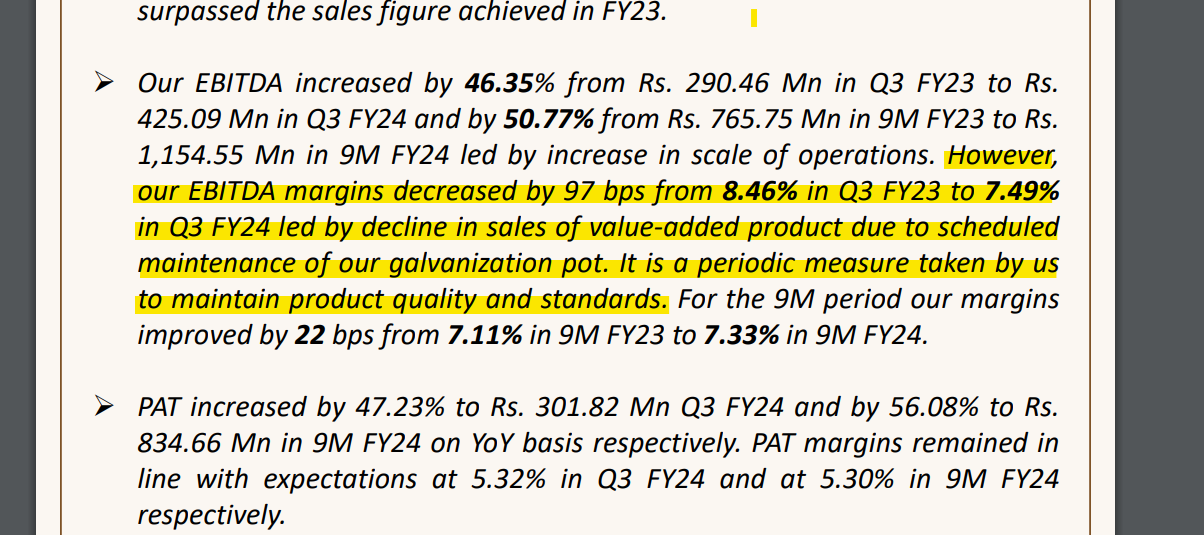

Management has mentioned this in Q3FY24 earning release. The sales of VAP were declined due to scheduled maintenance activity.

Disc: Invested

Hi @pranshukh ,

Management has mentioned this in Q3FY24 earning release. The sales of VAP were declined due to scheduled maintenance activity.

They are doing 1300 crores capex in next 3 years so what about depreciation?

These questions are important.

I dont think 100% capacity utilisation is possible in this sector, maximum 70-80%, and may be new capacity is coming for value added product, there is double digit growth opportunity in the industry so may be they want to have additional capacity to capture market share.

