Buy back rules link you have posted is old . New rules , SEBI have tried to plug many loopholes. They can’t do delisting without informing their intention in advance to exchanges, that also has to be done reverse book build only.

They can do buy back but their holding if goes up more then 75 % then even extra single share also above limit has to offloaded in exchange within one year.

And that’s why I was confused about benefit of this buyback

1 Like

Hi,

Before speculating into promoter’s plans of delisting the company, we should atleast make coherent statements. If buyback price is not attractive and only promoters tender their shares, then promoter shareholding will go down (and not up). This is not the first time its happening in a company, I was involved in a buyback in Nalco in 2021 where buyback price was actually lower than CMP and government majorly tendered their stake. What happened after that? Government’s stake went down (and not up).

Also, about your comments about some secret delisting ballots, its not how delisting works. The reverse book building process is completely transparent, where you can actually see (in real time) how many shares are getting tendered along with the tender price. So I would request not to speculate, unless there are reasonable grounds for the same.

Disclosure: Invested (position size here, no transactions in last-30 days)

Thank you. So what you are also saying is that as per the rules they have to necessarily announce their intention to delist before taking their holdings over 75% - is that correct?

I did not know how the delisting/reverse book building process works - I was asking a question if the price is open/transparent during the reverse book bidding process or will it be secret as I couldn’t make that out from the few articles I read. @HIMSHAH clarified that it is open and transparent. So that’s that. Not sure why you think I was making some claim that it’s secret.

Regarding the buyback, whether 75 is an attractive price or not is in the eyes of the beholder. In my view it is not, but for some people it may well be a good price. After all, it’s a few years since the shares have quoted in that range. Of course, if only the promoter tenders, their shareholding will go down. But that’s not what I said. Please read my comment properly. It is quite possible for promoter shareholding to go up if they tender some and others tender more. You can do an excel calculation. Again, @HIMSHAH in his latest comment has added some additional context regarding exchange rules that makes his initial observation clearer to me.

Fair enough about speculating, but I see this as a dialogue/exploratory discussion for me to better understand possible outcomes. It’s not like I blamed the company for cheating public shareholders. I am invested myself and have stayed invested because I consider it good value + trust in mgmt.

1 Like

True, they have to clear before offer that they want to delist. Then instead of tender it will be reverse book build . They just can’t say after buyback if their holding say increase to even 90 , that they want to delist. Then they will have to offload shares till 75 % again.

Nothing wrong in assumption. We are here to not only make money but safeguard our capital.

3 Likes

Anyone tracking this. Now market price is close to Buyback price, what happens?

, you can sell shares in market at higher price , or even if promotor. Wish they can increase buyback price.

Buyback update - https://www.bseindia.com/xml-data/corpfiling/AttachLive/00406cbe-371b-4ecb-ba0b-0d6a8bc4c50b.pdf

