Loose cigarettes sell ban in Maharashtra…

3 possible scenarios for ITC over next 5 years:

A. Cigarette revenues / EBITDA will fall, FMCG revenues/ EBITDA doesn’t grow.

B. Cigarette revenues/ EBITDA may fall, FMCG revenues/ EBITDA grows.

C. Cigarette revenues/ EBITDA will grow, FMCG revenues/ EBITDA grows.

Out of the 3 scenarios, scenario C is not really likely, given the continuous drop in cigarette revenues in last few years and no turnaround expected. Similarly in scenario A, no growth in FMCG revenues too is highly unlikely given the market dynamics. ITC has pledged lot of resources to ensure that FMCG grows to replace the drop in cigarette revenues. Hence, scenario B is the most likely to happen. But the key point to ponder here is : can FMCG EBITDA grow at sufficient pace to replace the fall in cigarette profits. That’s what will determine the future valuation of the Company.

Even though the FMCG margins are growing, they aren’t high enough to replace loss of cigarette revenue. There may well be a time somewhere in future when the cigarette revenues show a large drop even while FMCG margins are not growing fast enough. This is really going to be the key test both for the management and investors.

5 Likes

Any thoughts on impact of this on ITC? pls correct me if wrong, loose cigarettes generated taxes as sale is captured for the packet. So from taxation point, nothing changes. From share of unorganised sector, any idea on ratio of organized and black/unorganized in loose cigarettes category?

From consumer behavioral standpoint, various scenarios possible.

2 Likes

Not necessarily… a person who smokes will get his cigarettes irrespective of whether ban is implemented or not… on the contrary, they will buy a packet instead of buying loose cigarettes… sales volume may infact go up… also the large players have already started 5-piece packs to take care of this

3 Likes

Hi,

ITC following the others in the Hospitality segment likes of home delivery of food.

Additionally they are going for laundry services.

Thanks,

Deb

1 Like

https://www.itcportal.com/media-centre/press-reports-content.aspx?id=1932&type=C&news=beyond-tobacco

