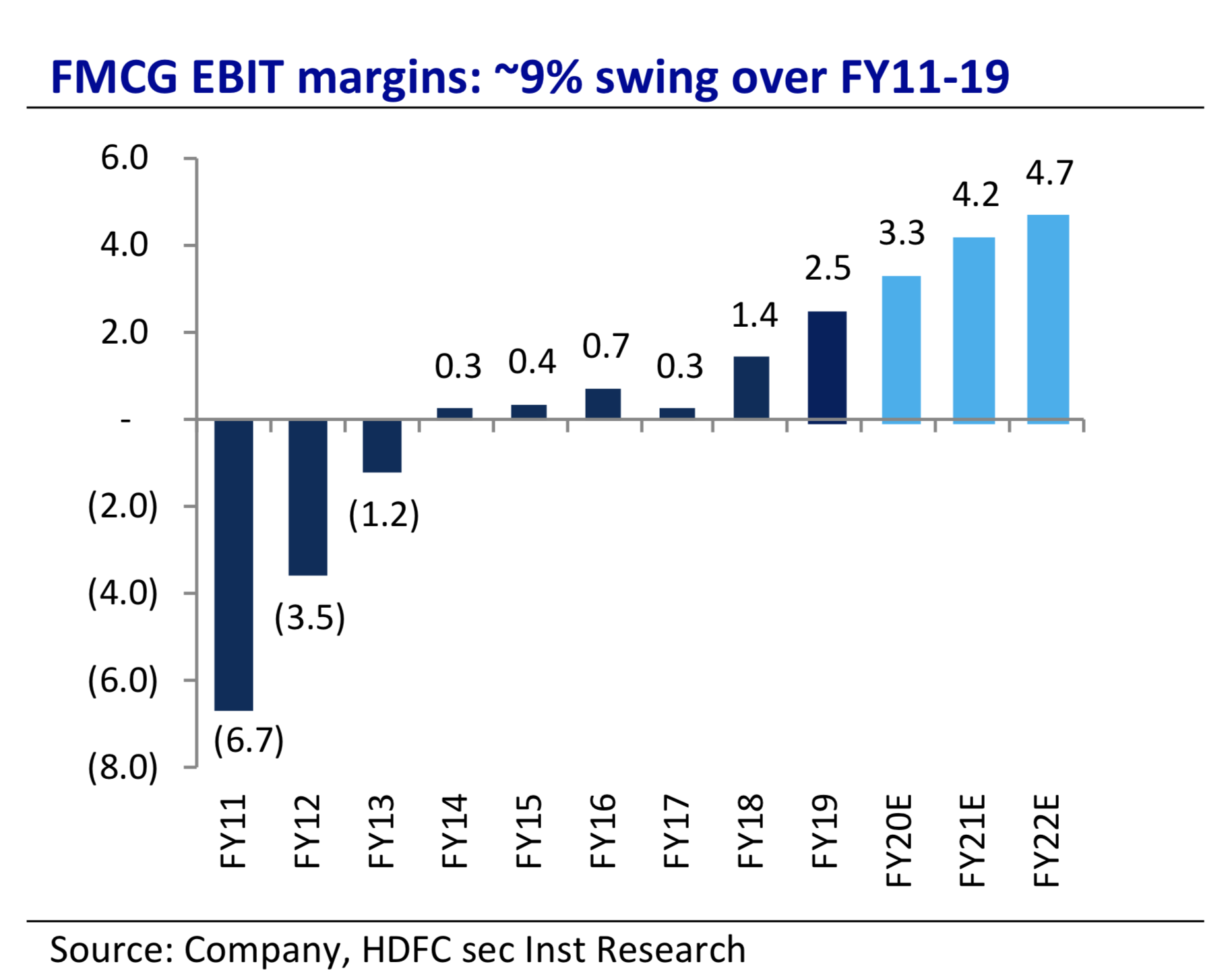

FMCG margin has been consistently getting better. I have attached a snapshot from HDFC Q2 report below.

HDFC also said in a side note that ITC’s gross margin is at par with peers ( 40-45 % ) but low margin is due to Higher upfront brand investments and Losses in retail business. FMCG EBIT margin expansion was driven by enhanced scale, product mix enrichment and cost management initiatives notwithstanding higher investments in brand building and gestation costs of new categories.

Everyone is comparing HUL margin with ITC now… But I think best would be to look at HUL margin in their early days in 1990-2000s. Actually HUL ( in their older version ) exists in India from 1933. From 1956 inwards its called Hindustan Lever. And from the beginning they are into FMCG products. I could not find earlier Annual reports in their website. So I read the AR of 2002 and attached a snapshot of their margin from 1992-2001.

Clearly margins have been low during the product gestation period. Margins did pick at a rapid pace. But thats mainly due to liberalisation in 1991 and lots of funds in flow. ITC is trying to build our own Indian brands competing with worlds biggest FMCG giants like Unilever, Nestle, Coke and Pepsi. It’s a matter of time that FMCG margins will gain.

They are already number 1 brand in Aashirvaad, sunfast cream biscuit, Bingo, matches (Aim/Ship) and number 2 in Yippe, Fiama, Savlon and Classmate. Plenty of other brands are emerging. These are no way easy goals to achieve competing with established players. Next decade will be a good one for ITC.

Of course our economy is not doing well and consumption is growth is slowest in 11 years ( after the severe financial crisis ) and the problem does look structural. But I hope that consumption revives in next months.

Discl: I hold ITC and hence my views could be heavily biased