I am introduced to this forum at the beginning of the year.

I had few shares though ESOP from my company in 1998. When I felt that the future of that company is not good, I moved them to TCS and Infosys circa 2006.I held without any transactions until beginning of 2016 where I felt, I need to redeploy them to stocks which can get better returns.

Then, I started redeploying slowly and during this period I was an uneducated investor for an year trying to figure out investment thesis from sites like moneycontrol news. End of 2016, I realised I did not reach anywhere and I sold when stocks appreciated 10-20% of buying price. Then the search led me to VP and value investing in Jan 2017.

Another 6 months (unil June 2017), without much understanding, I initiated certain positions, exited some as I did not had much conviction. Now from May-June 2017, I am trying to build a long term holding PF. Some of my old positions and some other positions I like to exit top bring it down to 15 from current 22. I am still building up my conviction on few and like to keep my PF at 15 shares at max in future.

As of now, in this raging bull market, I am at 4% loss mainly due to my top holding is at huge loss.

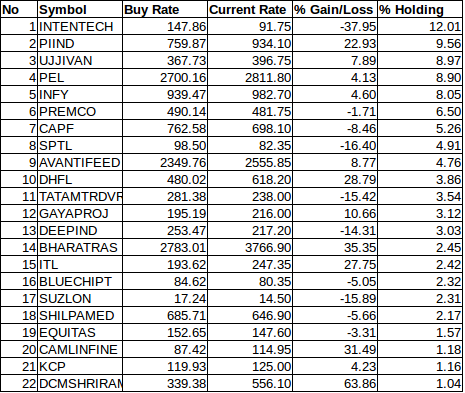

Most of the names except Tatamotor DVR are additions after Jan 2017.

I will add rationale for buying and holding in the next post. My target is good learning and 10-15% CAGR for first year and improve it over 2-3 years to 20-25% CAGR. However, I get less time to do my learning and still figuring out fundamental analysis and a big zero in technical analysis.

Please review my current PF and give me your valuable advice.

Especially I like to hear from seniors as well.

All of my holdings are covered in VP forums and I learned most from this forums.

Intense : I believe current story proposed by management and believe it is long term compounder. I believe in IT Products would be a good story for future and see good potential for Intense, So continue to hold at high loss. I started buying this at high price, before I learn much about valuations. Reviewing my thesis every quarter close to results.

PI Industries : Rural/Agri recovery and CSM long term order book and I believe long term story. Management and business quality. Conviction built mainly through this forum. Bought and averaged down.

Ujjivan : Banking/NBFC/MFI story. Good management quality though Mr. Ghosh. SFBs would do well and I believe Ujjivan can do well being good management.

PEL : Though had tracking position earlier, added more later. Ajay Piramal - Management quality and great capital allocator.

Infy - Will tender significant position to buy back. Remaining from buyback would be used like Parking of cash position. Large cap balancing as well.

Premco - Great textile story and I believe business have good days ahead. Quarter on Quarter I will watch the progress.

CAPF - NBFC Play. At current valuation, I felt CAPF can appreciate due to Management Quality. Still studying sector and building conviction.

Sintex Plastics : A friend referred. Still studying and building conviction. Low PE in sector as of today and I believe it will appreciate over 2-3 years horizon.

Avanti Feed - Long term story and conviction built after reading about it in VP forums.

DHFL - Housing theme and lower valuation comparing to peers. I believe company learned it lessons and story will improive only.

Tatamotors DVR - Found DVR is less pricey compared to Main one. almost 1.5 year holding now. May exit in future if things dont improve in 6 months to 9 months in terms revenue/profit. Banking on revival of prestigious Tata company under new chairman. Large cap balancing as well.

Gayatri projects : Infra and Road play. Seeing the story will improve from here.

Deep Industries : Entered considering High growth, trying to exit at no loss. ONGC issues affecting the company as it is the largest customer/

Bharat Rasayan : Agri/Rural Play. Looking to add when I get good entry price.

ITL Industries: Recent entry and expecting the story to improve.

Blue Chip Textiles : An entry based on magic formula being undervalued and profit/sales growth without much study. May exit any time if I cannot find any moats on long run.

Suzlon : Looking to Exit due to multiple headwinds. The story so far not played as expected. Under close watch and exit list

Shilpa - Pharma play. I expect the story to improve from here. I may exit as well as I struggle to understand pharma sector.