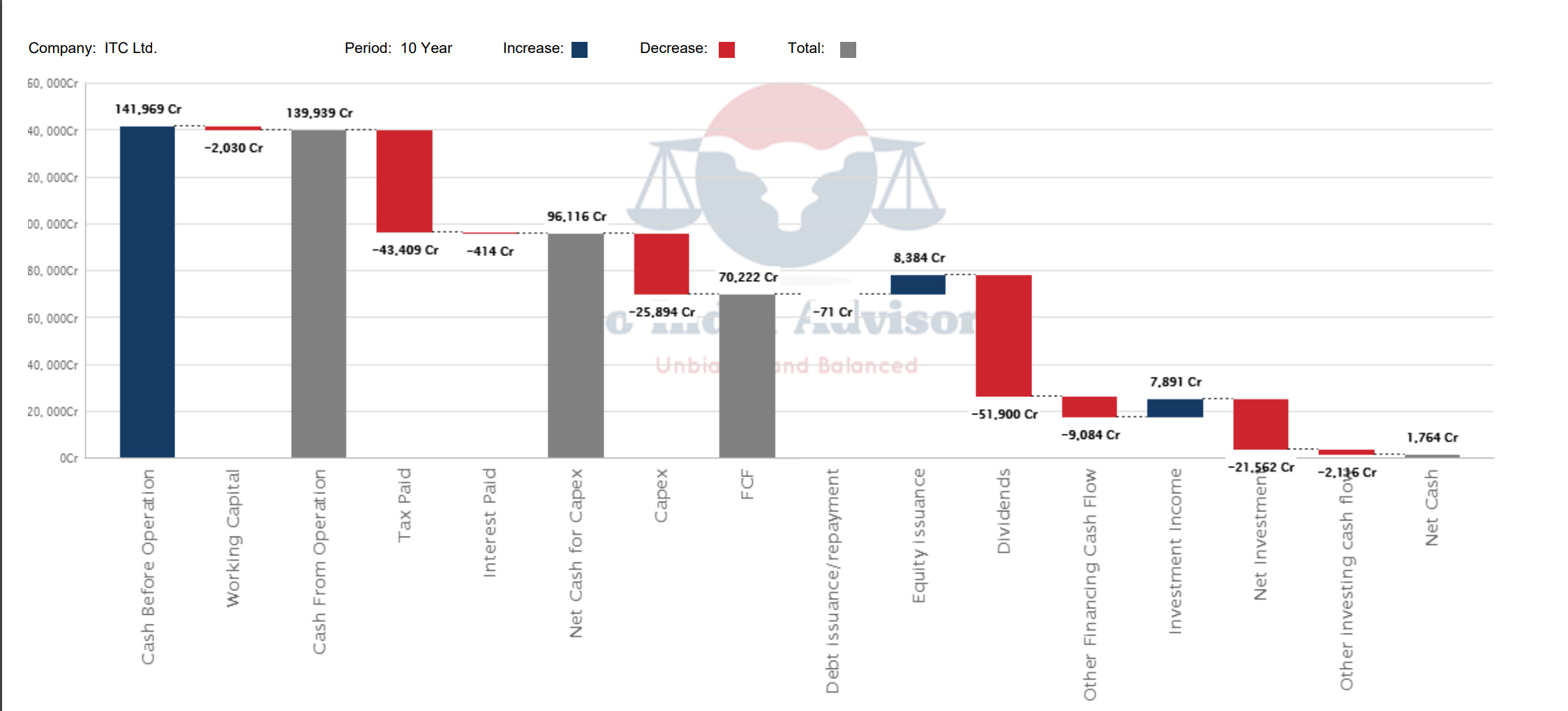

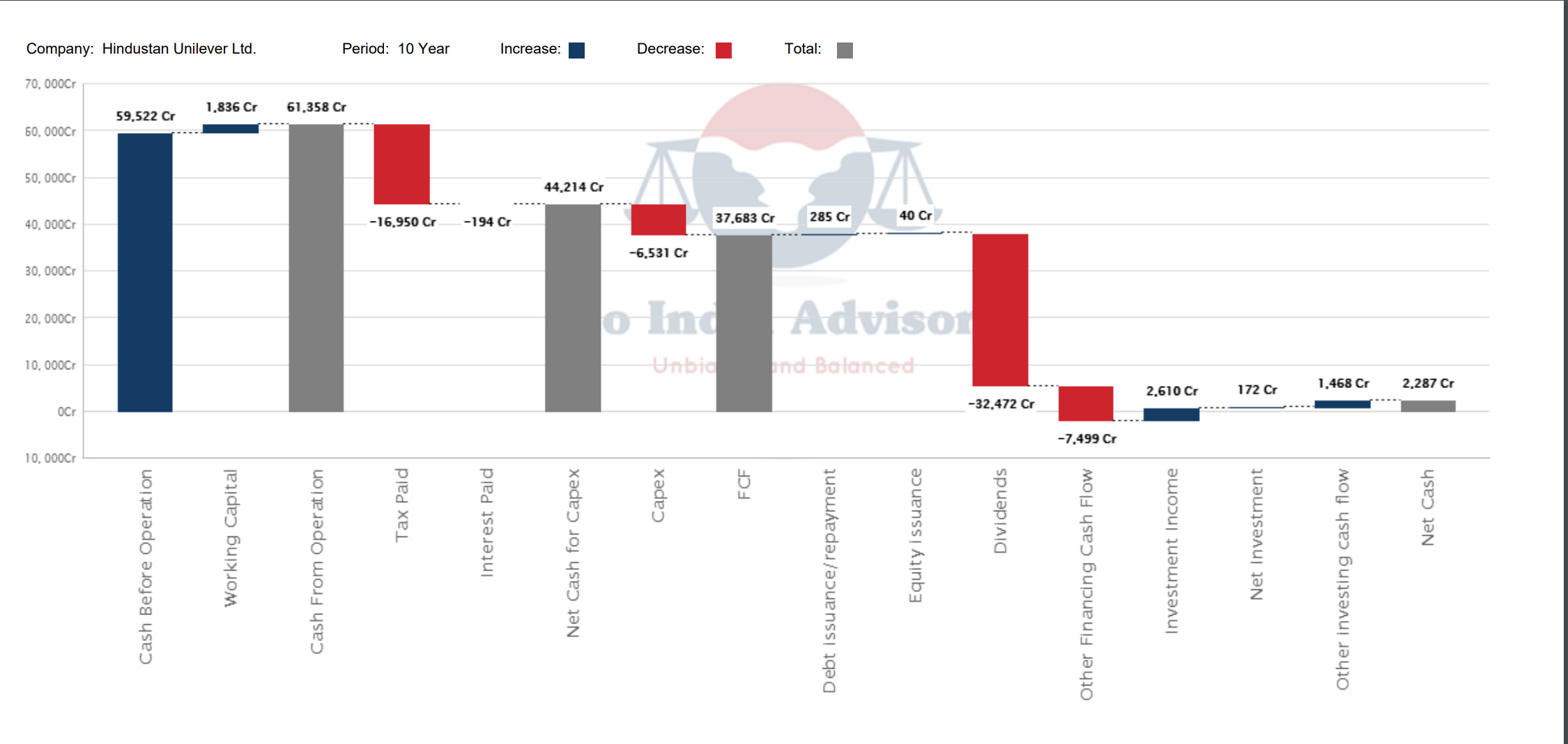

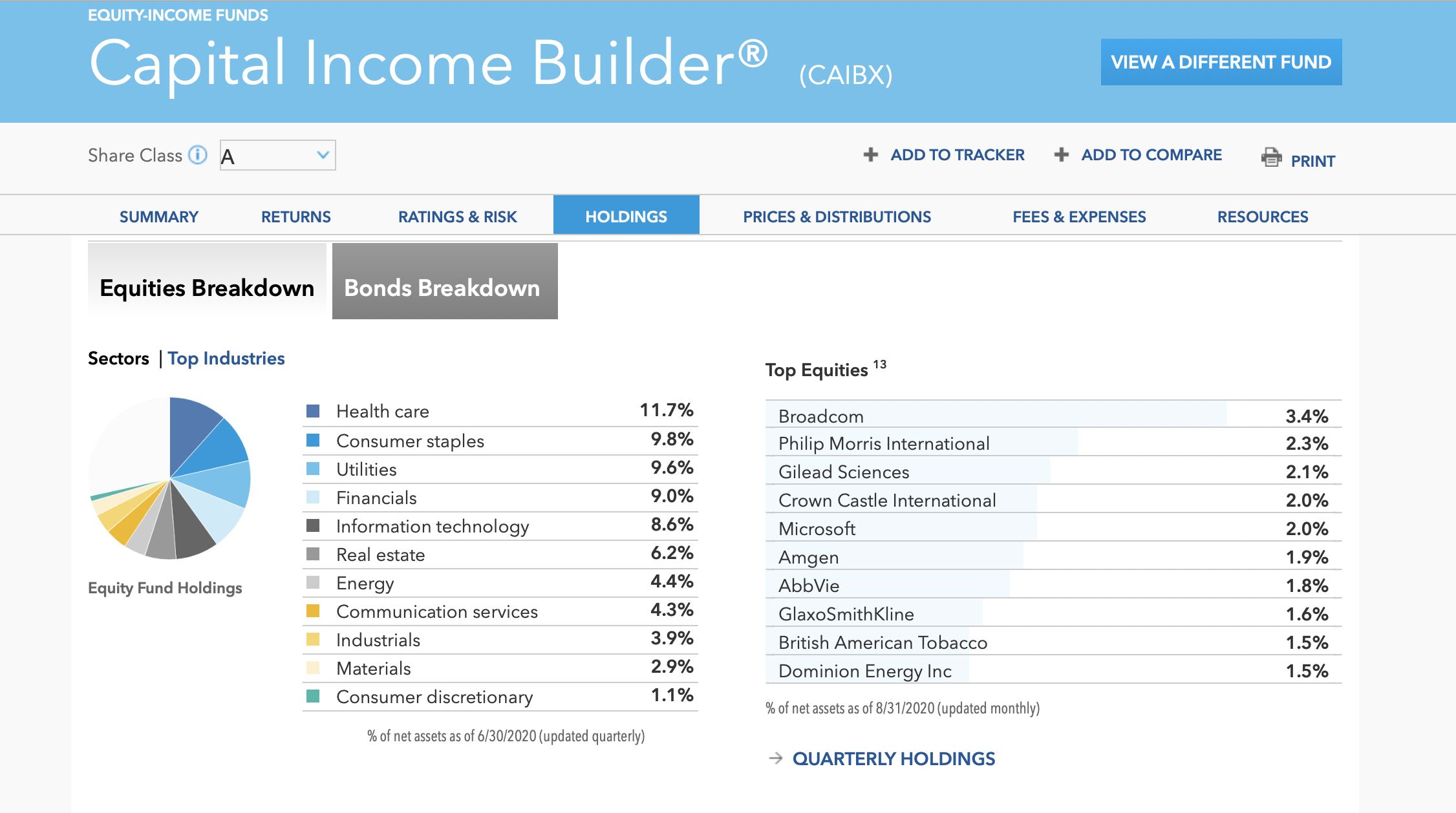

Comparing ITC with HLL

Mkt Cap - ITC - Rs210000cr; HLL - Rs486000cr

So HLL is 2.4x ITC

Comparing the cashflows:

ITC has generated FCF of Rs70000cr vs HLL of Rs37000cr over last 10years.

Source:GIA Stocks

Source: GIA Stocks

And bigger surprise is that, both have delivered around 9% cagr earnings growth in last 5years. ITC is already 3rd largest FMCG company in India by sales and it’s dominance will increase further.

2 Likes

I dont think reliance can eataway big FMCG margins. Surely they will eat distributors margins ( distributors will face existential crisis). For eating away big FMCG margins, ppl should not find any difference between original products and in-house products (so that reliance can threaten big FMCG). Reliance (without years of work)in no way create another nescafe taste (ITC sunbean is also inferior) , aashirvad atta taste ( i ordered ponni rice twice in big basket. First time it was good. second time it was worst- no consistency so we stopped ordering it) .

