This is my first attempt in writing to analyze the stock. Please feel free to provide your inputs.

Johnson Controls- Hitachi

Incepted as a joint-venture between two companies, the US-based Johnson Controls and Japan-based Hitachi Appliances, Johnson Controls-Hitachi Air Conditioning India Limited (JCH-IN) is one of the top three players in the Indian air conditioning market today. Established in 1984, the Company has grown from strength to strength over time and today JCH-IN is one of the most respected and largest business entities in the air conditioning products industry in India.

Headquartered in Ahmedabad, Gujarat, the Company has its state-of-the-art manufacturing facility located at Kadi, Mehsana. The Company’s manufacturing facility not only boasts of manufacturing a wide range of cooling products from residential to commercial cooling solutions but is also one of the largest single roof manufacturing facilities in India.

Complimented by a wide array of cooling products, the Company aims to become the number one HVAC Company in India by 2021 along with the enhancement of its market share in both B2c and B2B.

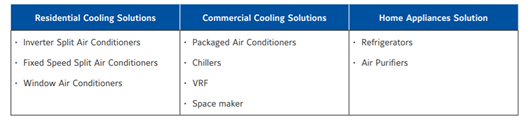

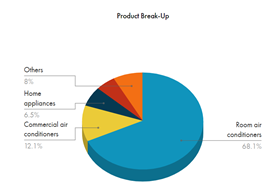

Product Offering

Offerings include home, industrial, and commercial cooling solutions like commercial air conditioning, residential and conditioning systems, absorption and centrifugal chiller systems, and heating & cooling (HVAC) systems among others.

• Room Air Conditioners: The Company is one of the top brands in India with a market share of approx. 12% in the Air Conditioner segment and is further anticipated to increase significantly by 2020-21

• Variable Refrigerant Flow (VRF): The Company’s VRF segment registered a growth of 14% in the previous financial year while, during this period, the growth rate was 25%

• Application-Based Air Conditioners – Telecom Air Conditioners: The company continues to dominate this segment being the single largest air conditioning solution provider for the cooling requirements in Telecom Towers. However, stiff competition and stressed margins in the telecom industry has led to lower or marginal investments in Capex based infrastructure

• Exports: Since the last few years, the Company has expanded its geographical boundaries in the export business. In the last couple of years, the Company has started exporting to Sri Lanka, Indonesia, Bangladesh, UAE, and Nepal, and this year added Bhutan, Myanmar, Maldives, Oman, Bahrein, Qatar, Saudi Arabia, Iraq and few countries like Kenya and Djibouti in Africa Continent. With aggressive focus and improved product lineup for exports, the Company has registered significant growth over last year

• Home Appliances: In the Home appliance segment, the Company deals in the premium range of refrigerator and air purifiers. The domestic refrigerator industry is witnessing a major transformation right from product and design innovations to giving value for money and energy-efficient solutions to consumers with a variety of choices. Gradually the consumer preference is moving towards high capacity models. These high capacity models offer the latest technologies like inverter technology with dual fan cooling, vacuum insulation panels, intelligent controls, etc. The Indian residential air purifiers market is anticipated to grow at a CAGR of over 29% from the current level of 14.14 million dollars to 38.99 million dollars in 2023, on the back of rapid urbanization, increasing purchasing power, expanding urban population and deteriorating air quality

• Service: The Company aims to offer the best in class products to customers and gives utmost priority to good customer care and service. For this purpose, the Company has also undertaken multiple service-oriented initiatives such as free service camp providing discounted service in pre-summer, customer delight program as well as free product check-up in offseason. Company retain its client base and provides service to over 1,500,000 customers

Research & Development Center

Global Development Center:

• The new Global Development Center (GDC), which is currently under construction, will increase the Company’s product development capabilities, particularly in commercial package air conditioning and residential air conditioning systems

• Located adjacent to the Company’s factory in Karannagar, Kadi, this development center will consist of office space of 6,600 square meters, and multiple labs spread over 12,000 square meters of floor space. These labs will include state-of-the-art research and testing facilities for measuring performance, reliability and electromagnetic compliance

• The facilities will allow for testing of air conditioners for global requirements in ambient temperatures ranging from -40 degrees C to + 60 degrees C

• New GDC will focus on developing residential and packaged air conditioner products for India, Southeast Asia, the Middle East, and EU markets. In addition, a range of capabilities related to user experience, industrial design, simulation, controls, design quality, project management, and engineering information systems will be established at the new center