Equitas : Good management quality under P N Vasudevan and new SFB. Still learning if it has good execution capabilities

Camlin Fine : Chemical play and making use of low valuation and future prospects. Took part of my learning process to watch

KCP : cement/sugar play, still learning and bought 1% stake for my learning.

DCM Shriram : Conglomerate. Part of my learning process. Reduced in recent run up and may increase back if a correction comes.

Cash Positition : 9% apart from the listed holdings.

One question only. Why have you allocated so much capital in Intense Tech? Have you analysed their products / services personally? I dont track it but a glance at its financials do not inspire much confidence. Such a high bet seems irrational though sometimes it may generate alpha.

That’s a great question and thanks for asking. It is part of my learning curve and may be a lesson for others also who loves to average down if price goes down for a story which they believe. I started buying at wild valuations, averaged down when I thought price is forming double bottom around 165 range, then stabilised around 120 range and then around 85 range to keep average buying price low. That ensured my capital allocation gone to the winds. I learned my lessons and I plan to reduce exposure once price appreciate to my buying price to less than 10% allocation of PF, not definitely the highest holding from that point.

Having said that I added more intense as I believe it is a long term story and seeing it as a great product company. It’s marketing skills are the challenge especially to US market and head winds in India to one of the large customer ensured muted top line/bottom line and many suspected management claims to be hollow. I observed management commentaries closely from Q4-16-17 results and will continue to do for some more quarters (3-4 more) to see if the story playing out.

Hi i am not an expert but in market for 13-14 years and had seen over years that these tiny 1% 2% 3% allocations are useless. Even if your 1% 2% 3% stock goes up many times how much will you gain finally. If you are bullish in a stock you must allocated 7% to 10 and even more on it to make meaningful changes in your portfolio. Try to allocate more to the performing stocks and not to the under performing stocks. If you dont feel confident to allocate 7% to 10% capital to a stock its better to let it go.

Averaging is a very very tricky game and in this game more often you will get caught in the wrong foot. So best to avoid it as much as possible unless stocks falls due to some external environment condition and there is no change in the fundamentals in the company. . Remember Time is the friend of the wonderful company, the enemy of the mediocre —Warren Buffett.

While creating portfolio its better to avoid named which are lager multi-baggers in the past/near future. Ofcourse there are some solid evergreen names like Kotak bank, Hdfc bank, asian paints, nestle which i feel investors can buy any time any price if he/she has a holding time of more than 3 years. But not all are not absolute quality. You have to find the difference b/n cheese and chalk.

Regarding your portfolio my advise is to try to find absolute compounders which i feel is mostly missing in your portfolio. There are lot of 25%+ compounds available in the market which can compound you money for years. Out of 22 leaving 5-6, none are in that category. Muitibaggers are nothing but absolute compounders.

I may be totally wrong in my assessment about your portfolio. So please take a note on that also. Cheers

Thank you @catchsudipto. I agree to your views on 1-3% allocation. It is part of my confidence building measures as I am not comfortable to buy 7-10% upfront. So I average up/down as per conviction to increase my allocation over time. I found I was averaging down and up at wrong times and trying to get better at that game. But my temperament, will not allow myself directly to go to 7-10%, as I doubt my own abilities to some extent so far.

Now you say " my advise is to try to find absolute compounders which i feel is mostly missing in your portfolio.", Share your views on what are those at current scenario (even though I would need to wait for valuation to fall to comfortable levels), may be 5-6 names you think are sure shot long term compounders. That will enable me to study them more and keep a buy list ready by re-balancing the PF if a good correction comes.

To make real money in market you have to bet big.early you understand that its better for you.You just require 5-6 stocks to make big big money.

Not all your bets will become true multibagger i.e 10/20/30 bagger or more. Its very important to look at the past performance of a stock/ promoter integrity etc to bet big.

For me if I had to bet big on 20%+ compounders i can bet any amount in Hdfc bank, kotak bank sundaram finance etc.For 15 to 18 percent asian paints, nestle, godrej consumers, Britannia marico proctor Page ind etc

For 25+ PEL, PNB hfc, dmart and sankara( not in this valuation) Bajaj fin,Rbl bank and Gruh finance. I am confident of 25+ cagr in these for atleast 3 years. Note I hold all these 25+ in my portfolio along with page and nestle.

