We should not expect dividend for fy21 as they are doing buyback for 120crs. For a believer this is the best thing to be doing.

1 Like

Yes, this is artificially inflated price.

More than dividends one should lookout for exit price. Whatever dividend yield in a declining business will always put your original invested capital at risk.

Good observation, unfortunately i don’t understand the business & competitive landscape that well. All I understand is

1.there is some 35-40% fixed cost & rest is variable cost business. Which limits the downside.

2. 10cr+ direct consumer reach.

3. Brand recall.

this stock came into my radar only due to the aggressive buyback policies over the years & the (cashflow)/(market cap) metric.

1 Like

Will be interesting to find the revenue modeling for this.

1 Like

Lots to like about Jagran’s Q2 results.

A few takeaways:

-

Circulation revenue is holding up - print’s not quite dead yet. It’s not at the same level as Q2 FY20 (pre-Covid), but per copy realization has gone up.

-

Sharp uptick in profitability - particularly commendable given raw material prices (newsprint) have been high. I think this is possibly a new normal that we can expect in terms of lower costs overall. As and when newsprint prices fall, this could further boost margins.

-

Advertising revenue is back including from government and most industries. Auto advertising is down (reflecting poor auto sales in general). In UP, possibly election related advertising expenditure could have helped.

-

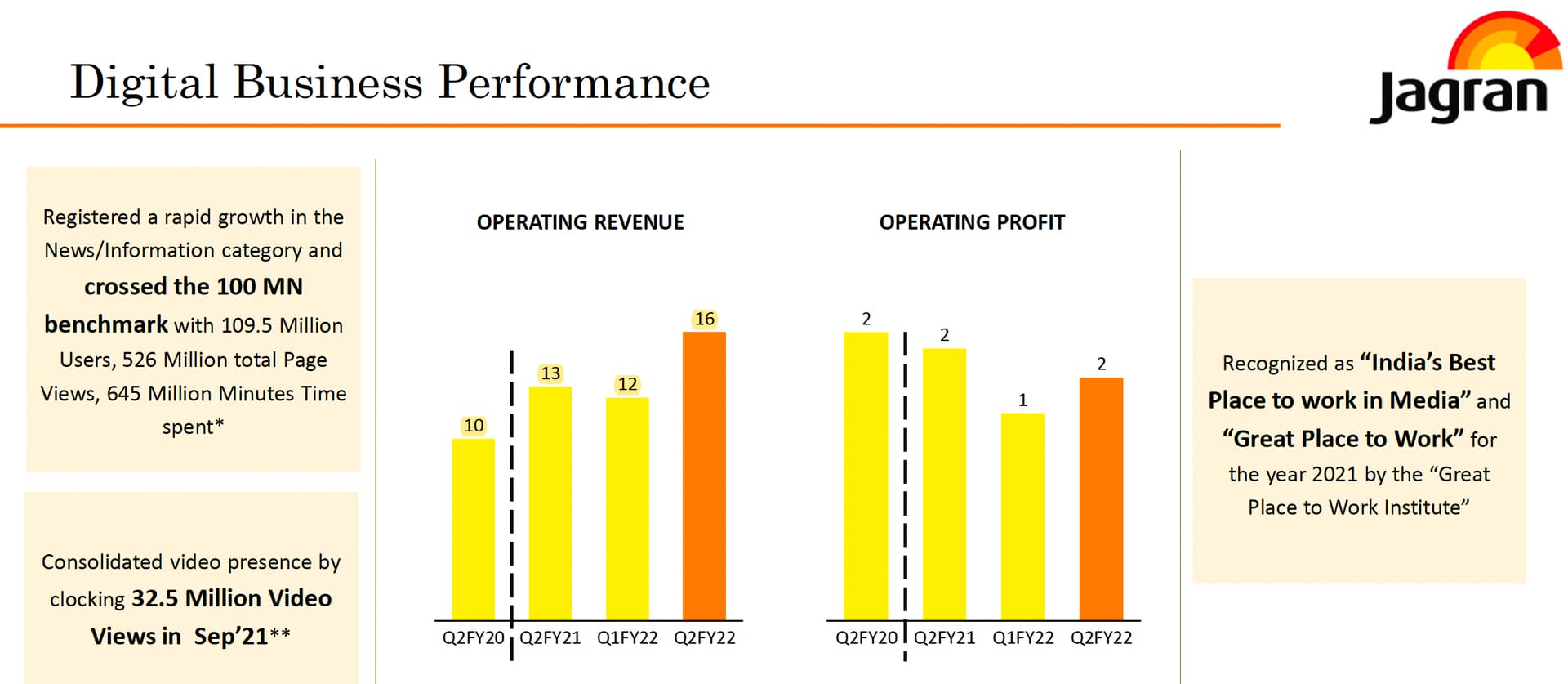

Digital and Radio have also done well. Nothing outstanding here, but generally positive.

-

Overall operating revenue is still 20% below pre-covid levels (i.e. Q2 FY20). Print growth will continue to be a challenge, but there’s the opportunity to grow it back to pre-covid levels.

Net cash at group level at Rs. 680 crores. Will be interesting to see if they do some further investments to spark growth or if they will stay content harvesting print as it stands today. Digital will be a long road, I think.

8 Likes

Surprising results. As you said correctly, print is not dead still.

Disclosure : Invested.