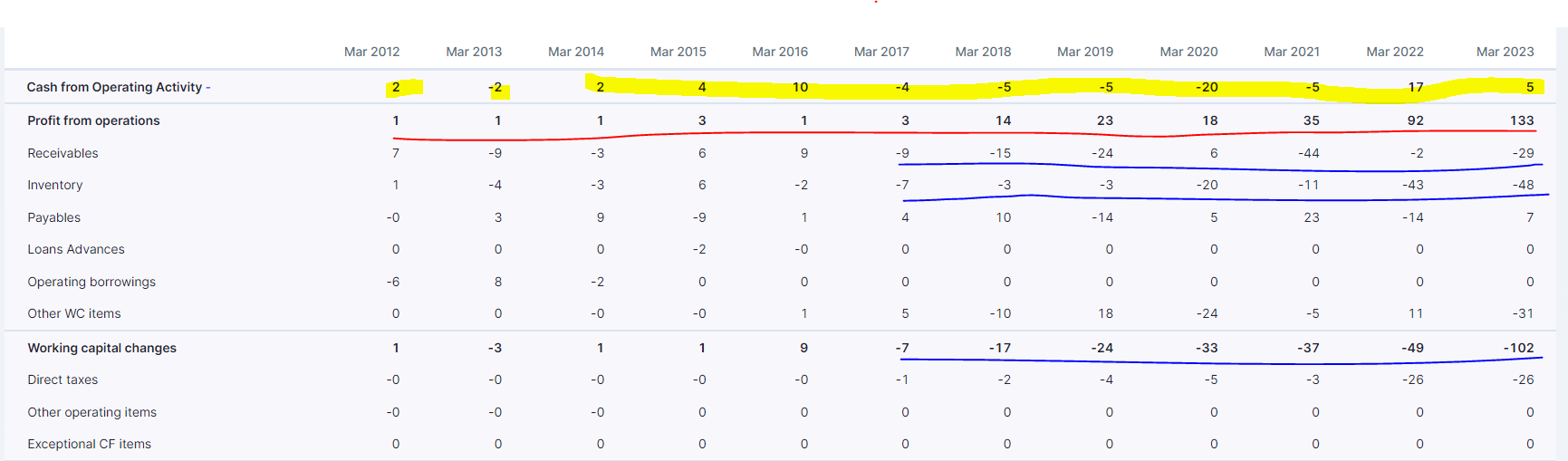

Why operational cashflow is (CFO) nothing compared to the profits

CFO is very negligible compared to profits. WC is very high (us it a red flag or normal?).please some one clarify

Because of company is in big expansion mode. Receivables and inventory are increasing. And receivables and inventory are normal in compare to sales. Working capital days not increased and same in line with past.

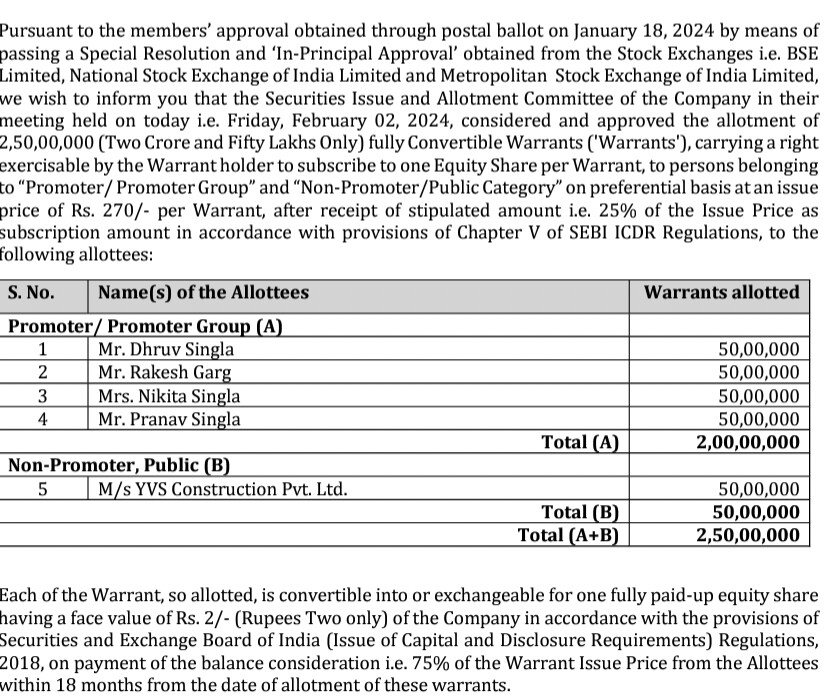

So this is done. A good move and the price of 270 should logically act as a base support though the markets are wiser and tames even the smart ones.

company can operate at 65% capacity utilization because they have to customize products which requires change in lines.

I listened to the concall. Obviously promoters are super positive. They mentioned that their only concern is thr delay in getting machinery that may delay the capacity expansion qoq. Answer sounded a bit cocky to me but let me hear the community thoughts?

One other thing they told - Market demand is about 13-14m tons and is growing at 14% or so yearly. Now, JTL has 9% market share and they expect to take it to 25% market share by FY28".

Does anyone have an understanding on why JTL can take market share from Apollo or other players? What can they do unique than others? I assumed its mainly a standard product and basically, economy growth is the tailwind for this business but in that case, i am not sure why they simply think they can take a huge market share from existing companies… appreciate any opinion from the forum?

I don’t have any position now but looking to add.

