Yep, I’ve seen this. Do we know anymore from the management or media reports about this? I think they sell to pharma actually.

ITC to manufacture, export nicotine and nicotine salts - The Hindu BusinessLine

And on vaping products, we need to have an RRP strategy - simply because that’s better for public health in the long term - moving people from cigarettes to reduced-risk products.

There are improperly produced counterfeit products - and that’s exactly why you need regulation - the younger population is attracted to vape.

Vaping/RRP is not as simple as just government will legalise them and the next day ITC’s product will be in the market. This requires years of development, and health authority approval (read PMTA from FDA) and you need to prove that they reduce health damage to actually market them as such.

Unarguably, the most accepted RRP products are owned by Philip Morris Intl - iQOS (developed by PMI) and Zyn (through the acquisition of Swedish Match). And PMI owns 25% or so of Godfrey Philips and are co-promoters. They have these FDA-approved products. ITC has no monopoly or natural right to win in this business. Sure BAT has a solid vaping product that they could introduce through ITC and they should.

To explain how difficult is it to get a PMTA FDA-approved Reduced Risk Product and to market it as such - Altria is (reportedly) buying a small startup (with like 3% market share of vaping in the US) for something like 18x sales (like USD 2.5-3bn). Because the said startup, NJOY, has one of those PMTA/FDA approvals.

I also don’t understand why companies in India do not disclose volumes.

All global majors share volume details for all the regions they operate in.

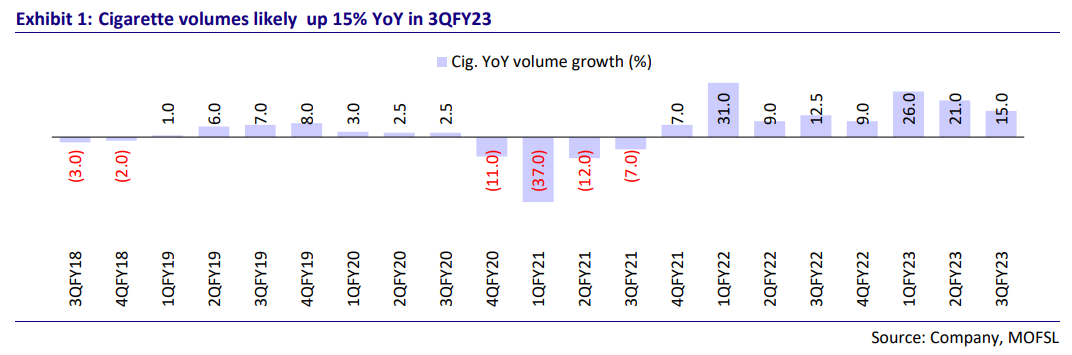

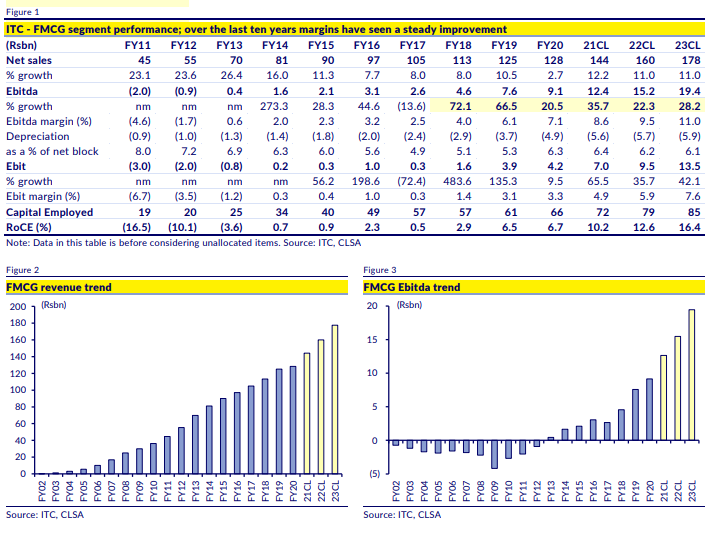

Look at the volume growth pre covid - so poor.

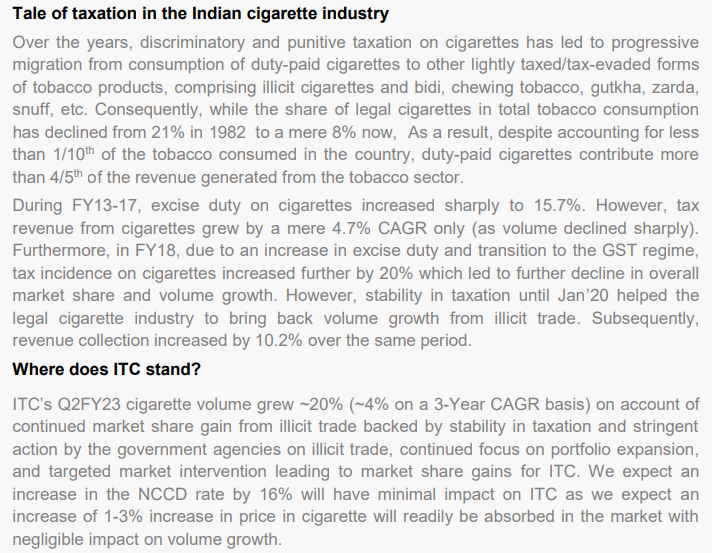

Any sustainable volume growth will come from a stable taxation regime.