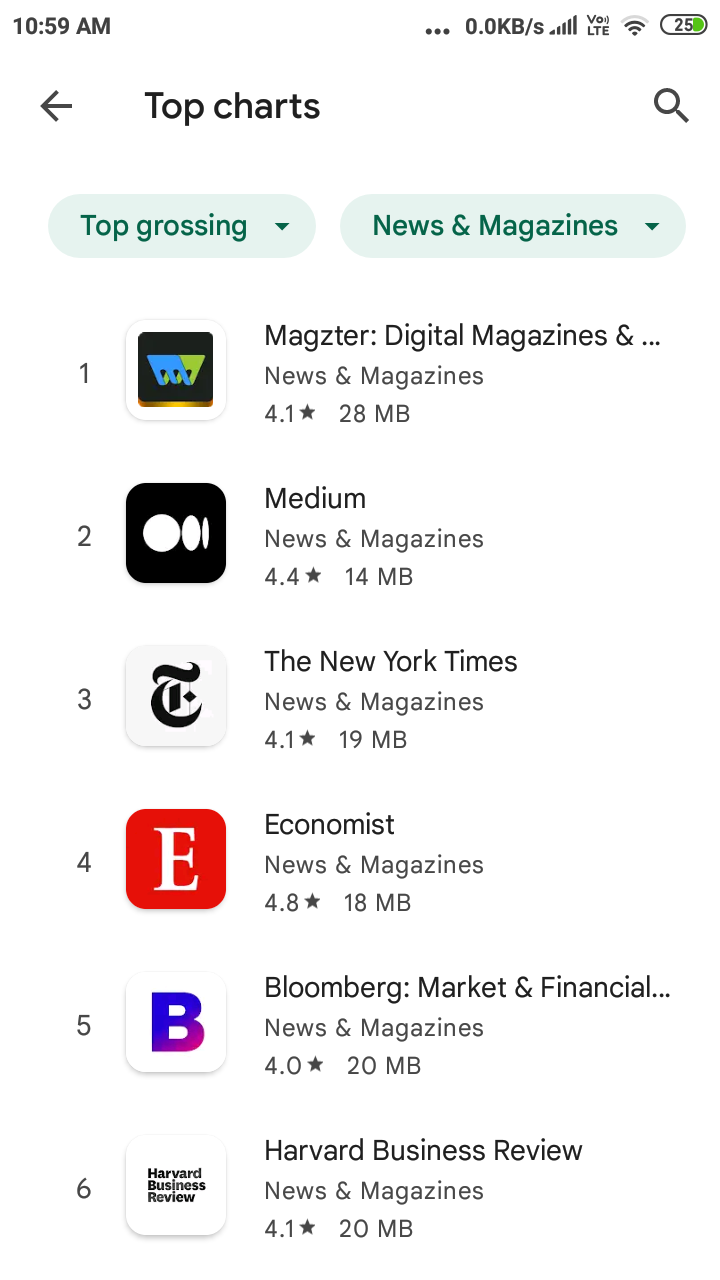

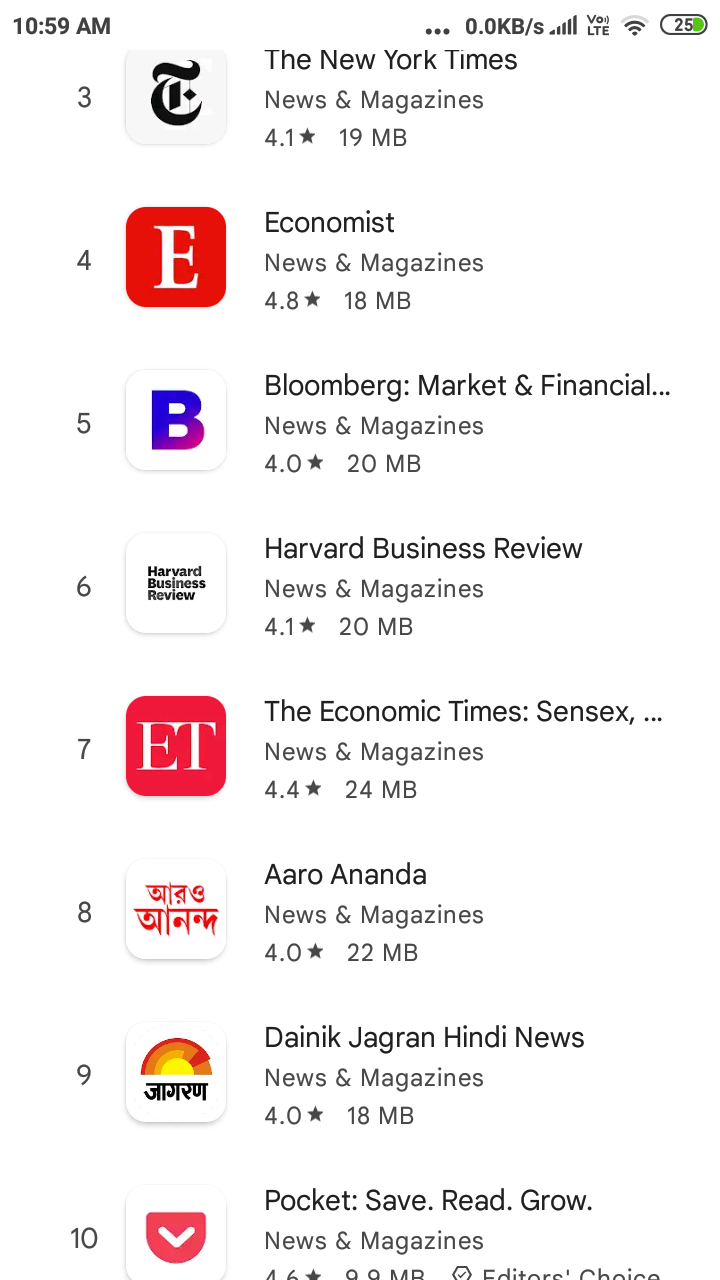

Jagran Prakashan has consistently been among the highest grossing News and Magazines app on android for few months and has been improving its rank.

@harsh.beria93 and interested shareholders, is there a way to estimate the revenue contribution of this part of the business.

Thanks

2 Likes

Jagran reports their online sales numbers. They are still small but growing. This is a number which should definitely be tracked.

