Disclaimer :- have invested in itc so can be baised.

When we see itc they have done most of there investment in there organic one but they question is what they will do with reaming cash buyback, dividend or something else.

And they have seen to do something else

You have seen they are starting to me aquire brands now and what they have is one great thing is control of supply side that most FMCG don’t have this make them may make brand that are there that are not doing good beacuse of many reason like lack of capital like savalon or even reach like mother sparsh.

They made savlon like buisness to turn from only 1 product company to be a good player in whole HYGIENE and wellness sector.

They have quickly expanded mothersparsh portfolio that is a key sign what a alredy well intergated company can do.

They lack the power to make brands like nestle and hul and even lack to quickly do operating leverage but have shown to quick act and transform company.

Just imagine if you just look at savlon being in a industry filled with many players still outshine them and if it was a simple company it could have been an easy 8-10 beggar.

So can they do that at a more rapid pace and with operating leverage,tax system being more consistent,agro opportunity been open,digital play working,transform of hotel buisness.

These all are going on together also move of illegal to legal cigrate is also can happen as economic growth start to play.

Curious which other FMCG company in the world focuses on this kind of ICMLs and what has been the prospects over long term?

Can an FMCG company focus well in both branding, distribution, marketing on one hand and ICMLs on other …or it is a better decision from the well experienced HUL to outsource these functions? What are the Tatas doing? As they are also a budding homegrown FMCG business in India? …some points to think on…insights welcome! Thanks

In the below interview, Mr. Sanjiv Puri says ITC will look to acquire Hotel Ashoka if bids are invited.

Doesn’t it contradict with what the mgmt has been saying that they wont do incremental investments in the Hotel space?

A change can happen in a minute on a personal level, on a team level, this is tough, more so when there are no vested interests.

Maybe, they cannot get over it or they are making the capex plans for the far future, or the management wants to leave a tangible mark with their tenure, and there is a connection between the food PF of the FMCG segment and the hotels.

So some allocation will always be there, with the justification that every other vertical’s requirements is taken care of, and dividends are distributed regularly, including the special dividends, if any.

Also, may be, they cannot utilize the free cash for any other ventures that fall in their circle of competence, as other requirements are fulfilled. So they have to do something, be it acquiring brands, small companies or investing more in the segments they are present in. They will grow where they are present.

Perhaps, a day will come when ITC will become another Info Edge, or maybe not, because of the way the hierarchy is shaped.

It is not just about the low downside, but it is also about the dividend yield and the stability and predictability of the businesses it is in, along with the knowledge of how management thinks or does not think, and perhaps the demergers, if and when they happen.

And depending on the AUM and the market conditions, MFs reduce or increase their allocation to ITC, or for any such stable and predictable business.

On a personal note, I guess ITC is as a restraint all the time, more so in a bull market, if one has allocated more, and brings solace at the appropriate time, when things don’t work out.

And obviously, investing in a single stock and taking exposure to it through a MF or ETF are not the same, even if they are sectoral funds, and the stock has high allocation in the funds’ PF.

ITC does have an IT company as well named “ITC Infotech” which is doing well from what I see in news articles . Though its not an IT Giant like TCS or infosys it is growing gradually well .

A mid tier IT company which is doing well might be a good sign for ITC on how it is diversifying its business away from Tobacco . But ITC infotech is not really listed under ITC’s balance sheet , Im confused whether they brand it as a separate business or part of ITC .

Good point but we need to see how big the deal will be and it is a single hotel and also in one of the prime location that is very hard to get and also is very near there very popular mayur hotel so if they can get at good price and make a singergy then can earn good and be a good investment.

The question will not be will they build or buy new hotels but about how much Money they will invest as if it small then it can be beneficial as it will help there cold food buisness that is growing rapidly and also is gaining great traction.

Also to add a point this place is very easy profit ground and looking most don’t have money to even bid so can get for good value and even if we look at tata it would be hard for them to invest that easily as itc can do as there main company is listed while there company is fully own and can put money easily.

not averse to the idea of demerger of the conglomerate’s fast moving consumer goods (FMCG) business.

Open to the idea of listing the company’s information technology (IT) businesses — ITC Infotech

The company has also not shelved demerger plans for the hotel business.

Over the last four years, our revenue from the FMCG business has increased from Rs 10,500 to Rs 15,000 crore with several of ITC’s FMCG brands having already achieved leadership positions.

Old Verticals

ITC FMCG

ITC Paperboard

ITC Hotels - Welcome Hotel

ITC Infotech will have sharper focus on Automation, Cloud-based Services, Digital Banking, Smart Manufacturing and Digital Workplace

ITC E-Choupal

New Verticals

ITC-MAARS — Metamarket for Advanced Agriculture and Rural Services.

ITC Hotels - Asset right - New Brands like Storii, Mementos, innovative staycation packages and in-home dining offerings such as ‘Gourmet Couch’ and ‘Flavours’.

The vision looks good but the market is not quite impressed with the associated actions and ITC is still hovering around the same levels for quite sometimes while other FMCG companies have gone up significantly. The major trigger should be M&A on the FMCG space and demerger of IT and hotel business to make it a pure FMCG player. Only time will tell if BT will allow this.

The valuations are a problem as ITC is not able to grow FMCG, IT or agri verticals fast enough to overthrow Tobacco as biggest cash generator which is a huge task. This won’t happen in a quarter or a year.

A demerger is a short term solution for traders. Long term investors should focus on why none of these verticals have overtaken Tobacco even when tobacco is facing so many headwinds.

