As they are paid by mainly gov agencies and EPC players, difficult to solve cash flow problems. Looks undervalued, but cash flow worries stopping me to take big position.

Any view?

@Anand6

I conducted an interview with the management and I’m quite satisfied with the their assessment of the situation and planned responses.

On the point of high working capital requirements, its typical of the industry, and the management actually feels this is a strong entry barrier to new entrants since a lot of domestic municipalities run under-budgets. Typically they can get up to 40% payment upfront through letters of credit and the remaining payment is subject to a lot of issues. Their remedy is to reduce dependence on the Indian market and derive 60%+ revenue from international markets (US, Singapore, RoW)

They are already delivering on this strategy and exports have gone up tremendously. Additionally, I learnt that working capital changes will be positive for FY20 which is good for the CFO.

Between 2013-19

cPAT - ~42 crores

cCFO - ~62 crores

So I don’t necessarily think that PAT is not translated in CFO by the company.

On the valuation: I developed an Owners Earnings discount model and I definitely think this is quite undervalued. Its order book now stands ~388 crores (increasing every month) and peak revenue potential of 500 crores. Compare this with its current market cap of ~180 crores.

Target Peak revenue: 500 crores

Target PAT (management guidance of 12%) : 60 crores

Current MCAP: 180 crores

Discl - Initiated tracking position at 139/-

Warm regards,

Uzi

9 Likes

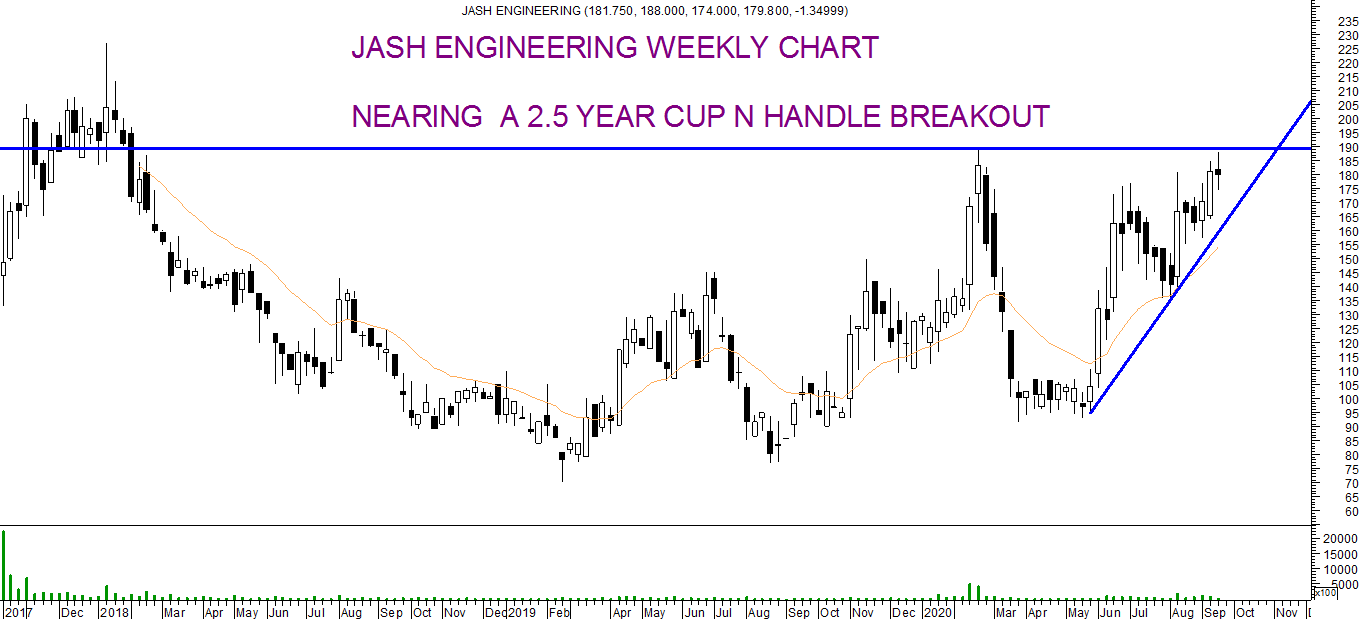

HELLO ,

looks like finally the Patience investment is gonna have a good times soon as per price action, and a 2.5 year breakout near the corner . Miten Mehta has recently invested here, are we expecting a turn around this company soon

