Look at the forward PE.

Q1 EPS = 4.1

Expected FY26 EPS: 15

Now, if you calculate the PE it comes out to be 40.

And believe me, this is a great growth stock and justifies this valuation as there is no competition.

Only the current management can spoil its run, that too from some fraud / short sightedness. Otherwise Ayurved is too big a sector and the leading players have high probability in easily going to 100k mcap in 10 years time.

I am nowhere saying that this company will be the leader but it is the leader as on date by far far bigger margin and taking right steps be it expansion and the capital allocation.

Sky is the limit if you consider the need of ayurved, the visibility it can get worldwide.

Don’t look at the ROCE, PEG, CAGR etc else one can get biased.

8 Likes

If your entire analysis of an 8,500+ Cr company with 2,100+ beds, 74% YoY revenue growth, and 45% EBITDA margins boils down to digging up one old article about a single sealed clinic….

My 2 cents: that’s not research, you’re mistaking clickbait for due diligence.

12 Likes

Just sharing thoughts of Sajal Kapoor on JeenaSeekho

It’s free for the next 18 hours.

Hope you find it useful.

Juggernaut on the roll?

Can this do an annual EPS of 20…

Waiting for the concall now…

2 Likes

Q2 2026 Concall - Key takeaways for me…

Launch of new products (ten plus )

Likely partnering with Entrero for distribution of products

Likey launch of franchise model with profit sharing structure (50 hospitals)

Likely inclusion of Ayurved treatment with Ayushmaan Bharat Scheme (will initiate a ramp up of leasing College based Hospitals model)

If these triggers play out in short term, the current rising trend in key profitability parameters may get the required tailwinds.

Surprisingly some words of caution thrown in by the promoter…

H1 relatively better than H2…

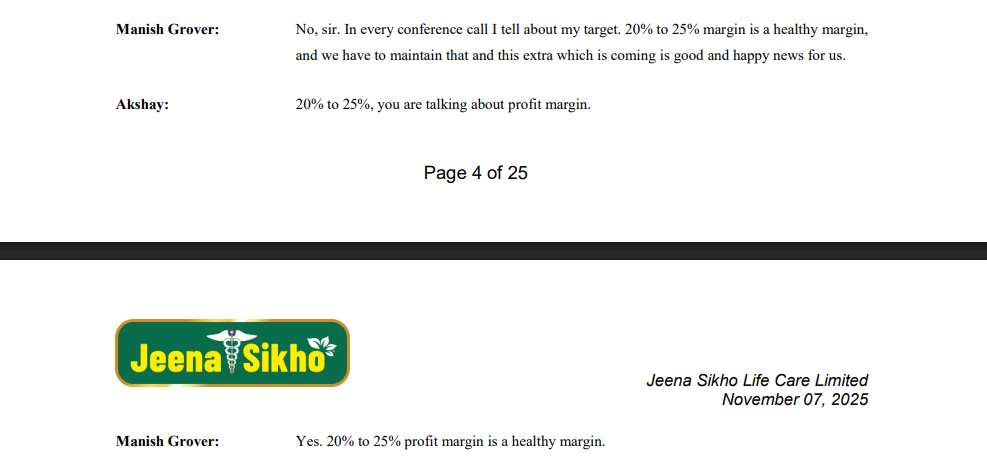

Long term profit margins reiterated in the range of 20-25% as against the current 31%…

No revision the guidance for the CFY either of rooms or profitability

Growth likely to slow down?..lets watch

Disclosure - invested and biased.

4 Likes

Q2FY26 Major Highlights which I think (without going into bed nos):

