Any news of ITC aquiring MTR ready to eat business and also Eastern Masala and that will make ITC a very strong player in the ready to eat segment in South India with export business to US and Europe

2 Likes

According to screener BAT’s shareholding and other fii and dii has gone down and the promoters shareholding has gone up.How is this being done with any bulk deals ever getting recorded?

1 Like

It is the promoters whose share holding is going up,so the Institutional investors are selling to promoters without actually doing any bulk deal.

2 Likes

Interesting to see that : https://www.itcstore.in/ is not processing any orders currently.

As per the current senario, I see ITC valuation to be standing just below it’s intrensic value with an all time low PE of 15.

Its a great business selling at fair price.

1 Like

Its PE is 25, Screener shows 15 because of one time profit from sale of ITC hotel

4 Likes

I think, we may have to exclude one time profit (due to sell of ITC hotels) and re-calculate P/E to get better idea.

Actually, I based my intrinsic value estimate on the 2024 financials, using fairly modest growth assumptions and factoring in qualitative aspects of the business..

Btw, fair point: after the ITC Hotels demerger, the PE of ITC Ltd did compress — not because the business suddenly got worse, but because the market now sees a higher share of earnings coming from cigarettes and lower-multiple segments.

3 Likes

Recently ITC sent its annual report and annual report of its subsidiaries are available at ITC website.

An observations on capital allocation worried me, look forward to views of fellow VP members.

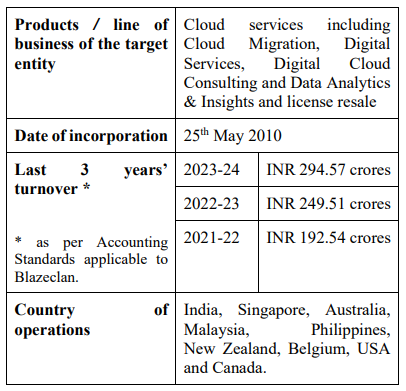

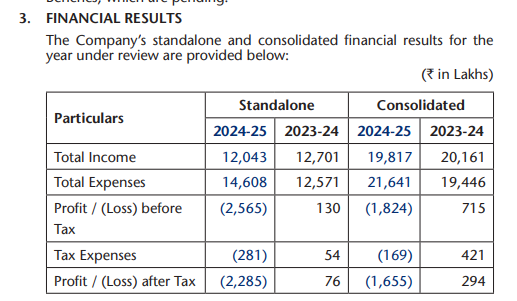

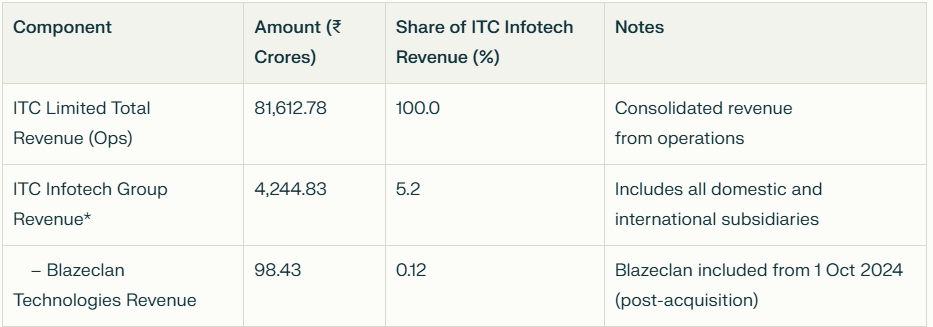

As per exchange notification by ITC Ltd, Blazeclan was acquired for approx. Rs. 485 Crores and was informed to have Rs. 295 Crores as annual revenue.

Whereas, as per published annual accounts, consolidated revenue in FY2024 was 201 Cr and in FY2025 reduced to approx. Rs. 198 Cr.

On top of it, it is a loss making business, even after 15 years of its incorporation and is in IT/ITES industry.

Question arises:

-

Why company overstated revenue numbers in exchange notification (for FY2024) vs those in published annual accounts

-

Valuable cash spent on acquisition of a loss making business, is it really worth.

-

Post acquisition Blazeclan has been proposed to merge with ITC infotech also, this will hide it’s subsequent standalone performance from scrutiny - is it a deliberate attempt to hide some financial goofup.

-

Above all, is management really serious on judicious allocation of capital or it is just another value trap where marketing stories are entirely different vs in reality actions of management.

Disc: Invested

25 Likes

Seems MTR going for IPO listing rather than selling biz to ITC.

2 Likes

i think you are right about the degrowth, what went wrong is not completely addressed?