awating a reply if anyone still tracking

1 Like

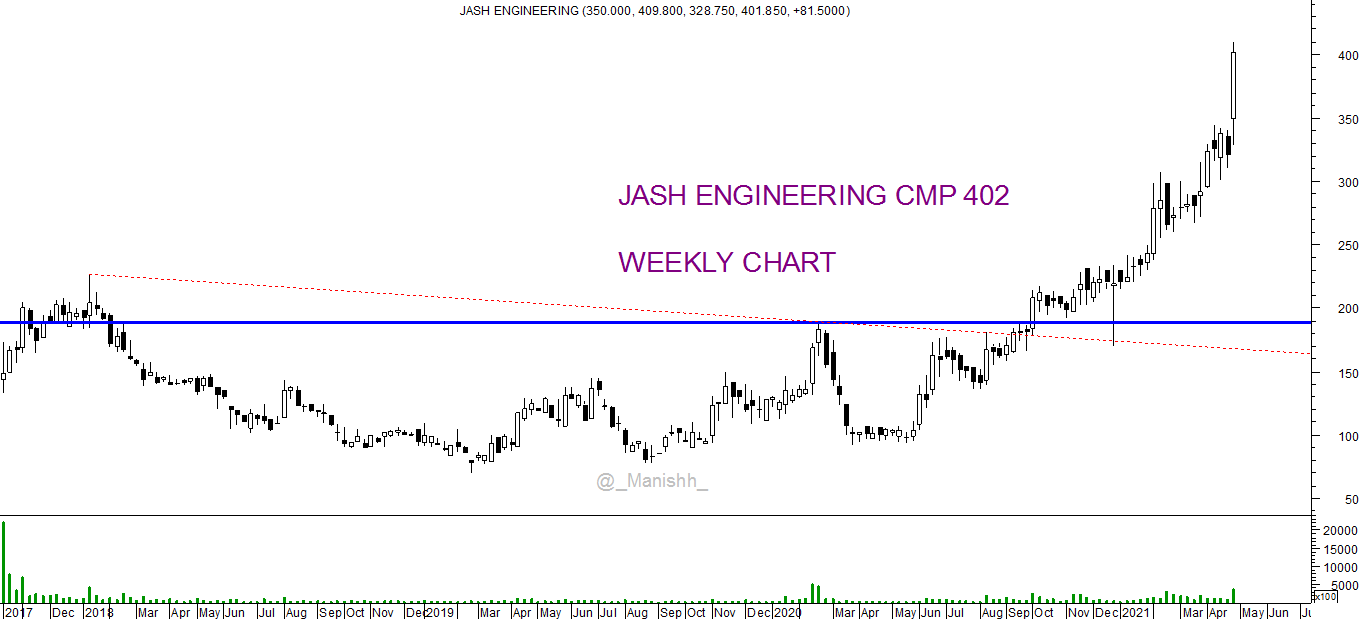

JASH ENG as i was expecting gave a good technical breakout

and Closing too on a Life High weekly basis after 3 Years

with good delivery based high volumes

any one have any update for the price volume action

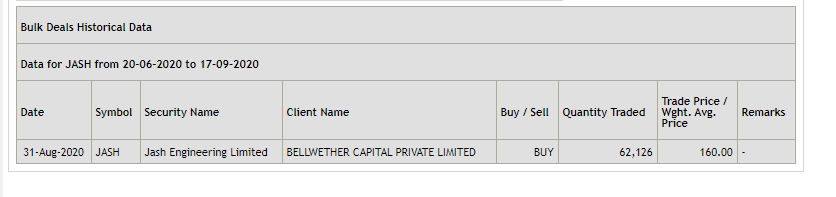

posting the follow up chart

Discloure : holding from lower levels and Added abv 190

Excellent results from Jash. Jash can be a big beneficiary of gov spending in water sector infra and domestic capex cycle revival.

disc. Invested

2 Likes

My worry here is a bit on order book growth . Last month was some 25-30 odd crs. A order run rate of 40 crs/ month would be crucial for next leg of growth for Jash

Did anyone attend the concall today?

Yes. Key points i can recollect.

- Focus on growing 15-20% CAGR.

