I have recently completed 10 years with Valuepickr. It has been a hugely rewarding association for me, as I am sure it must have for scores of fellow investors.

The idea behind writing this note is to share my experiences over the last 20 years of active investing in a hope that it helps young investors of today to realize the potential of attaining financial independence within a reasonable span of time.

I started my investing journey at the ripe old age of 36 around the turn of the century so most of you already have a head start! The start itself was accidental, in that I happened to read Peter Lynch’s “One Up on Wall Street” & it rang a bell! Lynch wrote at length about buybacks, mgt. buying, about share prices following a Co.’s earnings & many such gems that made a lot of sense. I guess being an entrepreneur for 15 years prior to reading Lynch, I viewed investing from a promoter’s perspective & not necessarily as an investor buying 100-500 shares in a Co.

Reading is one sure way of getting better at the craft. There is no dearth of investment classics, & I benefitted enormously from reading & re-reading them. You need to make your own private library of books from which you derive solace & comfort. It will surprise you that each time you re-read a classic, you are quite likely to learn something new that had perhaps skipped your attention earlier. Or it may be that as you evolve as an investor, you are able to relate better with the author.

Random thoughts on investing:

The starting point for any investor is to know yourself, your temperament, your nature & then being true to yourself, not trying to be someone else that you are not. To be able to think for yourself & have the self-belief to back your judgement. Don’t worry about being wrong, the investing game allows it, but make sure you don’t repeat the same mistake twice. I probably made more mistakes than anyone that I know, but it’s important that the moment you realise your mistake, you cut your losses asap, preferably the same day if possible. The inability to take losses, is perhaps the biggest stumbling block to wealth creation. Yes, your pride does take a hit each time but if you cannot take a loss, then perhaps you are better off not wasting your time on this journey.

It helps a great deal if you are an Optimist & believe in India’s growth story. Being cynical about life in general or having a negative disposition makes the journey very tiring. It is difficult to change one’s nature/ temperament, but one can always make the effort. Don’t worry about things that are not in your control, like markets being manipulated or playing on an uneven field. Focus instead on what adds value to your portfolio by being aware of all the developments relating to your investments.

Stay with what you understand. You will make fewer mistakes. It doesn’t matter if your circle of competence is limited. Humility is the key, & any kind of arrogance is a recipe for disaster. The markets won’t take long in humbling you as most of us have learnt the hard way! The key is to remain a lifelong student.

You have to enjoy the process of research. This is critical and I am not sure if it can be acquired. Perhaps learn to enjoy your own company as the journey is somewhat lonely. Investing, as I see it, is all about taking a gut call on the basis of available data, as you interpret it, without looking for re-assurances from others.

It also helps if you do not take yourself too seriously, & even have the ability to laugh at yourself with all the mistakes that you will make along the way! After a few years you know whether or not you are cut out for this game. If you decide that you are unlikely to enjoy the journey, then focus on whatever you enjoy doing but start an SIP on the Sensex or Nifty and you will still beat 70% of investors like us who eat, sleep and breathe the markets but are still unable to beat it!

Each investor has his own style as each one is different. I always took a few concentrated bets at a time & backed myself. Heavy bets are not taken in one go & you add as your conviction grows, as the story unfolds to your liking, no matter that the addition is made at higher levels. You have to make your winners count. They have to take care of all your mistakes/ losses. I did not believe in making shares “free of cost” & holding them forever. If there is merit in the story then why sell & if growth has plateaued or valuations are not in your comfort zone, then exit in total & look for the next story. The investment corpus is limited & the idea is to maximise returns. Hedging your bets by remaining invested in non-core ideas will lower your returns.

The rewards, however are hugely gratifying. A decade of focused investing can take you close to financial freedom. The real game only starts thereafter as you let the power of compounding work for you, and you start playing the game for the sheer joy of playing it! And then, if you are honest with yourself, you will realise that you are sitting on far more than perhaps what you deserve, certainly much more than what you would have bargained for!