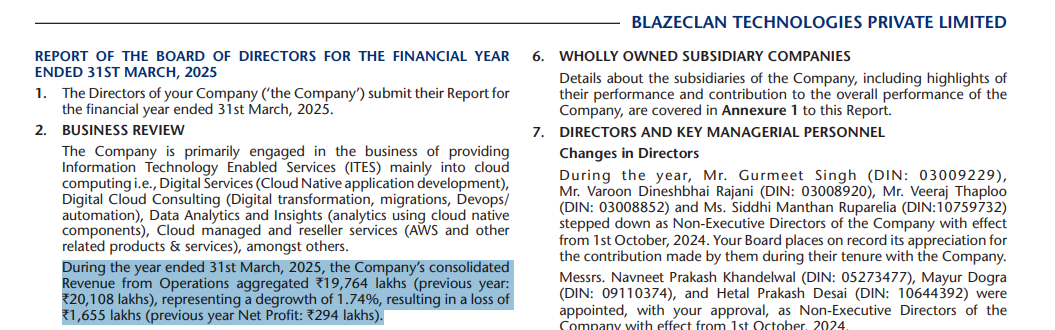

In ITC Limited’s Annual Report for fiscal year 2024-25, Blazeclan Technologies Private Limited’s contribution is described as follows:

- Acquisition & Scope: During the year, ITC Infotech India Limited (a subsidiary of ITC) acquired Blazeclan Technologies Private Limited, a leading cloud consulting firm, to enhance its cloud service capabilities.

- Consolidated Results (for period post-acquisition):

- Revenue: ₹98.43 crores

- Net Loss: ₹3.38 crores

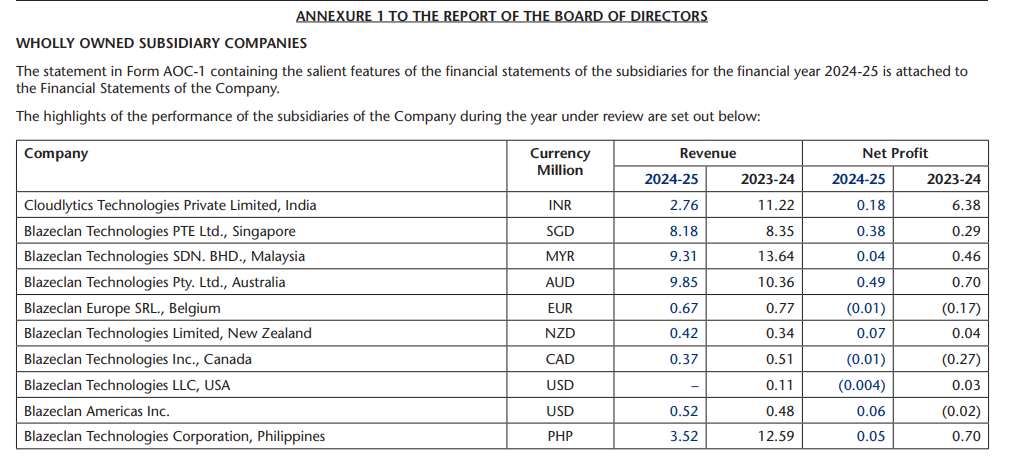

These results are consolidated from 1st October 2024 (date of acquisition) through to year-end. Post-acquisition, 10 wholly-owned foreign subsidiaries of Blazeclan also became step-down subsidiaries of ITC Infotech.

- Strategic Rationale: Blazeclan brings deep expertise in Cloud Migration, Digital Services, Cloud Consulting, and Data Analytics/Insights across major cloud platforms (AWS, Azure, GCP). This strengthens ITC Infotech’s “Cloud services” line by combining resources and broadening digital transformation offerings for clients.

- Financial Footprint in AR: The annual report specifically notes that Blazeclan contributed ₹98.43 crores in revenue but registered a net loss of ₹3.38 crores, reflecting costs and investments related to integration and business expansion during the initial phase post-acquisition.

In summary, Blazeclan’s financials contributed to the consolidated ITC Infotech group figures from Q3 FY25 onward, reflecting both strategic resource enhancement and initial post-acquisition integration costs.

My perspectives

- ITC Infotech contributed approximately 5.2% of ITC Limited’s total consolidated revenues for the year 2024-25.

will need to wait for another year or 2, to understand the expertise added by this acquisition.

6 Likes

My Takeaways from the recent annual report (2024-2025)

- The cigarette business overwhelmingly drives profitability, with a net margin outpacing all other segments.