Brand Value

• Backed by Strong Brand, Offering Inspiring Home & Life Solutions Increase in number of institutional buyers: While room Air-Conditioners (AC) are mainly sold to individuals, there is a large market for institutional buyers in this segment

Channel Expansion:

• In order to widen its reach to Tier II & Tier III cities, the company has expanded its distribution network in these towns through direct dealers and distributors; and today caters to more than 4,000 outlets. With more than 10,000 selling points across 1,350 cities and towns across India. B2C sales network which is supported by a strong team of more than 100 members. It also also partnered with more than 500 distributors in the PAC segment and more than 200 distributors in the VRF segments, to enhance the B2B presence in more than 140 cities across India.

• Growth of e-commerce retail portals and increasing nos. of organized retail formats in Tier II and III towns are going to create good growth opportunity for Room Air Conditioners category

• Smart city projects, High-Rise Buildings, Shopping Complexes, Malls, Hypermarkets now Penetrating in Tier 2 Cities as well are going to increase demand for air-conditioning business. Company is focusing and leveraging the strength of our channel partners

• Various government projects like Metro Rail, Airports, and High-Speed Trains, etc. are going to open big opportunity for commercial air-conditioning segment

• Increasing standards of Bureau of Energy Efficiency (BEE) for energy efficiency in products and focus on promoting Inverter Air Conditioners is a huge opportunity for companies

Strong technological support from the parent: HHLI has been sourcing advanced technology from its Japanese parent which has enabled it to launch superior products in the Indian market. “Hitachi” enjoys a strong brand pull, which has helped the company to steadily grow its market share in India. We expect the company to successfully leverage both, the technical support and brand strength, to grow in India.

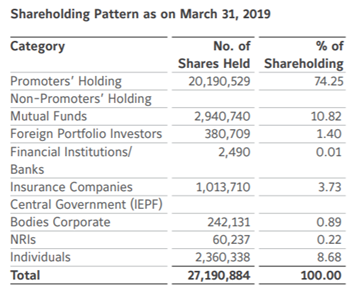

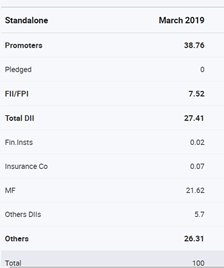

Shareholding

Shareholders have not been meaningfully diluted in the past year.

Covid 19- Risks

• Demand Issue: Customers may postpone their buy due to uncertainty in job and business environment. Customers willing to buy may not be able to purchase due to lockdown or restrictions in movement of goods and services

• Financing Issue: Customers may not buy due to unavailability or increased scrutiny while buying via easy financing and credit options

• Supply Chain: Movement of goods and exports may take a hit as ports and cargo are shut or restricted. Labor or workforce restricted movement may not allow the company to be fully operational

• Closure of Public entertainment places and Industries: Temporary closure of public and entertainment places may impact the sales and services of HVAC systems. Future projects such as the expansion of malls, industries, and smart cities may be impacted in the short term

Covid19- Opportunities

• Export: Japan is giving incentives to Japanese companies for shifting out of China. Considering the GDC is fully operational leading to expanding the export business and targeting South Asian and EU countries

• Strong Residential Demand: Considering the number of employees will start working from home, home appliances will be in demand. The demand may not be there immediately in the short term

• Strong Research and Development Center: Strong backing by the parent company with sharing of technology may help the company to produce superior and sustainable products

• Sustainable Products: George Oliver – Chairman and Chief Executive Officer of Johnson Controls recently said that “More resilient or flexible building space will be required to adapt to changing capacity or utilization needs. Safer environments will be created through seamless combinations of occupant screening, tracing and credential management, and more sophisticated ventilation systems. Touchless or frictionless access, lighting, and temperature controls will be implemented to minimize cross-contamination and enhance the user experience. Remote monitoring and service delivery, including condition-based maintenance, will significantly increase. These types of solutions are being deployed in some of our marquee projects today, and the list of ideas and offerings continues to expand”. This may drive innovation and implementation of new products launched in shopping malls, theatres, etc.

