Investors and Financial analysts Day ppt link -

3 Likes

In case you want to hear the investor day here is link from youtube.

I am surprised as why ITC has not published it on their web site (or youtube)

2 Likes

It seems that the stock market has not appreciated this effort taken by the management. This is reflected in the ITC stock price which is trading at the 2013 price. The dividends are good and hopefully things may improve from here on.

I just like what @Aniesh7 post says, ITC would be valued higher if it doesn’t do anything thing. Investing activity should be stopped and money should be given as dividends.

Disclosure: Holding

1 Like

Look at the return ratios. They are consistently declining. Poor capital allocation and liberal ESOP is hurting ITC stock price.

ITC management should exit from capital intensive business like paper and hotels and return the excess capital to shareholders.

2 Likes

paper and packaging business are highly profitable, they should not do that

ITC and HUL are in the same boat with respect to Sales Growth. ITC lags HUL in profit growth. HUL has awesome return on equity when compared to ITC. HUL’s PE is 63 where as ITC’s PE is 18.7.

ITC is looks cheaper to HUL in terms of Price to Earnings and Price to Book. I am wishfully thinking that ITC would rerate to at least half of what HUL is valued.

HUL

ITC

Pain points which a shareholder has to suffer

- BAT is a major shareholder with very little control over capital allocation. They seem helpless but they can enjoy the dividends. The minority shareholder is in the same boat as BAT. Normally shareholders are the true owners of the company.

- The allocations of the enormous cash flow generated in Cigarettes is pumped into ventures which has long gestation period. Till now the management has been able to provide hope. We might not know when their effort would reflect in the bottom line. It depends on the individual share holder whether to stay with the company or sell out. These are testing times.

- I think definitely that the returns from other ventures cannot match the returns from the cigarettes in which ITC is a market leader.

- The ESOP’s are immediately sold off and the shareholding is getting diluted every year. There is no possibility of buyback.

- Hotel industry is like the airplane industry which is capital intensive, historically generating poor return for the investor.

- Now ITC management is trying Asset light model in hotels which might be better than the previous model. They keep trying new business models to generate profits for the shareholders. They have the power to return or reinvest with the boards permission.

Possibilities in the future

- The Market could reward businesses with good economics even when the management allocates capital in lower return business.

- The dividend payout which is already good can be increased further.

- FMCG business model’s of ITC becomes successful and the company’s stock price rerates.

- The management stops selling ESOP’s and start becoming owners ( Skin in the game)

- Sell off the least performing businesses so that they don’t consume more cash.

It would be awesome. I can hold on to my ITC shares with these hopes. I wish the only mistake they shouldn’t make is to kill the goose that lays the golden eggs.

Disclosure: Holding long term - both ITC and HUL

7 Likes

Interesting Points: . I would like add to some points raised by you

Pain Points :

-

BAT is active shareholder : but one needs to understand they too are facing similar challenges at parent company level . For them the situation is worse as they have followed Aswath Damodaran advice and still share price has declined by 40% against ITC share price decline of 10% over last 5 years … Mind you BAT gives 7.8% Dividend in Pounds where bonds are giving near 0% interest rate . Shareholders see higher terminal risk in BAT vs ITC …

-

Cig business has dream industry structure . but built over 100 of years … Great FMCG years takes multiple decades to built and hence Moats are strong as patience to build is high .

-

ESOP was a pain point . They have reduced the quantum dramatically . This got addressed in 2019

-

Hotel industry is cap intensive - which made great sense when Corp Taxation was 40%+ … Look at businesses around . why they buy depreciating assets like cars in March … ITC had enormous adv vis a vis Indian Hotels etc as it could built hotels at 40% less cost just on basis of taxation

Possibilities in Future

- Optionalities are great possibilities - ITC is where Reliance was in 2016 …

- FMCG business has large headroom , but b2b business too has headroom … as industry structure in these business have become attractive post consolidation

- Agreed they need to sell least performing business . Lifestyle Retail was good exit .Now low end soaps is another good exit

9 Likes

Agree to most of your points but just a thought - In case of RIL, it had super normal growth businesses incubating in terms of Jio - The largest digital platform in country and Retail - One of highest growth businesses. Not to mention huge ecommerce play as well.