- Forming probably Stage 3

- Peak Margins

- Growth may come, however fundamentals might become rational

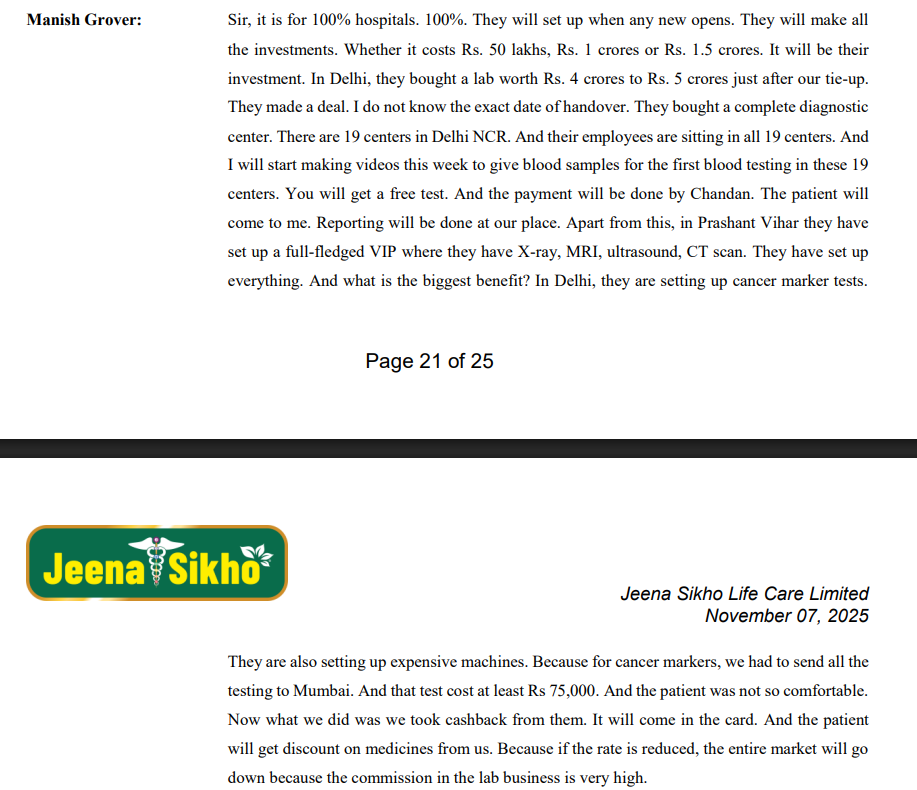

- Strategic deal with Chandan should bring inorganic growth

- Government Business now at 3%

- VIP Premium Centre = wellness retreat. Should drive higher realizations. How would they scale it!

- Technological development (salesforce) should bring down operational cost

- Occupancy rate current is 57% should go up to 70-80% in next 2-3Qs

- Entero exclusive agreement & qcom should bring more product business

Disclosure - invested

3 Likes

Absolutely fantastic results by JSLL! Hard to believe how the thread of such a great performing business hasn’t garnered enough attention of the community till now!

Was not expecting such growth, given the cautionary tone of the management in the last call.

Will be interesting to see what’s driving this growth……. Though the push towards broadening the sales network and increasing products profile seems to be showing signs of success…..too soon? Or is the product quality finding acceptance, really appreciated by the customers and that’s driving the demand?

The company, not the promoter, has taken a big share of warrants in chandan healthcare……. This is intriguing……let’s see if this comes up in the final tomorrow

Disc……biased and invested

1 Like

never had the courage to enter in this stock. myself being from health sector didnt understood their operations. their advertisement on radio (stopped now) were very dubious. really need to understand their operations ethical or not.