Avanti feeds a terrific multibagger i have no idea so no comments on it. CAPF is ok but i prefer bajaj fin as its sector leader. PNBHFC is better than DHFL. PI was a huze multibagger in the past and might have slowed down to a 18to 20% bracket. I hear lots of good things about Shilpa, but the sector is in bear market. Of late Bharat Rasayan and DCM Shriram are buzzing a lot. No idea on Bharat rasayan but DCM shriram is a leader in Fenesta windows. can be an interesting bet.

Ujjivan/Equitas is the play where you can make lots of money. But as Equitas is getting out of microfinance it might not grow fast. Market is betting on Ujjivan to show higher growth. Look out for Bhandhan bank IPO.

I normally aviod commodity/cyclical/high debt ridden companies. so no idea on the rest. cheers

Thank you for your views @catchsudipto. That helps. Most of them are in my watch list and I did not enter as I found them at high valuations without much margin of safety when I saw them.

PNBHFC is better than DHFL, but at much higher P/B. So I banked on DHFL valuation to catch up with rest. Bharat Rasayan and DCM Shriram - Both I plan to increase allocation if opportunity comes. Some profit booking and desire to re-enter reduced my holding on both (though both were never even 5% ever. PEL is already in PF. Many in 20+ com pounders are already at high valuations. I may exit few others and enter in some of them if a big correction comes at some time.

Valuation is an illusion. Nobody knows what is the perfect valuation. Everybody wants to guess but the smarter guys who tries a informed guess/decision does the best.

Anyway its you decision what to buy /sell i will not recommend any, but some important advise.

Always run behind quality as its the quality which will separate the man from boys.Never compromise on quality. Always buy quality even if its seems overvalued but a long runway in front and growing @20+ carg. Sector leader will always do better and fall less in a bear market than laggards. Cheers.

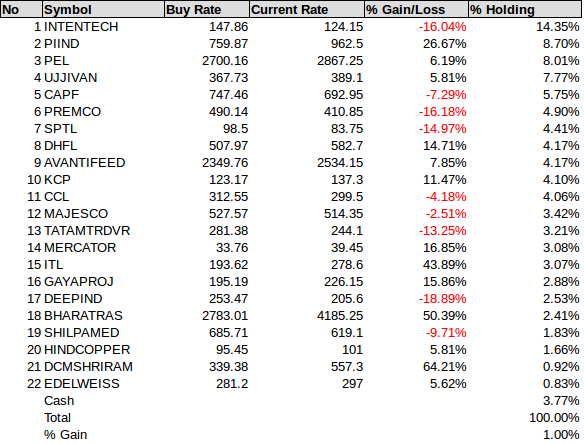

Thank you @1.5cr for reviewing and offering your suggestions. I already increased KCP to 3% of PF and increased DHFL by another 0.75% using recent fall below 600. I will see if I can increase allocation further. I am slow to to take significant position and I know that is a weakness in me as most ideas starts as satellite ideas and allocation moves up over the time and as and when I close another position. I am not further allocating further funds for equities as I am on transition between job/business, so that route not possible.

Thank you for frank views. Micro finance and SFB’s are a story I believe. I believe they would be leading next phase of growth in financial world as opposed to traditional banks and in comparison with some NBFCs. I had Satin also which I recently exited. Equitas also I may exit, but I am bullish on Ujjivan. As of today, Infosys is more of buy back play and will exit from it after buy back completion. Post buy back, I exited TCS earlier.

Tata Motors was an older bet before I started learning process of value investing and I may need to book losses sooner or later. I think as of now, I will watch the story for 1 or 2 more quarters.

I agree with Suzlon as well. Looking for an opportune moment to exit.

I beg to differ here.

Even on stocks on my exit list, if they are temporary downtrend, I would wait for the trend to reverse to exit to reduce the loss of capital as much as possible. Most of these positions are only few months, so I can afford to wait few months if I feel some temporary negative news keeping the stock price low and can reverse to a minor loss/minor profit to exit.

Let me try to explain quoting some one else, Hitesh as per today’s news report. “Once a company passes my fundamental filters, I look at the charts and apply my basic knowledge of technical analysis to discover good entry points”. I try in similar way to get a good exit point and if I am unable to get it in a specified time (for me a quarter), I exit then without bothering about my losses. What I dont follow in Hitesh is this “One dictum I follow strictly is to get rid of losers as early as possible, irrespective of the percentage loss. That helps restrict losses and maintain focus” which you also advocated.

Why I do that ?