Compared to that ITC has - FMCG & now we are hearing IT services incubating.

This makes RIL position back in 2016 much stronger…although it was much bigger in size also back then and petrochemicals is not exactly a dying or stagnant industry as well.

Disc: Invested hence critical. Not a buy/sell recommendation. Above views only for academic purposes and I can be completely wrong in all my assessments

2 Likes

In case of RIL - Oil was an industry in decline . look at what activist investors have done to BP, Shell etc . RIL has managed crisis far better as it did not stick to core and distributed money as dividends , but created new avenues of growth … Same is true for Tata , It started with Textile , then moved to steel then auto to IT … Indian companies are good at shifting talent pools to new profit pools

The degree of success depends upon management capability . That said RIL has excellent way of policy management … which few managements can do … Plus stability at top helped .

ITC messed up in initial stage of transformation by having tobacco executives managing new age business … The biggest takeaways in last 3/5 odd years is this realisation and now we have ex Marico star manager heading Personal care , Ex infosy man managing IT , even in tobacco they got a star manager from VST to improve hit rate in low end Cig brands . These are big shifts …

That said FMCG unlike Retail / telecom is high moat business and hence shifts are very slow and difficult . It takes generation to grow but stickness is high unlike Retail and telecom where low price can shift consumer base,

8 Likes

Infoedge or other tech companies invest in companies that they understand . similarly FMCG companies invest in companies they understand.

ITC had invested in new start ups like Sparsh ,Delectable Technologies Pvt Ltd | VCCircle , in past in distressed hotel assets like EIH and Leela etc + I think they have some interest in agri and tobacco startups . Plus it has large real estate assets - for strategic reasons

ITC is much conservative investor now as it had burned its fingers in 1990s by playing aggressively in financial services business which had just opened up …

3 Likes

3 Likes

3 Likes

This is something interesting development in my view. While it is too early to come to conclusion, but definitely correct thought from management on this. One more perspective is ITC effort to launch plant derived meat from peas rather than other prevalent ways. Good news to start 2022. ITC to launch plant-based meat products - The Economic Times

6 Likes

We don’t know how much these kind of products contribute to the bottom line. I don’t know about the breakup of revenue except for the ranking of staples. If the contribution is not meaningful, no matter the ease of procurement, manufacturing and packing, these kind of products will just be there in the PF.

Also, price is an important factor. It is not enough that these taste like meat, they fulfill the craving but the price has to be affordable too. Otherwise the market will remain small unlike cigarettes. Exporting will happen like the ready to eat meat products of ITC but being pricey limits the growth. Moreover, for meat products, the price is at least justified to some extent, given the quality and taste they deliver. But for plant based meat which is pricey, I am not sure.

Food trends take years to pan out, even if they do. Moreover these are highly personal choices. To overcome food craving thinking of something could happen after 10 or 20 years is difficult for many people. Smoking is different. The trends that grow in other geographies, need not happen at the same level in India unless the very supply diminishes, or the government takes a clear cut decision. Otherwise the trend will be a fad. The first mover advantage does not mean anything, if a particular information takes years to reach, and even when it does, if the beneficial decision is a hard choice to make.

I have no complaints or surprises regarding the launch of such products, it is just that, this FMCG/food race is a long one.

Just my thoughts and yes invested.

8 Likes

A member send me following question in private message on which I shared my thoughts. It may be useful on this thread and hence posting both the messages.

First message:

Hello Dhiraj ji,

Let me start off by saying that I have rarely seen anybody respond with as much humility and courtesy as you do, even to strangers! Thank you ![]()

I have two question regarding ITC.

-

Your thoughts on ITC’s FMCG products’ continued lack of availability, high sounding, jargon filled communication and obsession with new launches while neglecting existing products. Many ITC products continue to be available only in the annual report or website and inspite of many shareholders communicating this, I have not seen the management address this point ever. To me, the ITC management appears very similar to typical government officials and politicians with lots of nice sounding, non specific talk but actions mainly limited to protecting their turf and showing complete disregard for the common man (common shareholders).

-

Since cigarettes are going to be the major part of profits of the company for the next decade, isn’t it better to buy godfrey or vst since if cigarettes don’t do well, ITC profits won’t rise much and if cigarettes do well, godfrey and vst would benefit more compared to ITC.