Moreover if you observe their in-house aloo bhujia is far inferior compared to haldirams (on the other hand ITC launched four products, aloo bhujia was on par with haldirams. Again yippee vs maggie battle will raise in aloo bhujia, they wont be able to capture major market share). I am ready to replace nuts/rice with their brand(if consistency is there). I am not ready to replace taste oriented products.

Tell me one in house product where reliance got hit? (I maybe ignorant about their successful products)

Moreover, jiomart is not big thing. After all its a distribution model for kirana stores. ITC nestle HUL TATA have enough resources to launch another mart and compete with reliance in their own brand.

Until big FMCG are able to protect their IP rights they cant erode their margins.

4 Likes

Indeed, this company does not have to answer to any promoters. L&T is one more such company. BAT hold significant stake in ITC, can they not influence and drive the management and prevent the wastage?

Also BAT prevented stock option for Aditya Puri and director team as per one article back in 2019 and so their cash salary was increased significantly. Had significant portion of their compensation linked to long term stock options, they may take decisions keeping shareholders in mind. But this would reduce BAT stake…so that’s a double whammy. When HDFC CEO retired, his majority wealth was in his stake in HDFC Bank…I don’t think that holds true for ITC.

As as mentioned before, all PPTs and directions so far are far from satisfactory from the management. Until it is seen in actions like for eg seen by Tata’s when they started selling and coming out of non-core and loss making businesses, its sadly just time pass…

3 Likes

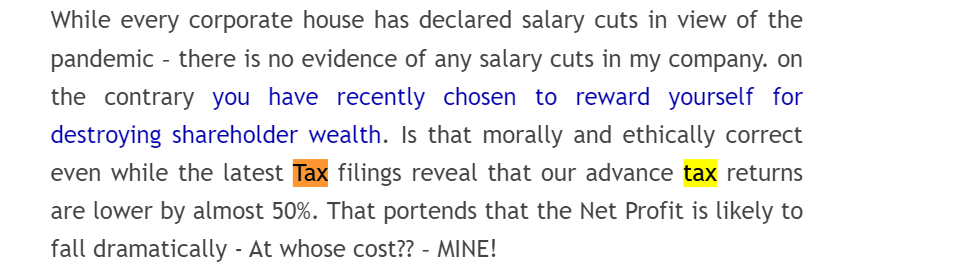

I am surprised by seing in this article that advance tax of ITC has reduced by almost 50%. Is that true? And this happening now, long time after lockdown has eased, shows time to come for next couple of years at least? Any insights welcome on this…

Can you please share the article about advance tax? I assume key reason would be decrease in corporate taxes last year.