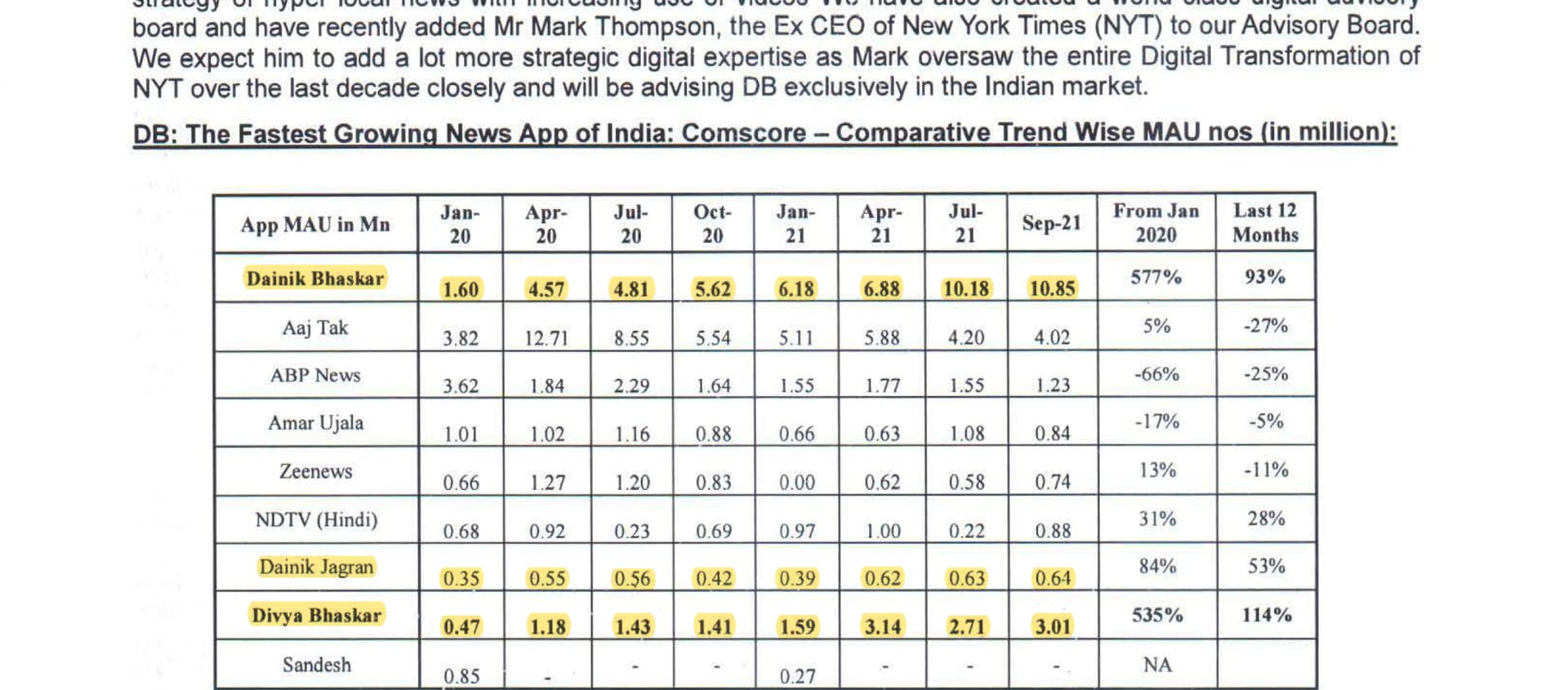

DB Corp shared monthly active users across major regional (including hindi) news and media companies in India in their last update. This might be a more appropriate benchmark and reflect economic potential of different apps. In this, DB seems to be doing exceedingly well. At the same time, dainik bhaskar doesn’t appear in the top grossing list, where jagran finds a mention. We can ask about this divergence in the next concall.

Disclosure: Invested in both DB Corp and Jagran as deep value opportunities (position sizes here)

1 Like

I think this is because DB Corp has kept it’s app free (free of charge and free of ads). I heard the management say in the last two concalls that they want to first establish online presence before starting to monetize. And I personally did not like this idea since in the online world there will always be somebody giving stuff for free and not even showing ads.

2 Likes

Promoter has pledged 99.99 % of the shares. What does it implies ?

Kindly go through the thread. It has been discussed extensively

Thanks Mr Mihir. I could only blame by lack of patience for not going through previous threads. But one pertinent question. When so much of capital is flowing in the market now particular of start ups , why , Jagran, a established profit making media firm should go for debentures at such high rates and need for pledging their shares towards it. Is it a factor of their reliability/reputation in the market ? .

The money was raised during COVID times as an emergency buffer. The rates are ok vis a vis the time they were raised. Regardless the company has done well since raising of money and the probability of obsolescence in newsprint is unlikely due to COVID.

Disclosure - Have exited recently.

1 Like

Thanks for the clarification. Any specific reason for exiting this counter ? ! .