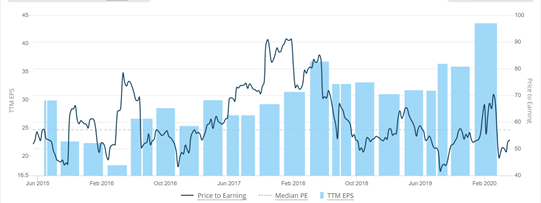

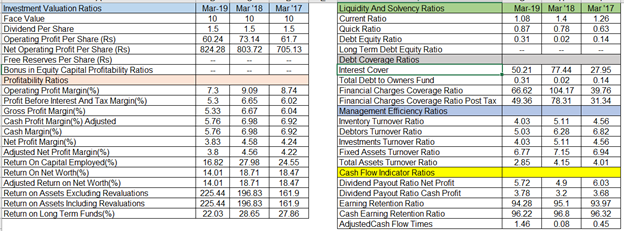

Valuations

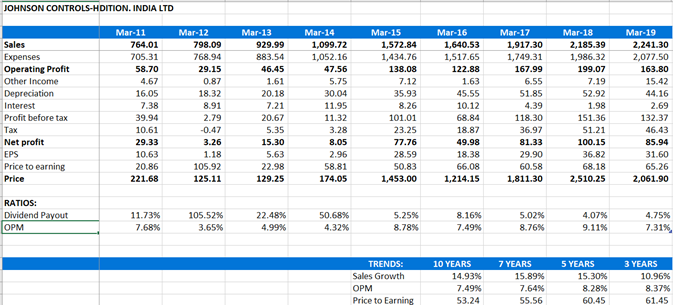

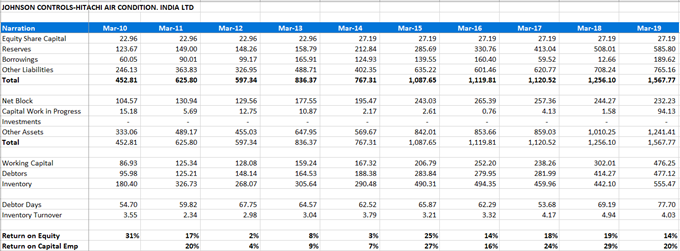

Profit and Loss

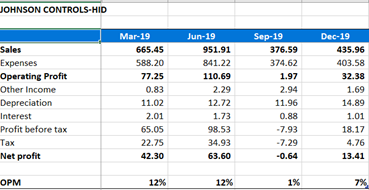

9m results for FY20

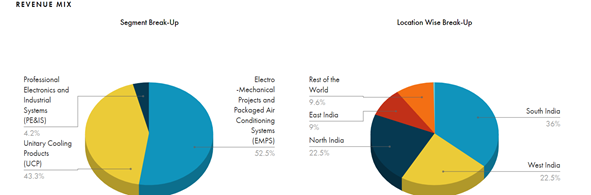

• The total revenue generated from exports of Cooling products for comfort and commercial is approximately 3%. The revenue from exports will be increasing due to operational of new manufacturing units

• The design and development service (Research and Development center) generates approximately 75% of revenue by exporting the technology

• JCHAC’s dividend (0.066%) isn’t notable compared to the bottom 25% of dividend payers in the Indian market (0.87%).

• JCHAC is richly value based on its PE Ratio (51.9x) compared to the Consumer Durables industry average (18.1x). It has historically enjoyed rich valuation due to quality of management, debt-free and strong support from parent company

• JCHAC is overvalued based on its PB Ratio (7.2x) compared to the IN Consumer Durables industry average (1.3x)

Balance Sheet

• JCHAC’s short term assets (₹7.5B) exceed its short term liabilities (₹4.6B).

• JCHAC has no debt, therefore it does not need to be covered by operating cash flow

• JCHAC has no debt, therefore coverage of interest payments is not a concern.

Cash Flow

Strength

- Home appliance products are premium products to target upper SEC customers

- Low price entry products launched to compete with Blue Star and Voltas with an

increase in advertising spend - Superior Technology compared and R&D services

- No dependency on China or any other countries for importing spare parts

- Strong sales and services

Weakness

- Low brand visibility and recall

- No major tie-up with multi-chain retailers

- Royalty Payments made to the parent company

- Tough competition from local players in AC segment i.e. Blue Star, Voltas, Lloyd

Competitive Analysis

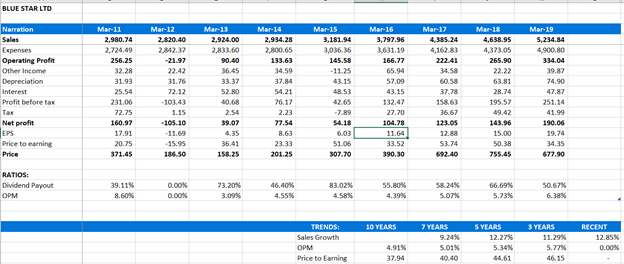

Blue Star: It has a 12% Market share in Air Conditioners and a 25% share in Inverter AC.