Its in the same article shared above by Vishal. In the Biggest blunder para, there is a mention on advance tax filings.

Thanks. Unable to figure out which period it refers to.

Pretty harsh article. If we evaluate all companies with same yardstick there won’t be any equity investment in India.

I guess ITC has become very polarizing stock. Cold look at numbers suggest company is doing okish. Reaction if more to falling stock prices. May be tobacco companies valuation has changed permanently like coal companies.

6 Likes

Definitely, in Q1 minimum quantity of cigarettes sold (50% excise duty and ITC own 85% profits dropped)

so they didnt pay any advance tax.

A laid back management/ old age home board - I cant sense this from the market. ITC is more dynamic in product launches.

OMG, they say Savlon is bad acquisition.

ITC is in spice segment. Do you think keralites will change to aashirvad from eastern, tamil from sakthi or aachi, bengali from sunrise. Acquisition cost of 100% company differs from selling part of the company. Moreover sunrise EBITDA is 100 cr and eastern also the same. Revenue sunrise is 595 cr and eastern is 890 cr.

Hotels: Management face savingly accepted they failed and moved to ASSET right approach.

ITC manages its companies with its sub-segment head. Board is just for thumb-sucking.

I dont care about board age etc until they are dynamic in the market. If HUL captured major handwash/sanitiser/disinfectant i would have been the first person to exit by saying its a PSU/Govt company.

Reasonable (proper) queries to ITC management:

In spice segment: Sambhar powder which they launched 5 years back in tamil nadu disappeared all of sudden. So marketing cost everthing is in drain ( i accept that sakthi/aachi never allowed them to get large market share but cost of failure)

They gloat themselves we are very close to farmers, dont know why they left pulses besan poha organised segment to TATA sampann.

Why are u allowing VST/ Godfrey to grab your market share.

What is R& D for smoke free products ( like phillip morris)

Like this, I can write lot more.

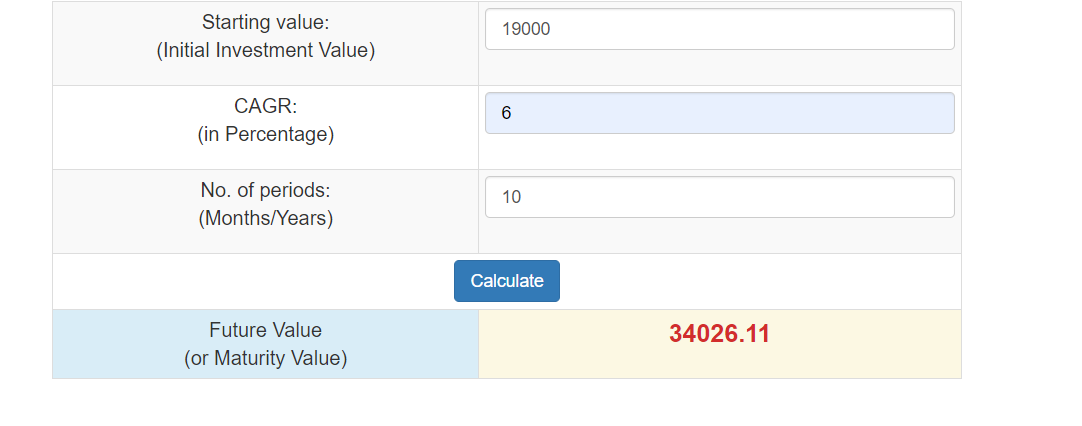

let assume ITC is having zero percent growth for next ten year, yet their revenue will be 32000 cr (because of inflation)

Remuneration of sanjiv puri is hiked. Absolute non sense. He is getting paid 6 cr till he gets YC deveshwar like or any other corporate head like salary he will hike it. More they shared august 2019 hike article and creating sympathy by saying " when whole world is doomed you are getting pay hike in COVID times "

This is 2018 article

2 Likes

Regarding eastern vs sunrise.

