I would suggest once again, all members to please control their emotions. Also, Savlon whether it succeed or not, may have very minor imact on total financial of ITC. What ITC need mutiple brand to work for it in my opinion. Secondly, how critical you feel your feedback of product is on ITC valuation in future? In my opinion, my view on ITC products, while may improve my conviction to buy and hold share, it would hardly move needle for ITC wealth creation perspective. It would need million of Dhiraj Dave to share similar thoughts and like products. Hence, would suggest members not to provide view on products as it would clutter the thread in my opniion. My apology if I hurt any members sentiment in advance.

31 Likes

Some things in right direction for ITC

$MO (Altria) has beaten S&P500 on a total return basis this decade even after falling nearly 40% from its decade high in 2017.

It is also the best industry in American history in terms of performance on a total return basis. Most of its returns came from dividends than from the stock price appreciation.

This is a nice take from Cliff:

“Tobacco stocks work b/c many conscientious investors hate them and keep their valuations down, thus boosting returns. There’s another subtlety here. It’s not a contradiction to be cheap forever and do well. Many think the only way to make money from cheapness is getting more expensive. But long term cheapness means long term buying cheaper cash flows. You make your money slowly but forever.”

11 Likes

CLSA on ITC

3 Likes

If anyone has the full report, could they please post a google drive link to the same?

1 Like

ITC CLSA Report, October 2020 - Highlights:

-

ITC’s FMCG business among most diversified in India.

-

ITC Targets: 220 (base), 255 (blue sky), and 140 (rainy day)

-

ITC not focusing on profits but on building capabilities and revenue in FMCG space. FMCG business is perfectly positioned to drive profitability. EBITDA margin for FMCG estimated to grow at 30% CAGR for next 3 years.

-

Nimyle, acquired two years back, has seen CAGR of 100%

-

ITC cash & cash equivalents stand at around 16% of market cap.

-

Dividend payout likely to increase in future thanks to cash+liquidity

-

Upgrading to BUY because we believe market is ignoring long-term positives.

-

Cigarette business cash flow remains steady

-

Other consumer staples with a confirmed BUY call include: HUL, Dabur, and Emami

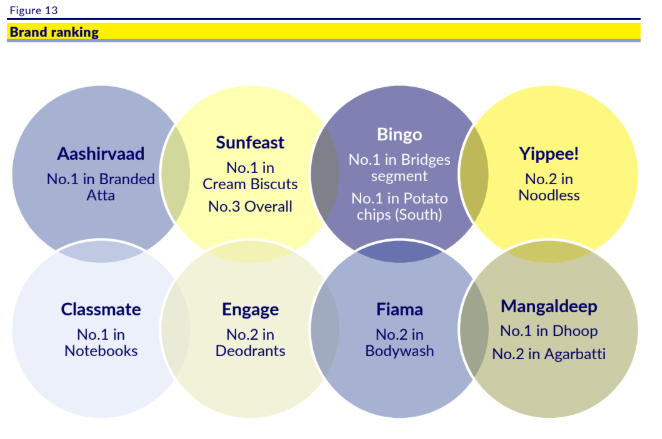

Brand ranking for various ITC brands, remember ITC entered FMCG business in 2000 only:

FULL CASE STUDY:

5 Likes

Latest CNBC interview (link)

- FMCG business:

o Staples doing well and growing over pre-covid level (discretionary is still below pre-covid)

o 41 new launches

o Education and stationary has suffered because schools are closed

o Margins have expanded by 130 bps this quarter

o 25 mother brands with consumer spends of 20’000 cr. (capital expenditure has been 1.6-1.7x of revenues; would have to pay ~4x revenues if went through inorganic route); the market size of these 25 brands is ~200’000 cr. (so blended market share of ~10%) - Capital allocation:

o Will focus on asset light (i.e. management) model for hotels

o Will return 80-85% profits as dividend

o Demerger and buyback: Board will discuss these

Disclosure: Invested (position size here)

7 Likes

ITC’s Sanjiv Puri said shareholder value is top priority, adding that he was ‘surprised’ by the stock price underperformance

ITC management trying to increase the stockholder value in various ways.

So we can wait for some year time to get good returns…

These sort of management acts makes one skeptical of this stock as an investment. Too much focus on share price rather than the businesses. If shareholder value creation is there top priority and as per there admission they’re investing in some businesses(FMCG) for that, then why is relatively short term under-performance bothering them.

Another interesting point is thr so-called alignment for going asset-light in hotel business. Why is a lull return in share price driving business decisions; shouldn’t the course of action be otherwise? If this statement would have come post hotel re-structuring, it would still have been okay.

I’m invested in this co. but jst trying to assess mgmt intentions and motivation here.

