Comparison with VA tech financially is presented in this video

Comparison with VA tech financially is presented in this video

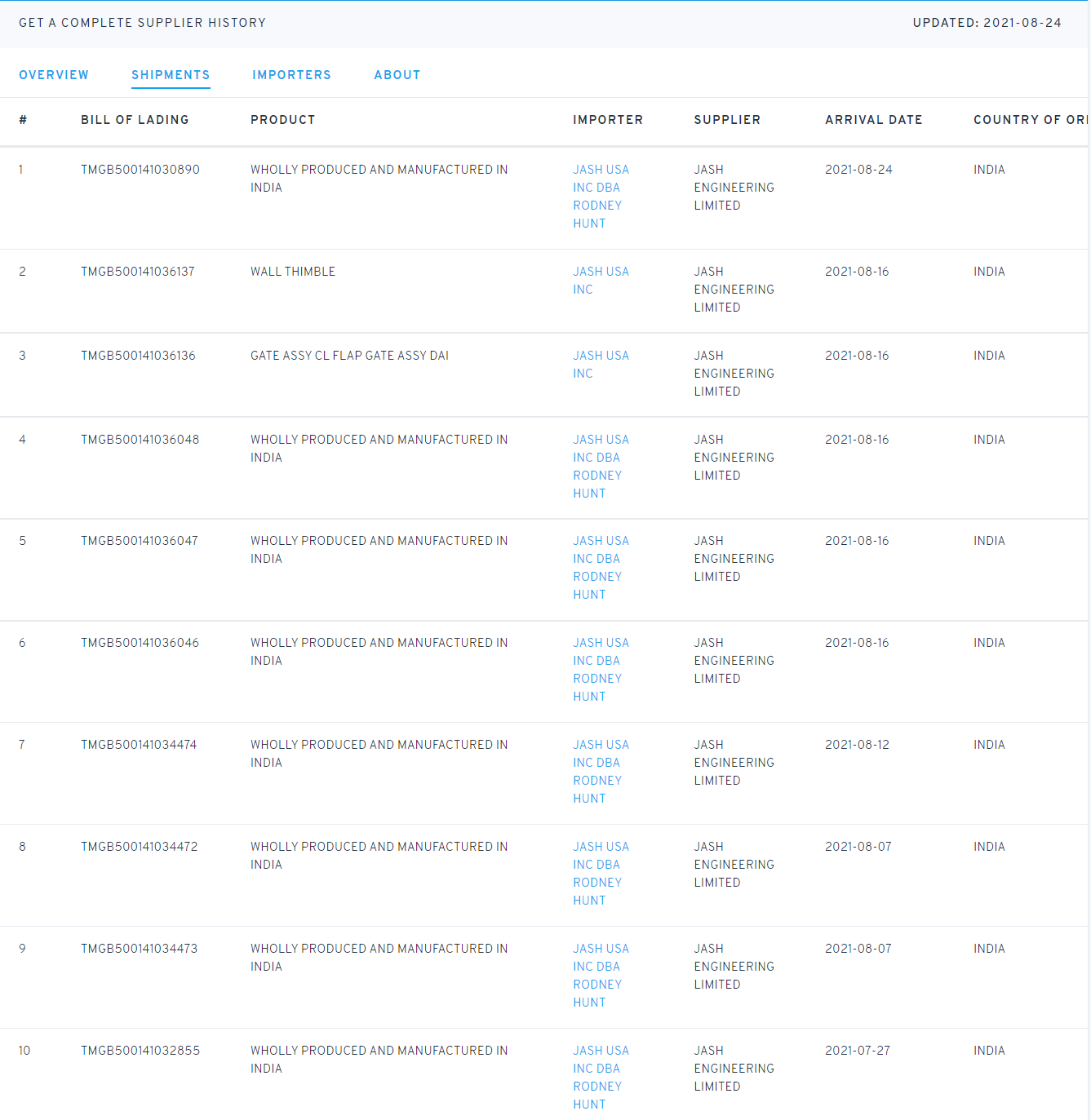

Company’s recent update shows good results for August.

The Swachh Bharat Mission-Urban 2.0 envisions a plan to make all cities garbage free by ensuring grey and black water management in all cities except those covered under AMRUT.

Does this mean more orders for Jash Engineering?

What is the lifespan of the products that Jash manufactures? Do the installed products need to replaced after a specific time period as part of maintenance or something?

Disclosure: Tracking

Flash floods due to climate change is going to spur demand for flood security systems

Is it going to benefit Jash?

Very nice interview of Mr. Pratik Patel, Managing Director of JASH.

Jash has been able to maintain the monthly order inflows. The order book momentum is also healthy with 476cr worth at hand.

The Jump in Rodney Hunt business is good news.