Thanks

Thanks for your kind appreciation.

My Reply:

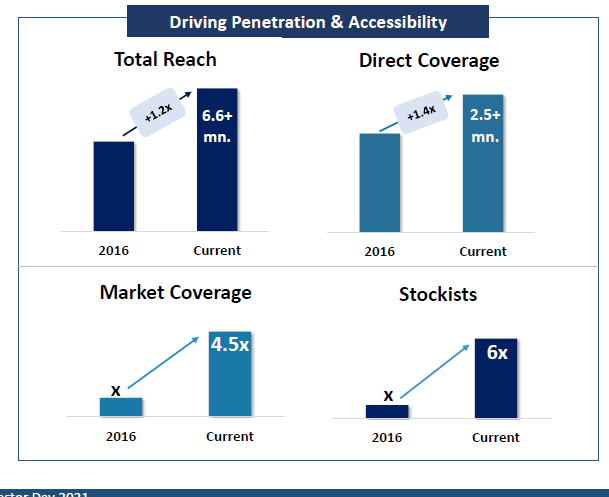

On first question, I agree with you about non-availability of products and other issue about over promising and under delivering by the management. That is the reason why market is giving PE of 18-20 vis other FMCG PE of 70-80 times. I also agree your viewpoint of absolute power with limited accountability. However, one aspect where ITC management differ from Govt officer is ESOP. They have skin in the game. Most of top management would have significant portion of free personal wealth tied in ITC ESOP. Hence, they also would be concerned for equity value in my view. Further, while we can definitely say management has not upto best class, despite such management, we see 3 brands developed in last 15 years and giving sales value of Rs 5000 Cr+ in Indian market. Neither HUL nor Nestle has reached such milestone in my opinion. Having said that, HUL/Nestle already have their own good brands and hence more focus on narturing their growth then developing new brand. But it is quite achievement to reach on scale from nil in 2005. The distribution reach of 6.5 million outlet. Refer to slide 47 in investor day presentation in 14Dec2021. Enclosing extract of same

In summary, all issues raised from your side deserve attention. However, the way I look at whether same is discounted in prices. I feel yes, but would know whether I am correct or wrong only after 5-6 years. If I am wrong, there is significant opportunity cost which I would bear. Hence, I would suggest you to please look at your risk profile, aspiration, time horizon and conviction and than take any decision.

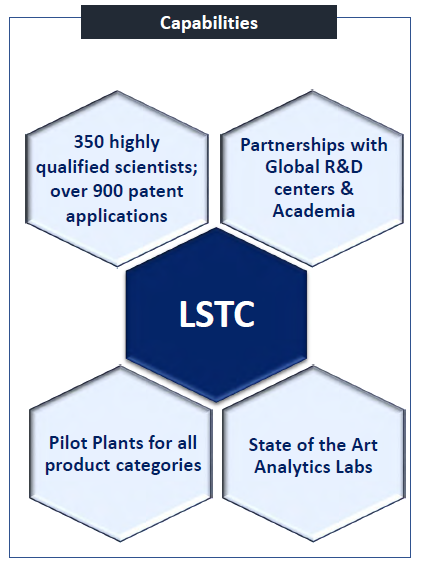

One more factor which really raise my hope is focus on innovation. Since they did not have any parent to source brand, they have done real work on developing products. While ITC management may have issue about distribution, but whatever product they market, that has the best quality among the peer. In the investor day presentation, while highlighting innovation, management did say that they are among second largest patent holder in Non-PSU/IT/Pharma segment among all corporate. While what is benefit of such reseach and whether it is useful or not, only time will tell. But at least during COVID time, they have many firsts to their credit in Savlon related range of products.

Referring slide 201 from investor presentation providing details of Savlon exension launches during COVID time. On lighter note, even ITC has now started using word platfrom ![]() Being born Mumbaikar, only platform I am familiar is one on which local trains(life line of Mumbai) arrives.

Being born Mumbaikar, only platform I am familiar is one on which local trains(life line of Mumbai) arrives.