Here’s an excerpt from an interesting article from 2015 (when the tax increases were fairly high - punishing volume growth)

Rather, said Syed Mahmood Ahmad, director at TII, sales of counterfeit brands and smuggled and counterfeit cigarettes had gone up as they are easily available at a cheaper rate.

“The escalating excise duty burden on legal cigarettes has almost doubled in the last four years, as a consequence of successive increases in Union budgets since 2012-13," he said.

Over the last three decades, legally manufactured cigarettes’ share of total tobacco consumption in India has declined from 21% in 1981-82 to 12%, according to the TII. During the same period, overall tobacco consumption increased by 42%.

ITC, in a statement after declaring earnings on Friday, said that high taxation had led to a significant shift in tobacco consumption to lightly taxed or tobacco products such as bidis, khaini, chewing tobacco, gutkha, and smuggled and counterfeit cigarettes that evade tax. These products currently account for more than 88% of total tobacco consumption in India at present.

“Tobacco addicts are shifting to other low-cost options, which are more dangerous, and counterfeit brands," said Jha, adding that increased use of counterfeit products resulted in losses to the government and the industry.

Meanwhile more recently, from Axis Equity Research from Feb 2023.

Now what the government should do is: (which balances health objectives and revenue objectives and really benefits all stakeholders - except the bidi/gutka employees and owners)

- Keep duty/tax increases small (which seems to be happening)

- Have a thoughtful science-backed RRP policy (not some stupidity like how they did with the sale of alcohol on the highways)

- Try to reduce growth of bidi/gutka/etc (idk how)

- Reduce illicit import/counterfeit through other restrictions.

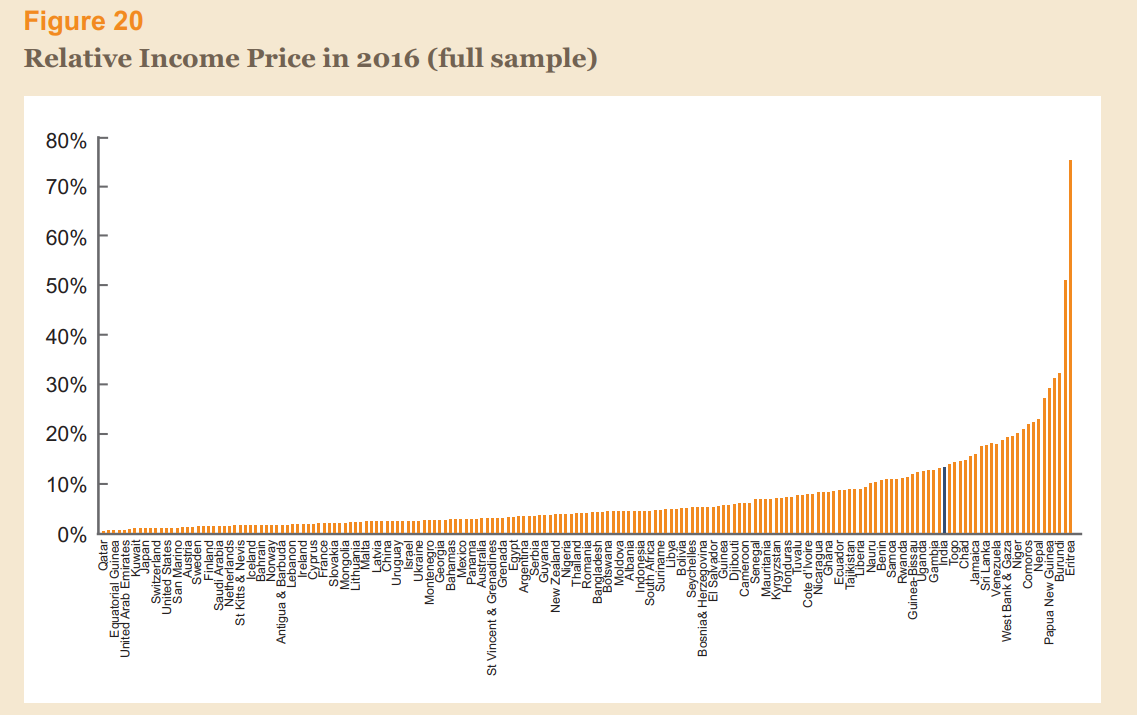

BTW, India is one of the most unaffordable places to be a cigarette smoker (so bidi rules ofcourse) - compare with countries of any substantial population.

So cigarettes are only smoked by the rich, so affordability is a lot better for that (very) small subset of the population.

To add to why investors should be pushing for an RRP strategy.

Look at PE multiples of RRP Advanced Companies (Philip Morris and (when listed) Swedish Match) and compare them to Altria, Imperial Brand, and BAT.

BAT is likely to re-rate as RRP starts to turn a profit and revenue contribution inches up.