The stock has fallen quite a lot in recent times… breaching 52 week lows. Changes in fundamentals,? print marterial price? or some other issue?

2 Likes

Rise in newsprint prices and rupee depreciation would have hit the company. Yogi government after coming to power put a clampdown on ‘wasteful expenditure’, which included cuts to government ad spend. Sectors such as real estate and education which were big advertisers earlier were hit by demo. Competitive intensity has also probably increased though circulation is stable. While fundamentals have taken a hit, sentiment has been hit much more. Add to that general bearishness around all midcaps.

5 Likes

anybody having idea what is happening…why so much fall, even assuming no growth now the dividend yield looks good plus newsprint prices will save another 50-60 cr this year…

~~ is there any doubt over the PL / BS numbers

I don’t think there is any governance issue. Company is hit by general economic slowdown, cost cutting (on ads) by government, buyback tax, poor sentiment for midcaps and so on. Government has slapped customs duty on newsprint import. If Q1 was bad, management says July has been worse than June. On top of that, the stock has large institutional holding and liquidity is low. If one large institution decides to exit, the impact on price is high. Benefit of lower newsprint prices will flow in only next year.

4 Likes

The overall market condition has deteriorated since I last posted on this thread. Central government spending which accounts for approx 40% of Jagran’s revenue (I think) has not revived. Private sector spending has also not sky rocketed. The management does say that the decline in government spending is because of the newly elected government and the high spending baseline around this time last year - I dispute this, because the commentary on government spending was sombre last year around this time as well.

However, the stock price has also depreciated precipitously, so now is a good time to do a back of the envelope valuation calculation.

Key Facts

- Current market cap - 1700 Crores (approx) - 25/11/2019

- Cash and highly liquit investments - 600 Crores (approx) - 30 Sep 2019

- Debt - 195 Crores in debt, 65 crores in lease liabilities (approx). - 30 Sep 2019

Key assumptions

- Net income - I am going to use the 6 month ended period to extrapolate for the whole year of 2019 with data coming from Sep 2019 financial statements. There was a massive adjustment on deferred tax liabilities to the favour of the company in Q2 FY20, I will eliminate this impact by calculating net income as NI = PBT*0.75

- Depreciation was 127 crores in FY19, it is about 71 crores for 6 months ended Sep 2019 in FY20. I will assume it will be about 130 crores in FY20.

- Net Interest expense - Investment income of about 40 crores and finance cost of about 25 crores in 2019 were recorded. Finance cost in 6M ended in FY20 is already 17 crores. I will assume that FY20 finance cost will be about 30 crores, a net interest income of +10 crores needs to be recorded.

- Capex of 24 crores has been recorded so far this year, giving a run rate of about 50 crores for the year. The equivalent figure for last year was 140 crores, while it was 50 crores in FY18. I will assume that it is about 50 crores for this year.

- Working capital investments for this year is negative, however they were about 100 crores in additional inventory last year and 100 crores the year before for increase in AR. I do not expect any of this to happen this year, nor do I expect the current negative WC cycle to persist. Inventory already is at a rather high level + newsprint prices are going down, AR is at about the level this business has always had (about quarter of sales). I will assume that WC investments will be about 50 crores per year going forward.

This is approximately equal to

Free cashflow to firm = Net income + Non cash charges - Net Interest income (1 - tax rate) - Capex - WC Investments

FCFF = 320*(0.75) + 130-10*(0.75)-50-50 = 263.5 or approx. 265 crores.

Assuming 0% growth in FCFF to perpetuity, and a required rate of return of 15%

Intrinsic value of the operating business = 265/0.15 = 1766 crores

Now that is just the value of the operating business without taking into account the 600 crores of cash the business has on its books.

Total value of equity = Intrinsic value of the operating business - MV of debt + book value of cash/liquid investments = 1766-260+600 = 2106 crores.

In essence, the market has added a negative growth premium to the business.