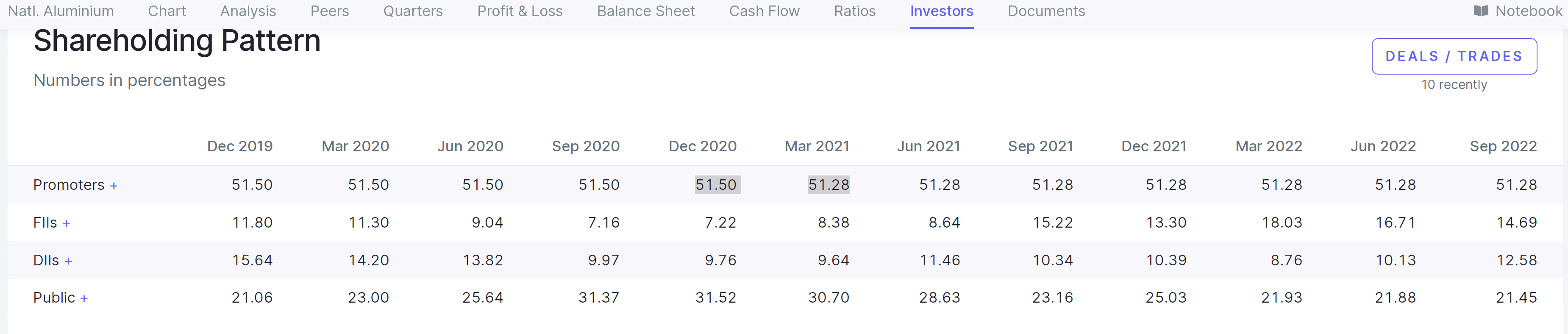

Promoter group tendering 3.6 crore of the 4.6 crore shares proposed for buyback. Post buyback (assuming all 4.6 crore shares are tendered), promoter holding will go down from 69.41% to 67.55% or so, as per my calculations. Promoter group will get about 270 crores at the buyback price of Rs. 75 per share.

Not sure what newsprint prices are currently, various articles seem to indicate they are staying stubbornly high. I was hoping for a stronger correction which has not played out.

1 Like

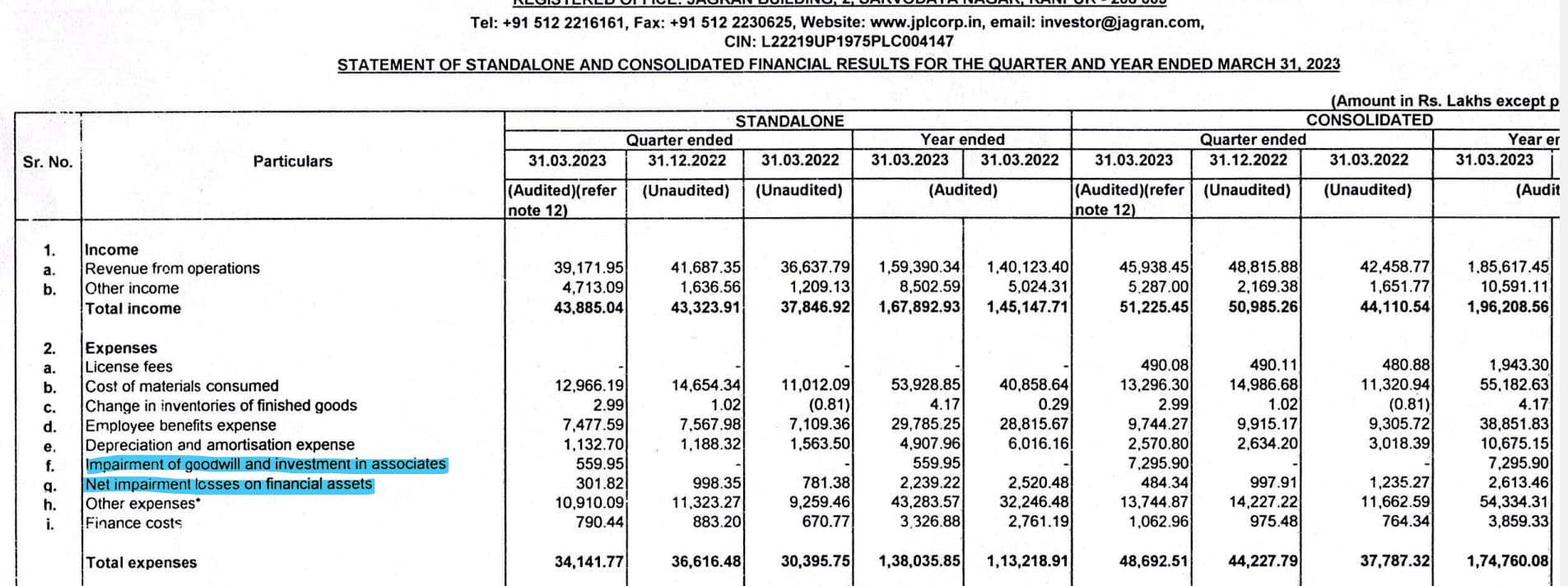

Noticed something weird in this Qtr results that i couldn’t understand. Can anyone help me understand what does highlighted term means?