7 Likes

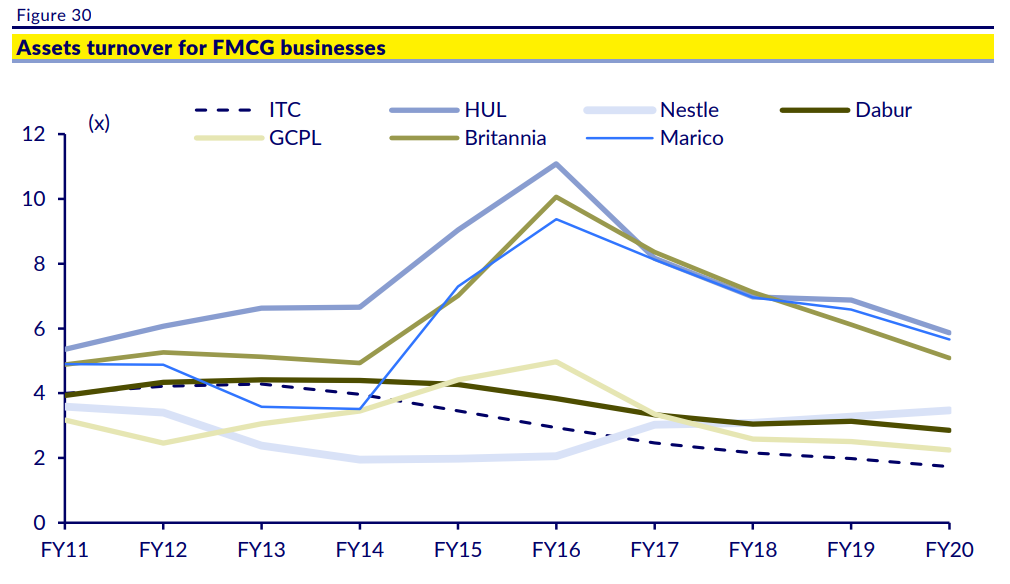

Asset turnover is worst in the industry mainly because of investments in ICML and in house manufacturing. They need some serious amount of sales to justify the fixed assets in place. But once sales scale up and all icml facilities are used to 100% it can seriously help in getting good profit margin. CLSA report points out example of Brittania who expanded margins using in house manufacturing.

1 Like

Shereen Bahn of CNBC tv-18 tried to dig out the underperformance of the stock several times but was left frustrated each time by Mr. Sanjeev Puri. (Never seen her this way before though).

4 Likes

There is lot of fuss around valuation of ITC, some even argue that it’s not possible to evaluate this business.

Points I considered while studying ITC:

Revenue Growth: we clearly see sales growth has been poor in last 5 years at around ~5%. However, in the past it used to grow at faster pace and in future growth can come back.

Margins: Margins have been above 30% since beginning and they continue to be that way even today.

Debt: Company has no debt. In fact they have big cash reserves, assets and hefty investments.

Cash Flow: Company is generating positive cash flow and despite all the issues with taxes and government regulations , it is generating more cash every year.

ROE/ROCE: 25% / 32%, I believe these are good numbers.

Dividend Yield: 6% This is good too.

So on paper nothing much to complain about. But there are some concerns like,

Mis-allocation of funds by Management: Yes, ITC diversified into Hotels and its capital intensive business. And with pandemic, this business has got its backbone broken. Investments made here are not paying of, instead incurring losses.

Still they are assets and pandemic is not here forever. These assets might generate revenue in future or land and infra can be used for other profit making activities.

Government regulations and taxes: Another big worry is government. Not only for ITC for everyone. You never know when and what it will do to the companies or the citizens

What we have seen till now is greed to squeeze more out of alcohol and tobacco has resulted in revenue loss for both government and companies. I didn’t check the ground reality here but smuggling is said to be rampant and its affecting government as well as businesses. I think government cannot just keep on creating even more disparity by the way of taxes where businesses start shrinking and illegal operations start growing in the country. Government will realize this sooner or later and things will change.

My take: Business is doing good and even though slowly, it is growing. Margins on consolidated level are good. Cash rich and asset rich company such as ITC can act boldly when opportunity presents. At current multiple of 13-14, valuations look very attractive, even with the concerns mentioned above.

There are many ifs and buts that need to go ITC’s way for it to start its growth engine once again. Negativity has been factored in and even from just dividend perspective one can make some space in the portfolio for ITC.

Please add other perspectives that anyone thinks I failed to consider and matters for the current and future price performance of this stock.

10 Likes

There is a solid reason for low valuation than other tobacco peers. They do not have an opportunity to misallocate, mismanage and sudden acquisition or decisions which may not be in long term investors favour. Not saying that ITC would do that, but they have this opportunity and history not with them so far. They need to show change with solid to the point decisions and not just talk.

Disc. Invested hence biased.

PPFAS view on ITC

5 Likes

I did a similar calculation a few months ago, but in reverse. What I was essentially trying to do is figure out at what price are the other businesses available for free.

I looked at what price is ITC trading at and compared it with its cig peers. It was trading at a marginal premium. I used difference that to look at the other businesses. (Please do let me know if I’ve made a mistake in calculations/approach)

"A quick back of the envelope calculation is presented below:

The above calculations are for FY20 and at a PBT level to ensure consistency.

