PPFAS added more ITC in Jan 2024.

I would still wait for base formation as the stock just broke the 200DMA but overall good time to add.

P.S. Looking to add to current position.

PPFAS added more ITC in Jan 2024.

I would still wait for base formation as the stock just broke the 200DMA but overall good time to add.

P.S. Looking to add to current position.

I was thinking the same. However this was only a vote on account. there are 2 budgets in the next 1 year and that brings uncertainty on the tax matter. Its cigarette growth has also tapered, which adds to the weakness

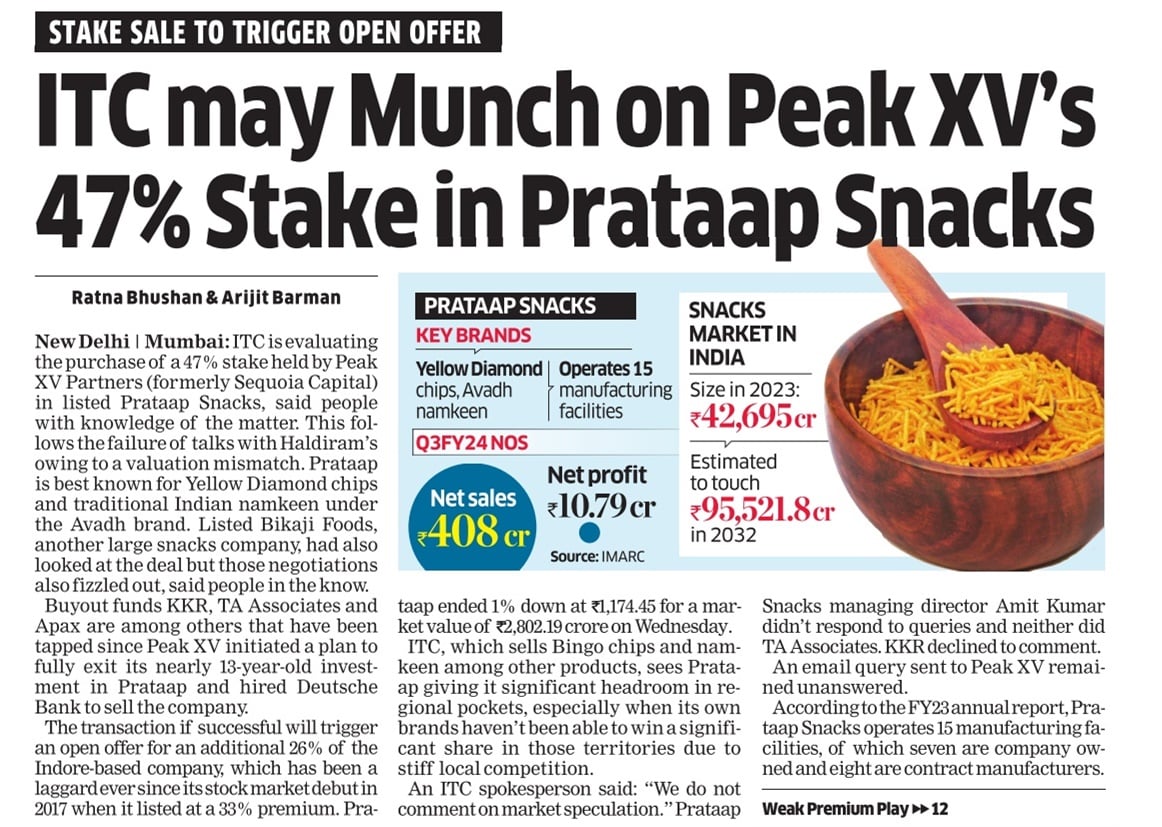

If the deal with Bhikaji and Haldiram failed, Itc has to be giving a higher offer unless Peak xv has toned down their expectations.

On a seperate note, Itc should be prioritising a buyback with BAT wanting to sell. The float is huge in the market. This can be a huge win win for everyone.