They have not mentioned in the notes what impairment they have recognized here. I don’t recall any recent acquisition, maybe it is one or more of of the FM channels they may have acquired under MBL. But I am not sure - could be something else too. We will know more during the investor call, I guess.

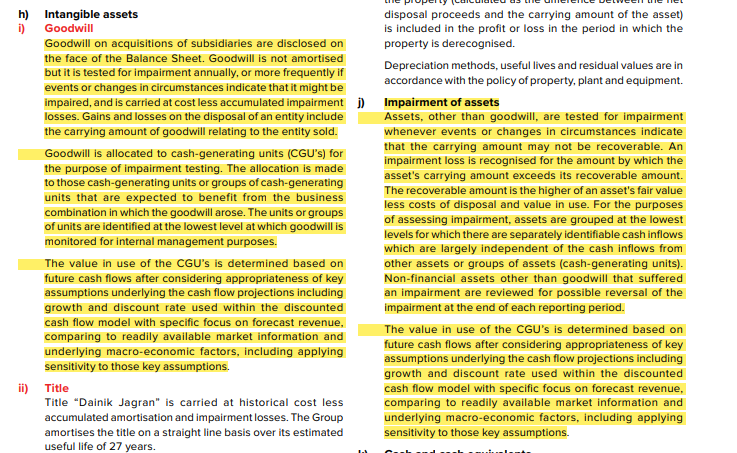

For a general understanding of goodwill impairment, you can read this article which explains it well - Goodwill Impairment - Balance Sheet Accounting, Example, Definition.

Please note that I am not accounting expert and hence my understanding may be wrong. I have gone through the Annual report for FY22 to understand goodwill accounting and impairment policy of the company. Page 226 (pdf file)/Page 206 (print file) annual report provide notes to account related to Goodwill and its impairment.

As we observe, there has been major charge of good will impairment of Rs 73 Cr in March 2023 quarter in consolidated accounts (vis Rs 5.59 Cr in standalone account). In the consolidated companies, Music broadcast is significant subsidiary of the companies. While the notes to result does not provide what all heads the company has provided for goodwill impairment, the price decline in Music Broadcast in March quarter could be one reason for major goodwill impairment.

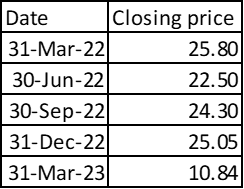

Fine enclosed quarter wise price of Music Broadcast price

During March 2023 quarter, price decline almost 60% from Rs 25 to Rs 10.84 per share and that could have trigger goodwill impairment in my view.

Recently, I have recently added Jagran Prakashan in my portfolio due to following factors:

- High Dividend Yield and Cashflow returning management.

