Key Buyers: Major buyers of ITC shares included ICICI Prudential Mutual Fund, the Government of Singapore, and Capital Group.

Transaction Value: The block deals amounted to nearly Rs 17,500 crore.

Share Price Impact: ITC shares closed at Rs 422.40, a 4.49% increase after the deals.

Analysts’ View: Positive outlook due to ITC’s strong brand and potential for FMCG volume growth.

Lowlights:

Concentration Risk: High volume of shares being traded might indicate significant offloading by certain entities, potentially hinting at some investors reducing their exposure.

Market Saturation and Stiff Competition: ITC operates in highly competitive sectors such as FMCG and tobacco, which are mature and saturated, leading to slower growth prospects.

Regulatory Challenges: The tobacco business faces stringent regulations, affecting its growth and contributing to overall volatility.

Diversification Impact: While diversification into FMCG is beneficial for long-term growth, it is also a slow process with lower margins compared to the tobacco business, thus affecting overall stock performance.

Economic Conditions: Economic slowdowns and fluctuating consumer demand have impacted revenue growth, particularly in non-core segments like agriculture and paper products.

Overall, ITC’s consistent dividend payouts and stable revenue growth in the FMCG segment are positive, but the decline in profitability and challenges in other business segments contribute to slower stock growth and low volatility.

however unlike in the past, ITC’s FMCG business is showing a lot of traction. Demerger of the hotels business will also unlock value.

ITC is like a fixed deposit for me. My purchase at Rs 190 levels a few years ago is giving me a dividend of nearly 8 per cent which is growing at around 10-12 per cent annually. The demerged hotel biz, other businesses which may get demerged in future and the expanded valuations are all icing on the cake for me.

Sorry for a naive question!

Neither the ITC group nor any of its group companies is insolvent as of now.

Then why exactly was NCLT approval required for demerger of hotels business?

Would anyone know?

All proceedings under the Companies Act, including proceedings relating to arbitration, compromise, arrangements, reconstructions and winding up of companies, are to be before the National Company Law Tribunal (NCLT).

So, while NCLT is the authority for insolvency resolutions, the above mentioned situations which ITC is going through now, will also be dealt by NCLT.

Everyone needs to follow due process irrespective of solvency status. Fairly trivial to search for this. First link on Google: Mergers & Acquisitions In India