- Current capacity (with minor capex) can do 500 odd crs of revenue. Post that new facility would be required. Company expects it will take 3-4 yrs to reach that number. Construction period of 9 odd months or any new greenfield facility.

- USA expected to go to USD 30 mn business in 3-4 years. This yr 13-14 mn . Target of 18 mn next year. USA the company is more famous on gates and not for screens.

- Profitability this quarter was high due to better export mix. Same should be true for Q4

- Introduced a new filter . Should be first one to mfg in India. Market potential could be high if pollution body orders are implemented.

- Mumbai bid - technical tenders have opened. Commercial in another few months. Expect significant revenue potential at decent margins from there.

5 Likes

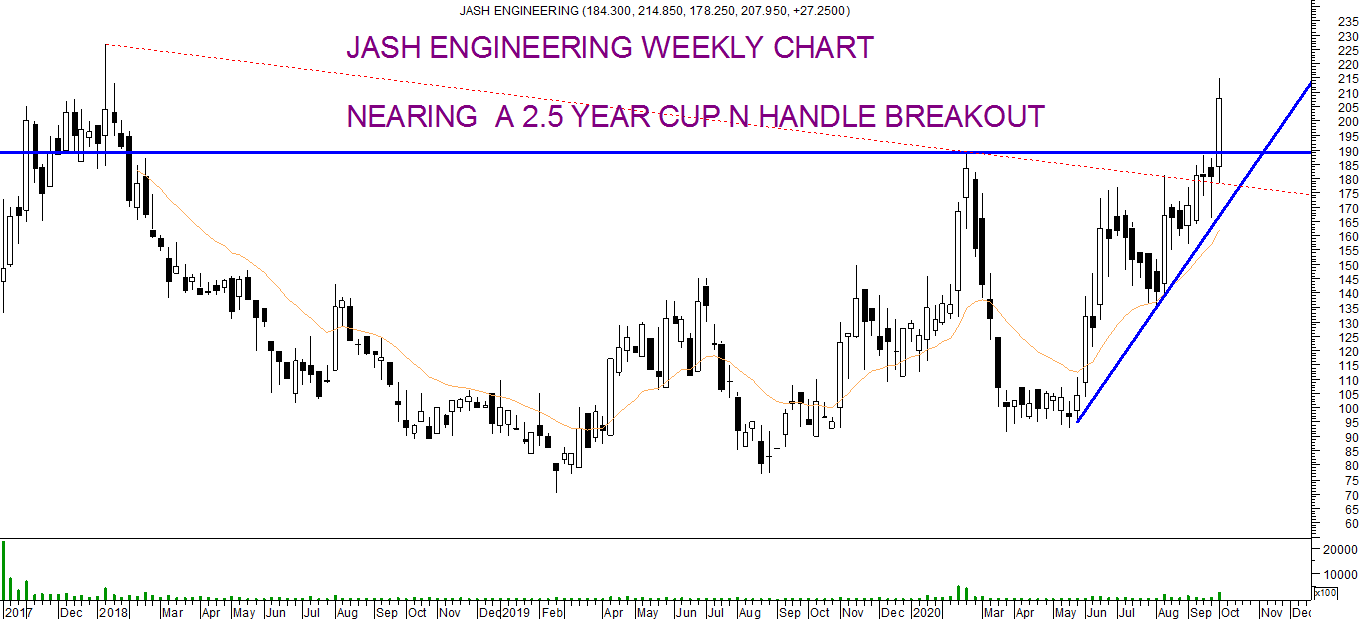

Jash Engineering finally outperforms

after a lot of patience , hope to see more returns here

any news today for the Spurt ?

