Oh, you are right. I thought DB Realty was part of DB Infrastructures (which is part of DB Group). This is a different promoter altogether. My bad. DB Corp had moved up similarly when Adani had announced purchased of DB Power assets last year (it fell through later) which is owned by DB Corp. I thought this was something similar. Should pay more attention, and not assume things!

In that case, there is a good chance this is due to results expectations only. That’s good news for Jagran as well though that litigation is a bad development.

It has been around 3 years of holding Jagran Prakashan for me. Jagran has been one of the most interesting and controversial (among my investor friends) picks for me. I thought of sharing my experience and learnings of making a contra investment. I first bought the stock at ~37 and kept buying till ~66-67.

Jagran was a case of classic value investing. This was as contrarian as it gets. There was (and still is) extreme pessimism around the stock. Everyone told me this was a sunset industry, this kind of value buying doesn’t work anymore, no FII/DIIs would ever touch this stock, who reads newspapers anymore and in this era of technology why do you want to touch an old school stock?

I always list down 3 reasons before I buy a stock. These were my reasons for Jagran –

Strong balance sheet strength and cash flows

Jagran had 600 cr of cash & investments on a Market cap of 800 cr. The company had also generated ~300 crores of free cash flow every year. There was no long-term debt and Dainik Jagran was the #1 newspaper in India, with a strong foothold in the Hindi heartlands. In fact, within the 600 crores is freehold land whose fair value is much higher than stated in the balance sheet.

Consistent history of promoters sharing wealth with minority shareholders

Whenever you are buying a company based on balance sheet strength or cash & investments, it is important that the promoters have a history of sharing wealth with shareholders. The promoters of Jagran have been excellent in this regard. Instead of making any unrelated acquisition, they have been buying back stock and paying regular dividends. When I bought the stock, the dividends and the buyback amount for the last three years was greater than the market cap of the stock at that point.

The predications about the death of print were a tad bit exaggerated

What happened in the west does not necessarily replicate back here in India. The growth of print had stagnated, and I was under no assumptions that this would be a 10x or a multibagger stock, but it was also clear that newspapers weren’t dying, at least not anytime soon. The company was still generating healthy revenues and cash flows. My scuttlebutt also showed that Dainik Jagran had a strong brand recall in its target market and was still favoured by the reader. An acquaintance also owns a small local newspaper in UP and she confirmed that newspaper readership was not declining the way people thought. The cost of a newspaper in India is incredibly cheap and hence people continue to buy it just out of habit.

This is where owner’s mindset is particularly important. If I were offered to acquire Jagran at 800 cr, a company that has cash & investments worth 600 crore and makes around 300 cr of free cash flow every year, would I buy it? Absolutely. It does not matter whether FIIs buy it or what the charts say. The market is a weighing machine in the long run, and it will weigh it correctly, sooner or later.

It has almost been a 3x since my first buy and I continue to hold it. Even today, excluding the cash and investments, the stock is available at roughly 4-5x free cash flow, with digital being an added optionality. The outlook for print is quite bullish for the next couple of years. DB Corp has posted excellent numbers and I expect Jagran’s numbers to be somewhat similar.

This was an important lesson that whenever extreme pessimism is priced in, the probability of market being wrong doesn’t need to be very high to generate a favourable return.

My post in Shivalik thread got flagged so trying here.

@dd1474 Since one of the reasons for increasing allocation in Jagran is expecting recovery in Music Discovery & as someone who is invested in both Jagran and Music Broadcast, I want to pick your brains - Don’t you think it would be more prudent investing in MBL. Management has guided about discovery, company is concalls regularly & for Jagran, its has surged almost 50% in a month and there are family disputes as well.

Thanks for seekiing my view. In case of Jagran, the newprint price decline, improvement in advertising (hence better prospect of Music broadcast as well, which has contributed to write down in March quarter results) and attractive value with cashflow geneating business, i find Jagaran Prakashan better suited for my approach. Irresptive of external chellanges, Jagran has generated feee cashflow and distributed to shareholder, which I could not find in Music Broadcast. Music broadcast may have supeiror performance due to operating leverage but is relatively inferior in cahflow generations. It need to pay license fees every 5- 10 years to government. Hence, I find Jagran Prakashan more appropriate for my investing style. Hope this answer and wish Music Broadcast also give return which exceed your expecations (indirectly wishing good fortune for me as well ).