After taking the cash and cash equiv. into account AND assuming enterprise value fairly reflects the intrinsic value of the business,

Enterprise Value = FCFF/(Required return on equity- income growth rate)

1700 Crores MV - 600 crores of cash and cash equiv + 260 crores of debt = 265 Crores of FCFF/(15%-growth premium)

Growth premium = (-4.5%)

It comes to individual beliefs at this point - If one believes that this business is not going to degrow 4.5% year on year from this point on, there is significant valuation cushion at this price point. However, on the contrary this business could well be argued to be fairly valued at this price.

The final dimension is that of dividend yield - The current dividend yield is 7%+ and that is considering a retention ratio of 60%-70% of net income. If this were to go down to only 50%, dividend yield would go up to close to 10% - I’d expect that to happen should growth opportunities for this business completely vanish as the market expects it to now. There is comfort here too.

But all of this is forward looking given where we are. The reason why the investment thesis on this stock has perhaps not worked out so far are two pronged according to me

-

None of the growth triggers including radio have worked out. This is a consequence of the industry/market situation since all players are suffering similar issues.

-

The current equity market LOVES growth and does not hesitate to pay significantly for growth. The concepts of value investing taught by Ben Graham are perhaps ill suited for this euphoria seen all around.

P.S : I hold stocks in Jagran Prakashan and my view may be biased. I am not a registered investment advisor and this is not an investment recommendation. Please carry out your own due diligence.

