I will keep the format of this analysis relatively simple- About, Positive, Negative and Management.

ABOUT

Jeena Sikho Lifecare is one of the leading Ayurvedic healthcare system providers in India. The company has been providing healthcare services for the last ten years.

The entire issue was a fresh issue that the company utilized to

-

To undertake marketing and sales promotion (no plans to do their own manufacturing).

-

To repay the short-term loan.

-

To meet the Working Capital requirements of the Company.

The company has a portfolio of a wide range of Ayurvedic products. The company also conducts various health checkup camps, and yoga sessions free of cost to make people aware of their health problems (customer acquisition, marketing and educating people about their products).

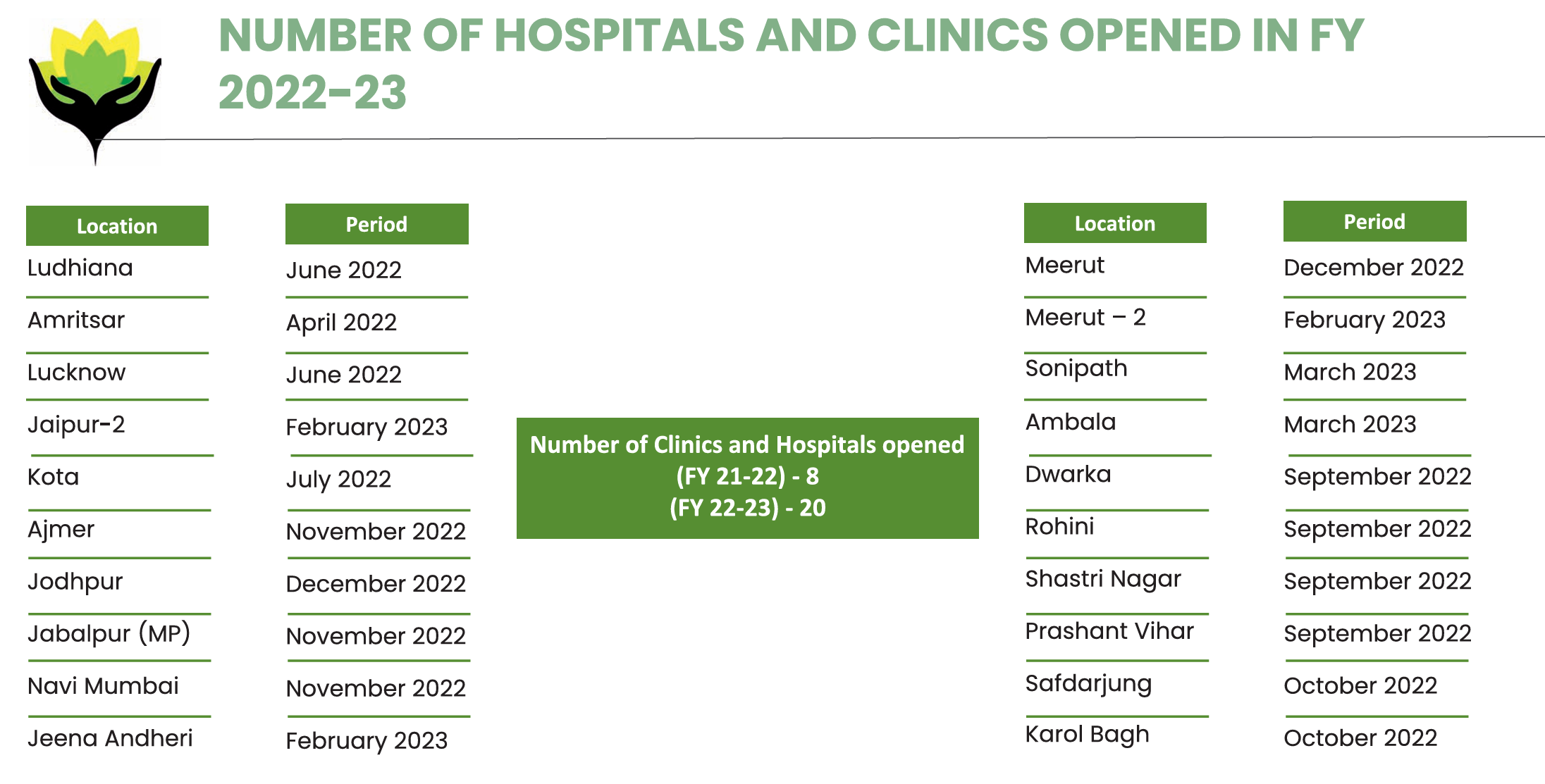

Operating 150+ Ayurvedic clinics in 23 states, out of which 9 clinics are owned & operated by it with the rest of the clinics being operated by franchisee partners on a commission basis. To maintain quality, all franchisees must follow JSLL’s standard operating procedure. (Shalby biz model).

The products are manufactured by those engaged in retailing of Ayurvedic products. The products are manufactured by a third party with prescribed quality standards which are branded under “Shuddhi”. After that, the company advertises it and the consumers connect with their Customer Support and can buy their products through their distribution channels.

Through Shuddhi Ayurveda Panchkarma Hospital (HIIMS) Co. offers treatment for Cancer, Diabetes, Liver problems, Arthritis, Cholesterol, Thyroid, Leukoderma, Joint pain, and many more through different methods such as Ayurveda, Allopathy, Homeopathy, and Naturopathy without leaving any side effects.

The company has 6 OSP Call centers through which customers can place their product orders and allows them to contact the nearest Shuddhi clinic.

Range of Herbal/Ayurvedic products:

Dr. Shuddhi Package (Shuddhi Kit) – 40-Day Detox Package

Shuddhi 32 Herbs Tea

Shuddhi Addiction Free Kit

Shuddhi Addiction Free Kit

Shuddhi Diabetes Care Package

