I don’t know about Jagran, but on the MBL (subsidiary of Jagran. Owner of Radio City) conference call Apurva Purohit (President. Jagran Group) mentioned that they have been seeing weakness in the economy since October-November 2019. Plus advertisers started cancelling confirmed ad spends since the 2nd week of March. So I think it is a combination of both factors.

1 Like

Hello Sarvesh,

Would love to know your views on the future of jagran prakashan. Have heard and followed you asking incisive questions at their concalls.

Thanks

1 Like

I have started a thread on MBL (74% subsidiary of Jagran). Here is the link:

Hi @sarthakkumar19_ Jagran is currently trading at cheap valuations (P/E of ~3x normalized profits against historic average of low double digit P/E). However all media stocks will show performance but with a lag as they are the first derivative of growth numbers in GDP which are currently undergoing a downward revision. So business will take some time to recover and so will be the valuations as its a small cap and belongs to a sector which is not a fancy of the current set of investors. Also, company is strong enough from a balance sheet perspective to survive this crisis.

How fast the recovery will happen is anybody’s assumption and will depend on overall speed of Indian economic recovery. But if I have to hazard a guess I think if one can hold this for the next 18-24 months, one can get 2x to 4x returns.

5 Likes

Will this crises lead to permanent erosion in readership, advertisement channel preference by the advertisers?

Monetization in digital space does not look that great either!

But this cirsis also has led to reverse migration to majorly UP and a good chunk of these folks may not return back to metros because of the efforts UP govt is making in terms of relaxing labour laws and such. In that case, if UP economy grows at a faster clip driven by rural demand, I see some prospects in the next 2-3 years for the company. Also, 2022 is the state election year before which we could see some ramping up of govt ad spends. All in all, next couple of years look interesting for JPL.

Disclosure: Studying the stock and no holdings currently

3 Likes

I considered both - Jagran Prakashan and its subsidiary MBIL for investment. Happy to hear contradictory viewpoints : -

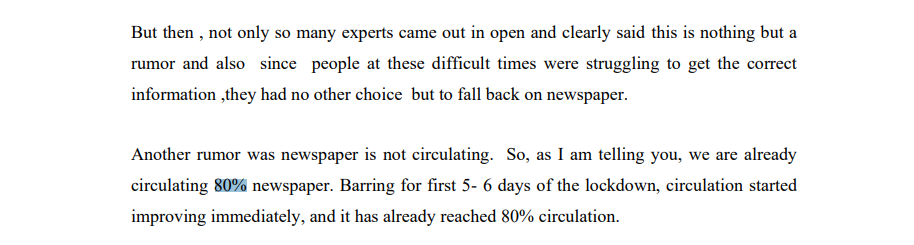

Jagran Prakashan :- This is a real Cigar-Butt valuation-wise. Taking a holding co. discount of 30-60% the co. is trading at 1.2 - 1.5 times trailing EV\EBITDA. While the co. will take some hit on topline this yr, the margins might be maintained owing to falling newsprint costs, Collaborative cost cutting by industry and circulation restored to 80% pre-covid levels.

Music Broadcast :- This is not an absolute cheap stock but a Fair business available at a cheap price. The company’s strong liquidity position will get it thru this phase where the topline hit might be 20-25%. Thus, here one is paying for a decent recovery and strong comeback of the business.

Which side to play is anybody’s call…

Disc. Not invested in Jagran. Exited MBIL in the recent run-up.

2 Likes

Can you share the reasoning behind this assumption. Incase it is through some source, would appreciate sharing the same.

1 Like

Check DB corp thread. Company Director mentions in a recent interviw that circulation is back to 80% in most places other than tier-1 cities. With railway stations, bus depots etc. closed, it is not possible to achieve pre-covid levels for the next few months. However, he also hints that ad revenues have dropped considerably. I feel the impact should be similar for Jagran too in circulation.

4 Likes

Can someone shed more light on Promoter’s Pledged Shares. What Project have they pledged them for?

Today’s exchange filing should clear the air around pledging

1 Like

The company has successfully raised debentures at around 8.35/8.45 percent for 250 crores. No shares of company are pledged, it is a non-disposal undertaking meaning that promoters cannot sell their stake below 60 percent till the redemption of debentures. The company has no major governance issues and are very investor friendly as they have redistributed a lot of money back to the shareholders over the last 3-4 years by dividends and buybacks. The companies circulation revenue is around 80 percent as on June quarter and i expect to get back to pace by end of year. The advertisement revenue will take time to recover but taking precedence of 2008 crisis, advertisement revenue took around 12-18 months to return to normalcy. Assuming the same the company trades at around 4-5x of normalized profits and a 10 percent yield. The company also holds a big share in Radio City which is also currently struggling but is one of the best run radio stations in the country. The current market cap of 1100 crores is highly undervalued but traditional newsprint despite a slow growing business is not going anywhere anytime soon. Solid contra, dividend yield bet in my opinion.

Disclosure - Invested

7 Likes

Can you tell me that from where you got this information because i am unable to verify it anywhere.

"The company has successfully raised debentures at around 8.35/8.45 percent for 100 crores. No shares of company are pledged, it is a non-disposal undertaking meaning that promoters cannot sell their stake below 60 percent till the redemption of debentures. "

2 Likes

You can find the link here

https://www.bseindia.com/xml-data/corpfiling/AttachHis/c099821c-a233-4568-b262-fd0996a76ac1.pdf

2 Likes

another of my safe bets reason for picking up this stock

1)P/E of 7 and average of P/E of past 4 years is around 4 .

2)dividend yield of around 8%

3)P/B ratio of close to 0.6

4)promoter bought own shares at 50 and 60 levels even higher

this stock for me is a no brainer gives more return than a FD ,divdend announcent of previous level or increase in ad revenue from election is going to make the stock trade at conservative 6 % div yield form current 8% even if it doesn’t i am happy keeping this stock with mouth watering dividends .

will add on drops

Disclosure:invested

A news published at a Respectable website:

2 Likes

Jagran returned ~1k crore to shareholders in last 3 yrs through buybacks and dividends.

Today the market cap of Jagran is 1.1k crores

This is a 50 year old company and the leader in its segment. Newspaper reading habit cannot die a sudden death. It will be a prolonged decline by which time, it can grow its digital business. The promoters are good and realize this.

Discl: Adding this stock regularly at dips.

Not sure what mr. market is thinking. Is it taking such a short term view?

Even pvr, inox are doing so much better compared to this when it is not so clear abt their reopening status …

1 Like

BREAKING NEWS september 8, 2020 (3.29pm)

BIG positive for JAGRAN PRAKASHAN

LOCKDOWN in UTTAR PRADESH LIFTED

Yogi Adiyanath-headed Uttar Pradesh government on Tuesday

announced that the ongoing Sunday lockdown in the state has been lifted

The latest decision comes after the state administration on September 1 had decided to lift the weekend lockdown in the state on Saturdays.

A CLASS POST BY vigneshb

pls see post 124-125