Thank you @RajeevJ for writing this note. It helps each of us to learn from your journey. I am more young at investing journey with only 8 years experience starting at more ripe age of 40.

Would you be able to share atleast one of stories of your biggest successes and biggest failure ? How did you build conviction in the success story especially as you are small cap investor?

I am diversified small.bet guy, but trying again to increase my allocations. Would you say typically how many stocks you remain invested and how big was your current big bet in terms of total PF%. How long you remain in cash, before redeploying it in another idea. For eg,you recently exited Pix. Did you already redeployed the gains to another stock ?

Apologies for this answer, but he is a big investor. Investor in a business in a more direct sense. Remember seeing him owning 1% or so of shares, traveling long distances to meet managements etc. So the scale at which he does is not the same as ours, assuming you don’t have positions like he does, and assuming we are the same. Just saying.

Interested in the details of his endeavors though, because I cannot recollect another member like him quickly, so there will be a lot of learning.

@RajeevJ Your post might look like a few paragraphs of common knowledge to newbies, but for anyone who has been active in the market for some time, these are great words of wisdom, which come only from experience, and all of which, while may not be practically doable by all currently, but if understood will help as the journey progresses and positions scale up. Thank you very much for this.

I kindly request you to share your story, including examples, about how you started your investment journey in stock picking.

I am curious to know your thoughts, views, and doubts during the initial stages when you were accumulating stocks and how the growth story of those stocks unfolded over time.

Additionally, if you have any failure stories from your experience with certain stocks, I believe that would also be valuable to learn from.

Thank you for sharing your journey. It’s been an inspiring read as someone in their 30s aspiring to achieve Financial independence and just starting off on that path. Over the last few months I have started taking this forum more seriously as well, and there’s such a vast ocean of knowledge on this forum! My awareness into finance came through first reading Robert Kiyosaki’s Rich Dad, Poor Dad. He also mentions books by Peter Lynch to get more useful information into the Stock market and criteria for picking good companies. Though my financial knowledge is still pretty basic, im sure it can only grow. and experienced members like you sharing their knowledge reinstalls my faith.

I had tried reading Intelligent Investor, but at the time i couldn’t get into it. would you recommend any subsequent reads as a progression to One up on Wall Street?

Thank you

The more I read your note the more convinced I am about the joy of being in markets even if it’s in a small way that I am in. The money does matter of course but the happiness of being right about a bet can’t be traded for just money

Thanks for sharing your experiences, Rajeev! A well-written piece. Learning a few new things, and a reaffirmation of many things that one knows, from successful investors like you is always so valuable. All the best for the next leg of your journey…

Great points of your journey.

I request if you can give few examples of you investment where you got right and wrong with reasons (mistakes)…this will be useful to our group

Responding to some of the points raised above & a few other thoughts:

As regards to my hits & misses, I have been writing in some detail, of most of my investments carried out over the last ten years on ValuePickr, which is such a wonderful site that I think you can access it all. It will pretty much cover stocks, both, which worked out well & otherwise. I think I may have given my reasons for both getting in & out in most cases.

In terms of the number of shares in the portfolio, your top 10-12 stock ideas should be enough to absorb 90% of your corpus. That too not equally. The weightage for different stocks should be in direct proportion to your conviction levels in each Co. 10-12 stocks is enough diversification and it also forces you to take meaningful positions in stocks where you feel bullish. Frankly, there is no point in being right with your investment thesis if you don’t make it count.

A few thoughts on selling: For starters, losses don’t happen when you sell or book them. They have already happened when the share price fell. With that clarity in place, it becomes a lot easier to sell & cut losses.

I always found selling to be trickier than buying. Stocks tend to have a bad habit of going up after you sell! I try not to track stocks after I have sold them. It helps me in managing stress. Earlier, I used to put down in writing, my reasons for selling a stock as it brought a lot of clarity. Reasons could be any, like valuations getting stretched, lack of growth, a mistake in buying the stock in the first place or simply finding a compelling story so having to sell an existing stock.

