Hi everyone,

I have attempted to do a deep dive into the Indian Cigarette Industry from an equity valuation perspective. The reason for doing is that when I was attempting to project revenue growth of Indian Cigarette companies such as ITC, VST I wanted an understanding into the drivers affecting Indian Cigarette consumption but could not find any comprehensive article or report. Thus, I read equity research reports, filings of listed companies, WHO reports, several studies analyzing tobacco usage in India, etc and thereafter aspire to share with you’ll the relevant information in a coherent and succinct manner. The information is by no means comprehensive and a Cigarette industry insider can accuse me of being “Captain Obvious”. However, having come across many ITC/VST investors who have limited knowledge of the Cigarette Industry (as I did prior to commencing my research), it is my sincere hope that this information can increase their knowledge to atleast a certain basic level in the shortest time possible. I hope that this information can aid an investor in making their own projections and/or evaluate the validity & possibility of Cigarette revenue projections made by analysts.

With the introduction out of the way, the key factors to consider while evaluating Cigarette consumption in India are:

1) Cigarette consumption is only 4% in India as compared to 25% in China or 28% in Europe. However, can this fact be extrapolated to assume that Indian Cigarette market has huge growth potential? Not by a long shot. This is because not only does the Indian consumer has several options to get his/her tobacco fix but also these alternate options are substantially cheaper than Cigarettes.

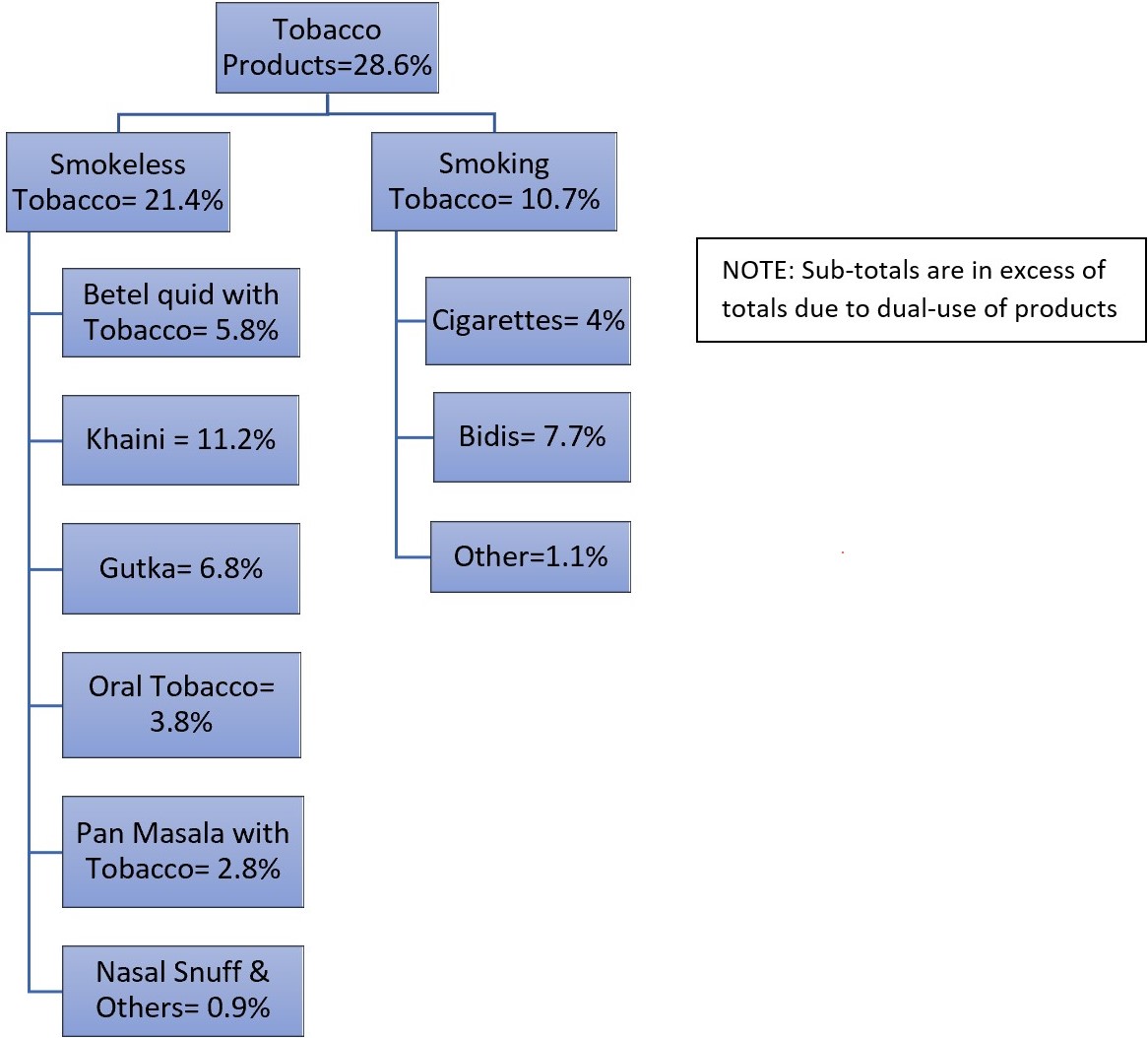

As per the GATS-2 survey tobacco usage in India is 28.6% and thereby is higher than most countries. However, tobacco usage in India is very different from other parts of the world. Smokeless tobacco is twice as popular as smoking tobacco. Even within smoking tobacco, bidis are twice as popular as Cigarettes. Cigarettes are only 14% of the total tobacco consumption. Thus, an assumption that the Indian cigarette industry has a long growth ahead, simply because of lower percentage use of Cigarettes compared to other countries, cannot be sustained.