Disclosure: My view may be positviely biased due to my investment. I may exit investment without informing Forum. I am not SEBI registered advisor. I am also not suggesting any investment action.

@dd1474 and other seasoned friends here, i am trying to calculate Jagran’s ROCE for printing business ex. excess cash. Below is the my calculations, need a cross check from the experienced members here.

Mar-12

Mar-13

Mar-14

Mar-15

Mar-16

Mar-17

Mar-18

Mar-19

Mar-20

Mar-21

Mar-22

Mar-23

TTM

Sales +

1,244

1,412

1,589

1,662

1,754

1,864

1,868

1,940

1,772

1,133

1,401

1,594

1,586

Expenses +

952

1,122

1,224

1,227

1,255

1,337

1,400

1,533

1,397

879

1,044

1,298

1,301

Operating Profit

293

290

365

435

499

526

468

407

375

254

357

296

285

OPM %

24%

21%

23%

26%

28%

28%

25%

21%

21%

22%

25%

19%

18%

Other Income +

45

28

52

30

49

40

27

25

18

27

56

85

93

Depreciation

66

69

73

95

84

82

82

75

84

69

60

49

48

TOT EBIT (OP Profit)

359

359

438

530

583

608

550

482

459

323

417

345

333

Mar-12

Mar-13

Mar-14

Mar-15

Mar-16

Mar-17

Mar-18

Mar-19

Mar-20

Mar-21

Mar-22

Mar-23

TTM

Share Capital +

63

66

65

65

65

65

62

59

56

56

53

44

Reserves

688

853

886

968

1,292

1,605

1,459

1,281

1,315

1,438

1,609

1,318

Long term Borrowings

177

310

293

279

109

0

0

0

0

249

249

81

Short term Borrowings

135

165

162

353

243

81

91

293

199

2

12

192

Lease Liabilities

0

0

0

0

0

0

0

0

33

26

55

54

Other Borrowings

21

22

24

100

27

75

0

0

0

0

0

0

Trade Payables

67

88

112

101

51

103

107

136

151

81

117

145

Advance from Customers

14

17

21

16

18

32

19

16

17

17

16

28

Other liability items

282

242

312

332

220

251

304

319

270

292

266

357

Total Liabilities

1,447

1,764

1,874

2,214

2,025

2,213

2,043

2,104

2,042

2,160

2,377

2,219

Fixed Assets +

506

504

507

498

704

715

740

728

715

659

635

548

CWIP

61

131

114

72

79

76

12

3

2

2

2

2

Investments

292

477

596

630

677

757

601

569

567

905

1,085

1,062

Inventories

68

73

88

82

59

83

62

163

182

51

80

84

Trade receivables

244

302

325

350

351

414

471

482

436

339

338

361

Cash Equivalents

72

49

31

489

34

78

38

40

28

79

129

45

Short term loans

0

68

52

8

5

4

4

4

5

3

4

4

Other asset items

205

160

161

86

117

87

115

115

108

123

104

113

Current Assets

384

424

444

921

444

575

571

685

646

469

547

490

Current Liabilities

363

347

445

449

289

386

430

471

438

390

399

530

Debt

333

497

479

732

379

156

91

293

199

251

261

273

Cash

292

477

596

630

677

757

601

569

567

905

1085

1062

Excess Cash

-41

-20

117

-102

298

601

510

276

368

654

824

789

Net Working Capital (CA-CL)

21

77

-1

472

155

189

141

214

208

79

148

-40

Net Fixed Assets

506

504

507

498

704

715

740

728

715

659

635

548

ROCE

68%

62%

87%

55%

68%

67%

62%

51%

50%

44%

53%

68%

Legend:

Cash = Investments

Current Assets = Inventory+ Trade recivables+ Cash equv.

Curr. Lia = Trade Pay + Adv. from customers + Other liability items

Debt = Long term borrowings + short term borrowings

I have not included excess cash to avoid compressing ROCE artificially.