- FMCG (Others) and Agri offer healthy revenues with lower but growing profit contributions.

- Paperboards, Paper & Packaging balances stable profits despite some cost pressures.

Factors Behind Flat Profit Growth

- Most of the FY25 bottom-line growth at the consolidated level was driven by “discontinued operations” gains from the hotels business demerger.

- When these are excluded, the core business saw only a 0.08% increase in net profit over FY24, primarily due to input cost inflation, weak volume recovery, the need for sustained brand investments, and a strong base year.

- The company’s own narrative emphasizes resilience, but acknowledges that multiple operating headwinds and only partial pass-through of cost increases limited both volume and profit growth in the ongoing businesses.

This performance is consistent with the overall “muted” to “flattish” narrative seen across many consumer and manufacturing companies operating in the mixed demand and cost environment of 2024-25

Key Financial Performance Insights for FY 2024-25:

Continuing Operations (Core Business):

- Revenue Efficiency: Operating expenses consume 68.13% of total income

- Core Profitability: Continuing operations deliver a strong 23.68% net margin

- Tax Rate on Continuing Operations: 25.69% effective tax rate

Discontinued Operations (Mainly Hotels Demerger):

- Exceptional Gain: ₹15,654.65 crores profit before tax from discontinued operations

- Low Tax Impact: Only 0.76% of total income used for discontinued operations tax

- Net Contribution: 17.85% additional margin from discontinued operations

Combined Financial Performance:

- Total Profit Before Tax: ₹42,471.17 crores (Continuing + Discontinued)

- Total Tax Expense: ₹7,529.11 crores

- Total Profit After Tax: ₹34,942.06 crores

- Overall Net Margin: 53% - exceptional performance driven by hotels demerger

Segment Wise

| Segment | Revenue (₹ Crores) | Segment Profit Before Tax & Finance Costs (₹ Crores) | Net Profit Margin (%) |

|---|---|---|---|

| FMCG - Cigarettes | 35,893.57 | 21,091.35 | 58.76 |

| FMCG - Others | 22,015.12 | 1,590.23 | 7.22 |

| Agri Business | 20,163.79 | 1,540.30 | 7.64 |

| Paperboards, Paper & Packaging | 8,424.58 | 883.11 | 10.48 |

| Others | 4,288.11 | 670.73 | 15.64 |

| Total | 90,785.17 | 25,775.72 | 28.39 |

| Segment | Notes / Explanation |

|---|---|

| Cigarette Business | Most profitable segment; high margins due to strong pricing power and market dominance. |

| FMCG (Others) | Margins pressured by input costs; competitive space but growing top line; key for ITC’s diversification strategy. |

| Agri Business | Good revenue growth, but comparatively modest margins; supports supplies and value-added export-led growth. |

| Paperboards, Paper & Packaging (PPP) | Margin pressure from higher wood prices, yet maintains solid profitability; stable, mature business segment. |