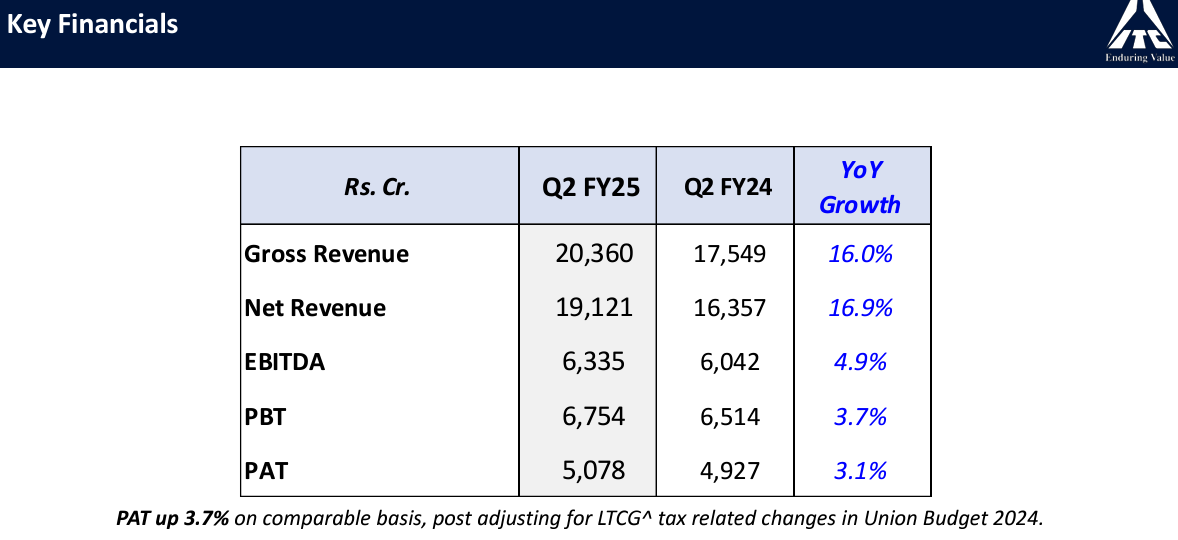

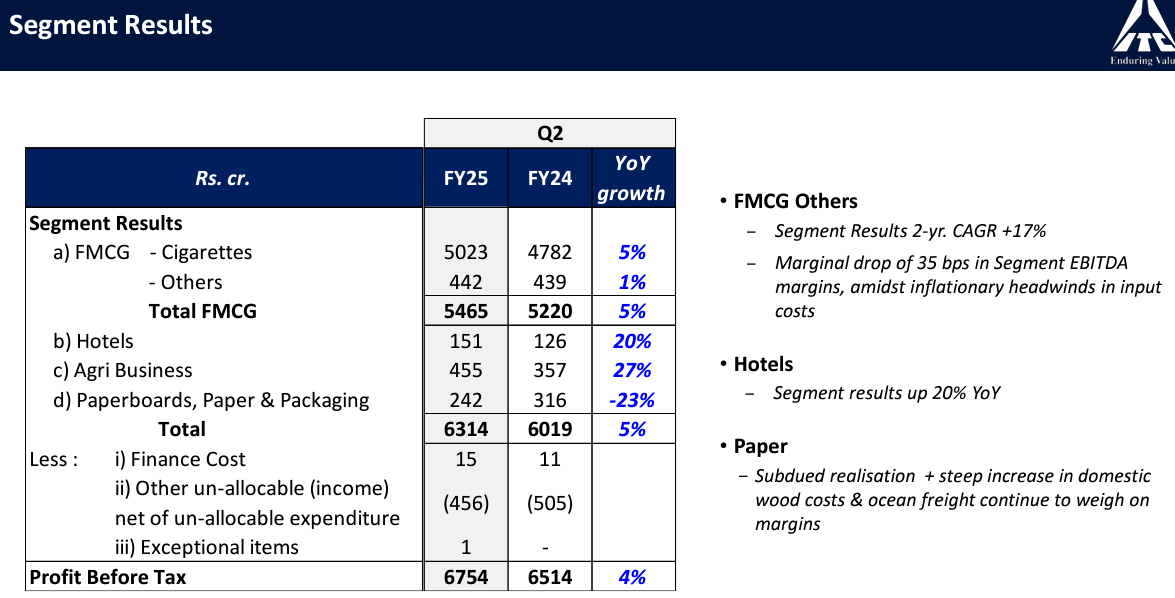

ITC Q2 FY25 Results: Top-line, Bottom-line, and Key Insights

Few insights from ITC’s Q2 results and investor presentation:

ITC delivered robust top-line growth in Q2 FY25, with Segment Revenue reaching ₹23,025 crores, a 9.3% YoY increase. This growth was propelled by notable contributions from various segments:

FMCG: Both cigarettes and other FMCG products witnessed healthy growth, recording 6.1% and 6.3% YoY increases respectively.

Hotels: The segment demonstrated a strong rebound with a 10.9% YoY growth in revenue.

Agri Business: A significant 22.2% YoY surge in revenue was observed in this segment.

Despite this overall growth, the Paperboards, Paper & Packaging segment experienced a decline, with revenue decreasing by 6.8% YoY. The presentation attributes this performance to the impact of low-priced Chinese supplies, subdued domestic demand, and subdued realizations.

ITC effectively managed inflationary pressures on input costs, resulting in resilient EBITDA margins for Q2 FY25. Key strategies employed included premiumization, supply chain optimization, calibrated pricing actions, digital initiatives, and strategic cost management.

The Hotels segment, in particular, showcased strong profitability, achieving a 20.2% YoY growth in segment results, reaching ₹151 crores. This impressive performance was fueled by a two-year CAGR of 34.2%.

Demerger update: Scheme sanctioned by NCLT on 4th October 2024 (certified copy of the Order awaited)

Overall, the Q2 FY25 results demonstrate ITC’s ability to navigate a challenging market environment while capitalizing on growth opportunities in its diversified portfolio.

Disclaimer: Invested and Biased. Less than 5% of PF. No transactions in the last 30 days. Post purely for study purposes. Consult your advisor before any transactions

Almost 3 week since it is approved but certified copy not issued by NCLT / Or received by company. Is such delay normal or there is something else - which is unknown to retail investor.

my understanding, unless certified copy is received by company - ITC hotel’s separate listing will be delayed, accordingly.

These are normal delays only. Expect listing by Q4th mostly before March, 25 as per mgt. AFAIK, demerger process and listing in any business takes about 12 to 18 months.

ITC Approves Share Acquisition In Oberoi And Leela Amid Hotel Business Demerger

The step has been taken to consolidate the shareholding of EIH and HLV under the company, ITC said in a regulatory filing. Post such acquisition, ‘the total shareholding of ITC in EIH and HLV would be 16.13% and 8.11%, respectively’. ITC currently holds 13.69% in EIH while RCL holds a 2.44% stake. In HLV Ltd, ITC holds a 7.58% stake.

Hotels as such is a cyclical business and capital intensive. One of the reasons, many like ITC are moving into a FOCO model which is comparatively asset lite. BT will immediately offload its entire stake bringing down the price, upon listing. The ones with a long term view and conviction on brands like ITC, Fortune, Welcome, Oberoi, Trent, and Leela can use this opportunity to add more.

My two bits… ITC is a perennial hold and business that has so many moving pieces that a few of them out shine and a few lag… Agri biz that was a laggard last few quarters (when the export of wheat was banned) has come up and the paper board business is currently facing headwinds… The hotels business is a deep cycle business, with huge capital demand and bad return on capital… hence the companies moving towards the asset light model, where they just deploy their ops expertise and mktg muscle, with a 3rd party putting in the capital. I would be looking to sell the hotel stock at the 1st good opportunity, mat want to see a quarter or 2…BAT will certainly exit, will try do it in an efficient way, but their stake will not amount to much, as the Parent will continue to own 40%. so it remains to be seen, as to who will buy… maybe retail public…

Let me try to put my question differently…rather than what one would do with their ITC hotel demerged stocks, what must be ideal market cap of ITC hotels as on today, with Indian Hotels trading at a mcap of almost 1 lac crore and PE of approx 76? Is this valuation of Indian hotels sustainable ? If the hotel industry is all about deep cycle related to capital intensive nature, the trajectory of the sector should not work in unison but rather depend in individual companys capex…however something unique happened last few years after covid and we saw this sector also move in unison…is this sustainable change?

Post COVID there was a sudden surge in travel demands since everyone was locked up and for almost two years travelling was very difficult. This will eventually normalise.

For Indian Hotels revenue in FY21 had dropped to 20% of FY20 and since the return in demand has also skyrocketed the revenue to almost 4x the revenue in FY25. Even profits have gone from -320 Cr to 2200Cr and Hence there has been a rerating in the stock and the absurd valuation.

But we should be extremely careful at getting into such stocks at these valuation.

From 2007 - 2021 there was almost zero returns in the stock and such cycles can repeat.