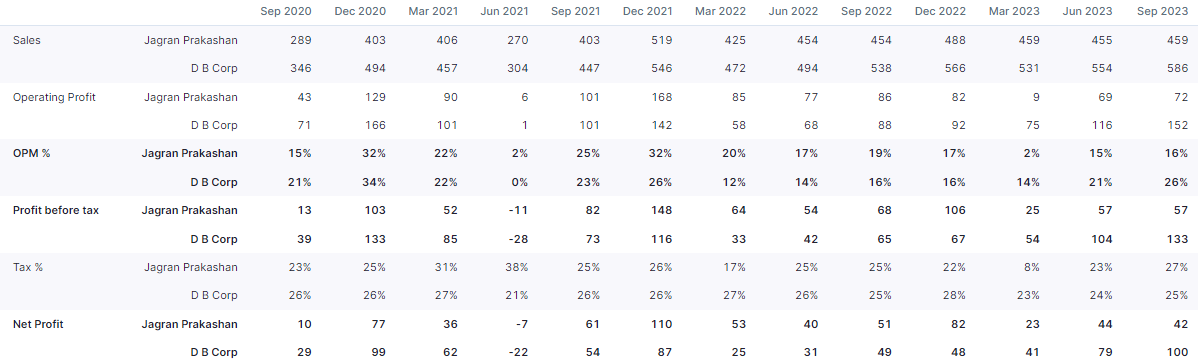

Seems like from Sept 2022 onwards DB Corp has taken a decisive lead wrt to Jagran.

Earlier the Revenue diff used to be around 10% but now it has increased to >20%

Also somehow DBCorp has been able to realize the benefits of the fall in print cost better!

Dec 2021 Mar-22 Jun-22 Sep-22 Dec-22 Mar-23 Jun-23 Sep-23

It is difficult to say exactly why DB is getting a premium from market over Jagran. Might be that there are elections in states where market is dominated by DB (mp, CG, rajasthan) and the same is being factored in the prices. Also, DB were able to recover their sales much quickly post Covid and hve maintained the momentum.

I was looking at jagran some time back and saw significant pledging of promoters share. Don’t know how much pledge is there right now but you might want to check that. A lot of jagran earnings are from their investments and net profit percentage from only their core businesses might be compared with DB to gain sone other insights.

Overall i think DB has been much aggressive and relatively more successful in pursuing organic growth and the same is being factored in by market.

Of course I could be completely wrong so please do your own due diligence.