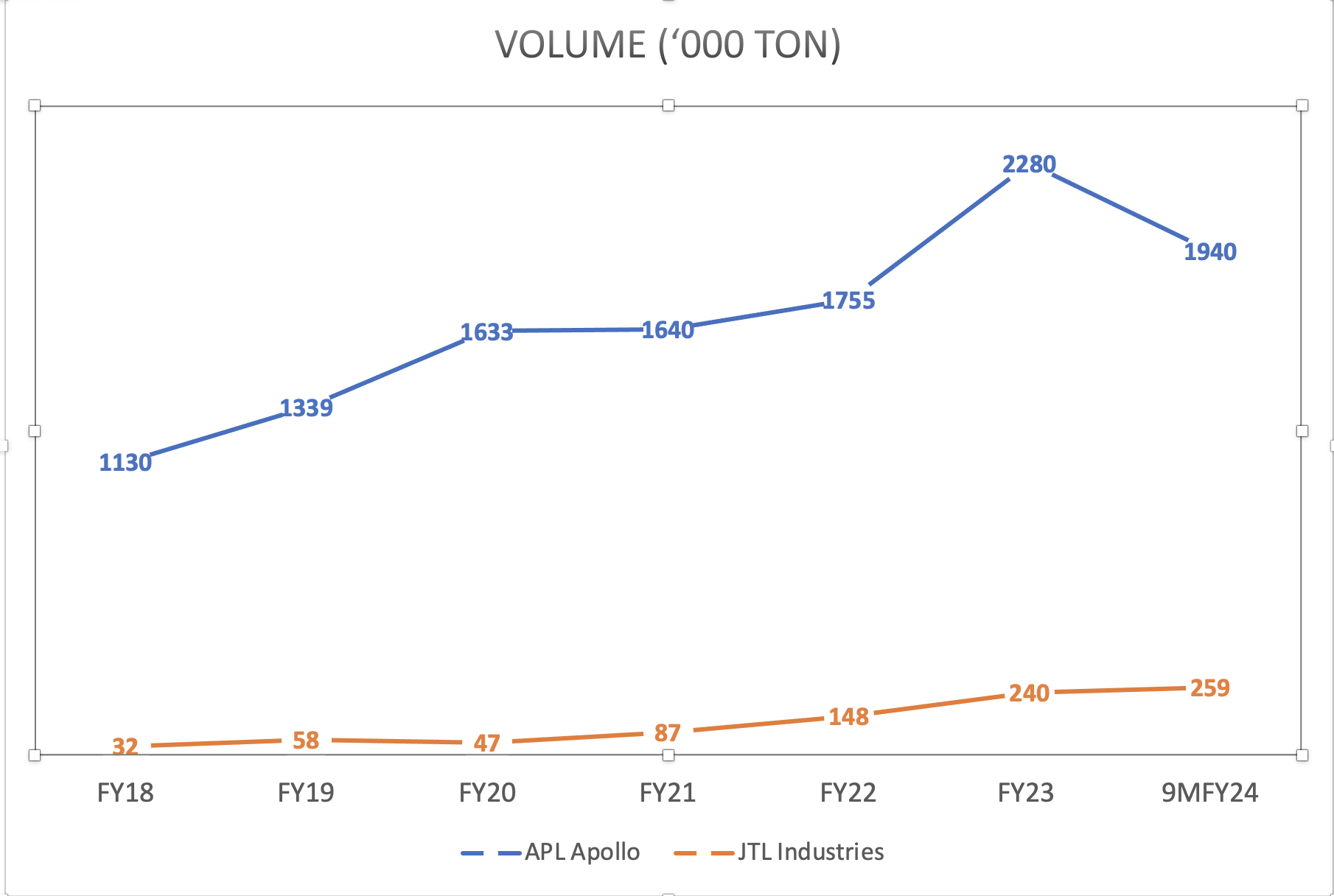

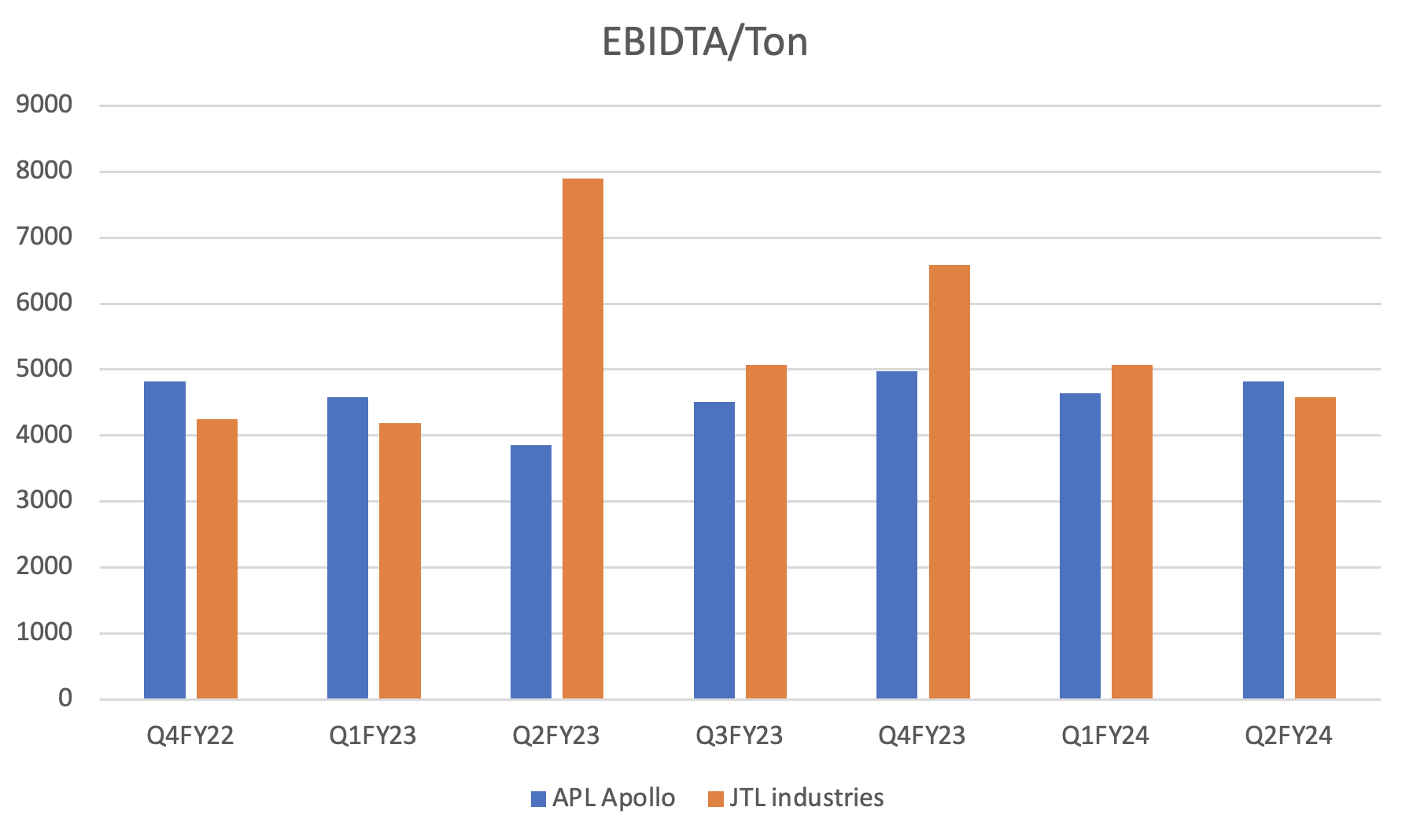

I have done some comparison with APL Apollo for volume growth and EBIDTA/ton.

Pace of growth has been phenomenal while maintaining EBIDTA levels.

JTL is extremely small right now but when they talk about growing 3x the industry and having 25% market share in 3-4 years, I am trying to understand why they feel so confident in taking market share away from current providers.

For example, if they believe that they can replace demand served by imports or demand served by unorganized players, etc.

Even I had a similar feeling while reading the con call about how they were talking about doubling capacity and so on. Given that other players are also increasing capacity, shouldn’t overcapacity translate to lower margins for all or is the demand so monumental that the excess capacities will be absorbed?

