@amishra, Yes, in the hind sight, I agree and in future, I plan to have a trailing stop loss of 25-30% for the entries where loss is not yet there. However Intense, Premco, Avanti, Ujjivan - I plan to hold as of now.

I understand as that I have the following P&L weightage by thew following which drags the PF.

|Intense|-31.93%|

|Premco|-11.12%|

|Avanti|-11.14%|

|Ujjivan|-8.26%|

I agree to this @nav_1996 . But for me one learning is that, conviction building should be a slow process and I increase/reduce allocation over the time. I usually cannot gain conviction to add a 5% position. I tried to add minimum of 3% for any new entry and I figured out that is not easy for me either. Hence I have a trailing list where 50-60% of PF is in 10 names, then a reducing tail where I increase/reduce based on conviction getting building up.

Just an alternative, not deeply thought though. Take it with a pinch of namak.

See you have close to 30 stocks. Make a conviction ranking. Sell the bottom 15 and load on top 15. You will get a solid 15 stock portfolio. Apply TSL on that.

Thank you @harsh.beria93. As of now I am out of almost all the names here and moved to 50% of cash when covid related crash started. Out of remaining 50%, almost 40% I am following the recommendations of an advisory and invested, so cannot reveal here. So I am invested for roughly 10% on my own as I dont get much time to research any story and I need to sharpen my stock-picking skills. Some I still hold on loss are VividInd (50% booked loss), Shivalik Bimetal etc among those 10%. Since my PF itself was small, current investment by my own plans are very less.

After a while, I thought let me update some of the holdings I have now.

Almost half of my holdings (~50%) is held through the advisory and I do not plan to disclose/discuss it here,

Inviting views.

Some of these medium/opportunistic I do a lot of churns based on technical views.

Note: I am novice in both technical and fundamental analysis. I buy with very less study and I can be wrong and this is for learning purposes and I learn through my mistakes and wins too.

Trimmed some of scripts in profit and generated some cash to increase Infy to 2% and bought a microcap anuhpharma (1.5%) at 98.5 when a friend suggested it. Market cap now is 560 crore. As per screener it is an under valued bet as valuation still not caught up with sales/profit growth of many years.

Sold off Credit Access Gramin and increased Infy, and some others in buying range. Fully invested.

On hindsight, this was one grwt suggestion…I couldn’t act upon. All my ideas were multibaggers for me and high conviction. Only problem that market had a different ideas and some were multi beggars… learning curve is good. When I started this thread of my PF was X, it is now about 2.5 X which includes some fresh money. But I benefitted through this six years of journey and all the learning from valuepickr and screener

Few Churns in a month and some profit booking and changing some of the horses.

Exited Infosys, Credit access Gramin, Engineers India, HBL Power and sharda cropchem completely, Booked partial profit on some to generate cash.

Booked profit and exited Agarwal industrial corp, Dynamic Systems and booked losses on Amararaja batteries and exited with no loss no profit HG infra

Invested in Dr Reddy’s for about 3% of PF. Added Dhanalakshmi bank, UCO Bank and Bank of Maharashtra as a basket of small banks. These would trading bets for 15-20 % gain as I don’t understand banking too well and don’t have a long term view other than that banks are turning around. Took a small trading learning position 0.5% on Fredun Pharma as I feel down side limited technically.

Started accumulating TCS hoping to keep it long term.

High churn hoping to convert some notional gains to real gain and reinvest.

The reason for recent entry to Amara raja was technical as it crossed previous high of ~ 660 and it went below that level and most recent top of 650 and hit my stop loss which was set at 10%, hence exited.

Past experiences made me to adhere to technical stop losses even if the stock is fundamentally strong as I may not know all of the reasons stock going up and down, being an individual and small share holder.

Stock is undervalued on PE Basis and trading close to 10 year low and not caught up with median PE, so invested for reversion to mean A decent Pharma company and I believe in the current bull run the valuation will catch up. Also I expect the decent profit growth to continue.

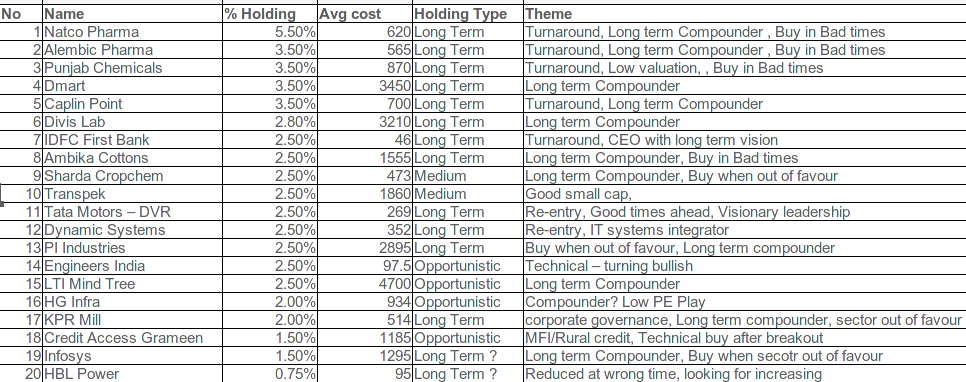

There has been multiple churns here. I use my personal PF as high churn and regular profit booking. Caplin Point is untouched. Pi Industries bought more, some Natco Pharma bought after trading earlier IDFC Bank changed to IDFC for the full investment, bought back some Dynacon Systems. The PF looks as below. Suggestions are welcome

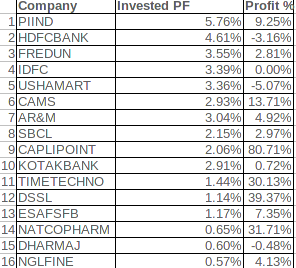

I think ESAFSFB profit percentage is incorrect. Anyway are you betting on the NPA to come down in coming quarters?

One thing I noticed, the GNPA and NNPA numbers for Q3FY24 was already out by 4th January on the quarterly business update document published by the company(below). So this should have been priced in from then. But then you see the gruesome fall after results and everyone blaming it on the NPA’s, because the rest of the Q3 result is looking good.

Thank you Harsh for the comment. I sold around 70% profit before the recent upmove when it was touching near 50 DMA. It was a bad decision in hindsight.

Yes, you are right. It is -7.x%

I am keeping tracking position as I think management is good and to keep close watch.

As per con call, NPA situation can persist atleast for 2 quarters …Hope it will not go worse and they would be able to continue to grow