Btw the company is sitting on huge property assets (long term) as well; I have done a high level DCF a while back with base case at approx.140rs/ per share.

Also, huge short term investment property (260cr fair value vs 90 value on balance sheet).

Reverse dcf shows market expectations is 4% degrowth.

One of the antithesis is the a/c receivables that mgmt have recognised in annual report last year 339cr. Outstanding as of mar 2021.

Receivables is the nature of biz and again every co. vl have receivables issue in this period. That’s also pretty much priced in ( has fallen more since I last posted ).

Against that there’s an added kicker of revenue sharing optionalty wid Google/Meta. If dat happens, thn tide is going to reverse much quicker than anticipated.

P.S :- Receivables this period - I meat that fr almost all cos. the receivables in FY 22 & probably FY23 will be higher due to supply chain issues.

Speculation

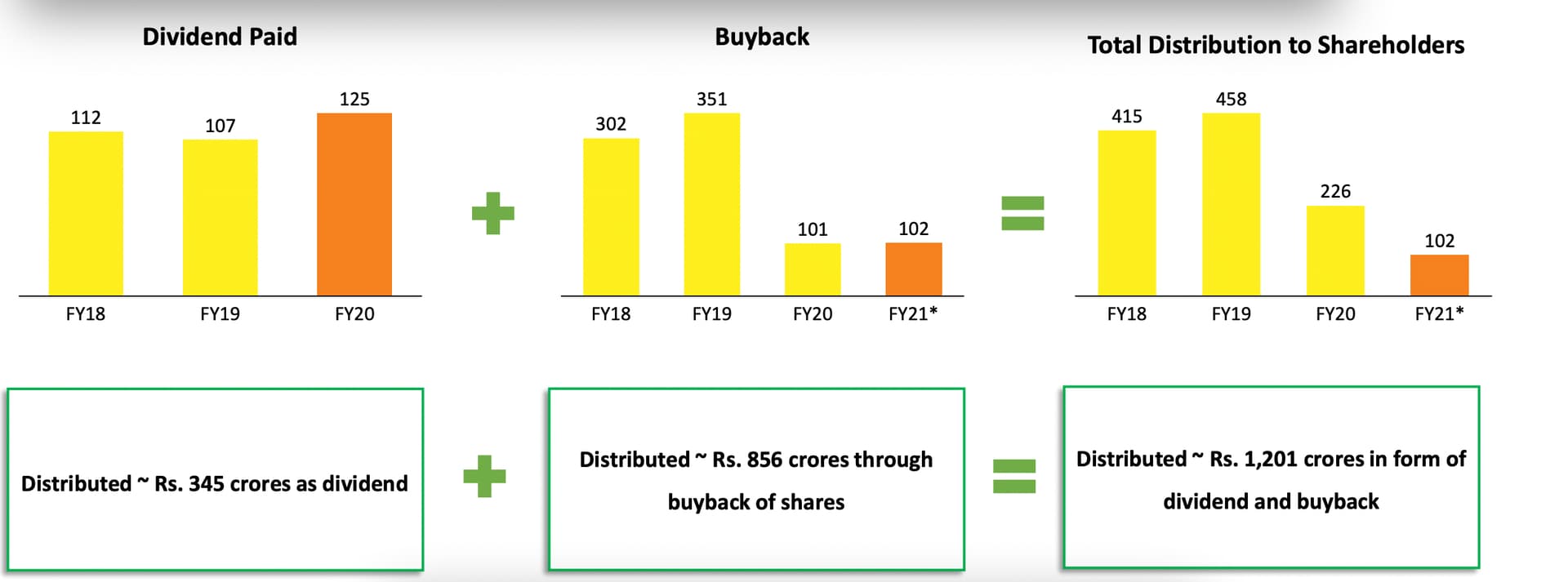

By August 17th, 2022, the company would have completed 1 year since the last buyback closure. Jagran has a history of continuously returning capital back to shareholders over the past few years.

I am speculating one more buyback announcement this month, an open market buyback to the quantum of some 150cr to buy back some 1.96cr from the existing shareholders.

Doing so will increase the promoter shareholding to 75%.

since they were not able to utilize the entire amount proposed for last buyback @60rs, this time the offer price could be in the range of 60-75rs.

Note: This is pure speculation and not an investment reco.

Understand regulation on facebook , google to pay fees to newspaper companies for the news they publish is underway. If materializes, it could be game changer for Jagran !.

Marketcap is 1750cr > generating a solid cashflow of 300+ Cr . i.e Price/Cashflow is below 6.

800 Cr sitting in Mutual funds, Bonds, Bank deposits & Cash. i.e 1/2 the marketcap is available as liquidatable cash.

70% is already owned by the promoter, 10% is with HDFC ,12% with retail&HNI folks and rest with NRI’s FPIs & corporate bodies. - Concentrated shareholder a good sign for delisting.

Despite being in a sunset industry, the business still has solid acquisition proposition for large media tech companies.

What would any sensible promoter do? buyback and increase their shareholding to a regulatory max of 75% & Pursue delisting attempts @ book value or slightly higher. Look for a strategic partner who can add complementary strengths [Like Sharechat(35kCr valuation] ] and move forward.

That seems like a pretty lousy buyback price, given they are well positioned for much better profitability in a quarter or two and possible other growth options like their digital app, radio (plus potential revenue sharing with Google) appearing to be shaping up well. What happens if you don’t tender and promoters end up attempting to delist (assuming their stake goes over 75% post buyback)? Do you have to just tender your shares at whatever price they announce then? I recall Ineos Styro trying to delist a few years ago, and they were not successful then.

As per new sebi delisting rules it is not easy to delist without reverse book built. So your assumption is wrong in that way. Yes if no other tender shares in offer , then promoter will try to adjust in a way that their shareholding reach 75 %.

Thank you. I read this article - All you wanted to know about reverse book building - The Hindu BusinessLine. Gave me more clarity. One question - Is the reverse book build process like a secret ballot, i.e. will the price at which various shareholders offer their shares be not known till the end? I guess the discovered price will largely be driven by the price at which 1-2 key large stakeholders (e.g. HDFC MF) offer their shares, given this is not owned widely.

Anyway, this is hypothetical. Maybe they don’t plan to delist, but just seems like that may be the way they are heading.

Reverse book build is complete open and transparent and available daily on bse and nse. One can check how many shares tendered and at what price and take decisions

For me it’s interesting as well as confusing buy back. What’s company’s intention ,to increase their share holding or reward shareholder as well as promotor ( wich they have right and it’s legal ) .?

They are going for buy back of 17.5 % capital And they have shown their intention that they may also offer shares in buyback. So practically they are reducing their own shareholding at 75 rs y tendering, That also if we assume all shareholder tender shares. If hdfc don’t tender then their shareholding will decrease more from 70 % @75 rs which I fail to understand the logic behind it.

Either they will have to increase tender buyback price from 75 to 100 or more so other offer shares in buy back.

Currently, promoter holding is 69.4%. Public holding is 17%, DII is 10.4% and FII is 3.1%. If public offers up at least 50% of their present holding and FIIs offer up 20% of their present holding, the promoter shareholding will actually go up after the buyback even if HDFC only tenders a very small number of shares. It will go up over 75% actually. If HDFC offers up a bit more, promoter holding can go up to 78-80%.

Looks like the objective may be to get public holding to a small number and then go for delisting. But if reverse book build is transparent as you have clarified, then staying invested could pay off. Of course, all this assumes the business does well and there is not something else going on. It’s more or less a bet on the management’s ethics.