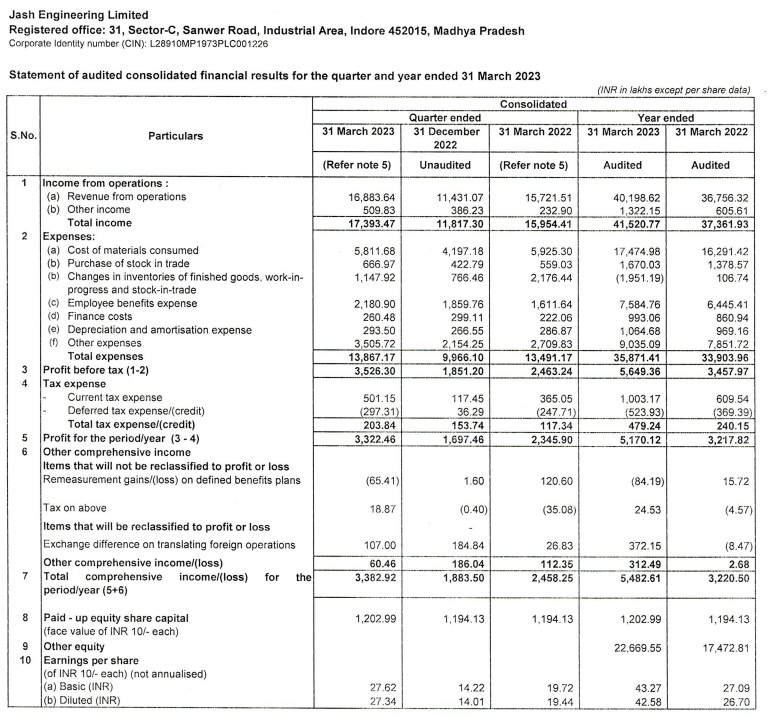

With todays update JEL is expected to do Rs.177 crore revenue for Q4 2023 and consolidated revenue of Rs. 386 crore for FY 2022-23.

1 Like

Not sure how did you calculate Q4 FY23 revenue from the update. Can you please clarify?

very helpful… thanks for updating this regularly

1 Like

Good result from Jash !!!

Dividend 6RS since company is celebrating 50th anniversary ![]()

The Board discussed and granted an authority about the investment related terms, rights and

arrangement between JASH Engineering Limited, India and Waterfront Fluid Controls Limited, UK

in view of the transaction – Potential Acquisition of 80% share capital of Waterfront Fluid Controls

Limited, UK subject to satisfactory confirmatory due diligence, plant/factory visit, management

meetings/discussion, regulatory approvals and execution of the transaction documents as

recommended by Due diligence agency after their report

6 Likes

Has the company released their investor presentation? The management in the concall is talkin about a UK competitor going bankrupt. Can someone help with the name of that?

1 Like

Waterfront Fluid Controls Ltd, UK

Presentation can be downloaded from this link, PDF file ~9MB

https://archives.nseindia.com/corporate/JASH_23052023194102_INVESTORPRESENTATION23052023.pdf

2 Likes

Company has shared some information with investors to clear their doubts and answer some questions we may have.

‘Human waste water and Industrial waste water cycle : This comprise 60-70% of total sale.’

‘For over 80% of our clients we have payment terms of either before delivery or post dated cheque or LC with a credit period of 45-90 days’.

‘We are targeting annual growth between 15-20% and expect to cross Rs. 1000 crores

turnover in 6 years time that is by 2029-30’.

‘After the acquisition of this company in UK, the company is not contemplating any further

acquisitions in the near future. The reason for this that the company will still take 3 years

to realize the full potential of the acquisitions in UK and the acquisition of Rodney Hunt in

USA’.

