Being their client for multiple water treatment plants across India and Overseas. They are first choice for sluice gates, primary inlet screeners etc but their drawing and especially electricals sucks, very poor with electrical drawing for Distribution board of these gates. Have to go for 5-6 revisions before its technically approved. I believe they outsource some of their work.

8 Likes

Could you tell us how long your company has been sourcing from jash and how that relationship has evolved over the years. Why deal with jash and why not someone else. Also Please share your company name if you are at Liberty to do so. Thanks

1 Like

Great insight, appreciate it. So is that a major deterrent to you (and other companies) or is it just one of things which Jash sucks at and you can live with? Also, given your knowledge of such business, does Jash stand a good chance of becoming the number #1 player in most of the products they sell? Would be really helpful if you can throw some light on the TAM for this business and how you see Jash in the race for a dominant market position? Thanks.

1 Like

You also need to see the Sep order pipeline (17 crs only). While Aug has been good and no doubt company is doing well, the 100 odd crs order book could also be a lot of what could have come in Sep got preponed to Aug. Disc - invested

2 Likes

Majority of orders are outside of India. In current scenario when rest of the world is slowing down, order postponement/cancellation presents big risk for the company.

3 Likes

Old orders might get delayed or cancelled but new order wins have been way better than last year. Anyone placing orders in such times is doing so after much thought

2 Likes

Water is too critical for delays and order cancelation. Flooding caused by excessive rains and global weather change could push demand for replacemnet and new valves and gates.

1 Like

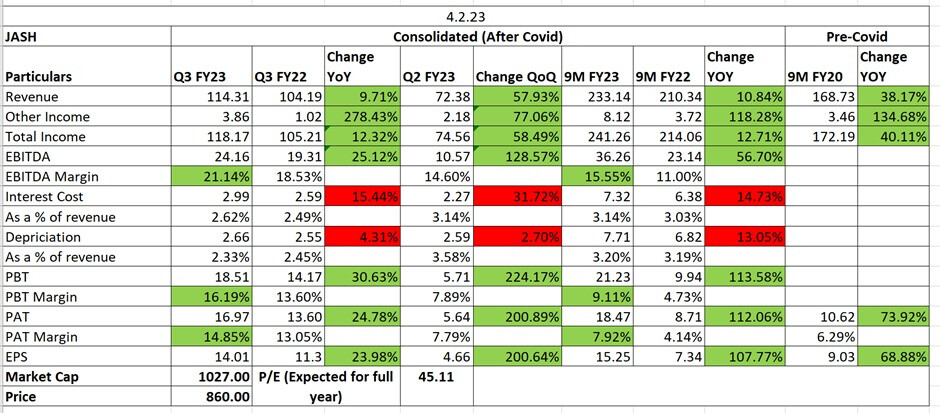

| - | Giving a sales outlook of 430 cr on a consolidated basis for FY22-23. Out of which only 118 cr has been achieved as of H1 FY23. They are very confident in achieving 430 crs of revenue. |

|---|---|

| - | There is growth of 30% in standalone revenue but lower dispatches from subsidiary companies have subdued the 1 st half consolidated results. However looking to the billing already achieved till date we are quite confident of significant jump in Q3 revenue on consolidated basis. |

| - | Improvement in Q2 profitability on standalone basis augers well for annual profitability because in subsequent quarters revenue is expected to grow at a sustained pace. Profitability of subsidiary companies is expected to significantly improve as their Q3 revenue improves. |

| - | Raw material prices are going down which is helping in improving profitability. |

| - | Expecting order booking to get significantly higher in next 4-5 months as lot of contracts are on finalization. |

| - | India & America are the strongest countries for Jash in terms of revenues. |

| - | Margins are likely to be sustainable at current levels if there is no further price rise in raw materials. |