Disc: studying

JTL is in secondary steel however Apl in primary steel. Whenever there is big gap between primary and secondary steel, market shifted towards secondary steel.

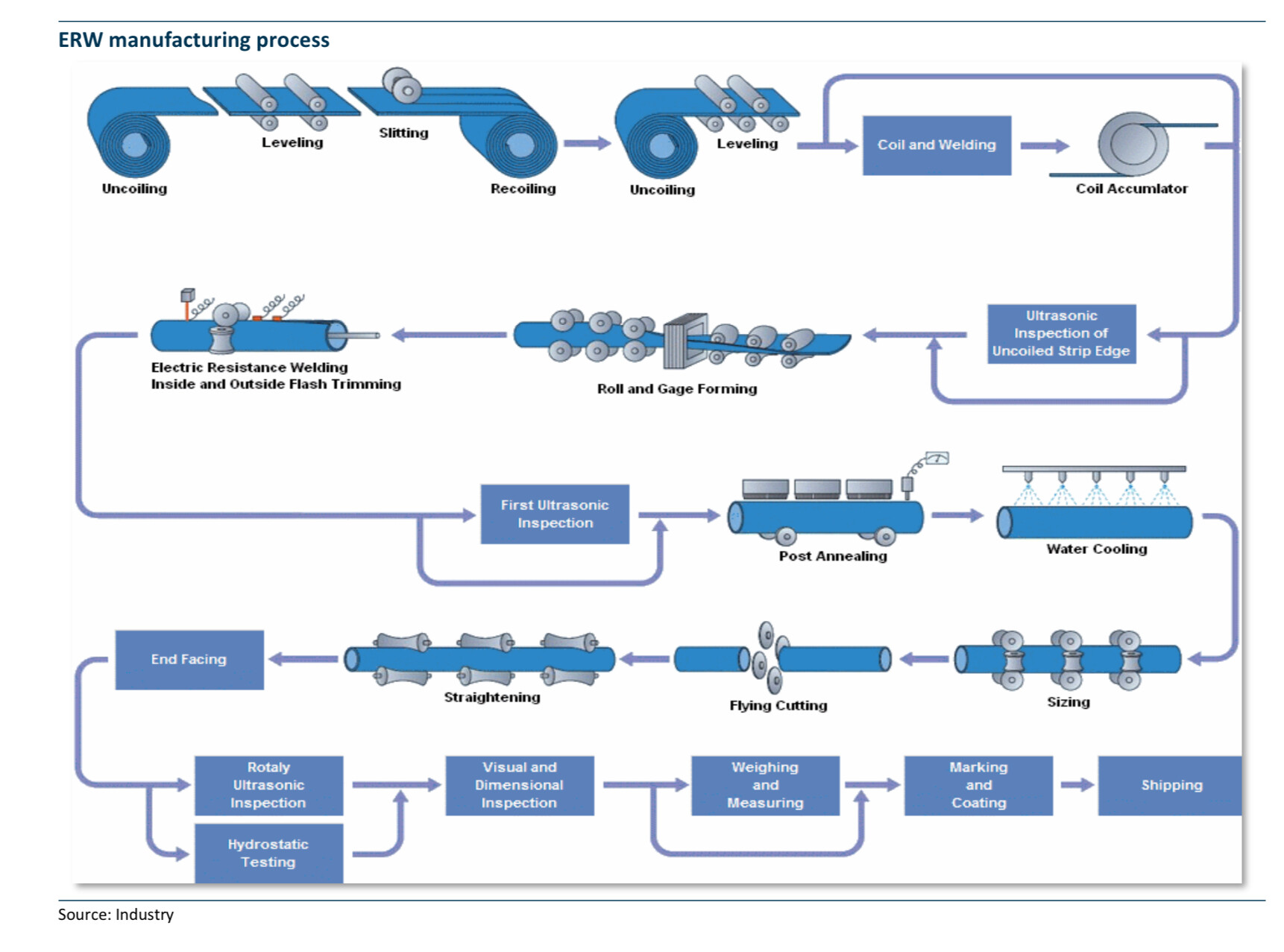