4 Likes

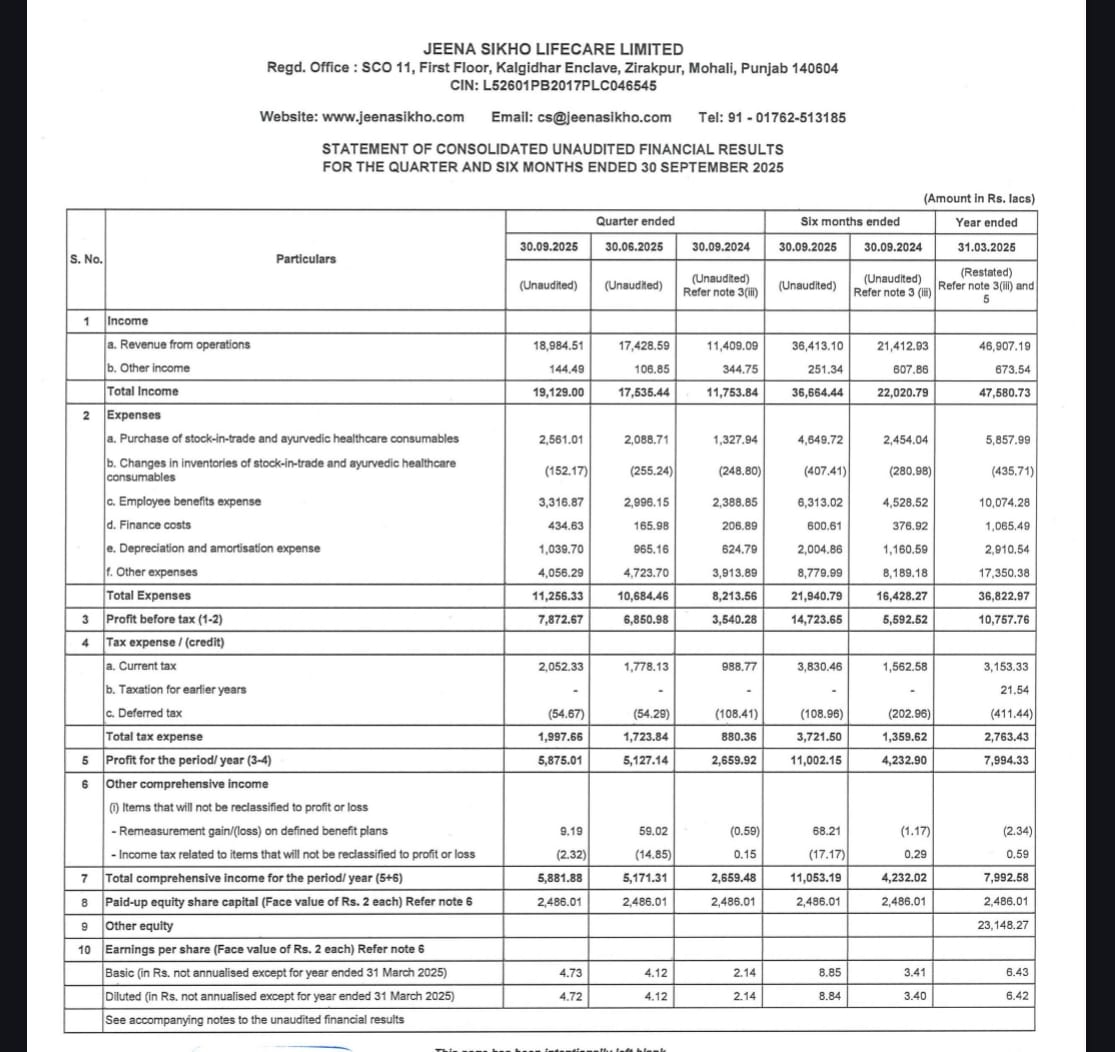

Jeena Sikho Lifecare – Q3FY26 Results & Concall

Financial Highlights

- Revenue up YoY 92%, fueled by 138% growth in medicines and supported by 56% growth in services

- EBITDA up YoY 240%, EBITDA margin 45% vs 26% last year

- PAT up YoY 405%, PAT margin 30% vs 11% last year

- With the high growth in medicines, revenue mix changed significantly.Last year Q3: Services ~55%, Medicines ~45%This quarter: Services ~45% vs Medicines ~55%

Beds / Volumes / Occupancy / Capacity Expansion

- Operational beds now 2,290 vs 2,220 previous quarter (Q2FY26)

- IPD volumes up 84% YoY, OPD up 89% YoY, Day care up 139% YoY

- Video call consultations up 214% YoY

- Occupancy 58% vs 57% previous quarter (Q2FY26), despite Q3 being seasonally weak

- 475 beds in development

- Occupancy target to reach and maintain 70-80%

- Beds target 7000-10000 in next 3-5 years

Medicines / OTC / Product & Margin Strategy

- 1 OTC product launched till now. 2nd product about to be launched this month and more in pipeline (~16 planned in next 1 year)

- Currently medicine products are manufactured by 3rd party. Plans are there to manufacture in house from this year. This will give better control over margins

Network / Partnerships / International Expansion / Future Outlook

- Internationally 2 daycare centres started. 4-6 more in pipeline in countries like Dubai, Nepal, Kazakhstan. International focus is increasing

- Partnership finalised with Entero Healthcare, distribution through Entero to commence by next 15 days

- 34 Lab centres of Chandan opened. To expand to 64 soon. Partnership with Chandan is driving increased footfalls.

- To launch Jeena Sikho health card, which will allow customers to avail discounts on medicines/tests by referring more patients or kind of loyalty program. This will increase repeat customers and make them stickier in nature.