Loss of capital is something we need to be careful when we try to minimise opportunity costs. So like we may wait for entry points, I believe we can wait for exit points too for a reasonable time period. I consider it as different from timing the market. I find it very difficult to wait for an entry point, but easy to wait for an exit point. I am trying to improve on my entry point as well.

The exit planned as story is not playing out as expected, not after a quarter results. But probably days after, thinking again through my rationale. So the chance of further down immediately is not very probable and I look for an exit point in usual ranges which was there in a month or two. Usual market volatility brings stock there very often. If it does not happen in stipulated period, then I exit without further wait.

@sta I think you misunderstood. Let me try to explain in detail both my exit decision making and actual process of exit.

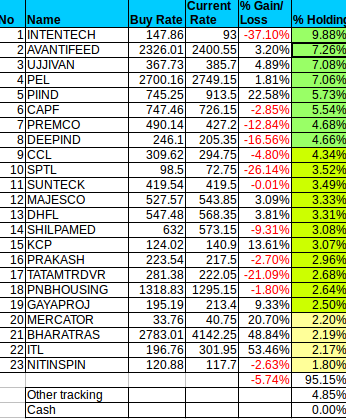

Exit decision making: The time frame decision to exit varies based on in-depth study when a I entered in some scripts without full study or based on changes in business varies from case to case from few weeks to many months. I am improving on my entry decisions. At a point, I had 50 tracking stocks in PF (as recent as July 2017) and I exited most of them one by one.

Exit Process once decision done: After deciding if I need to exit (by evaluating if the thesis working or not) for a reasonable period, I take maximum a quarter to exit. During this period, I see anything contrary to my older view crops up and I reserve the right to change the decision

For eg: In my current exit list Deep Industries remains. I am waiting to clear temporary negatives due to ONGC order cancellation or waiting to see if any positive triggers forming.

Sintex Plastics is on possible exit list and in further study mode as so far it did not play out as I was expecting. I was on evaluation mode on Tata motors DVR as well and now I decided to continue holding as I can see business is turning around, though slower than I expected.

PF as of yesterday. I could see I turn to green at the end of the month, only to go red as most PFs with small cap and Mid cap heavy done. During this period

I added more to high conviction ones.

Newly entered: PNB Housing, Nitin Spin, Prakash Industries, sunteck realities. Exited very small position I had in DCM shriram. Booked profit on certain scripts which had more than 25% profit by selling 20% of holding across the board when I could get my target price to have cash toadd on high conviction ones. Tracking Positions (4.85% of total PF) in HAVELLS , EDELWEISS, HINDCOPPER, Pritika Auto, SYMPHONY, SHEMAROO

Last 9 months lot of churning happened in some of the scripts.

Exited some of them where I could not keep conviction. Like, Deep Industries, Sintex Plastics, SunTeck, Dewan Housing, Shilpa, KVP, Prakash, Tata Motor DVR, PNB Housing, Gayatri Projects, Mercator and ITL.

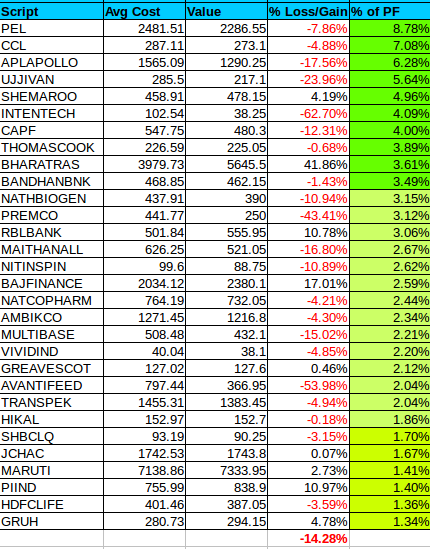

I increased allocation on certain names averaging down/up as the case may be like PEL, CCL, Shemaroo etc.

Reduced allocation to some like CAPF, Intense Tech by booking some loss,

Increased overall allocation by 50%.

Cash ~5% of PF.

I find it easy to average down and it is very dangerous. So trying to improve on that front.

If you are 100% equity guy, you badly need large caps. If it is small portion of your networth, then anything less than 5% allocation is waste of effort as it will NOT change your financial standing either way.

Intentech, premco and avanti are big drag having significant drawdown. However you seem to be OK to hold. I think you could have possibly used trailing stop loss with 20-30% below latest peak to minimise these DD. Money saved is money earned…