On second point, I feel (and may be wrong), the de merger of ITC is question of when then why. It is whether in 2 years or 10 years, I do not know. If that being case, I would be happy to hold ITC then second and third player. I sold VST Industries after holding for more than decade in August 2021 and hence my view may be biased. You please do your work on same

Apology for long reply.

Disclosure: Among my Top3 Holding, Not A SEBI Registered advisor, Not recommending any investment action, my view may be biased due to my holding.

26 Likes

Major Shareholder is not running the business

The top management does not have considerable stake in ITC. In fact the major shareholder, BAT has rightly opposed to give ESOP’s to the management as it would dilute its 30% stake in the firm. Hence in my view they do no have SKIN IN THE GAME. On the other hand the majority shareholder who has SKIN IN THE GAME is BAT. But they are not part of the management. This may be one of the reason ITC trades at low PE.

Reference:

ITC, which followed a mix of salary and ESOPs (employee stock option scheme) as remuneration structure, had to change it after British American Tobacco (BAT), a shareholder in the company, opposed it in 2018 to prevent dilution of its shareholding.

Source: ITC CMD Sanjiv Puri's pay jumps 47% in FY21 - BusinessToday

Poor Capital Allocation

The management has not been able to generate the same profit margins which they get from Cigarettes. They have invested in Paper, Notebooks, Hotels, FMCG and Technology. All these generate far less returns when compared to Cigarettes. The reinvestment of capital has not been beneficial to the existing shareholders both the major shareholder and the minor shareholders.

** ITC is in a conundrum, where its best option would be to BUYBACK its stocks instead of di-worsifying to lesser margin generating ventures**

Reference:

The term “diworsification” was coined by legendary investor Peter Lynch in his book, One up on Wall Street, to describe the over-expansion of a company into new growth projects and businesses they do not fully understand and which do not align with the company’s core competencies.

Disclosure: Holding

8 Likes

Thanks for providing counter view point. Appreciate your comments.

Find enclosed my view on your comments

BAT not having management control

ITC is not a newly listed company. During 1990s/2000s/2010s also BAT did not had control over business operation of the ITC and the company has created great wealth over that period. Even during that period, management was allocating capital not in the most efficient way (with diworsification in NBFC business in 1990s) and also faced criminal charges (due to Chitalia scam for export fraud and fight between KL Chugh and BAT for management control). Hence, in my view, as compared with 1990s and early 2000s, the situation has relatively better in context of alignment of management and shareholder interest.

Poor Capital allocation

I accept that capital allocation for the ITC is not the best for shareholder. However, now with management indicating limited capex in Hotel business and also increased Dividend payout to 80-85% of net profit, I see things may improve. As indicated, management has increased payout since April 2020. While much need to done on that front, I feel ITC has scope to improve on such lower base.

Find enclosed interesting link from 2010 ET article when Probably most competent professionally management in India also faced issue due to under performance. During that period, ITC was appearing relatively better, despite inferior Capital allocation and limited alignment of shareholder and manager interest.

18 Likes

Just few cents here. Everyone complains that ITC products are not visible in the stores. Despite that they are generating a revenue clocking 15-16 K Cr. Imagine once they capture shelf space in stores. I completely agree to then point that they need to concentrate on proper distribution channels. Company is said to be working on distribution for last couple of years. There is also a conflict between distributors and online stores ( for all FMCG cos ). I hope there is some clarity soon on this.

Market is not giving bigger multiples mainly because of FMCG margin. I also dont see that suddenly jumping to 20’s soon. I have written here a year ago how HUL’s margin developed during 90’s. It is in HUL forum ( back then ITC page didnt exist ).

In 1992 HUL had a margin of 6% ( Taken from Annual report of 2001).

I couldn’t find older Annual report older than 2001 HUL. so I couldn’t see how was their margins before. Margin expansion for ITC mainly will come from ICMLs.

They are strategically located close to agri procurements and automates the production hence bringing the cost down. HUL for example outsource these and some argue that thats why they have higher margin, but since I dont have any numbers for ITC, so I cant comment on that. Capex that ITC announced on FMCG is going to building these facilities. I believe FMCG margins will slowly increase in the coming years and dont expect a big leap anytime soon. It will be gradual but steady.

When will market notice such a development and reward by giving higher multiples, thats not in our control.

10 Likes