Hi Panduranga, this is very good scuttlebutt.

ITC is Just spending 2% of sales on advertisements. Then, I excluded cigarette sales, Hotel Business, agri & paper business Sales and considered only Branded packaged foods, personal care, agarbatti matches, wheat & Spices etc sales - even then their spend on Advertisement and promotion came up to only 6%

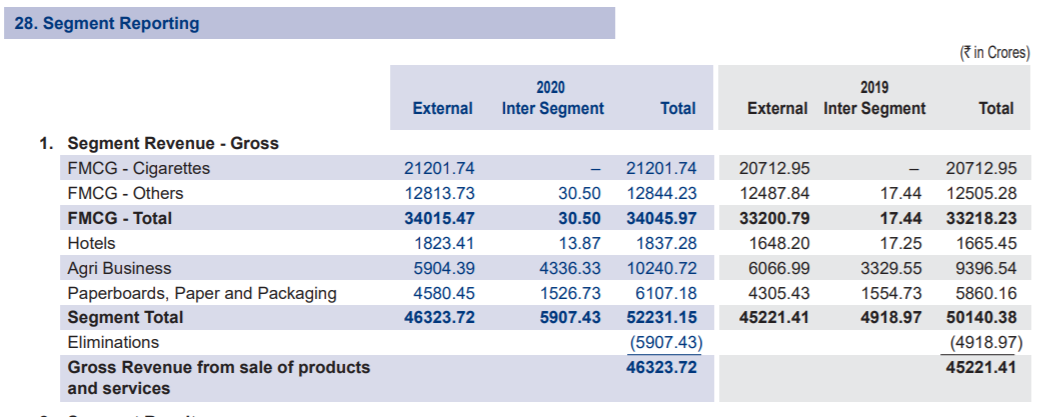

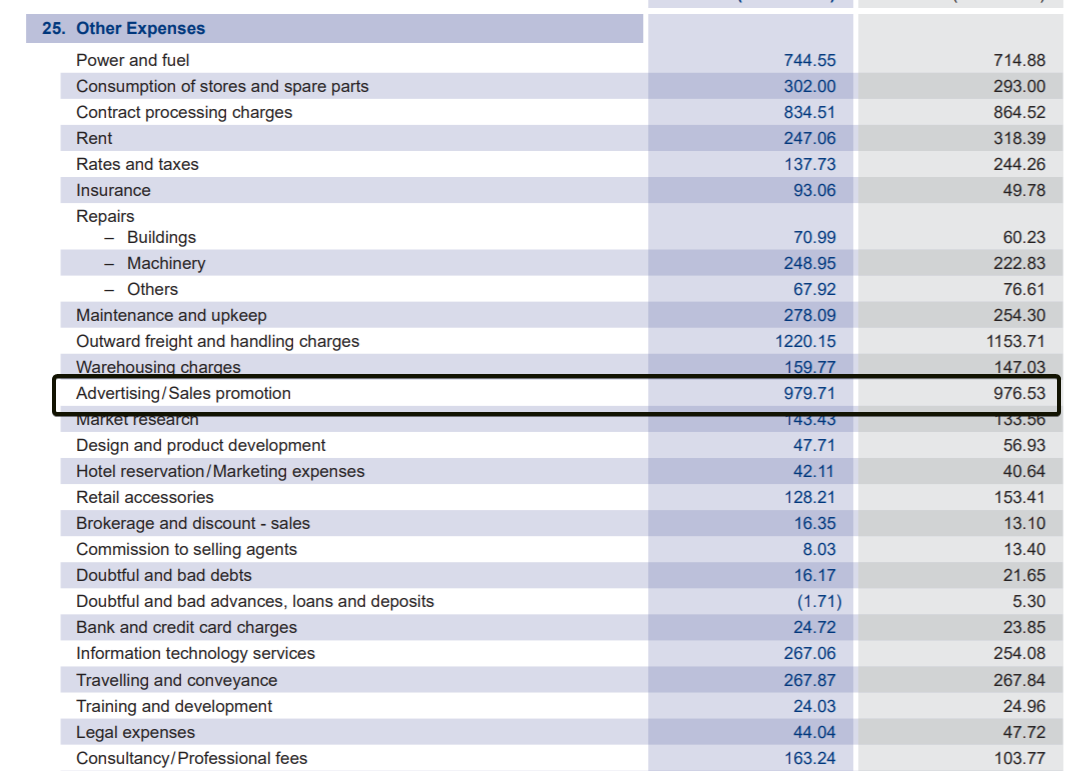

From 2020 annual report, the contribution from FMCG is 12.8k crores and they’ve spent 980 crores on advertisements as a whole. Since the contribution from cigarettes would be negligible (zero ideally), we need the FMCG spends should be around 900 crores to get a rough estimate (compare that to HUL who spends 4800 crores on advertisements and promotions). ITC isn’t even spending 1/5th on ads compared to HUL but the revenue contribution for ITC’s FMCG is 1/3rd vs HUL. Statistically, ITC should spend more