Shuddhi Divya Sanjeevani – Antiviral

Started ‘’Shuddhi Ayurveda Panchkarma Hospital’’.

Basically, these are small clinics

WERE DOING A DEMERGER BETWEEN SHUDDHI LIFECARE PRIVATE LIMITED (DEMERGED COMPANY) AND JEENA SIKHO LIFECARE LIMITED (RESULTING COMPANY). The hospital business and retail business.

The documents were returned by Sebi as there was some error in the document.

The management will correct the mistakes and try again.

HIIMS is separate from the Shuddhi clinic business.

Origine Naturspired offers beauty and wellness products that help to nourish skin, hair, health, and face naturally.

At, HIIMS one can avail of Ayurveda, naturopathy, homeopathy, naturopathy, and panchakarma treatment services for healthcare for every critical health concern.

No one can confirm if the products and treatment of this company are actually helping people and treating them successfully. We need a lot of patients or the company’s product users to agree in unison about their authenticity.

A Chain of 150+ Ayurvedic Clinics All Over India

A certified team of 200+ Ayurveda doctors

The treatment is not just based on products but on changes in lifestyle

They are more of teaching people how to live rather than selling products

Can do complex treatments through Ayurveda at Hiims, according to them.

Patients with kidney failures undergoing dialysis are being treated naturally without any modern machines or ways but by ayurvedic treatments. And the kidneys are getting healthy again and have stopped dialysis.

Even serious incurable diseases like bp, asthma, cancer, and heart problems are being cured.

With medication, food, and lifestyle, yoga is also important.

Profile of one of the doctors at their Clinics: Dr. Nidhi Punia: Dr. Nidhi Puniya has more than 10 years of experience in Ayurveda. Her areas of expertise include the management of diabetes, kidney disease, rhinitis, sinusitis, liver disease, joint pain, piles, paralysis, depression, etc. many individuals have benefited from her Ayurvedic treatment. Her motive is to spread information about the ancient old heritage healing system of Indian culture-“Ayurveda”.