Prataap Snacks clarified they are NOT in negotiation with ITC for stake sale.

Currently, Number of equity shares outstanding for ITC stand at 1232crores increasing regularly with the ESOPS. Only other companies which have a higher number of shares outstanding are the likes of VodafoneIdea, Yes bank, IOB,IOCL, Suzlon, ONGC and Tata steel.

Apart from regular ESOPS, ITC has declared bonus issues in 2005,2010 and 2016. If one goes through the 1105 posts above, the discussion on a buyback from ITC has been discarded based on the shareholding tussle between govt of India and BAT.

But, now BAT is looking to monetize on the recent runup in ITC shares and looking to sell their stake upto 4.03% (they have clarified that the stake will not go below 25%. )

A buyback at this moment can work to benefit BAT, GOVT of India (which has directed PSU’s to give back dividends and do buybacks) and retail shareholders.

Reducing the float before the Hotels demerger also benifits all the invested parties further as less shares will have to be issued. How/ Why has ITC management not been thinking in this regards is a surprise to me since the company is sitting on a cash equivalents of atleast 5000crores+.

Any counters to the Buyback suggestion are welcome.

Hi Devarshi, Good point on buyback by ITC to utilize the excess cash since its not going to be funding the hotels, the asset heavy business anymore, and FMCG is also more or less over the phase.

I am all for buyback but feel BAT should sell in open market and then buyback should be announced.

Short term dip should not really concern long term shareholders…Infact the short term dip will ensure greater shares get extinguished in the buyback; more rewarding for remaining long term shareholders.

BAT stake sale and buyback announcement together might give a feel of favoring BAT over other long term shareholders. As if giving them a decent exit, instead of BAT selling in the open market. Also will set precedence for the remaining 25% shares when they want to sell in future…

With significant cash at hand, I believe ITC group should consider couple of inorganic acquisitions and focus on expansions thereby increasing the shareholder value. Buybacks generally are not always great in long run.

ESOPs should be further regulated. Pay the employees at par with the market practices instead of diluting the overall equity. ITC has consistently given away significant ESOPs. Investors would be closely watching

Hi. Could you explain why are buybacks not a great idea to increase shareholder wealth?

A buyback has not been possible at ITC because of tussle between BAT and government. Now, BAT stake sell is the primary reason for buyback being a possibility. Plus. It won’t be just BAT but all stakeholders benefitting.

BAT, still has a board representation, will they really agree to a buyback post their stake sale when they have nothing to gain?

ITC is not exactly a fast growing company that goes about with organic/inorganic growth. Most businesses are now generating huge free cash. I doubt if ITC has any plans to enter a new Business field requiring cash, although I wish they enter hospitals or green hydrogen. Buybacks are better for everyone as it reduces float, Raises share price, and improves returns per share in the longer run. ESOPS are not going to be revised anytime soon. A similar reason has made TCS and Infosys darlings of investors as they do buybacks regularly.

It depend on which buyback route the company management prefer. If it is from open market, then BAT may not find useful after it timmed its stake to 25%. However, if it is tender route in which all shareholder get right to sale share to company prorata (subject to small shareholder reservations), BAT shall not mind as despite reduction in share capital, BAT stake would remain in tact in my view.

Disclosure: Among my top three holdings, my view may be positively biased. Not a SEBI registered advisor. Not sugggesting any investment action. No tade in last 12 months.

Media reported that ITC was planning to enter hospitals some years back. After that, I haven’t come across any further developments.

Technically buyback would increase the share price for some time. Taking into consideration the total number of shares, the uptick would be limited. Also duration of upward price sustenance is subject to market conditions(demand/supply/overall sentiment), often some gains are lost. The subtle message which ITC management team is providing is that they don’t know what to do with the cash generated. So the options are to either give it back to shareholders as dividend or plan for the buy backs.

There are ample opportunities to scout in market for meaningful acquisitions. The value it brings and the sentiment boost will lead to higher demand and hence higher share price valuations. Also note not all acquisitions translate into higher valuations. Some acquisitions will be more valuable than others. It is a cultural practice such large conglomerates should imbibe.