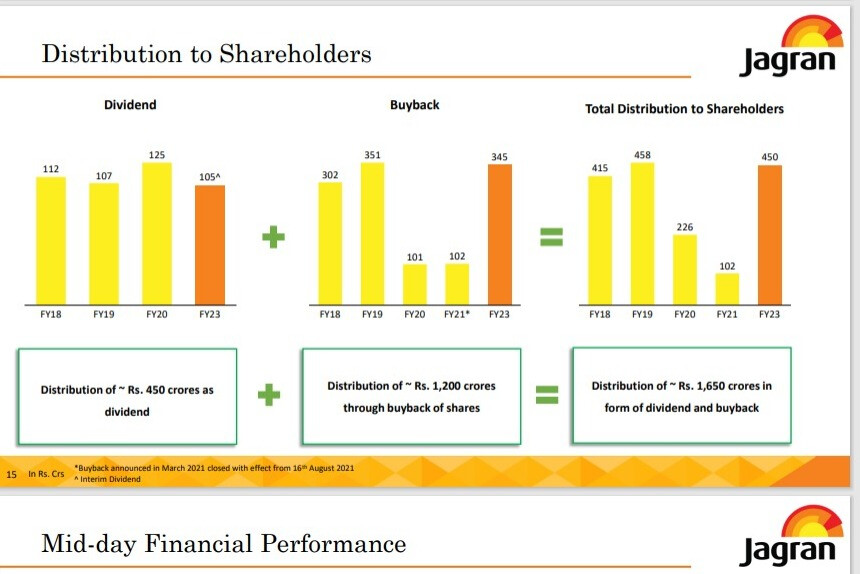

At current price of Rs 75 with Dividend of Rs 4 per share declared in FY23 (and also likely to be sustainable), one can expect around 5%+ Dividend yield from this investment. Further, as compared with current market capitalization of Rs 1600 Cr, the company has already distribution Rs 1650 Cr (by way of Dividend+ Cash buyback) as per March 2023 presentation.

Future cashflow to investor would depend more on future profit and business prospect, but at least intent of management to share cashflow with investor is strongly established from past action in my understanding.

-

Improving Business Prospect:

Media Industry was worst affected industry from COVID. While recovery in economy also resulted with delay, recovery in advertisement and subscription revenue to print media, still it just managed to get to level near FY2020, which means no real growth in past 3 years. Further, profitability was also adversely affected by higher newsprint price. As per Screener compiled import price data of Newsprint, Newsprint import price peaked to Rs 73.54 per kg in October 2022 and now trades at around Rs 65 per kg. The decline in newsprint price along with stable GDP growth and 2024 being Central election shall augur well for sales and profitability of the company in my view. My record of being right with forecast is pathetic at best. Hence, reader shall do his/her own due diligence, as my forecast may revert to mean (that is being incorrect) and very low probability of being correct. -

Concern for Minority shareholder:

The management of Jagran Prakashan did IPO of Music Broadcast in March 2017 as price of Rs 333 (10 face value+ 323 premium per share). Subsequently share was split in 2 paid up (5 shares) in Feb 2019 and bonus issue of 1:4 share in March 2020. So, 1 share held in the company would have been now 6.25 shares, reducing IPO cost per share to ~Rs 53. However, the market price of Music Broadcast was at around 20-25 per share. In order support Minority shareholder, Music Broadcast issue a Bonus preference share (with approval of NCLT), where by only non-promoter investor got a preference share. This is very positive steps in my view. In Past, we have seen Reliance Power did same but the price continued to decline even after that action. However, I consider this as a very positive gesture from promoter.

Negative:

- The management did acquisition of Music Broadcast at around Rs 500 Cr for ~70% equity stake in the company in 2014.

Jagran Group to acquire Radio City | Mint

At current market cap of Rs 382 Cr of Music Broadcast, value of 70% stake ~ Rs 270 Cr, decline of 45% over almost decade of holding. One can also attribute current decline market capitalization to industry fortune also as Radio business continue to suffer post COVID and is the most adversely affected segment of Media sector (if one compare revenue in FY20 with FY23). However, as on date, the acquisition did not yield required return for investors in my view.

https://www.screener.in/company/RADIOCITY/

Disclaimer: My view may be positively biased due to my recent investment (around 1.5% of my equity portfolio). Purchased share in last 15 days. I am not a SEBI registered advisor. I am not suggesting any investment action in the company. I may exit from the company WITHOUT INFORMING forum in case I find any other investment opportunity or change by asset allocation. Reader shall consult his/her investment advisor and do due diligence before making any investment decision.Future cashflow to investor would depend more on future profit and business prospect, but at least intent of management to share cashflow with investor is stongly established from past action in my understanding.