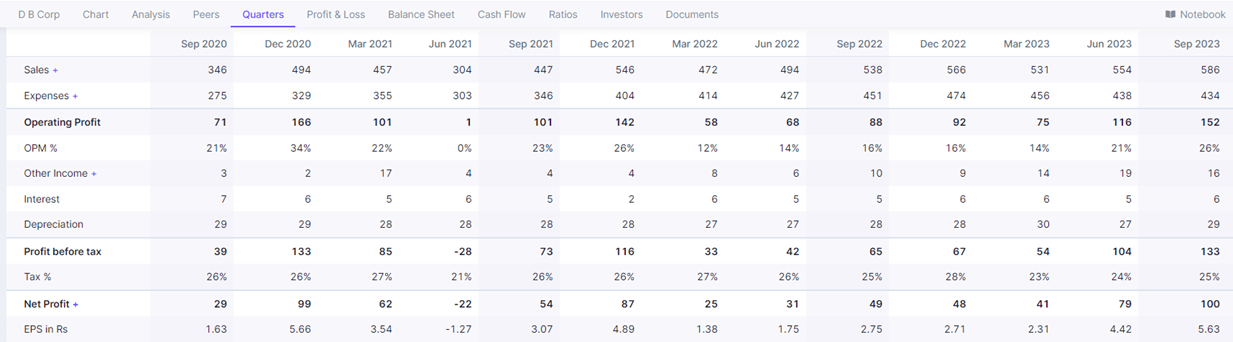

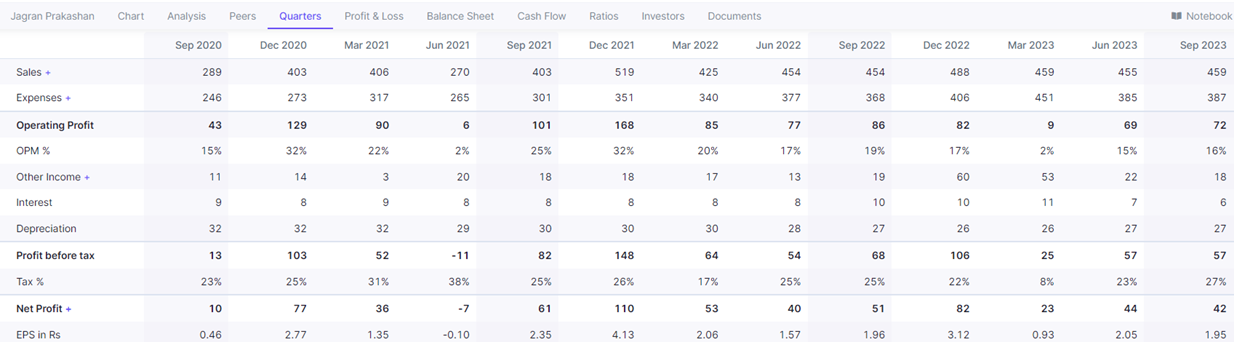

Post Q2FY2024 results of Jagran Prakashan, I find that the company performance has not improved. As per presentation of the company, performance continue to be adversely affected by limited growth in advertisement revenue and higher newsprint cost. While it expect improvement on both these factors and report improved performance during next H2FY24, I find something specific to the company which has adversely affected the performance then industry wise issue.

The rival to company in Hindi newspaper, DB Corp also reported number for Q2FY24. DB Corp continue to show superior performance due to higher advertisement revenue growth in lower newsprint cost.

Find enclosed quarterwise performance of both the companies.

In September 2022, Both DBCorp and Jagaran operating profit comparable Rs 88 cr and Rs 86 Cr respectively. In next 12 months, DB Corp Operating profit almost doubled to Rs 152 Cr same, for Jagaran declined during the period.

So, in my understanding, while the industry is doing reasonably, Jagarna Prakashan has lost market share to the peers in last 12 months. I would contribute to promoter family conflict as main factor for lackluster performance. Since, Jagaran Prakashan, was short to medium term trade (with expectation of benefit from higher ad spend in election year and lower newsprint price), I would have to exit at appropriate price. Given the family conflict situation, it is difficult for me to visualise benefit of better prospect being reflected in company performance. Hence, I have decided to exit from my holding in the company.

Disclosure: My view may be negatively biased due to my exit from the company. I am not SEBI registered advsior. I am not recommeding any investment action.

HDFC Mid-cap Opportunities Fund exited a large chunk, though 90% of it was absorbed by its own HDFC Multicap fund. My worry is if the stock’s underperformance is being caused by it losing market share. There is also the promoter dispute which is not getting resolved. But between the two, market share loss would be the more concerning thing. Hard to recover credibility with readers once they move away to a competitor.

Nevertheless, I expect Q3 margins to be much better given advertising revenue uplift from the elections that happened and the national elections coming up, and lower newsprint costs (per management commentary, there is a lag in benefits accruing from the fall in newsprint costs due to higher inventory. My guess is Jagran must have had more inventory than DB Corp).

I thought the Jagran results have been very good this quarter, especially considering valuation gap versus peers, and have been somehow surprised by the markets relatively muted reaction today.

Large positives for me were:-

EBITDA has grown a solid 43% YOY despite slower YOY growth in revenue (5%). Margins have also expanded from 16% last quarter and 17% Q3 last year to 20% now, and this increase is going to get better as the twin tailwinds of revenue growth come into Q4 and also newsprint price corrections start reflecting even more (all peers have confirmed sharp falls in newsprint costs over the last couple of Qs). Just cost of materials for this business has gone down to 24% from 30% last year already this quarter

This is an industry which will benefit from large operating leverage as supply of ad volumes is pretty unlimited in print and additional pages can be added when volumes come in, whilst fixed costs remain the same. In my thesis I expect this operating leverage to play out with increased ad spends expected in Q4 (H2 is generally heavy for the industry + election ad spending will now come in a big way for media)

From a value perspective things look very attractive still. At 1.1x MCap to sales, last time when tailwinds were there this was at 3x sales. Even 6.3x EV EBITDA current multiple looks very cheap versus the usual 11-12x multiples in good times. Value is further confirmed by the excellent dividend yield of 4%+

Peers such as DB Corp/HT Media have already seen significant re rating. Even radio industry peers like ENIL and Music Broadcast saw significant re rating post tailwinds starting last quarter. In my thesis, I expect Jagran to also be a similar beneficiary, with these EBITDA margins benefits just starting to come in + Q4 and Q1 ahead having twin benefits of revenue growth + margin benefit.