So are you saying that there are some specific opportunities in the market for which ITC should use this cash instead? Can you give a couple of specific examples?

BLOCK DEAL ALERT: ITC

BAT to sell 3.5% stake in ITC via block deals

Block deal price band from Rs 384-400.25/sh

Max 5% discount offered

Total Deal Size Rs 16775 crores for 43.6 crore shares

Citi, Bofa Broker to deal

Hello,

The impending block Deal happened yesterday. In this BAT sold 3.5% of its total stake amounting to 17500 crores around price of 400.25 per share. After this transaction BAT will hold around 25.5% stake. I feel BAT’s overall stake reduction is the good news considering their earlier stand on buybacks and business diversification plans.

And surprisingly around 30 parties bought the available shares. the biggest being ICICI Prudential Mutual Fund. As per data compiled from BSE, ICICI Prudential bought Rs 4,963.10 crore worth ITC shares in 16 block deals. It was followed by the Government of Singapore purchased shares worth Rs 3,664.11 crore in one block deal.

For more details you can refer the below articles.

Who are buyers of ITC shares in nearly Rs 17,500 crore block deals? - BusinessToday

In my view we can see a good upswing in share price in a quarter or so nearing the book closure date for Hotel business demerger. And once the business is demerged financial ratios like ROE and ROCE of ITC going to improve further as Hotel business was more capital-intensive business. that will also increase more cashflow and in turn dividends to share holders, as 85% profit is being currently shared as dividend. Even there will be additional interest of buyers for hotel business.

I feel more good days are ahead for ITC and its investors.

Disclaimer: Invested so views can be biased.

Thanks,

Deb

If you look at who they donated to (AITC and BRS), the parties don’t have any impact on taxation assuming NDA stays. I dont think we should draw a correlation between electoral bonds and tax policy of the Govt at this juncture.

Can someone explain what’s with the sudden jump in shareholding in FII? Surprisingly this is the same time ITC started experiencing a rise in stock price.

There is no sudden jump in FII.

Ownership of Tobacco manufacturers (india) limited was simply reclassified from public to FII.

| Common Size Without UAA | Mar-23 | Jun-23 | Sep-23 | Dec-23 |

|---|---|---|---|---|

| FMCG | 38% | 42% | 42% | 40% |

| Hotels | 22% | 20% | 20% | 20% |

| Agri Biz | 10% | 12% | 11% | 11% |

| Paperboards, Paper & Packaging | 24% | 22% | 21% | 22% |

| Others | 6% | 5% | 6% | 6% |

| Total | 100% | 100% | 100% | 100% |

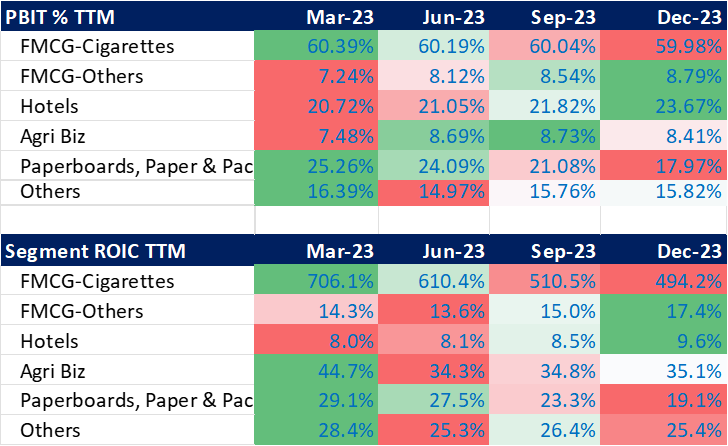

In FMCG-others segment, there is improvement in PBIT margins & ROIC.

Just making an attempt to understand the effect of demerger.

The above calculations are made using data from Segmental reporting.

Disclosure- Invested.