Jash has come to my notice quite late it seems through a successful stock picker I’ve been following on Twitter. Read and listened to Q2 and Q3FY22 concalls to understand the company and what it’s been doing recently. It seems like a company Peter Lynch would buy or recommend. After reading the posts here, I feel the company is poised for growth and has a long runway because of its long history and the kind of industry it’s in. Plan to read the AR and DRHP for more insights and make a pilot buy tomorrow.

good results and a very encouraging con-call. Rodney hunt should break even this year. Orders are getting bigger. New clients are getting added. Product portfolio is constantly expanding. IMO The next few years should see strong earnings growth even if RM prices doesn’t cool off from here. Earnings would be largely driven by exports. If for some reason domestic picks up it will be a bonus… Considering all this Valuations are still very reasonable

Disc: invested

Q3 con call updates Jash Engineering:

Investor FAQs

Very insightful. Looks like all the acquisitions they made will start contributing to the overall Sales and PAT in a significant way in 2-3 years time. It does look like a company that is well planned out in terms of how and where they want to be in 3-5 years’ time i.e. de-risking by spreading across India, Americas and RoW, a plan in place to increase PAT to 14% in 4-5 years time. On the flip side, their accounts receivables and inventory periods have been increasing over the last 3 years. They did clarify that it is not to be taken as an indication of future bad debt problems but that is a concern. Also, any adverse impact in retaining or attracting skilled manpower (who understand their custom engineered products well) is the biggest risk according to them. So this is also a key monitorable.

It is a very detailed document covering all the details about the company like - its Moat, competitors, strengths, weakness, opportunities, capital allocation, capex strategy, capital allocation - acquitsition / tie ups, expected turnover in next 5 years…etc

Most of the details are covered as required by any investor in this FAQ document

In my view Jash will be a decent compounder giving 15-22% CAGR over the next few years driven by earnings growth (PE expansion is difficult since stock is decently valued). Given dependency on customers to pick finished goods, high WC requirement and conservative management, stock price returns of 25-30%+ looks difficult. Disc - Tracking and invested since long.

Probable reason for the sudden surge in the market capitalization.

Regards,

Dr. Vikas

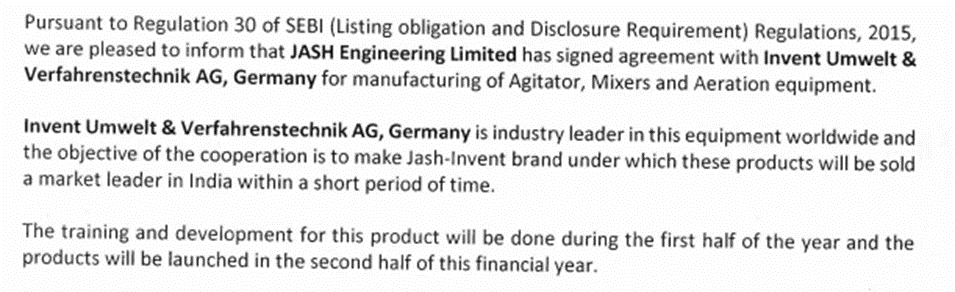

Other important updates given to the stock exchange by Jash Engineering on 9th and 12th April 2022.

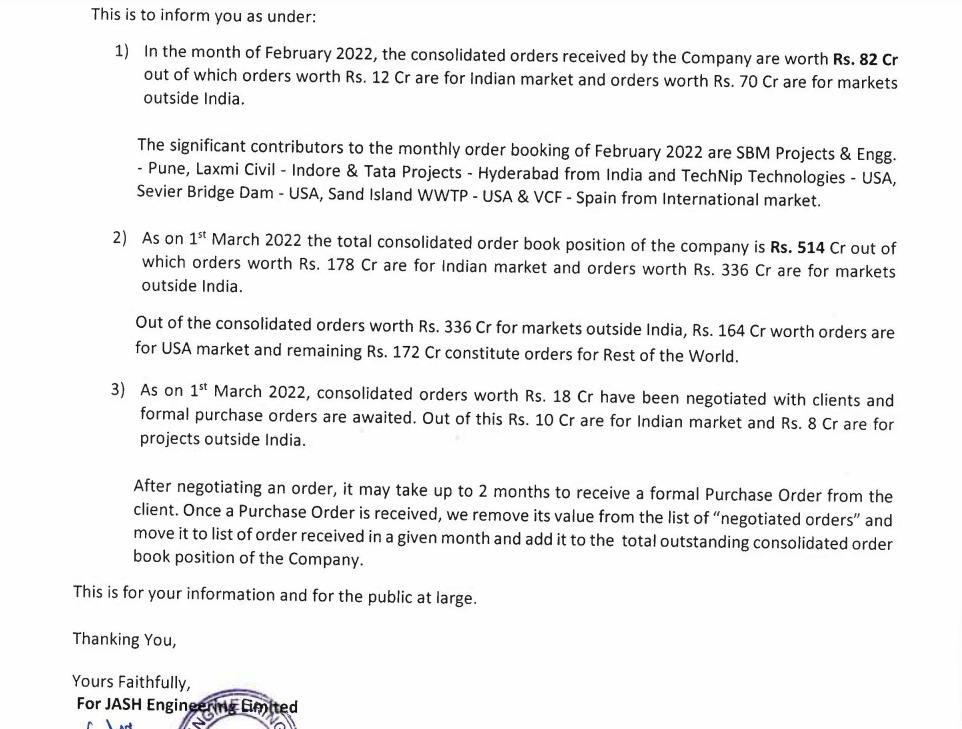

Sales Revenue Target for FY 22-23 Rs. 430 Crores.

I somehow feel if this rating update happens now - they might have upgraded the rating. The order book has become stronger in the last 2 months

Going forward, it looks like Rodney hunt is going to contribute big time to its revenues and profitability. Does anyone know how big can Jash get in terms of market cap? If they do become one of the best companies in their domain, how big is the TAM globally? I say globally because they have presence all over the world i.e. USA, Asia, Africa and Europe. And how much of it can they capture in the next 10 years or so?