Some of the competitors are as follows:

-

Jiva Ayurveda

-

Zandu Ayurveda

-

Swastik Ayurveda

NEGATIVES

Is this diversification or diworsification- The retail business is asset-light with higher cash flows, as there are no fixed costs incurred. Added the hospital business with costs of infrastructure, doctors, maintenance, etc (although doing it through franchises), and also opened itself to various regulations that need to be followed by hospitals and clinics. Even for the franchise owners to follow all the rules and not conduct mismanagement it seems difficult and doubtful, this will impact the brand name of JSSL.

Weak distribution- The majority of revenues are from call centers. This is not so scalable and people nowadays don’t prefer to go through calls to order products, they like to do it at the touch of a finger (although they do sell through online means, but its very minimal).

Trade receivables have increased significantly, this should be a cash business right, because it is serving B2C clients. (risk).

Shuddhi Ayurveda Panchkarma Hospital, the point is that many people in tier 1-2 cities don’t believe in these therapies (forget the critical application cases of heart/kidney/diabetes problems), so they have opened these clinics in the perfect locations (tier 3 and 4 cities)

But then there is a risk of scalability, whether they can start and grow these clinics in tier 1 and 2 cities.

The hospitals in Thane, Laxmi Nagar, and Prashant Vihar seem to have a lot more manpower than others, leading to higher costs (images below in positives).

Ms. Nikita Juneja tendered her resignation, dated June 2, 2023, from the post of Company Secretary and Compliance Officer the Company, and no reason was given.

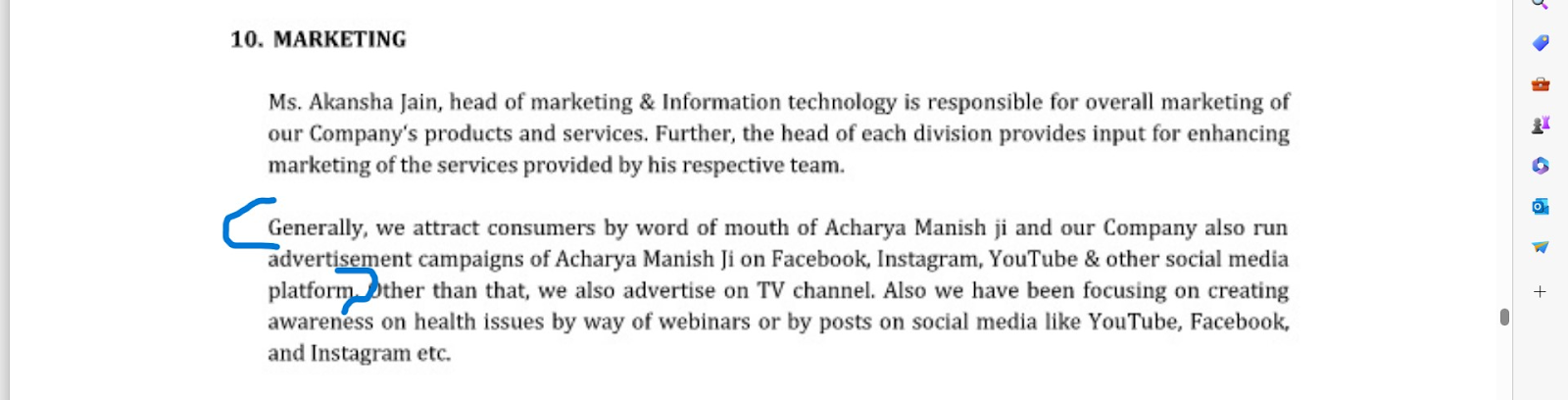

The retail business packaging has the branding in the form of the MD’s photo, it seems they are basically selling the products through his name and do not have their own recognition (huge risk).

Acharya is the producer of the Narendra Modi movie, starring Vivek Oberoi. Why not just focus on the Jeena Sikho business and deploy money (although it is his own money, he can do whatever he wants) for its growth rather than becoming a movie producer?

Promoters focus on their business and increase their stake as much as possible if they are confident in its growth. He is rather investing his money in a movie that has a huge chance of becoming a flop (can also be a huge success) because that’s how the movie business is (not meaning to say anything regarding the movie or its storyline), let alone the lead actor is forgotten (no recognition).