6 Likes

Price declined due to issue of bonus preference shares to public shareholders. You will get details in music radio forum

@HIMSHAH

Your point is valid. However, the Prefernce share are issued only to non-promoter group and hence Jagran group did not received and only minority sharholder benefited, but price decline resulted in lower valuation, and hence impairtment loss in my limited understanding.

1 Like

I was tracking jagran. But exited. Paper industry is dying . Newspaper cost increasing. Digital media eating away advertisements revenue. Sale price of paper don’t cover cost. People read online news and watch tv, tweeter etc has taken sheen of this sector.

So was interested when price was down and exited when got reasonable returns

2 Likes

By not taking bonus preference shares the minority shareholders of Music Broadcast benefitted but minority shareholders of Jagran Suffered. Further on 22nd June 2022,when the whole scheme was already declared that only minority shareholders of Music Broadcast will get preference bonus, the management holding 29,15,512 shares of Music Broadcast,under, RSMA ADVISORS PRIVATE LIMITED sold to Jagran Prakashan at around Rs: 22.70,there by adding losses to Jagran Prakashan.

2 Likes

@hemantbhatia

Completely in agreement. More so when IPO of Music Broadcast happen, the company issued new shares and offer from Sale was only from Promoter family members and not from Jagaran Prakashan. While, I can understand it might be stategic investment for Jagaran Prakashan and hence they did not wanted to reduce their holding, but in that case, Jagaran Parakashan Minority shareholders have not gained any thiing from premium issue of Music Broadcast. So if equity price decline from IPO price, Jagaran Prakashan Minority shareholder also took hit due to MTM loss, but no profit realised by selling shares to New equity shareholder of Music Boardcast by Jagaran. In that case, I would assume it would be fair for the promoter who sold their share in Offer for sale shall have taken hit and not Jagaran Prakashan. Jagaran Prakashan shareholders also include minority shareholders and not only promoters.

So completely in agreement with your view point.

Discl: No change from previous post

2 Likes

This is a disclosure about a strange petition/litigation against the company by the promoter family members themselves (including the Chairman and MD, the patriarch, Mahendra Mohan Gupta).

Quoting from the disclosure here "The petition has been filed before the Hon’ble National Company Law Tribunal, Allahabad, on behalf of Mr. Mahendra Mohan Gupta (Chairman and Managing Director, and shareholder) Mr. Shailesh Gupta (Wholetime Director and shareholder) and VRSM Enterprises LLP (shareholder). The petition raises issues concerning oppression of the minority shareholders i.e. the Petitioners, by the majority shareholders i.e. the other members of Gupta Family, both at the JMNIPL and the Company level. The petition does not allege any mismanagement in the affairs of the Company. In addition to the said other shareholders, JMNIPL and the Company have also been impleaded as Respondents.

Thoughts?

1 Like

Purely conjecture on my part, but this could stem from possibly a family dispute between the various brothers (Mahendra/Shailendra v/s Dhirendra/Devendra)

At best, hopefully the day to day functioning of the company is not hampered while the family settles its disputes through appropriate forums

At worst, it could be a case where the company performance is affected by the feud especially given the next year should be good for the media sector given various elections.

As an aside, possible M&A if dispute can’t be resolved could be a possibility too. This might result in value unlocking for minority shareholders. Not sure if it is connected to Jagran in any way given they are not true competitors, but DB Corp shares have been on an absolute tear in the last few months.

1 Like

Could be, I guess. But was wondering if it’s also connected to that Music Broadcast issue that @dd1474 had mentioned.

Certainly, paper pulp prices should support better operational results for this quarter, but I think DB Corp’s recent share price performance may have had more to do with the land parcel that DB Realty sold to Prestige.

1 Like

Unlikely this is connected to the pref shares issued by Music Broadcast though we are all speculating here. Hopefully the company prvoides more information in the near future.

Also DB Corp (Dainik Bhaskar) is a newspaper company and is not connected to DB Realty in any way.

3 Likes