As per the management before Covid-19, there was no major demand impact of the company’s AC due to low-priced entry-level products i.e. Unitary Cooling Products and there is likely to be visible price rationalizing with no inventory overhang present. The focus of the management will be in the Tier- 2, 3 & 4 cities with online sales for certain products like water purifiers to also be launched. The company generates 6% of its revenue from online sales.

The revenue generated from HVAC is approximately 52% and from the sale of the domestic air conditioner is approximately 42%. Inverter-based room-ACs comprised ~45% of room ACs and ~47% of Blue Star’s room-AC revenues

International orders inflow and execution from Dubai and Qatar are seeing good traction with order visibility from SAARC and African countries in the Electro-Mech Projects and Packaged AC systems. The management stated that it is seeing good traction from hospitality and rail orders.

Shareholding

Promoter holding is low and float is high which impacts share price volatility in the short run.

Valuations

Profit & Loss

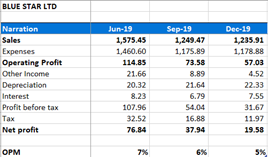

9-month results of FY20

• Blue Star dividend (2.09%) is higher than the bottom 25% of dividend payers in the Indian market (0.87%)

• Blue Star is undervalued based on its PB Ratio (5.3x) compared to the Consumer Durables industry average (18.1x)

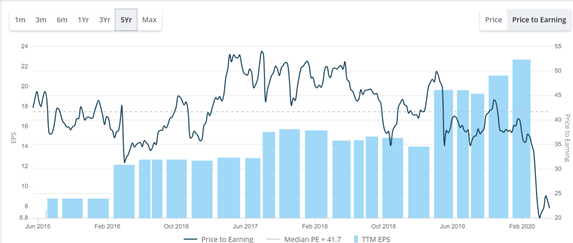

• Blue Star is currently value on its PE Ratio (21.5x) compared to the Consumer Durables industry average (18.1x). Blue Star has 5-year median PE is 41.

![image|629x293]

![image|629x293]

Balance Sheet

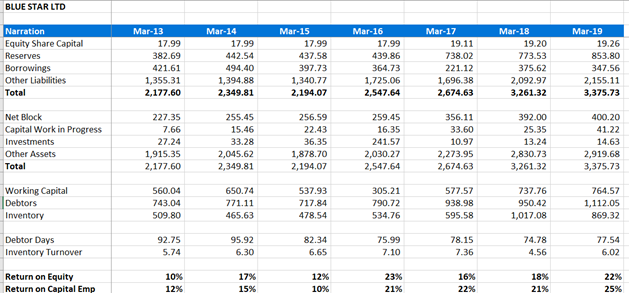

• The past five years have seen Blue Star’s margin expand, due to 32.64% in average net income growth surpassing 9.68% in average revenue growth, which suggests that the company has been able to convert a larger percentage of revenue into net income whilst the growth in their top line

• Debt is well covered by operating cash flow (150.8%)

• Interest payments on its debt are well covered by EBIT

Strength

- Brand visibility and recall

- Presence in multi retailers and individual outlets

- Reasonable pricing

- Strong sales and services

Weakness

- Components such as compressors, there was still a dependence on markets like China

- Revenue dependency on the hospitality industry and Govt of India Infra projects which may be impacted due to Covid-19

- The company continues to face slowdown from real estate and infra space resulting in order inflow de-growth of ~20%

- Liquidity crunch (debt- INR 3.96b) and have plans to raise NCD’s to meet capital expenditure and other expenses. This has aggravated due to Covid-19 issues and weak demand outlook in the first half of FY21

Conclusion

Johnson controls may increase their market share by having more pricing power and reach due to its non-dependence on importing spare parts. The cash-rich company may not be highly impacted as compared to its peers in the short term as demand outlook will be weak. The enhanced manufacturing capacity may help increase its exports to South East Asia, Middle East, Africa, and EU countries.

The company has always traded at high valuation compared to its peers and may do well in the near future considering the enhanced product mix, branding, increased manufacturing capacity, and increasing export business.

Disclosure: Invested - 0.5% of the portfolio

References