Let’s dive further into individual product segments:

From total consumer spends of ~20k crores, ITC makes ~12.8k crores

- Aashirvad alone which contributes 30% to this, has a 28% market share and is growing at 15%+. Can spend more

- Sunfeast can be a big brand for ITC in the future (they can replicate the strategy used by Marico with Saffola). Big opportunity to come up with new products and increase ad spends

- Bingo too is doing well (in a duopoly with PepsiCo) and there’s a good possibility of introducing new products

- Yippee is gaining market share (~25%) from Nestle in a big way but it is to be seen whether they can grow healthily on a higher base. Ads are a must in this segment

- Additionally, I have no idea how ITC is unable to sell Fabelle which is a very good product but just not visible in any of the Kirana stores. Recently noticed in one of the nearby stores that a Fabelle chocolate display rack is used to keep Dairy Milk chocolates

ITCs total capital employed in the FMCG segment is around ~6600 crores and is currently making 12.8k crores in revenues with a meagre OPM of 4%. However, things have improved since March 2020 and the margins have touched 9.2% for Q3-FY21. Once ITC is able to make 10-12% sustainable margins in the FMCG segment, the ROCEs will start to touch 20-25% which seems to the key driver for re-rating

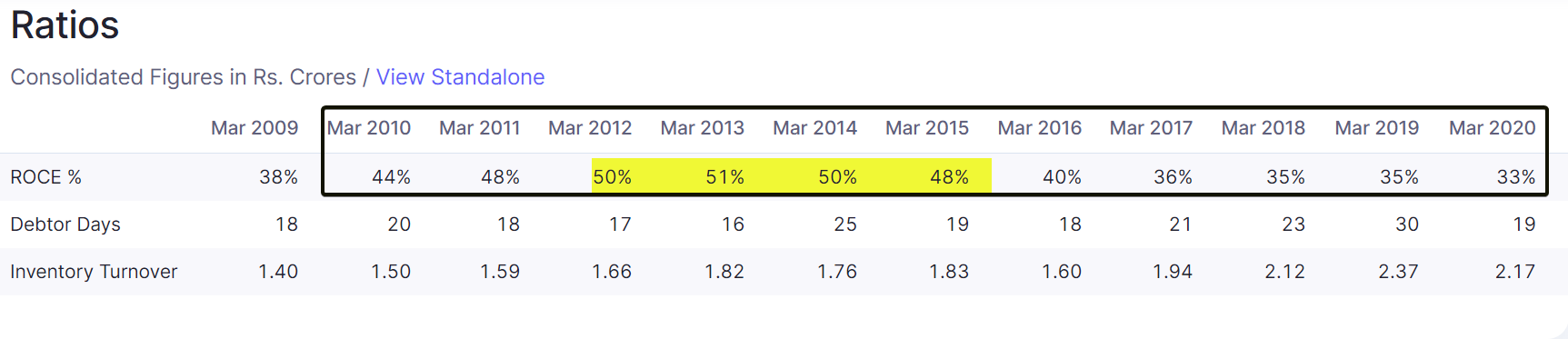

While most people say that ITCs profits have grown in double digits (like HUL), the stock price hasn’t grown, it’s completely justified since the incremental growth has come at a significantly lower ROCE as seen below. ROCE is down from 50% to 33% which is never comforting. Can’t see stock getting re-rated unless we see massive earnings growth or better profitability/efficiency metrics

Assuming 12% OPM, ITC can make ~1200 crores in net profits which is still around 8% of the profits from Cigarette segment. Even if ITC manages to 10x its profits by 2030 from the FMCG segment and keep the margins at 12%, it will still not reach 14.5k crores which is the contribution from Cigarette segments in 2020… Just give it a thought on how much capital needs to be employed in the FMCG segment to reach 12k crores profit. Now, with 85% payout and investing only 2k crores into the business, this is surely a big task to achieve. Lot of questions needs to be answered by the management; execution has been below-par which is a major reason for such big underperformance

Disc - ITC is one of my biggest holdings