Try not to fall prey to the easier option, that of adding to the number of stocks in your portfolio as they do not necessarily help with your returns. I also found it easier to sell while the stock was going up than when it started to correct, more so as your scale of operations increase. When stocks are rising, as is the case in the current bull market, it’s all the more important not to get complacent & to keep revisiting your investment thesis & keep a close eye on the valuations to see if it makes sense to book profits. If its not a buy any more, it could be a sell!

I like to mention some of the stocks that I like at current valuations. I am holding them & may have possibly have written about them on their respective threads.

WPIL (CMP 3,414/-): The Co. has just received the full amount of over 600 crs for sale of one of their european subsidiary. Able mgt. Huge growth opportunities.

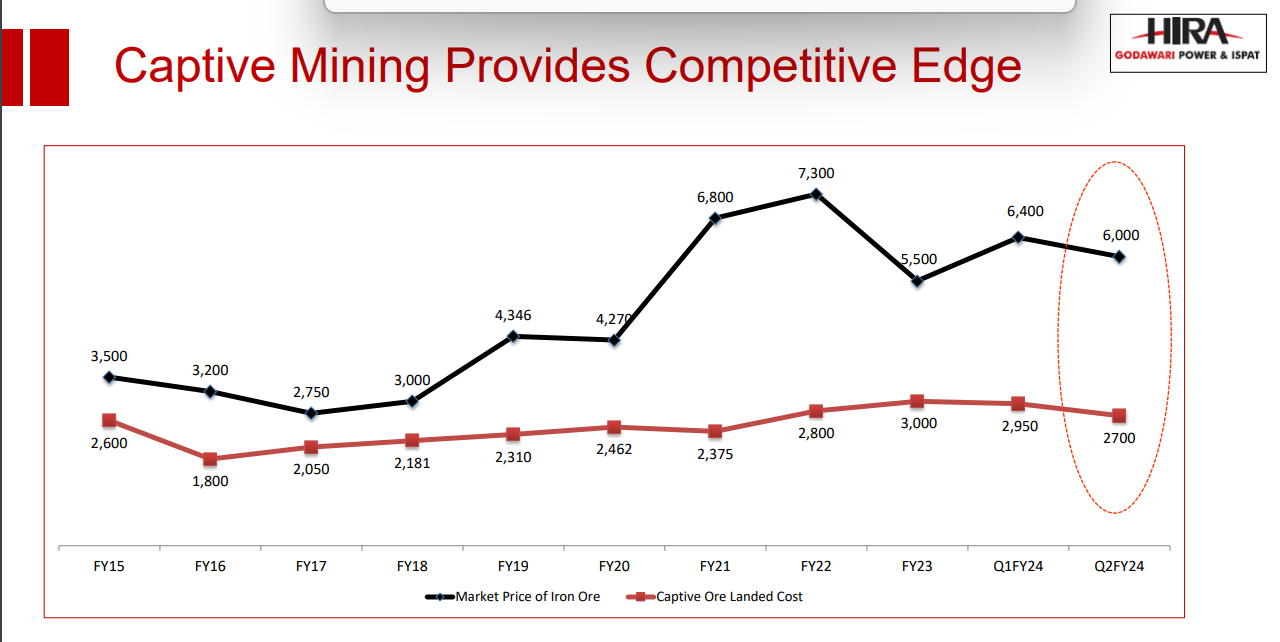

Godawari Power (CMP 687/-): Debt free Co., owns captive Iron ore mines with lease period of another 35-40 years, so barring unprecedented fall in ore prices, GPIL will continue to generate huge cashflows year after year. Steel companies buying ore end up paying three times the cost, which almost means free money for the next many years!

MPS (CMP 1,730/-): Companies ability to acquire profitable Co.'s at reasonable valuations & integrating them with itself has the potential to generate huge wealth. The Co. has been walking the talk & has been rewarding its shareholders handsomely along the way.