Understanding the ERW manufacturing process in detail

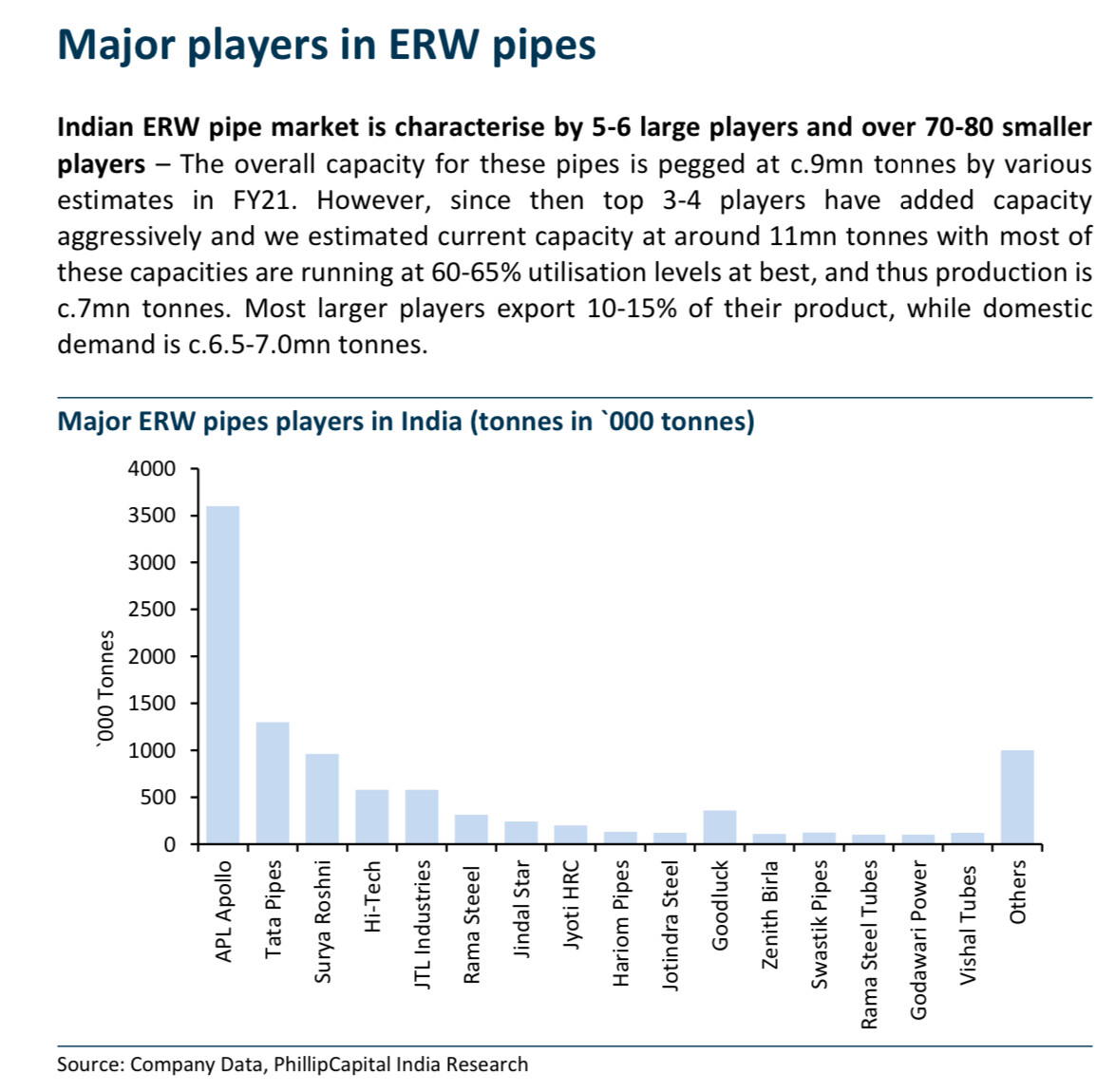

Good data points on the ERW Industry. The pie is big for the top5-6 players to grow and capture market share from unorganized and smaller players