ITC investments and cash

ITC presently has a market cap of Rs. 2.42 Lakh crores. With a segment level profit in the cigarette business of Rs. 15.83K crores, ITC is trading at a valuation of 15.29. The listed space of the cigarette industry is made up of two more main players – VST industries and Godfrey Phillips. The average of the two comes up to 11.135. So ITC is trading at 37% above the industry average PE on a PBT level.

If one were to consider their investments and cash without any discount (i.e. subtract them from the market cap and consider them at their reported value), ITC trades at a PE, 44% above the industry average.

ITC Valuation carrier forward

Based on the above table, ITC does seem to have room for the other businesses as well in its valuation. The valuation for the other businesses does seem relatively well priced at a PE of 21.9. Improvement in margins will trigger an expansion in earnings. That’s the main thing to watch for…

ITC Revenue, Profit, PBT Margin and Revenue Growth

In summary, ITC is a potential Dhandho opportunity to keep an eye out for but at the current price, it may not be as good as people think it to be. What level would cause it to be Dhandho? At a market cap of Rs. 1.76 lakh crores. That translates into a share price of 143. That’s when the other businesses would be free. "

There could be a scenario where the other businesses could be available for free (based on FY20 earnings of course. Using FY21 is a bit tricky).

7 Likes

I was going to put up a long post but the response from PPFAS is concise and direct.

Investors need to stop complaining about capital allocation to hotel business. Management has already declared their intention to not put in more capital. Itc has excellent properties. All it needs now is better brand building like Taj, Oberoi, Hyatt or Leela. A brand which you would want to declare to the world on Instagram and Facebook. People in my city don’t even know where ITC hotels are located. That’s a pretty lethargic job done on marketing and brand building.

Unless cigarettes sales improve, ITC underperformance will continue, till the time Fmcg takes over as the largest revenue generator.

1 Like

Very intrsting update :

1 Like

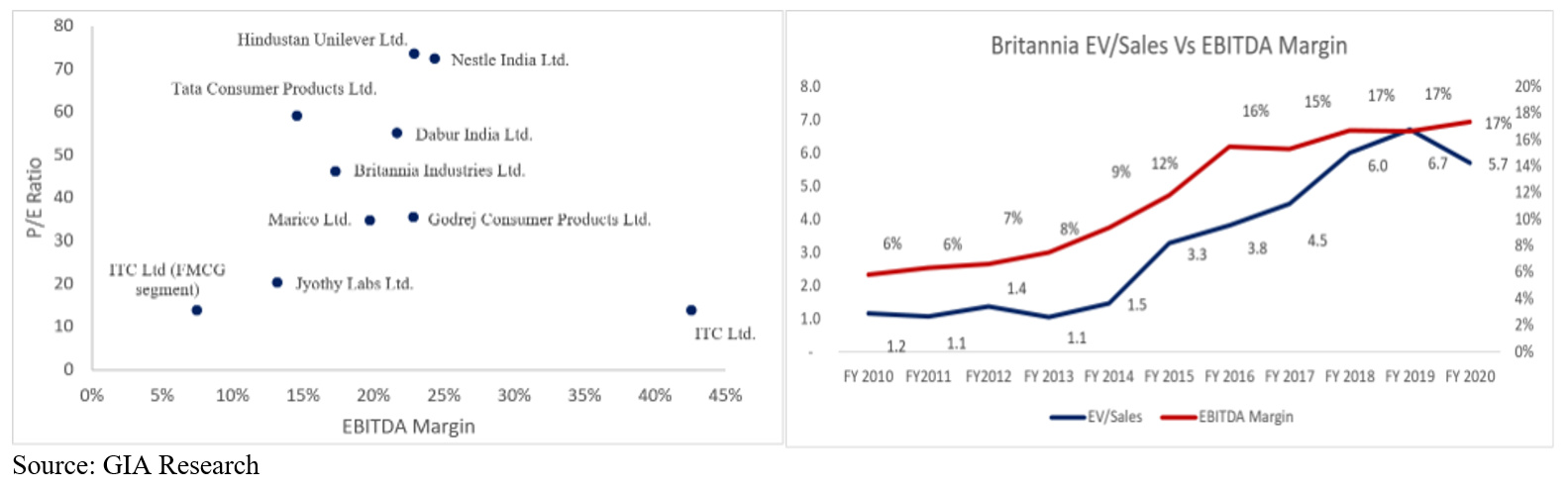

Did some work on ITC, clearly the de-rating seems to have run it’s course and most investors agree that it is cheap. However the key question is what will lead to re-rating of ITC. According to our analysis, the most important variable to monitor is the EBITDA margin of it’s FMCG business. As ITC improves it’s FMCG’s operating margins, the stock will re-rate sharply. Same happened with Britannia. Have a look.

Source:ITC (Is This Cheap?)

9 Likes

Marriott and ITC hotels are having some kind of franchisee relationship . So ITC hotels have access to largest loyalty customer base (Marriott Bonvoy) which could be a good thing.