4 Likes

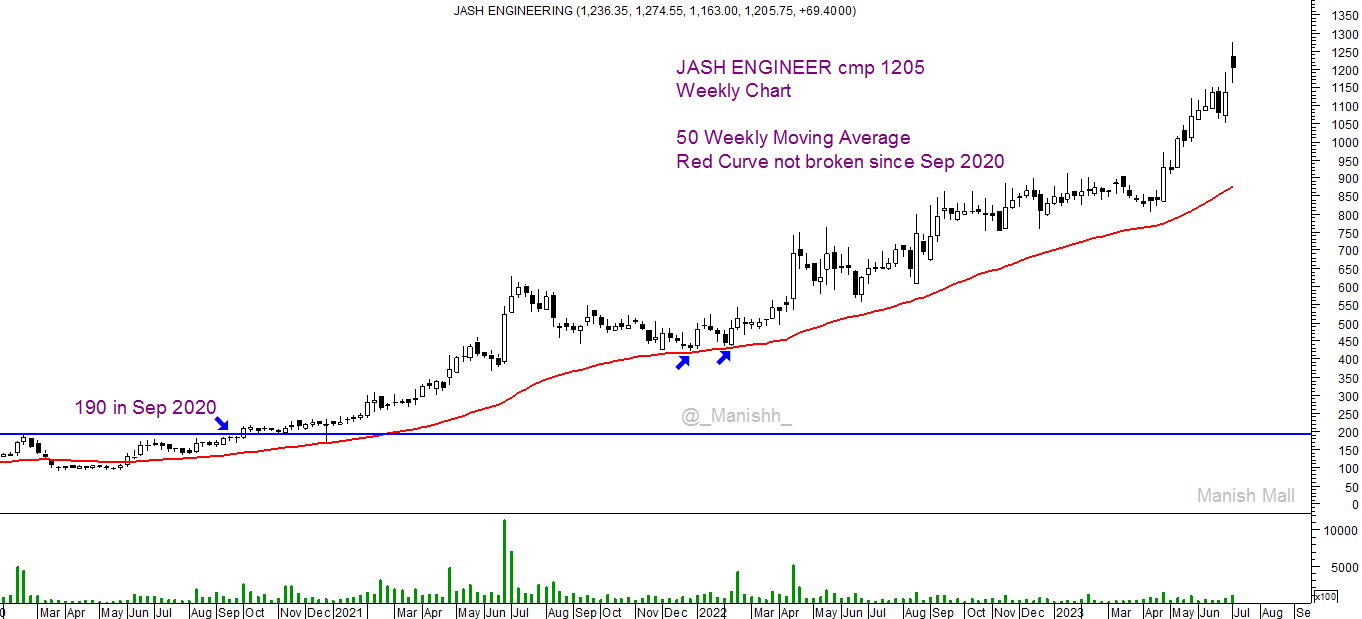

I had earlier posted chart of Jash Engineering around 190 in Sep 2020

and than a follow up chart around 400 , Cmp 1205

Though i have a very small Allocation left now,

was going through the chart today which was without Moving Averages since long time

Today attached 50 WMA ( Red curve ) and was surprised to see how

JASH has not broken this 50 WMA since Sep 2020 after all the Volatility of Markets

in Hindsight if i had this WMA since earlier would have helped in

Riding Full qty , even doing Canslim at times .

Just posting a Chart for Self Learning how one can Technically Ride the trend.

and what’s the Current Fundamental views now

7 Likes

Thanks for this @devarshi84 . I never they were into “Treatment Process Equipment” too.

Municipal / urban sewage treatment is a big focus area in swachh bharat . The treatment of municipal wastewater involves various methods, including physical, chemical, and biological processes. Physical processes such as screening and sedimentation are used to remove large solid particles and separate them from the liquid portion. Chemical processes, such as coagulation and disinfection, involve the addition of chemicals to facilitate the removal of dissolved contaminants and kill pathogens. Biological processes, such as activated sludge or trickling filters, utilize microorganisms to break down organic matter and nutrients.