20 Likes

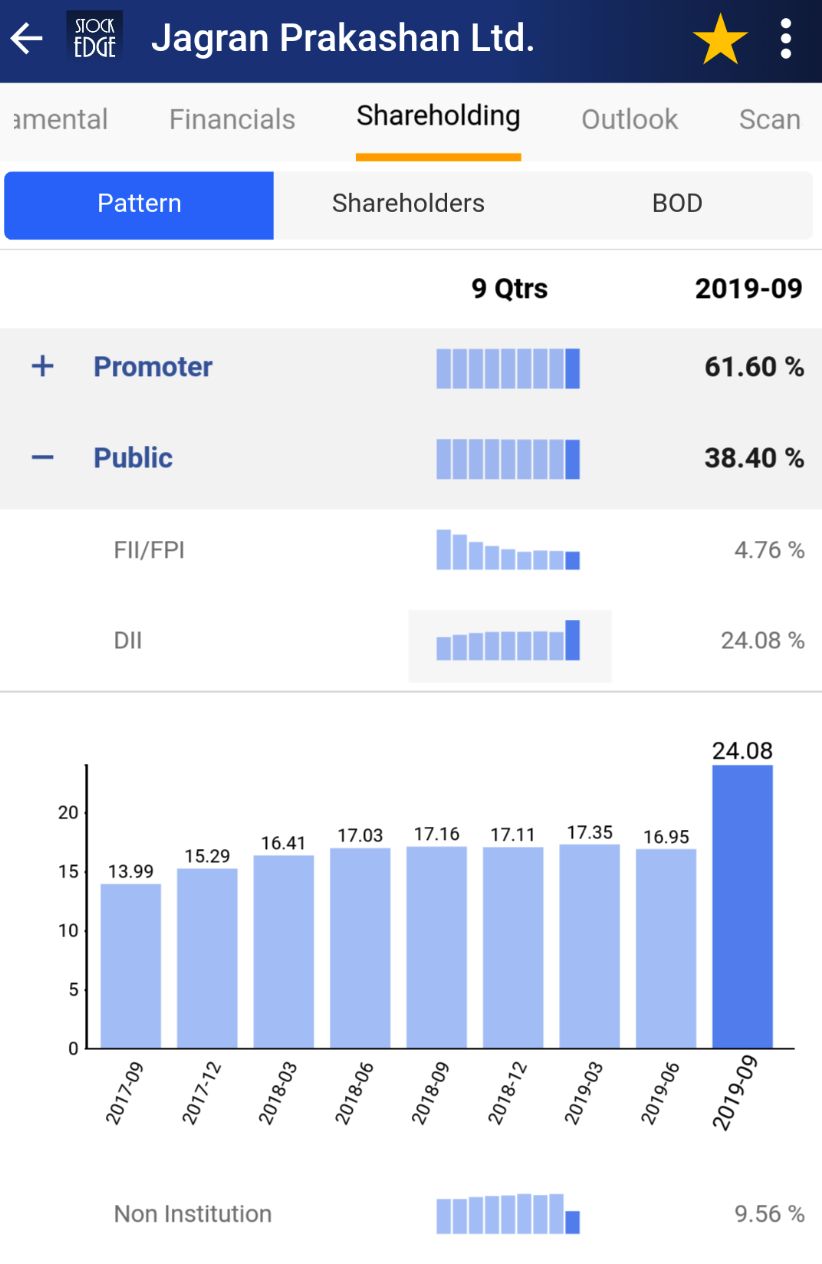

Could it be that institutions are unwinding of position in old media businesses ?

its actually otherwise… retail has been selling continuously and DII have been buying, almost 8% has been bought by DII in last quarter itself…!

as usual retail might have sold in panic.

Disc: Invested

2 Likes

That seems to be the case for this quarter, but FIIs have sold off heavily over the last 1.5 years. Maybe it’s hit a bottom.

Data from BSE does not support it, between June and Sep retail shareholding has increased, while ICICI Pru has done the major offloading.

June 2019

Sep 2019

Jagran Prakashan to consider buying back shares on 9th December

1 Like

That’s a detailed evaluation and kudos to you. I have gone through last concall posted on their website. What I could understand was that their major avenues from government tender notifications which has been stopped and few government companies started reviving.

Now days, most of the government tender notifications and bidding is on line. Probably , I agree with you that market is assigning a negative growth premium. I could not see any pockets of growth for at least 2 years. Really wondering why the company is indulging in buyback

1 Like

What a turnaround in this co did 400cr buybacks in dec and now raising debentures and entire promoter holding is pledged . It is sign of huge distress at the promoter level. Keep track specially of small mid caps as bombs and missile are coming from everywhere in this market. Promoters in good time could create a good positive story about them by there actions to please shareholders but in crisis real things comes out.

Disclosure: Tracking since last year no holdings.

1 Like

its a non disposal undertaking, not a pledge. It just means as long as company loan is not paid promoter will keep on running the company. Secondly it had debentures last year also. they get very competitive rates. makes a lot of sense to keep some money handy just in case things become very bad. Every company (large or small) is exercising bank lines etc so that they are prepared for worst and at that time they have cash hand.

2 Likes

Sir, please don’t create posts without full knowledge and fact checking. It is an NDU not a pledge, buyback decision of 100 cr from open market was taken (not 400 cr) in a pre-coronavirus scenario as the company’s shares were cheap even at 66-67 Rs odd price (44 rs now) as per the management. In a coronavirus scenario, it is good thing to shore up liquidity as liquidity ought to be raised when it is available and not when you want it, thats how conservative managements behave.

Jagran is a net cash company and business comes under essential services so will continue. Profitability will be hit this year for decrease in ad revenues but that will be one-off.

5 Likes

First of all thanks for pointing out my mistake that it is NDU not an pledge, second as per new sebi circular Non-Disposal Undertakings

(or agreements) (“NDUs”) are signed usually by the debtor in favour of the

lender in relation to any loan obligation undertaken by the debtor. An NDU helps

in ensuring that the debtor does not transfer the shares held by it in a

company by way of outside arrangements such that the creditor is left without

access to significant assets of the debtor. Usually, the usage of an NDU is

prevalent in the stock market as shareholders, predominantly promoters, tend to

undertake a loan against their shares in the company and with an understanding with

the creditor that they will not alienate or create any other form of

encumbrance upon the shares, therefore, creating a negative lien upon them. Typically,

the shares are transferred to a new escrow demat account for the purposes of

this arrangement, but the beneficial ownership over the shares does not change (remaining

with the debtor) and the creditor is also not able to dispose them off to clear

off the dues (unlike a pledgee).

In the banking

sector, such NDUs are coupled with a power of attorney (“PoA”) thereby

appointing a security trustee. The combination of the NDU along with a PoA

ensures that there is a positive as well as a negative covenant in the

arrangement such that if the debtor (being the shareholder) fails to keep up

with its dues against the creditor, the security trustee can exercise his

powers under the PoA to alienate the shares in favour of the creditor (or any

other person). The alienation of the shares by the debtor is safeguarded by the

presence of the PoA and the escrow account under which such shares are held.