Attaching a Updated Chart , Last posted at 190 levels

US operations (Rodney Hunt) did turn positive in FY21-22

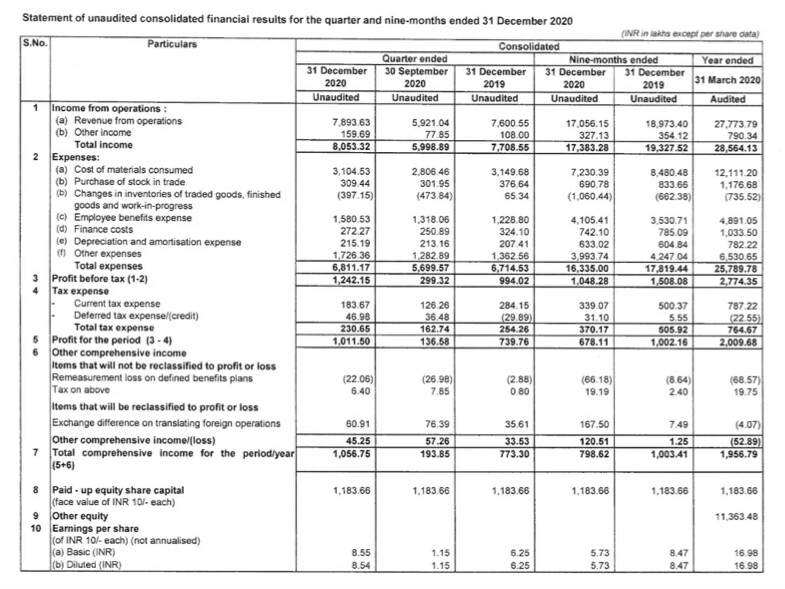

Very good Q4 and FY 21 results despite pandemic challenges.

4 Likes

Q4FY21 CONCALL

Please note I have compiled only the key Business updates that are of importance in monitoring the progress of the business. These are not comprehensive. They are heavily edited for ease of summarizing

Storm water cycle.(5-10% Revenues )Worldwide this is becoming a big business because of flooding. We expect huge orders to come through from Bombay Muncipal Corporation because Bombay is facing a lot of storm water issue nowadays.These projects of Mumbai city offer us a potential business opportunity of over ₹150 crores during 2022 / 2023 / 2024 .presently we are doing ₹1-2 crores of business a year. We see close to 40% growth in domestic demand just because of the Bombay

Renewable energy(5-10% Revenues) is not picking up because of Covid. Govt has no resources to spend on renewable energy. However we know that this market has huge potential and we are waiting for that potential.

Industrial usage(10-20%, of revenues) Capital investment as everyone knows, is subdued in India currently. However, when the capital cycle improves in India we expect huge growth even in industrial usage of all equipment

Water control gates are 54% of revenues, not very comfortable with water control gates

being such a big contributor. However, we are working on it, next year we are quite

hopeful that valve(currently 14%) would be much bigger than what it is today

In India most of the product our market share is already more than 50 %

New development launched Disc filter with Invent of Germany.This disc filter is now mandatory to be installed in most of the sewage treatment plants in India(new and old). We have got the order for the first two machines and we expect to be the first company in India to start this production indigenously. Over the period of time we are projecting Rs.25 crore minimum business.

Invent is world leader in aeration and mixing technology,We intend to join hand with Invent and produce these products in India and give stiff competition to companies like GE, Xylem, etc. who are world leader and presently they are leaders in India

Order book Rs.427 crore of which outside India is Rs.271 crores as against 156 crores from Inida…Far and Southeast Asia is now going to become a very big part of our business because we have more than Rs.150 Crores worth orders in that area now,

- We got our first order for 7 Screw pumps in Malaysia last year and we expect further orders from Malaysia more than 50 such pumps are in pipeline. These pumps cost anywhere between ₹60-70 lakhs to ₹1.5 crore .there is no other manufacturer in Asia,most of the manufacturer are in Europe and we have a very strong price competitive advantage against that.

- Our present position in Singapore is very strong. We have already secured orders for

products worth ₹100 crores in Tuas water reclamation project

Rodney Hunt achieved close to 14 million in sales which is a significant growth over the last year.have become EBIDTA positive in Rodney Hunt. minor loss this year of $5,000 . have order booking in excess of USD 18 million and expect to receive further orders worth over USD 2 million

can touch USD 20 million in sales in the year 2021-22 with a reasonable profit.

Once the company is profitable then it will open doors on projects which we cannot bid today due to limitation in bonding. This will allow us to scale up further and bring Rodney Hunt within top 2 players in Water control gates market in USA by 2024-25 with sales in excess of USD 28 million. In 2 years twe hope to re-achieve the number 1 position in US market

Guidance Due to covid giving a conservative figure of ₹340-360 crores in spite of having orders of ₹427 crores as on 1t June.Expect improvement in our EBITDA from 18 to 19-20%. Ultimately our aim is to give 23-24% in EBITDA in 3 to 4 years

CAPEX This year, we are doing ₹9 crore and ₹8 crore worth of expansion will do after

November. Can do ₹500 crore revenue in next 3 years.the next phase of expansion would be

investment in Chennai and investment in SEZ for additional land to make a new plant

in 2023-24.