Charts look good in my opinion. The bottom is clearly in and we seem to be in an uptrend after a Stage 4 fall and Stage 1 consolidation until recently,

Disclosure : I am invested in self and family accounts and am biased, have buy transactions in the stock and other peers here earlier and last week. I am not a SEBI registered advisor and this is not investment advice,

Many things look good but there are three issues 1) Promoter group legal troubles 2) Falling circulation 3) Rumours of acquisition.

Not much one can do about 1 and 3, but watch and hope for the best. But I am concerned about Point #2. There was an over 6% fall in circulation revenue this quarter. I don’t think there must have been price cuts (not sure, but generally no one’s taking cuts), if so, it reflects a decline in circulation.

Also, they continue to underperform vs DB Corp on most parameters. I have stayed invested, but something’s holding this back.

I agree with your anti thesis pointers in the narrative, but in my opinion till the EBITDA margin expansion + revenue margin thesis here is intact, there is significant scope for the stock to deals with these overhangs.

Even if I am very conservative in my assumptions and take Q4 revenue as flat over Q4 last year and 20%+ margins (already delivered in Q3) as the margin base, it gives me an estimated topline for this year of ~1900 Cr. At 20% OPM, EBITDA is ~400 Cr and PAT is 200 Cr+. At even historical median valuations, there is still is significant upside in share price in my thesis. And this is base case.

What I anticipate would be bull case as like I mentioned above I expect strong revenue tailwinds from central election advertising in Q4 and Q1, coupled with the added benefit of reducing newsprint pricing and operating leverage play out. Revenue could be significantly higher than 1900 Cr for the year in that case. Projections look even much better than above if that happens. I think this is rightly reflecting in DB Corp/HT Media but not in Jagran, yet.

Not only upcoming Q4, Q1 should also be strong with the election advertising peaking in March/April/May.

All true - the issue is the industry itself has become unattractive. I agree with your points, but whether it attracts interest to move the price is the question. Personally, I feel it will get attention only if the market goes down a bit more. But let’s hope for the best

I was thinking about the promoter pledge today (actually non-disposal undertaking) and when I looked at the rating rationale related to that NCD, I realized that this NCD will be redeemed (assuming it will be) this week. I don’t believe Jagran has any other major long-term debt.

If this redemption happens, I guess the promoter pledge will go away too. I am not sure how that will impact the stock price, but theoretically, it should be a positive development (assuming other factors such as circulation, newsprint costs etc. have not deteriorated). Thoughts?

While the promoter group is busy flaunting over LinkedIn and other social media platforms. The shareholders lost value over time in this business.

One simple thing such promoters can do is to share cash flows regularly with shareholders however, what they do is completely reverse, they keep that cash in the company and take hefty salaries and perks to enjoy their lavish lifestyle.

Just check what all Aakriti Gupta (the daughter of promoter) is doing over LinkedIn, giving gyan to people over wealth, corporate culture, ethics, business and entrepreneurship etc. while travelling to useless conferences.

You were wise and made the right call here, @dd1474. I should have exited too when you wrote this. They do seem to be losing market share in the Hindi heartland even though their results have been good in Q4 due to the advertising revenue boost (excluding the large provision made). This has been a good lesson on being more cautious about taking bets when terminal value and management issues are greater than perceived undervaluation. They have stopped doing earnings calls for the last three quarters too, which is also a signal of deeper issues. Maybe I will get lucky and get a decent exit at some point as I am not under pressure to sell. Let’s see. Irrespective of what the outcome is, I see this investment now as a process mistake.

Frankly in my opinion days of publishing industry is getting over. Rationally think how many newspapers u purchase at your home daily ? All people are glued to their mobiles and read news their . So impact of newspaper going down, my dad was senior in news paper industry and I have observed this industry very closely. So for long term this industry won’t give spectacular returns