2) Cigarettes are around 3.5x price of bidis and around 11-12x price of Chewing Tobacco.

Cigarettes are extremely expensive compared to other Tobacco products. Because of the sheer price difference between the tobacco products, switching to Cigarettes from Chewing Tobacco or Bid involves a huge monetary impact and thus its not easy for a Cigarette company to “up-sell” and convert a bidi/tobacco user. One can also argue that the refinement of a Cigarette cannot be compared to a bidi (or the social nuisance of chewing tobacco) just the way you cannot compare a country liquor with a single malt whisky (even after adjusting for alcohol content). This is a fair point.

However, the idea in this point and in the previous point no.1 is to show that the Indian consumer has several tobacco products (available at a variety of price points) to choose from and such variety in tobacco products is not so prevalent in most of the other countries and thereby projecting growth rates in cigarettes based on other countries and/or assuming that Cigarette companies can easily “up-sell” their Cigarettes is seriously flawed.

3) Can cigarettes be taxed higher?

Before this question can be answered, the following questions must be considered:

a) How much have Cigarette prices increased over the years?

Various studies inform us that cigarette and bidi real prices increased about 3% and 3.70% respectively on a yearly CAGR basis from 2000 to 2018. However, at the same GDP/capita increased much faster. That means cigarettes and bidis take a smaller portion of our wallet now as compared to what they did in the year 2000. Cigarettes have actually become CHEAPER by 20% (and bidis by 30%) when compared to that in the year 2000!

b) What are the tax rates on Cigarettes in other countries?

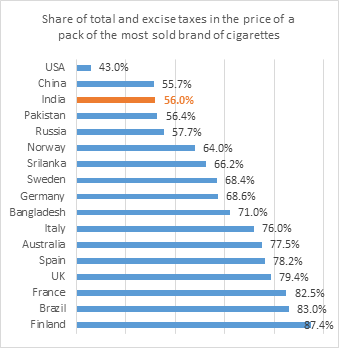

India has a tax rate of 56% for the year of 2018. While there has been further increase in taxes in India after 2018, the tax rate on Cigarettes is less than that of many countries as can be seen in the chart below

Furthermore, WHO recommends that the taxes should be at least 70% of the retail price. However, despite their inclusion in the GST demerit list of highest tax slab and even after accounting for the recent increases, taxes on tobacco products are still below the WHO recommendation.

Now, when the information presented in 3a and 3b are looked together, it is rather unlikely that taxes on cigarette will reduce. On the contrary, there is every chance that it may increase further. Unlike most investors I hope that now, with this background in mind, you will not be surprised if & when the Government increases their taxes on Tobacco.

4) Tobacco use has been declining in India

a) Various study have noted that over the past three decades, the prevalence of smoking has declined steeply and consistently. Smokeless Tobacco, after seeing an initial rise, has also declined but by a lesser magnitude. The GATS-2 survey (conducted in 2016-17) shows decline in tobacco use as compared to that prevalent during the GATS-1 survey (during 2009-10)

b) Furthermore, under the National Health Policy 2017, the Indian Government has set a target for reduction of 30% (from 2010 levels) by the year 2025 . Thus, it is highly unlikely that there will be relaxation in Government policies towards tobacco.

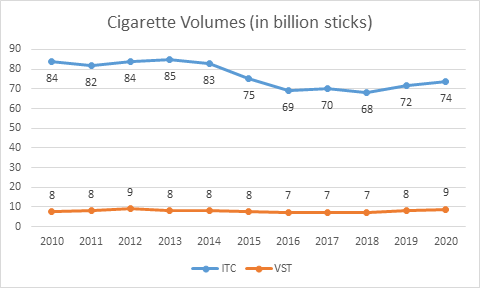

c) Market Data

The combined Cigarette volumes of ITC Ltd (the largest cigarette manufacturer in India) and that of VST Industries Ltd (a manufacturer of “value” cigarettes) have not grown in the past decade. As per various equity research reports published by ICICI Direct and HDFC Securities, the volumes have marginally declined as can be seen below:

CONCLUSION

Based on the above, as of today, it is my view that the revenue growth in Cigarettes is very unlikely to come from any significant volume growth and instead the companies will have to primarily rely upon price increases for increasing revenue. Price increases, as we have seen, can increase revenue but only up to a certain point as beyond that, the consumption will fall. Furthermore, price increases have to be shared with the Government in the form of GST and cesses. Hence, one must be extremely vary of making any strong revenue growth projections for Indian Cigarette companies. Is strong volume growth possible? Sure, but the question to ask is how likely is it? It is my view that investing is a game of probabilities and therefore less likely outcomes should not be modelled while projecting revenues.

Needless to say that if the underlying factors change then my view will (and should!) change.

The various studies, charts, graphs, etc referred to above are duly linked and referenced in a more detailed article published on my blog. In case you want to read the article then click HERE

Note, the usual disclaimers apply