Lets talk about cigarettes.

Background:

Main reason for market to punish and re rate ITC started happening after 2017. On July 2017 it touched 367 and in downtrend since then. ITC cigarettes volume growth has been abysmal mainly due to higher taxes. consumers shifted to illegal cigarette mainly being them so cheap.

Can ITC get back to its old growth in cigarets:

ITC management has demonstrated to Finance ministry that although they had heavily increased the taxes, it has collected lesser taxes from cigarettes than years before. Meaning illegal cigarettes market have grown multi fold and consumers also switched to that being super cheap and every one ITC + government has lost revenue.

In the recent years finance ministry seems to understood this and didn’t increase the taxes on cigarettes. And that lead to increase in volume for ITC ( of course covid re opening also played a role, no doubt). So ITC could very well get its volume growth back. ( Note: here this doesn’t mean there will be new smokers, this simply means shift towards legal cigarettes from illegal ones ).

Since ITC has improved margins, any additional revenue on cigarettes will bulk up the bottom line. OPM for cigrattes are about 60 % now.

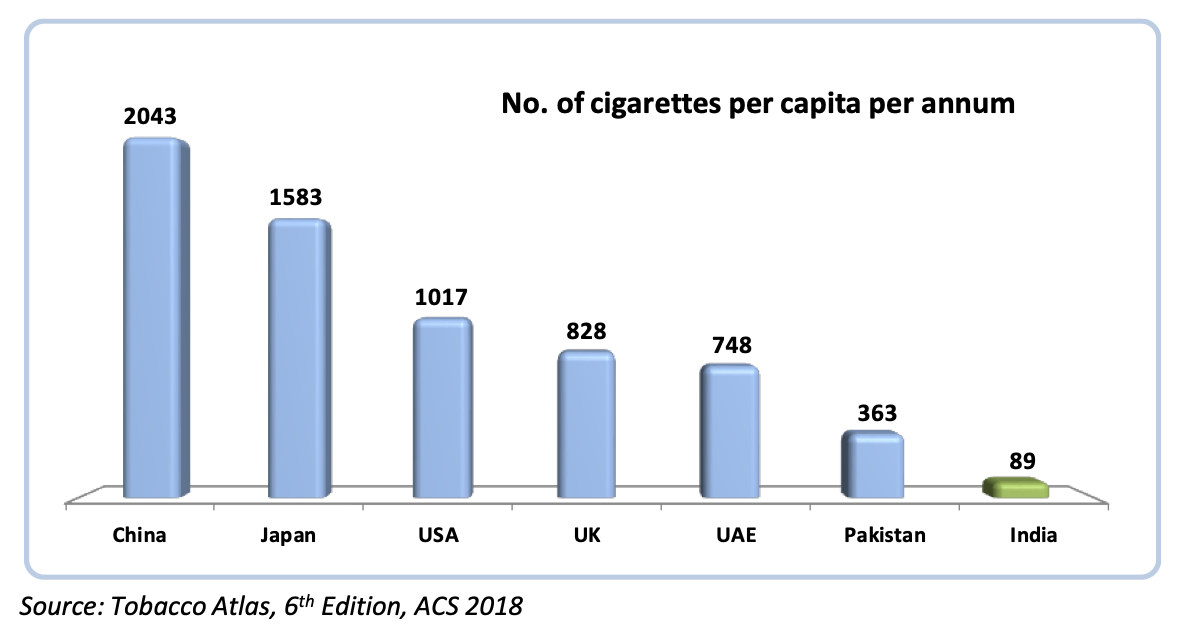

Opportunity size:

Cigarette consumption is not high compared to other countries

We have one of the youngest population in the world ( Im not batting for youth to smoke more, but many young persons smokes during college days and leave it after that ( me being one example of that)). Indian demography is such that peak population is around 16-18.

So there is enough head room to maintain the revenues.

ITC plan for Future:

ITC is always looking forward in its prospects adopting Industry 4 as well as sustainability. ITC realised that other forms of nicotine consumption are on the rise that could act as a replacement to smoking. To capture the growing demand for oral and vaping products in the US and EU markets ITC has setup ( in the process of building ) a nicotine production plant in Mysore using a new subsidiary “indi vision” in Mysuru. This is expected to put ITC as one of the manufacturers of purest nicotine in the world (stringent US and EU pharmacopoeia standards for use in pharmaceutical products). This plant will produce nicotine and nicotine salts mainly for the purpose of exporting to US and Europe markets. Hence it will also bring lots of dollar revenue.

Discl: holding same as last post. I hold a large portion hence my views are biased, please do your own due diligence before investing.