I dont know about sunrise. I am from kerala and can speak about eastern from my experience.

Eastern has a very bad name in Kerala if I am not wrong. Atleast , we avoid eastern at any cost.

I cant find any links other than this old news. But recently also similar allegations were there against the same. I am not sure whether they are right or not.

https://www.qatarliving.com/forum/qatar-living-lounge/posts/shocking-news-eastern-curry-powder

Very well written.

But if one had confidence in ITC in 2017-looks like he invested thereabouts, then what has changed in the business other than the price.

Only if someone invested in 2010 or earlier one can make these claims.

Though agreed all 10 points are spot on, but BAT as the largest shareholder seems satisfied with the management.

Hoping for extreme pessimism and 8% yields to enter

5 Likes

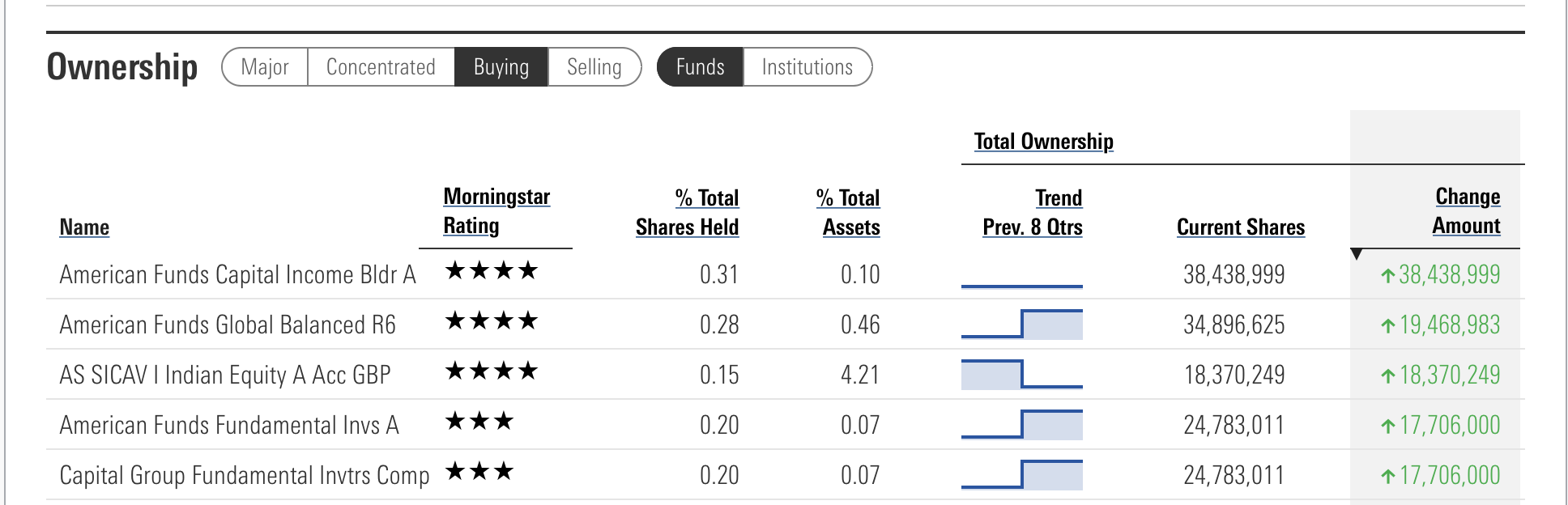

Who has been buying ITC stocks recently

…

Why is Amercian Capital Builder buying it - Higher Yield for Retirement … It has been buying most of tobacco stocks across the world … Interesting … While the supply of ITC stocks has increasing because of offloading by HDFC mutual fund … new buyers like PPFAs and American income funds are taking up their place …

7 Likes