- A chain of super speciality VVIP clinic/day care centres targeting mid health problems like joint pain, obesity, hair, skin etc. in planning (team hiring ongoing)

- FY26 PAT target ₹225 Cr. Long term PAT target ₹1000 Cr expected in 3-4 years

- Forvis Mazars (Top 10 globally) appointed as internal auditors.

Key Risks

- The most prominent risk I see in this business is its dependency on Manish Grover. He is basically one man show in terms of branding of Jeena Sikho, which is a big risk.

- As Manish Grover himself said in concall, this is a business of trust. Anybody can set up an ayurvedic hospital or launch a new product, there is no moat. But Jeena Sikho has built trust over the years (by courtesy of Manish Grover ofcourse). It is crucial that they maintain this trust. Any adverse publicity or big critical news and the downfall would be inevitable.

Conclusion:

Overall good set of numbers and a great outlook ahead. Bed additions, Occupancy and New OTC product launches remain key trackables.

6 Likes

I have a prepective regarding Jeena Sikho. Ramdev came to be the sensation maybe around 2005 , he was much bigger sensation than Acharya Munish.

But in the end he had to pivot towards FMCG which he successfully did. Unlisted Ptanjli Ayurved has around 6,000 crore revenue and we don’t know how much money comes from ayurvedic products and how much comes from clinics.

So I don’t know how long they can keep posting this kind of numbers and we have precedent of Baba Ramdev.

2 Likes

I don’t know either. It’s a risk we take in almost all businesses one way or the other, although the degree of risk varies ofcourse.

I judge the businesses based on their execution senstivity & error consequence. If they are high, I size the position small or medium only if valuation is not rich, but never large allocation.

Regarding Ramdev part, the thing is Ramdev also had clinics and centres (probably still has). But he is too much politically exposed, and there are too many shady practices of his clinics’ being highlighted by independent media (not the usual TV ones, you may look up on youtube). He has done many false advertisings, faced supreme court rulings several times, had to issue apologies etc.

Till now, nothing such sort of thing with Jeena Sikho. Though, they also had some dubious ads, but nothing big to highlight. Even thats stopped now, they have started to say allopathy, homeopathy and ayurveda all have to work together to heal india. Focusing on r&d as well.

But, there are early signs of them forming a religion/cult like following, which is evident from the investor concall as well. But I don’t know if I should look at it in a bad lens or good one, as of now. Only time will tell. I have my risk measures in place if something goes wrong  .

.

3 Likes

I was listening to the radio and their ad got played. I was shocked by the casual claim of curing just about every disease including cancer. That was a red flag for me.

PS: Never been invested.

3 Likes

Yeah, that’s the riskiest part, them making dubious claims, which can hurt their reputation overtime.

Even in their PPT, there are testimonials of people claiming to be cured from cancerous lumps with just panchakarma, which obviously can’t be true.

2 Likes

I have been following this counter since long time. Mind you my view maybe biased as I am ENT surgeon practising since 15 years. Have been investing since before COVID era.

What I fail to understand is the valuation of Jeena Seekha Vs say HCG. Both are near the same market cap.

HCG - Health care global is the largest oncology chain in India. Imagine how many oncosuregons, medical and radiation oncologists they maybe employing. They maybe having many advanced Da Vinci robotic systems ( costing several crores) with them. Also so many oncology drugs, many advanced radiation techniques ( again costing in crores)

Now compare that to Jeena Seekho - Panchkarma, Beds and ayurvedic medicines.

I simply don’t get it.

Yes. market loves growth and asset light businesses. But this surely looks off.

TOO GOOD TO BE TRUE.

Maybe some accountant in this board finds some corporate governance issues when studied in depth.

Not invested and not going to.

The valuations are simply not justifiable even on common sense.

Personal Opinion.

5 Likes

Ummm Sir, Sorry for my naive question, but couldn’t understand.

Are you trying to imply Jeena Sikho is overvalued vs HCG or is it undervalued?

Very Good Q. Yes. I feel both ways. Jeena seekho is overvalued and HCG is relatively undervalued even compared to other hospital chains.

My conviction in HCG is because of 2 people - Sajal Kapoor and Aditya Khemka. ( please search for their youtube videos)

I am invested and biased in HCG. Its around 10% of my stock holdings.

Personal opinion.

1 Like