The company management has created pledge of 24% of its holdings. Pledge of 6,525,812 Equity Shares done at an average price of Rs. 2316.2 was reported to the exchange on May 31, 2021.

I came across this interesting article which is behind firewall. If anyone a member can let us know some key points…Also, how would a better star system result in economies of scale? or result in more buyers buying efficient products…as cost would always be higher for efficient ones…unless they face lower taxation?

Also, is there any chance that in future AC would be taxed higher as they result in global warming and emissions?

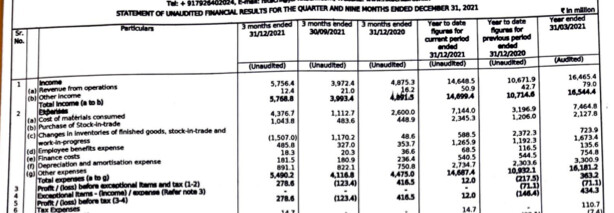

Quarterly results are out.

Revenue has improved over YOY but was unable to show profit(PAT). Seems like input inflation has stuck hard this time and PBT turned negative. However EBIDTA is in +Ve territory.

Johnson Controls Hitachi has been selected for the AC components PLI scheme. Committed investment is around Rs 100 cr. Hopefully they will start significant exports from India. If this happens, it’s revenues and profits will be more steady going forward.

Considering the steep correction in the counter and an upcoming full season for the AC players, was looking into this business with strong interest. But going through the annual report in detail, some surprising points stood out at me which acted like anti thesis pointers. Would be good to have views on below points:-

Page 35 Annual Report : The company does not enter into forward contracts to manage commodity price risk. It does hedge though for Forex. This is a business where material costs form 63-65% of total sales - I find it amazing that what seems like a good quality MNC does not safeguard the consistency of their margins and cash flows.

This is already playing out this year. The previous quarter margins have been massively impacted. In fact the already poor EBITDA for Dec 2021 would be in loss if not for the negative inventory number.

I also checked how the raw material costs have been managed versus Blue Star, Voltas. There is a massive difference, with the Indian companies suffering no where near the margin loss suffered by JCHAC.

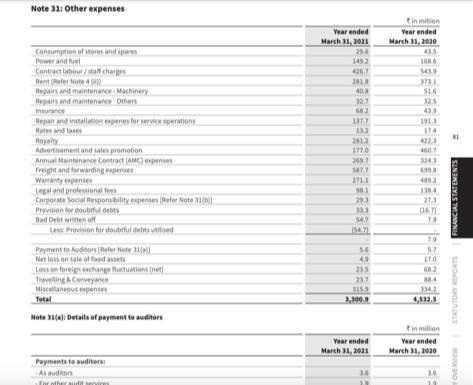

Page 81 Annual Report - For a 7-8% EBITDA business, the parent charges quite a heavy royalty. Royalty numbers for 20-21 have ranged between 1.6-1.9% of sales, which is ~30% of the operating margins in the usual scenario. In the current scenario, where they have not managed commodity risk well, it very well might be the entire EBITDA margin!

@ankush12495 rightly points out above why this business having unfavourable economics and not generating cashflows. I agree, and am very surprised measures described above (especially commodity price hedging) are not implemented by a what seems to be top notch MNC parentage. I wish there were some conference calls where the management view could be gauged on this.

Makes me think towards that pledge mentioned @babu44b in Jun’21. Could it be that this is a company where capital is not as well managed as you would expect in a good MNC. Why would they not borrow from the parent companies? It does seem that Johnson and Hitachi are not being too benevolent towards the India JV, whilst they continue to make good money through royalty.

Disclosure : Not invested, tracking. Not a registered advisor.

Very good write up and points! I think the same may be a reason this company is available at 4.5K Cr mcap and I see this gap as an opportunity to be eventually filled, unless the company is in eternal self destructive mode - which I would not expect.

Could the reason be the issue of a joint venture between Johnson of US and Hitachi of Japan that maybe causing issues of poor capital allocation? Are they allocating capital properly in other geographies where they have this same JV in operation and also is Royalty there appropriate? Thanks

Disc: Invested hence biased. Transactions this week as well. Not a buy/sell recommendation

What is concerning to me is that revenues were also down YoY…not sure why when consumption is in full swing…

Increase in loss can be margin pressure but revenue down significantly was not expected by me…

Also, anyone aware whats the traction in manufacturing for export? I remember the CEO said couple years back that they want to increase exports multifold…not sure whats the status there…any YoY change would be good to track…

They have some pledge share also…I think very few MNC would have pledge share…seems a bit odd to me…The inventory levels are also high it seems…is it same for other consumer durable companies also in last year?

Lastly, this is a joint venture between johnson control and Hitachi but seems that Hitachi is in driver’s seat…whats the vision of these two companies for this JV? Does anyone see eventually Hitachi making a buyout from Johnson controls?

Disc: Invested since couple years with a small allocation and added little in recent crash this month. This has been a loss making investment for me so far. With whatever little we hear of management, the vision on India being manufacturing hub for export and new & relevant product launches for India is there, but numbers have not been good so far…Not a buy/sell recommendation.

This has been a hope stock for long. Highest profit it made was 100 Cr in 2018. Even if things turn around and it achieves that it will be 35 PE, still very expensive.

A simple ground observance will exhibit the fact that JCHAC products are declining in market share. This can be directly correlated with the constant fall in company’s financial performance. I have been invested in this script since last May. It was a haste decision and after tracking the company for around 1.5 years, I have observed that the company has not been able to convert opportunities into sales.

I recently bought multiple ACs for a new home, and was looking into the brands. I eventually chose Daikin looking into various factors.

Daikin is currently offering imported products from Japan at very competitive prices. I would keep Daikin a notch higher than Hitachi in terms of brand image, and considering their offerings and price points, it does seem that Hitachi has a very serious competitor. The space was already competitive, but now the brand is flanked by Whirlpool/Voltas/Blue Star at lower price points, Daikin at similar and O General/Mitsubishi at the higher range.

The upside here could only come in terms of margin expansion in case of serious commodity deflation, seeing them even beat meager growth expectations seems tough in the current market scenario in my opinion.

How about the opportunity and intention to make India their export hub…the make in India pitch that it’s CEO has talked about last couple years…not sure about the traction & growth of this piece but many Asian & African countries have similar weather profile & good export candidates…can this move any needle? thoughts welcome