My thoughts. Overall a class company.Rodney hunt USA has finally turned around and should contribute meaningfully from here on. Company may benefit from Biden’s infra push as well. Expect 15-20% revenue growth over the next few years with improving margins due to increasing share of exports and better product mix. For anything more than that India business has to really take off with govt getting serious about Water infra which is the need of the hour

Managment takes efforts to explain their business to investors.Have interacted with them a couple of times in the past. They are very shareholder friendly and thats a huge plus if you are investing in micro caps. They are clearly eyeing a higher Market cap(Mentioned Jash being a good investment opportunity a couple of times over the last 2 concalls) .RM increase is a risk as most contracts dont have an escalation clause

Would recommend new investors interested to start with the Investor Presentation. Its nicely done

Disc: Holding with no transactions in last 30 days

12 Likes

I request the forum members to share their thought on the following:

Most of the large scale industries look towards automation and SCADA systems to improve control. Considering the fact that JEL supplies products which are going to be used in large scale water treatment systems, has the management ever mentioned about the using electronic actuation as a mean of controlling the equipment? As far as I know most of the JEL’s products require manual control.

Disclosure: Tracking

1 Like

There is an investor / result concall today at 4 pm. You could join in and ask

Good question. Actuation whether it be electrical,pneumatic or hydraulic doesnt have to be done by Jash. These are things which can be done on-site. Jash just needs to facilitate that via some add-ons. The manufacturer of actuator can be someone else and installation yet again someone else . Now this is what normally happens with a lot of pump and valve installations so i assume its not very different for jash but i could be wrong. Either way its not something i am too curious to know as the answer wont change my investment thesis but its always good to learn something new ![]() .Installing actuators is not a big deal. You can ask the management. They are very shareholder friendly

.Installing actuators is not a big deal. You can ask the management. They are very shareholder friendly

Whats worth knowing is that they make custom products as per the clients needs. Thats why clients dont go to chinese because theres likely to be a lot of back n forth dialogue before finalizing the design

Thanks for your input.

If JEL has the ability to support automation for its products through customization, then they can further collaborate with someone as and when the need arises.

I will try emailing them to get some more information on that front.

1 Like

Things that stood out for me in Q1FY22 Concall

- On Weak quarter : poor offtake of finished goods due to second wave of Covid plus there was increase in payroll cost, freight cost and change in treatment of commission expenses in case of

Rodney Hunt. However Covid has not greatly affected the production output of the company - Healthy order book of 468 crores and strong order pipeline.Stick to earlier guidance of achieving 340-360 Cr Revenue this yr

- Finer details of Bidens Infra plan will be ready by the next year and by then Rodney hunt will be in the green and eligible to Bid. Company is making enhancements at Rodney hunt to cater to Make in America projects

- A lot of big water treatment projects are coming up in India. Expecting strong domestic demand

- Seeing plenty of opportunity for Disc filters in India now. Seeing a lot of bids

Disc: Invested

5 Likes

Hi all

Have just found this company when I applied a few filters on Screener. Have gone through the AR and Investor presentation along with the above thread.

Company seems to play in a good sunrise sector. Have made several smart acquisitions and international partnerships to grow. The management’s guidance of 500 Cr revenue seems achievable in the next 2-3 years. Margin profile also looks good. Rodney Hunt is a wild card, and can throw positive surprises.

One question - are there any listed competitors? Are Ion Exchange or VA Tech Wabag a competitor?

Disc - invested

1 Like

Rodney Hunt isn’t a wild card anymore. Overall growth and profitability of this subsidiary has been well established. The upside from the USA infra spend is an add on plus if it happens

Yes what I meant was that this profitability should now start showing results with US’s infra spend push. From the concall, Rodney Hunt has a good brand name in the US (Jash haven’t been able to penetrate via their own name).

VA tech is EPC while Jash is an OEM, so it is a supplier to VA Tech. Ion Exchange i m not sure but they are more like Wabag .

Disclaimer: Invested started accumulating very recently Jash : A Hidden Gem?

1 Like