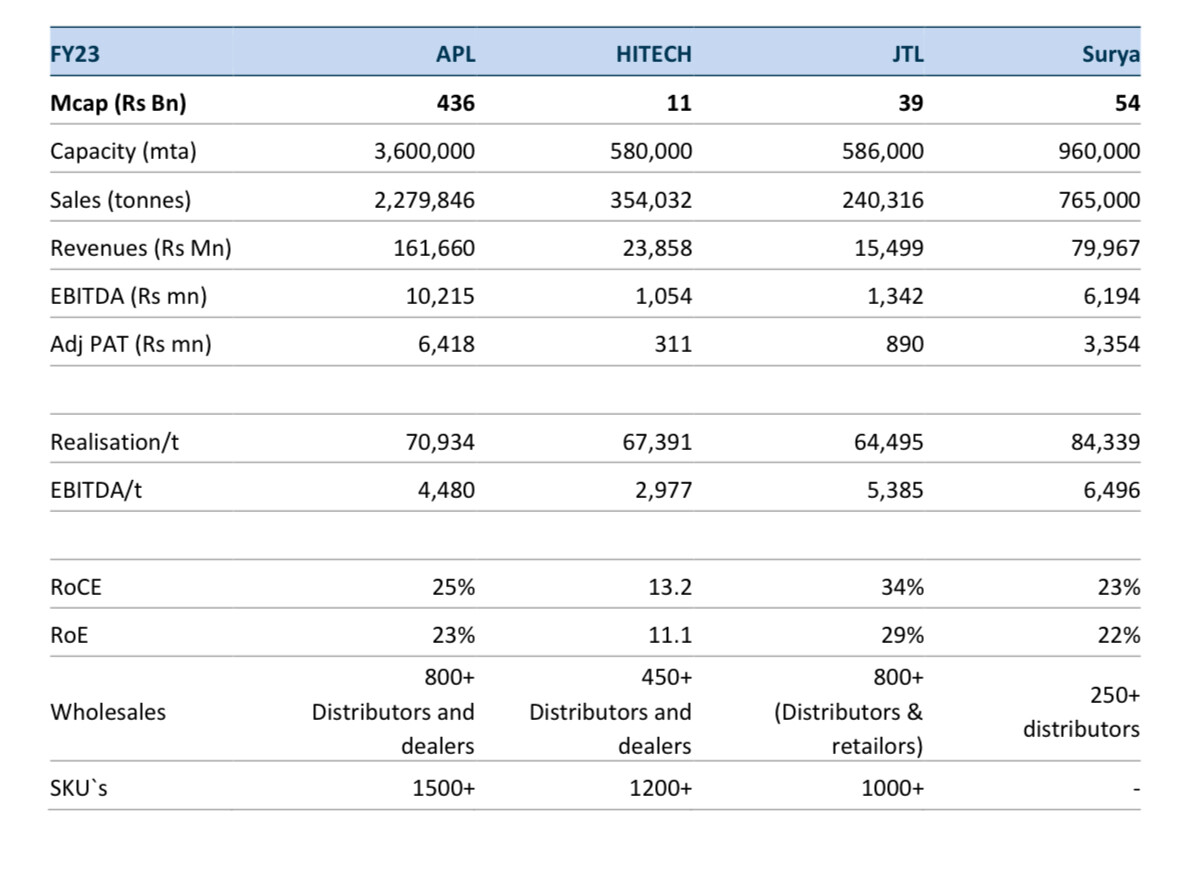

Comparison of key players

Isn’t ERW black pipe a commodity product where they plans to expansion. And that will lead to inventory gain and inventory loss cycle. plz correct me if i am wrong.

Yes, you are correct. Given the strong tailwind of (1) broader end usage and (2) market consolidation - the bigger established players with access to better technology can capture incremental market share on higher margin products.

This is the same playbook we have seen playing out for CPVC players, where despite being a commodity all players (Astral, Supreme, Aashirwad) have faired well.

One should brace for volatility, as we have seen in the past for both APLapollo and JTL.

Stock is down by 19%, what is the issue?