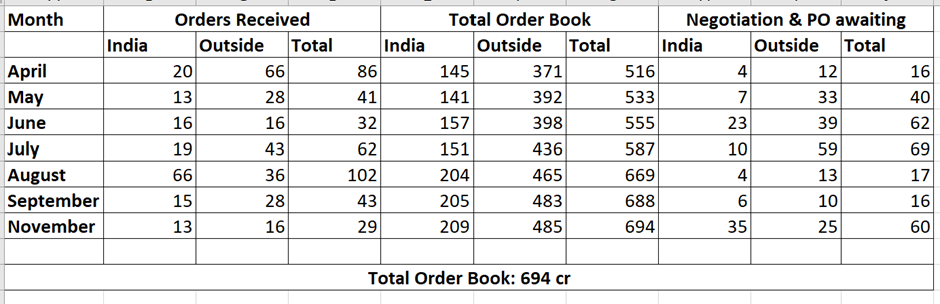

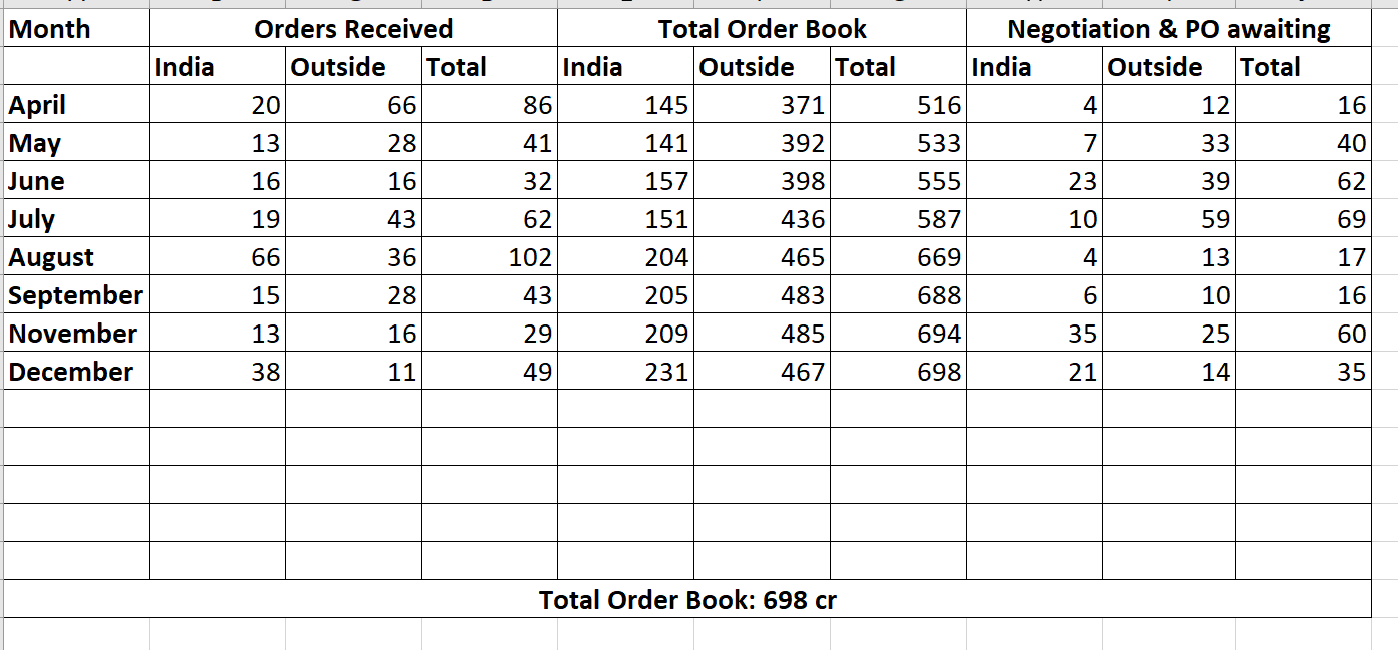

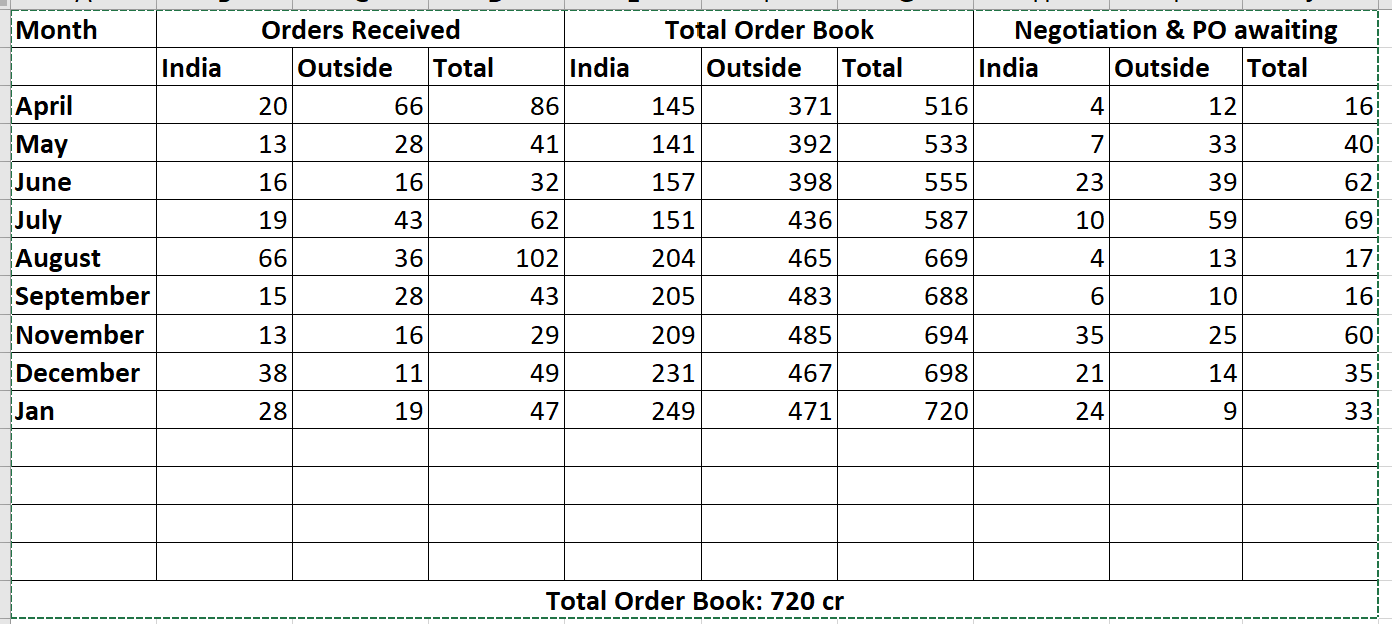

- Order Book is increasing. Negotiation or PO awaited Book is also increasing.

5 Likes

So with this update sales for the Q3/2023 would be around 95-100 crore, growth of ~ 47% QoQ and YoY, with highest ever order book.

2 Likes

The order book is also increasing every month.

Lot of fluctuations in Negotiation & PO awaiting though.

6 Likes

Jash Engi. Q3 FY23 Result Update:

- The Company has an order book of INR720cr as of 3QFY23, which is executable over the next 4-6 quarters. Order pipeline is also strong and ~INR33cr deals are already negotiated till Jan-2023 while another ~INR26cr deals are under negotiation.

- Projecting to have 430 cr revenue in FY23. 9M revenue is 230. Seems a little difficult. Q4 is a very strong quarter though.

- Want to reach revenue target of INR 750 cr by FY27. Increase PAT margins to 13-14% from 8%.

- RM prices volatility is very high. Due to which margins are highly affected.

- Jash plans to invest INR20-25cr over FY23/24 for 2 expansions – new SS fabricated facility at unit 2, Indore by Jun-2023 and new facility for process equipment at Shivpad, Chennai by Jan-2024. Jash may also invest INR20cr in new facility for gates and screens at Houston, USA by Mar-2025. Jash makes consistent operating cash flows to fund capex and dividend payout.