I want to see a demerger too but not one that is hurried because there was so much noise that half baked companies got listed. I have held this same stance in previous posts also. Let FMCG and IT be self sustainable and overtake tobacco first. That shoud be the criteria for demerger.

Officially ITC is 100% publicly owned i.e., there is no promoter. BAT subsidiaries together hold about 29% stake in ITC.

They have nominated 2 directors to a board which has 16 directors.

One wonders whether BAT as erstwhile promoter:

a) is seriously interested in businesses other than tobacco

b) while treating ITC as associate/investment, driving the management hard to enhance shareholder value.

IMHO, until these are answered in the affirmative, the share price is likely to languish.

Following is an extract BAT annual report 2020, indicating where ITC stands in BAT scheme of things.

**Cash flows from FMCG or paperboards are not going to beat the tobacco business **

The cash flows from FMCG or paperboards are not going to beat the tobacco business ever ( unless tobacco is completely banned in India which is improbable) The management is overwhelmed with the cash inflows from tobacco. They are trying to reinvest it but they have not been successful in beating those returns. No wonder BAT will be unimpressed with these ventures.

If BAT owns roughly 30% which is nearly 1/3 rd of the ITC, they should be having 3 directors representing them instead of 2. They seem to be under represented. Out of the total number of directors there are 7 independent directors.

BAT, the major shareholder is obviously not the controlling shareholder. So it is easy to infer that BAT needs approval of some other directors as well to have a say in the operations or reinvestment. Looks like the majority in the board of directors vouch for reinvesting in new ventures like asset light hotels and demerger of Infotech.

There are directors on the board who are passionate about Hospitality, Hotels and Hoteliering . They obviously have their agendas on the table even though returns have been comparatively poorer. Now the management is doing " strategic reset with asset light model". It basically means the previous investments in hotels have not paid off for the shareholders.

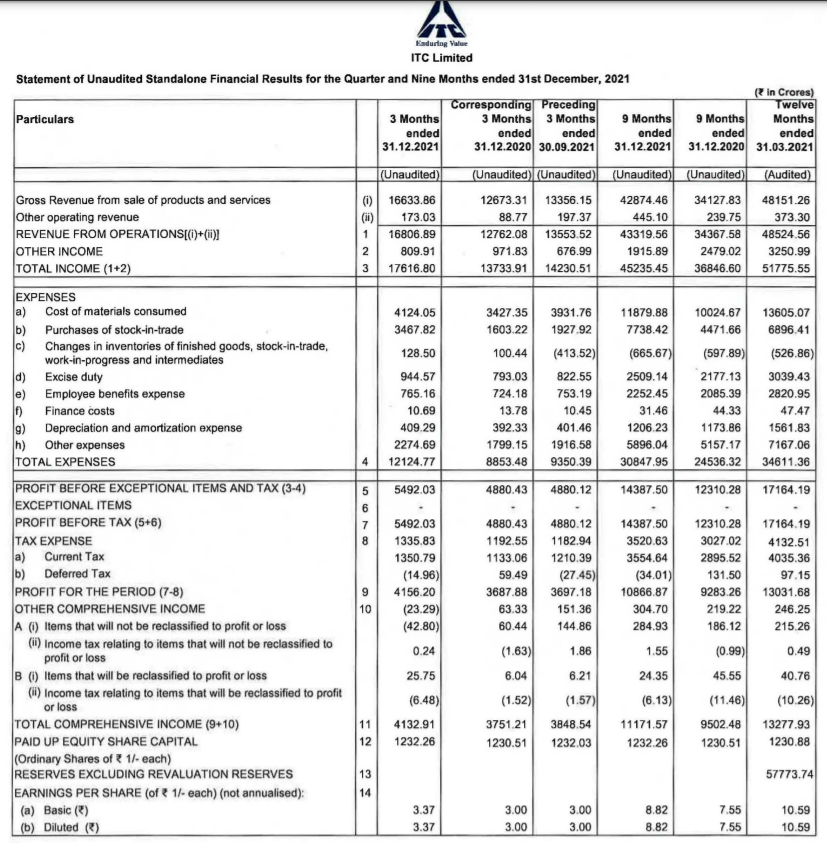

From what i have seen, the profits reported has exceeded pre pandemic levels and seems to be the highest ever for a single quarter. See the results here and the investor presentation here..

Per the press release, Gross Revenue is at Rs. 16,633.86 crores representing a growth of 31.3% y-o-y while EBITDA at Rs. 5102.10 crores grew by 18.2% y-o-y. PAT grew by 12.7% y-o-y to Rs. 4,156.20 crores.

Two very interesting observations from the presentation:

The project for the state-of-the-art facility to manufacture and export Nicotine & Nicotine derivative products being set up by the Company’s wholly owned subsidiary, ITC IndiVision Limited, is progressing as per schedule. The facility is being geared to manufacture purest nicotine derivatives conforming to US and EU pharmacopoeia standards.

Construction of the manufacturing facility at Guntur for value-added spices is also progressing well. The Business seeks to significantly scale up its presence in food safe export markets leveraging this world-class facility and its identity-preserved sourcing expertise, custody of supply chain and strong customer relationships.

Paper board and packaging division seems to be doing really well and i believe this is a potential divestment candidate. The quarterly revenue for this segment is now exceeding 2K Crore with PBT at 448 Crore which translates to nearly 21% margins. These are industry leading numbers - a much smaller player EPL(Formerly Essar Propack) clocks a quarterly revenue revenue less than 900 Crore and PBT in the range of 70 to 100 Crore trades at a market cap of 6K Crore.

ITC Infotech also seems to be growing well with YTD revenue up by 21% YoY to 2,181 crore with PBT margin at 27.6% and PAT at nearly 21%.