Va Tech Wabag (CMP 607/-): Turnkey water supply & Water recycling have huge growth potential. A technology based Co. run by technocrats has of late come on the radar of the MF’s who are increasing their stake. Amounts written off earlier are also gradually coming back.

Vedanta (CMP 256/-): Demerger into 5-6 focused companies has great potential of creating wealth over the next 12-18 months. Meanwhile, enjoy the steady stream of dividends!

Lincoln Pharma (CMP 612/-): A Co. with decent operating margins & valuations. Mgt increasing stake over the last few years. Potential to get re-rated as the Co. gathers scale.

Also invested meaningfully in Redtape (CMP 445/-), but its more a hold currently than a buy with a somewhat muted Sept qtr. Needs to be given a longer rope!!

Great List. Just a query on Vedanta. We do not have an accurate picture on debt repayment. Once Cash Rich HZL is now sitting on debts due to consecutive large dividends.

I am conflicted here as once the metal cycle turns it would throw profits but concerned on this above aspect. What is your thought process and how have you overcome this concern?

Thank you for sharing your experience. As a newcomer to the market, I am finding it difficult how to go about researching a company and how much time does it takes (on average ) to do research before taking a position .

@hardik_shah1

Regarding Vedanta, I feel the valuations are what they are precisely for the reason that there are some doubts in the minds of investors. I feel that the promoter is a wily operator who has been in similar situations multiple times. The Co. has after I wrote the post has paid another round of interest on its NCD’s.

Meanwhile, the shareholders too have received a dividend of Rs. 11/- per share. I feel comfortable holding Vedanta & expect the demerger to go through which should result in decent value creation. At least the downside is pretty limited.

Vedanta Limited: Bondholders approve restructuring of $3.2 billion worth of bonds More than 97% of bondholders of Vedanta Resources VRL approved the restructuring of $3.2 billion worth of bonds due to mature in the next three years.

The company said in a statement that the restructuring will reduce its debt by $1.1 billion and extend the maturity of the bonds by an average of three years.

Vedanta’s shares were trading at Rs 263.80 on the National Stock Exchange on January 3, 2024.”

This is indeed good news for Vedanta shareholders as the Promoters now have enough time to successfully split the company into multiple focused entities which could create enormous value.

MPS Q3 numbers were clearly disappointing, more so as the mgt. had needlessly upped the guidance just a qtr ago. The numbers themselves were not that bad, with operating margins getting better despite the set back in the e-learning business. I guess the mgt too has learned its lessons & will hopefully, going forward, let their numbers do the talking! I guess the the pressure of having concalls after every quarterly numbers also gets to the mgt whose enthusiasm to please shareholders can sometimes get the better of their judgement! The mgt. though has stayed committed to their vision 2027 of 1500 crs, & hope to actually achieve it before time with similar margins.

I am of the view that the mgt. is well meaning & have by & large walked the talk over the last 7-8 qtrs, which is a sufficiently long time. I also believe the the mgt. has the wherewithal & ability to grow inorganically by successfully acquiring companies & then integrating them. That is what will create shareholder value in the long run. It matters less that the vision 2027 is realised 2-3 quarters behind schedule but the journey forward should clearly show a pattern in that direction.

The Co. is generating free cash flows of about 130-150 crs annually. Has given a interim dividend of Rs. 30/-, & could easily give another similar final dividend (I think the mgt has mentioned something to this effect in the previous concall, admittedly to be taken with a pinch of salt!) That would make the stock give about a 4% dividend yield.

I feel any meaningful correction from current levels of about 1490 could present a decent buying opportunity & I will look to add.

@Kuldeepjadeja The following graph from the Co.'s investor presentation will clarify better. Those manufacturers who do not own captive mines end up buying ore at market prices that are substantially higher than the cost of ore extracted from captive mines. This difference in price goes straight to the bottom line of the Co.