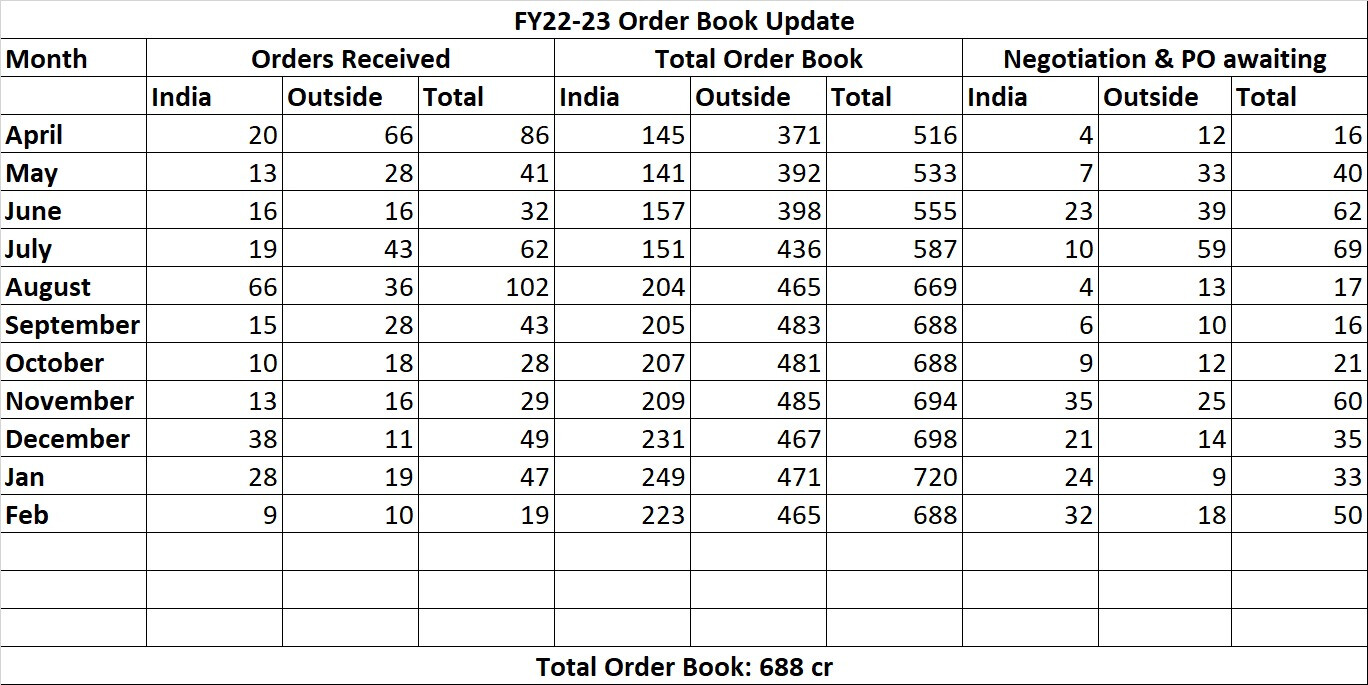

Jash Order Book Update: Provides an increasing except Feb month where they lost a 32 crore order.

5 Likes

To whom did they lose the 32 cr order and why? and what type of product?

This month one order in domestic worth Rs. 16 Cr. has been short closed due to project getting shelved.

They ve only mentioned about 16 cr project being shelved.

Hi @Lajja_Shah can you help explain how the order cycle works?

From what I understand, orders that are under negotiation have a 35% strike rate (management presentation).

Once an order is negotiated and closed, it takes about 2 months for the actual purchase order to come in.

Once the purchase order is received, at that time, that amount is moved from Order pipeline to Consolidated orders book.

Is the above understanding correct?

Secondly,

If you look at the table, the orders received are basically the same in September and October (288), despite receiving 28 orders in October.

Further, the total order book is still 688 Cr at end of Feb - same as it was in Sep.

Does this mean, they have lost some orders and gained some and the net order book is still the same without much progress?

Or does it mean, that since the October 688Cr order book, some of that is already in execution and has been moved from order book towards revenue generated and so it’s not actually a sign of lost orders?

Thank you.

Discl- invested with small tracking position

1 Like

Your first understanding is correct.

In second, it is difficult to determine how much goes to revenue as they do not give any clear indication. Both the possibilities could be there but more likely is the possibility of net order book as if they would have started execution, wont be a part of order book.

Thank you.

Wondering if we can get more clarity on that.

It would be helpful to model out future revenue.

If we know what the monthly run rate for order pipeline is, the strike rate, and the average time to execute an order, and the attrition rate (cancelled order rate) we can at least come up with some approximation of future revenue.

Seems like to increase revenue growth, first they will have to have enough booked orders (which seems like they already have) but they will also have to execute faster if they want to recognize that revenue early.

The 2nd part of that will require investment in resources/infra so some clarity around how they can accelerate that would be helpful from management.

1 Like

You can refer to this report… might get some idea

1 Like

Thank you.

It says "The Company has an order book of INR720cr as of 3QFY23,

which is executable over the next 4-6 quarters. "

That’s not bad, so majority of the revenue should be recognized by FY 25, or max FY 26.

In that case the revenue for FY 27 should be much higher than 750Cr which the company is aiming for.

Thank you for this, will try and see if I can get some more specific info.

1 Like