This may lead to lack of liquidity on the side of the promoter if the movie fails, also may lead to lack of focus by the MD on the operations of the company.

Only 2 reviews on the website of Jeena Sikho, something seems off as they talk about 1 million satisfied customers. Image from their website.

Low awareness about Ayurveda, will need to do high spending to educate people about the benefits and cons of Ayurveda.

According to them HIIMS is able to cure diseases like bp, asthma, cancer, and heart problems.

If this is true then why are hospitals even existing? They say they cure diseases with no side effects, even diseases like cancer are cured (no official cure found).

If this is true then just the awareness needs to spread nothing else, it would already be big through just customer referrals.

Major risks for the ayurveda industry are regulatory concerns, consumer perception, and competition. There are a lot of unorganized players with small shops and establishments, providing the same type of treatment.

They intend to expand domestic reach, currently having a limited presence, this they are planning to do by giving low-price solutions, this will lead to margins dilution as expansion increases.

No Edge- Management believes that the competitive edge they have is providing satisfactory grievance redressal mechanisms and long-term customer relationships, that’s no edge in my opinion, but rather a requirement (learned this thought process recently from a great and humble investor).

The company and Directors of the company are currently involved in certain legal proceedings.

This case was against the company. A few other cases with the same statements are against the promoters and directors.

There are also a few cases regarding property and PMLA (prevention of money laundering act).

“A team of doctors on Friday, March 03, 2017, raided one of our group concern Divya Upchar Sansthan`s store twice, on the allegation that center is selling a drug, ‘Divya Kit’ at the cost of Rs 4,200 and claims that all diseases can be cured from this medicine. Further, after the investigation, all of these allegations were found malicious & false but no formal clean chit has been given to Divya Upchar Sansthan & no further action has been taken by the health department. The firm has given their clarification, but no reply has been received by the Union health department of Chandigarh’’.

Were there Under the table payments to clear this?

Misleading the customers with wrongful marketing?

There is a chance that none of it will be true, it’s just my assumption.

The activities of their franchisees, agents, or distributors could have a material adverse effect on their goodwill and the “Shuddhi” brand (the sale of their products is dependent on the brand recall).

The illegal distribution and sale by third parties of counterfeit versions of their products could hurt their reputation and business.

They don’t have a manufacturing facility, all the manufacturing is done by third parties, and they have not entered into any long-term agreements with their manufacturer for the supply of our products and accordingly, they may face disruptions in supply from their current third party manufacturer/suppliers.

Promoters did a bonus issue within the year before the IPO.

The average cost of acquisition of the equity shares was less than the face value after the bonus issue was conducted for the promoters.

Misdoing by the management, not a shareholder friendly decision.

have not applied for patent rights for formulations for any of their existing products.

Punjab & Delhi contribute to a substantial portion of their revenues for the period ended on September 30, 2021, & the year ended on March 31, 2021, March 31, 2020, & March 31, 2019. Although this has come down from 95%, still high at 88%

They operate in highly competitive market segments that are highly fragmented among several market participants. In the general ayurvedic product market, they compete with numerous multinational and Indian companies with sizable market shares as well as the broader industry comprising numerous small competitors. They also believe that free information available on their and other internet websites about ayurvedic products & homemade remedies also poses a competitive risk. Moreover, barriers to entry for the market segments in which they operate are generally low. They anticipate these low barriers to entry, combined with forecast growth potential in the ayurvedic industry, will lead to increased competition both from established players as well as from new entrants in the industry. This could include attrition of their staff to their competitors or the staff establishing competitive enterprises.

Promoter Group entity “Divya Upchar Sansthan” is authorized to carry out business similar to that of JSSL. As a result, conflicts of interest may arise in allocating business opportunities between their Company and JSSL.

High risk of increased related party transactions with promoter groups, already happening but can increase further.