1 Like

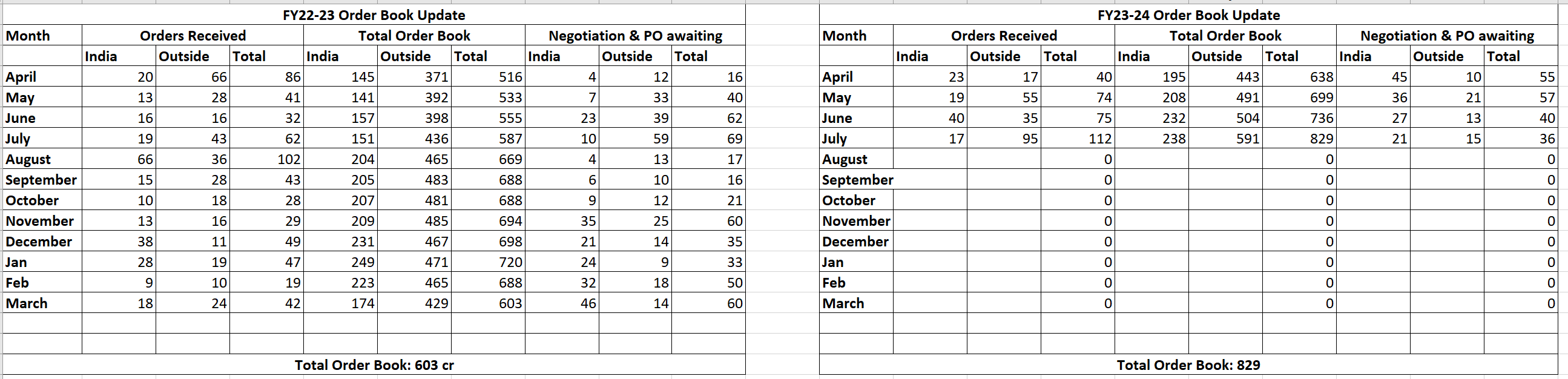

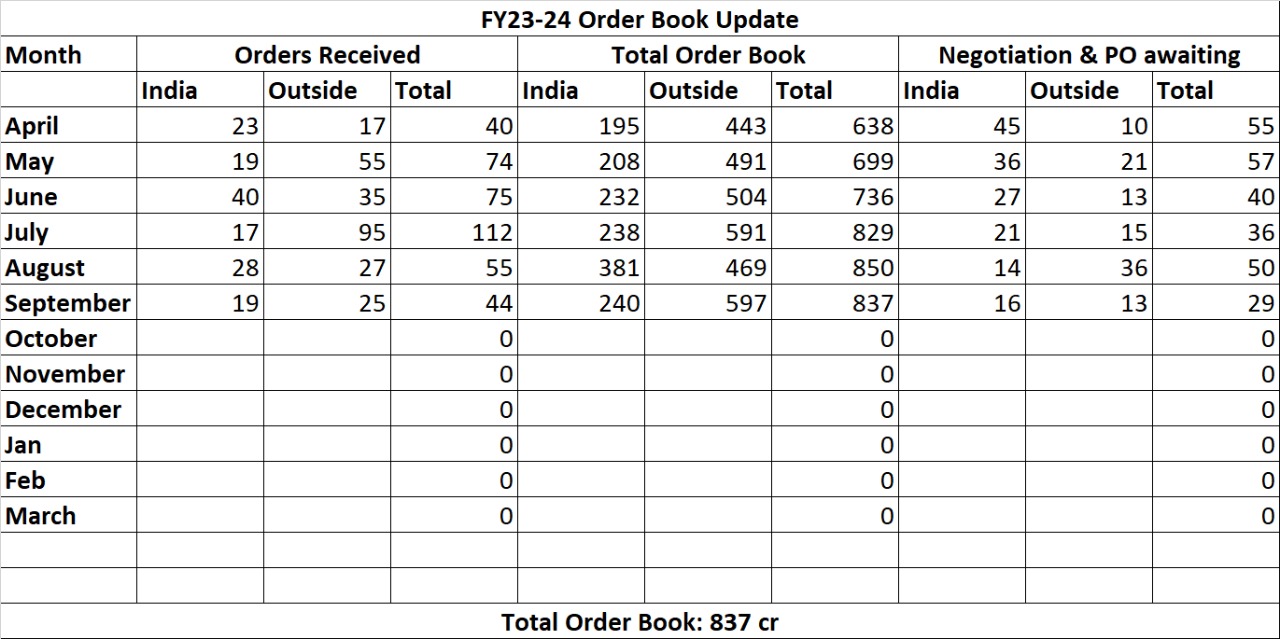

As per estimates, for Q1 FY24 sales should be around 56 crore and considering low volatility in metal prices they should be able to do positive PAT (yoy).

2 Likes

Very solid numbers for Q2 FY 2024.

Based on order book updates for Q2 FY 2024, Company may report sales of Rs.110 crore at least. The margin for Q2 is also expected to be on higher side in comparison to YoY.

1 Like