Disclosure - Invested.

Some random thoughts on Jagran Prakashan & the sector as a whole.

Jagran’s Investor presentation post Q3 numbers pretty much lays to rest, the theory that “Print” is dying! It still contributes bulk of revenues & profits & continues to grow, “Digital” may be the future & growing rapidly, but has a long way to go before it is able to replace Print in any meaningful way. This belief of Print being a dying media has gained so much momentum that the sector as a whole has lost meaningfully in terms of valuations. The numbers however tell a different story. So, either the numbers start to disappoint quickly going forward or the very thesis of “Print” dying needs to be re-visited.

Perhaps this belief has gained traction as it has played out this way in the developed world, where Digital had gained meaningfully at the expense of print. India is a different market, in the sense that unlike the developed world where the market has stagnated, the Indian market will continue to grow as more & more Indians get literate. Something that will continue to happen for the foreseeable future.

Even if the theory of Digital rapidly replacing Print plays out as is the common thinking, it is again the listed media companies like Jagran, HT Media & others that are likely to be the main beneficiaries of this trend, having invested huge resources in garnering market share in the Digital space.

The Q3 numbers make valuations somewhat compelling. It will be interesting to see how the story unfolds, but perhaps the de-rating has been over done!

7 Likes

Both PEG and reverse DCF indicates negative growth expectations of the market. I am expecting solid numbers in q4/full year given it was the election year that historically have been a high point. OPM has improved, EPS will see growth due to buybacks and coupled with top line growth should be the lever for re-rating.

D- invested and biased.

1 Like

I am keen to see how Jagran Prakashan’s (and DB Corp’s) Q4 results pan out. Newsprint prices have been quite high - Newsprint sector faces new hurdle on recovery path - Exchange4media, and it will be interesting to observe the impact on their costs. My sense is that we can expect better top line growth in Q4 and though OPM is likely to shrink a bit, the overall impact may not be that much. If there is also strong radio and digital growth (even though they are quite small in overall contribution), this will be a strong rerating candidate. However, if OPM hit is high, then that will pour cold water on rerating hopes.

Long-term, print is not going to grow (and even if it does, will likely be insignificant), but given the fall in consumer demand for electronic goods, postponement of big ticket purchases, and real estate recovery, I sense that print demand will at least not fall for the near future, and continued ad spends/pricing should support better valuations.

1 Like

If my valuation assessment is correct, Isn’t the company almost a cash bargain at its current valuation?

Cash - 160 crs.

Investments( Other than MBIL ) - 840 crs.

MBIL investment quoted - 577 crs.

++++++++++++++++++++++++++++++++++++++++++++++++++++

Total - 1577 crs.

++++++++++++++++++++++++++++++++++++++++++++++++++++

Debt - 352 crs.

++++++++++++++++++++++++++++++++++++++++++++++++++++

Net - 1225 crs.

The co.'s annualized EBITDA on current comes to be 340 crs. - So at current Mcap of 1400 crs. its selling at EV\EBITDA of 1 or literally below the total cash + investments at the co.'s disposal.

Is this truly the market-a-voting-machine in short term or something amiss in my understanding?

Disclosure :- Invested. Transaction in last 30 days

2 Likes

My hypothesis is that after the last couple of buybacks, there is currently insufficient float for a large investor (FII/UHNI investor/MF) to take a significant position to move the price. The retail hands that are still invested here are possibly not exiting despite the low price (or maybe because of the low price). I agree with you that despite the lack of growth, it should be valued much higher than its current valuation. It requires some trigger which has been missing.

1 Like

Not sure how float is dat bigger an issue, I mean FIIs are accumulating and good chunk is wid public too : -

Seems pure play value investing still not back in fashion ![]()

Yes, FIIs are accumulating, but not that much yet if you look at 2019 numbers. Yes, it is quite possible pure play value investing (albeit with very low/zero growth terminal value given uncertainty of payback from digital efforts) is still out of fashion. We will see. FII or DII stake has to typically increase on the back of public shareholding going down. If you see, that is not quite happening yet. Prashant Jain from HDFC MF is sitting on a big chunk which he will never sell as we know ![]()

1 Like