POSITIVES

The return ratios are spectacular- at close to 100% (seems very odd)

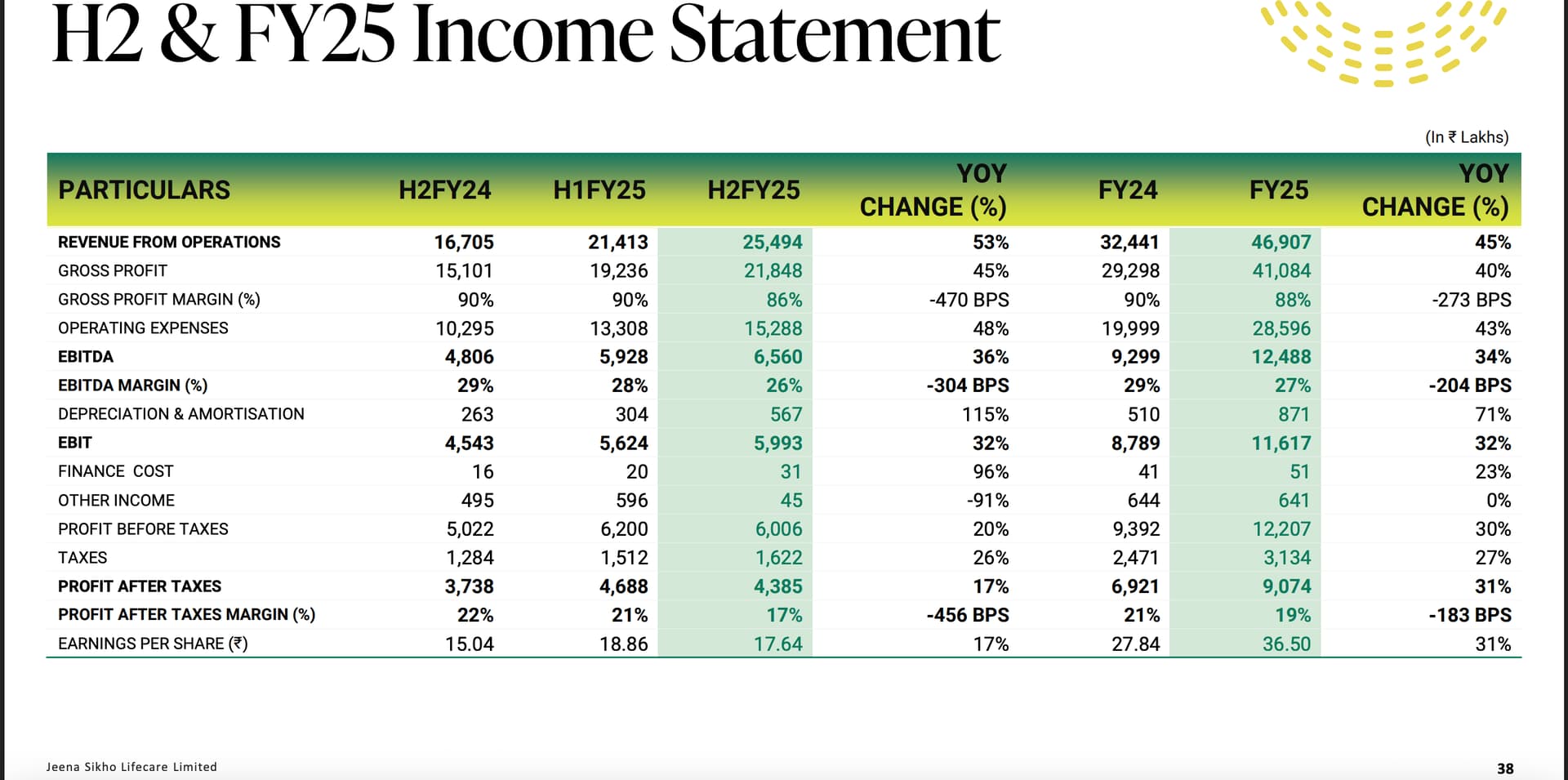

Mar 2019-22 there was no significant growth (maybe due to covid), then growth kicked in in September 22 where margin and topline increased, this also continued in mar23

Borrowings have reduced to negligible from 16 cores previously.