11 Likes

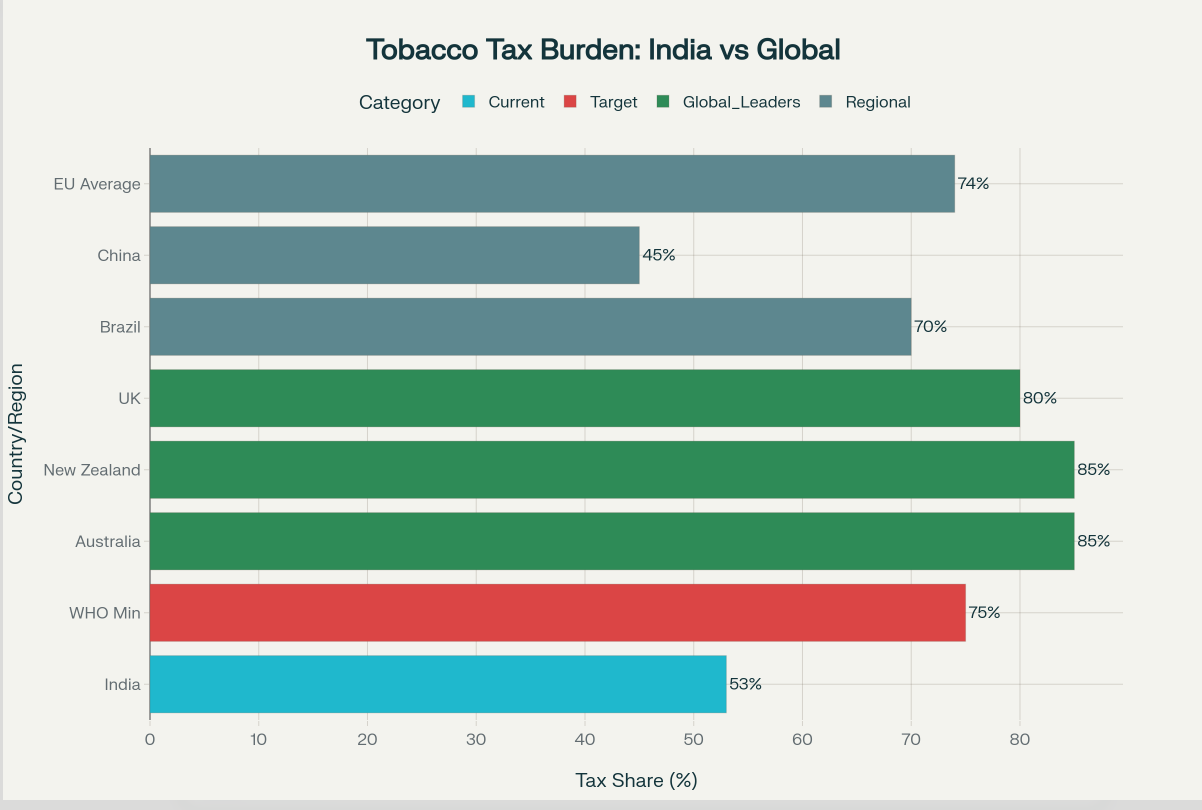

Government proposes to the GST council to have just 2 tax slabs, 5% and 18% while the sin goods like tobacco products levied a 40% tax. Depending on whether there will be additional excise duty on top of that, this can either be extremely positive or negative to ITC.

9 Likes

I’m curious how this could be extremely positive. Could you explain in detail?

1 Like

The current average tax including cess is approximately 53%. So 40% for sin goods without cess can reduce prices and increase volumes

8 Likes

Players like Nestle, Britania, HUL have seen optimism on expected demand boost (due to GST slab change) - wondering if ITC’s Other FMCG business (excluding tobacco products) will not be the beneficiary of the same.

2 Likes

Yes, definitely. But today the biggest contributor to both revenues and profits is the tobacco business. Hence, I explicitly mentioned it. In a decade’s time, ITC FMCG should be able to demand a PE premium equivalent to Nestlé and HUL if they keep pumping money into that business and expand their portfolio through organic and inorganic means.

1 Like

Yes, raising the tax upto 40% can bring in volatility in the price it is traded. when compared with the taxation on tobacco products is greater than 80% globally.

As per WHO, 75% is the benchmark tax can be levied on tobacco to products. So I won’t get surprised if they raise in next fiscal.

My assumptions on the valuation:

India’s FMCG market has surged at a robust 14.9% CAGR over the last five years, outpacing the country’s GDP growth of around 7.1%.

Meanwhile, ITC Limited’s sales grew steadily at about 8.8% CAGR during the same period. Looking ahead, I’m assuming the ITC’s growth is expected to align more closely with India’s GDP over the next decade, driven by diversification and expansion beyond tobacco.

Though ITC’s stock is undervalued today in my view and anticipate a reasonable 2x to 3x return rather than a blockbuster 10x gain.

Risks:

Taxation on Tobacco products shall be increased further.

3 Likes

It seems that, certain entities in market are assuming that, 2 Slabs could be 5% and 18% based on various statements but there could be surprise element and actual 2 slabs could be different. So the Auto sector which is currently moving up, may see some corrections going forward.

At the same time, it is highly possible that, total tax on cigarettes may have to be increased beyond 53% since there will be shortfall in tax collections after implementation of 2 slabs as anticipated.

There is also a possibility that, though Slabs will be only 2, but there is be Additional Layers on top of that which may result into total 4 to 5 slabs. We have to keep in mind that, today we have 7 slabs, 5%, 12%, 18%, 28%, 35%, 45% and 48% considering all cases (high end cars are taxed at 48% as well). The standard GST rate for most passenger cars is 28%, but this is often accompanied by a compensatory cess ranging from 1% to 20% based on the vehicle’s engine capacity, length, and body type, which can push the total tax burden on cars to as high as 48%. This may be reduced to some extent.

ITC generally give sub-optimal returns if bought at Fair Valuation which is its current valuation. I am assuming that there will be more negative surprises once New GST slabs are rolled out and ITC might be available close to P/E of 20-22 as well. As per my historical data, if bought much below Fair P/E, ITC can generate good returns, so I am more cautious about it as of now.

I may be proven wrong this time!!!

7 Likes