Such an arrangement has been intentionally designed to avoid the framework of a

pledge to ensure that banks do not hold more than 30% of the shareholding of

the total paid-up share capital in the company as mandated under section 19(2)

of the Banking Regulation Act, 1949.

The complex legal arrangement has been formulated to avoid the compliance

required under section 19(1) of the Banking Regulation Act as the holding of

shares in an arrangement of pledge has a possibility of the bank becoming a

shareholder (in case of non-payment of dues) resulting in the company whose

shares are so pledged/encumbered to become its subsidiary.

Irrespective of the

structure of an NDU, there is no doubt that it creates an limitation of some

sort upon the shares of the promoters (especially when it is coupled with a

PoA) and it is vital that such information is disseminated adequately in the

public sphere. Previously, the Securities Board of India (“SEBI”) had amended

its formats under the SEBI (Substantial

Acquisition of Shares and Takeovers) Regulations, 2011 (“Takeover Regulations”)

to ensure that appropriate disclosures are made with respect to NDUs within the

scope of “encumbrances” to help investors in taking an informed decision.

A non-disposal undertaking (NDU Agreement) is an agreement to not dispose off shareholding held by the person holding the shares (“NDU Provider/Obliger”) in a company, usually a Special Purpose Vehicle (“SPV”). This agreement is usually coupled with a power of attorney appointed on the security trustee. It is a combination of contractual negative and affirmative covenant wherein the Obligers agree not to sell the securities unless the sale is required to discharge dues to the lenders. This Agreement involves a deposit of shares in a new Demat account which is then linked to an Escrow Account. The power to sell is given to a Security Trustee who may exercise the Power of Attorney appointed on it along with this Agreement and appropriate the resultant proceeds towards payment of their dues. The PoA and the escrow account safeguard the lenders against any attempts by the Obliger to breach its promise. Furthermore, this is not like a pledge where a beneficial interest or right of the Lender is created in the subject matter. The need to set up this complex legal framework is to take more than 30% of shares in a company as collateral and yet not attract S. 19(2) of the Banking Regulation Act, 1949 (“BR Act, 1949”) which mandates that a bank cannot hold more than 30% of shareholding of the total paid-up capital in a company unless it conforms to S.19(1) which is banking business and any activity in promotion thereof.

So my conclusion is it is still risky though now I know thanks to you that its not as risky as pledge.

what’s really important is to get information why such NDU was created and then take a decision

- As promoters want to have liquidity for any acquisition opportunity or any other need that may arise in covid 19

2.Promoters need money as they are short on funds for investments/debts made in personal capacity

2 Likes

Its listed subsidiary - Music Broadcast(Radio City), seems to be a bargain bet right now. I wd have started a new thread for it, but the statistical cheapness begets taking a deep dive. It can be more of a typical value investment as a part of a diversified portfolio. The stock is available at an EV of 2.67 times last yr’s operating earnings.

1 Like

Interesting find. The recent credit rating report by CRISIL says this:

While the base case assumes a decline in revenue by 22-25% in fiscal 2021, in line with the industry standard, MBL’s credit risk profile remains supported by its strong market position, healthy liquidity of over Rs 215 crore as on March 31, 2020, nil debt, and high financial flexibility. Furthermore, expectation of waiving off of license fees for radio players could support their operating profit and, hence, remains a key monitorable.

Zero debt, good liquidity, low P/E (8) and P/B (0.7). It deserves a deeper look.

Would be great if you could start a new thread.

1 Like

Thanks.

As mentioned, I may not be the correct person to start new thread on this. For my personal portfolio, I buy these statistically cheap cos. only on basis of cursory numbers analysis. I’ll start that portfolio thread soon.

Disc: Invested. 5% of personal portfolio.

1 Like

Why advertisement revenue down 25-30% both for radio and print (Jagran) in Q4 pre Covid-19 period ? Shift in platform preference or weak economy ?

For radio, the reason was cut back of ad expenditures by govt nd local retailers.