Doubled assets from 19-21 from 13 to 24 crores, then doubled the assets again from 22-23, 28-60 crores

Cash flow from operations has been increasing y-o-y.

Promoters have increased their stake from September to March 23, from 65.89 to 66.20

Establishment of new ‘New Shuddhi Ayurveda Panchkarma Hospital’.

According to the hospital industry, new hospitals take 2-4 years to breakeven, as these clinics are small the breakeven should be faster. They also follow the franchise model, which reduces capital investments further.

Hospital & Institute of Integrated Medical Sciences (HIIMS) Delhi (NCR), India has been conferred with a certificate for being Asia’s Biggest Integrated Medicine Hospital given by WorldKings (world record union). The certification has been given to their hospital having 1000 beds and provides various range of services like OPD, IPD, and Day Care including therapies like Postural Medicine, Zero Volt Therapy, Living Water Therapy, Light Therapy, Panchkarma, DIP Diet, Meditation, Yoga and Circadian Timeline and the said Hospital was founded by their Managing Director, Shri Acharya Manish Grover.

They are following the Shalby model, one big hospital (HIIMS) and a few small clinics (Shuddhi hospitals), advanced/complex surgeries at the big hospital, and simpler treatments at clinics (in my opinion).

At Jeena Sikho Lifecare, they believe in treating any kind of disease whether it be kidney problems, liver problems, cancer, diabetes, or high blood pressure in such a way that leaves no side effects behind and also helps people to get rid of these diseases for once and all. - if this truly works, then this company can be big. This will be the place where people come from throughout the world for being treated, but it is a big IF.

Company is focused on cost management, they look to operate the business at the lowest cost possible.

India’s ayurvedic products market exhibited strong growth during 2015-2020 and is expanding at a CAGR of around 15% during 2021-2026, according to them.

MANAGEMENT

All this info will be from his website https://acharyamanish.com/. Why does he have his own website though? Isn’t the company website enough, or does he also want to sell through his website (shady)?

Also there is no mention of his company Jeena Sikho on his website (shady again).

The company is run by a renowned Ayurveda Guru “Manish Ji”(key man risk).

Acharya Ji is reckoned as an ingenious practitioner of Ayurvedic Medicine. Drawing from his own experiences, profound wisdom, intensive research, and dogged devotion to the health & wellness cause - Acharya Manish Ji has relentlessly and intuitively worked on concocting some of the best holistic Ayurveda treatments for various ailments and diseases.

Based on Ayurveda sutras, his treatment methodology works on addressing the root cause of disease and balancing the tridosha(vata, pitta, kapha) - by aptly using Ayurvedic principles of detoxification, purification, recuperation, and rejuvenation.

For over two decades, Aacharya Ji has been helping people by acquainting them with the wonders of Ayurveda.

Through his TV Shows, Acharya Ji has been earnestly spreading awareness about the wonders of Ayurveda. And how it can address different health issues, ailments, and diseases.

Patients from all across India and abroad share their health concerns with him in the TV Shows. Acharya Ji listens to their concerns and health issues. He counsels them, guides them, and suggests the ayurvedic solutions. People avidly look forward to his TV Shows and Live Events. Watch and enjoy the Videos.

In 2009, an effective and innovative Ayurvedic medicine kit (Divya Kit) was unveiled. It’s a complete Ayurvedic package that helps improve digestion, boost immunity, balance hormones, and trigger detoxification

Legacy planning is secure with Shreya Grover, the daughter of Manish Grover being in the company.

Conclusion

I haven’t gone through the financials deeply, as after understanding the story I didn’t want to waste further time on this company.

In my opinion, this industry is meant to be unorganized and very difficult to change.

Ayurveda as an industry seems promising but I think this is not the company through which it is to be played.

Is the company a fraud, we don’t know that, what we know is that there are more than 5000 listed companies except for JSSL, I found more negatives than positives. Hence I will stay away.

I was blunt in this analysis and maybe a bit biased towards the negatives. Don’t take this analysis at face value and try to research on your own, and maybe if you find something interesting or contradicting to my view, do share.

Always open to criticism.