Did you get to know anything wrt licence fee/royalty , any update on this issue?

Unfortunately, no updates - provisions are still affecting profitability so status quo prevails, I suppose.

Maybe we all can write to investor relations. investor.relations@irmenergy.com

Update : I have sent a mail requesting for provision amount, updated on SETC CNG pilot bus project and to conduct investor calls with management.

1 Like

I am not sure if this is due to pilot project undertaken by IRM however still encouraging news given it’s Trichy route.

1 Like

Hello sir, did you received any response from the company, also as per today’s notification IRM has appointed Mr Abhay Gupte as independent Director , previously he was with Deloitte - how this appointment should be seen - will it strengthens the corporate governance? Your views , asking so as to learn things more & understand

Thanks

Divyansu K Taneja

Have been tracking IRM for last 2 months and attempted a valuation exercise below:

Key Financial Inputs:

- Capital Expenditures (CAPEX): ₹800 crore (total to date)

- Net Cash (Cash minus Debt): ₹180 crore

- Annual Cash from Operations: ₹120 crore

2. Assumptions for DCF Analysis:

- Revenue Growth Rate: Assuming a conservative annual growth rate of 10%

- Operating Margin: Maintaining current cash from operations margin

- CAPEX: Assuming ongoing annual CAPEX of ₹80 crore (10% of total CAPEX to date)

- Working Capital Changes: Negligible

- Tax Rate: 25%

- Discount Rate (WACC): 10%

- Terminal Growth Rate: 3%

Adding the PV of the 5‐year cash flows and the PV of the terminal value yields an enterprise value of about: 296.7+1,034 ≈₹1,331 cr

Incorporating the net cash (since the analysis provides an “adjusted” net cash of ₹180 cr), the equity value is: 1,331+180 ≈₹1,511 cr translating to per share price of 368

Looks cheap but majorly the numbers look good due to assumptions which have to hold with fluctuating gas prices, licensing fee and reduced APM allocation.

Discl: Invested in last 30 days

2 Likes

Have you accounted for the Royalty fee promoter charges for IRM brand in your valuations?

New CNG station in Banaskantha. Interestingly they’re opening more in Banaskantha than new Trichy - Namakkal GA.

https://maps.app.goo.gl/dsWK1gB7YrQF8nrN6?g_st=iw

Unfortunately I haven’t received response yet from investor relations and have sent a follow up. Suppose more queries from fellow investors will help!

1 Like

IRM energy is still in investing phase and once pipelines in Trichy Namakkal area are established next 3 years growth could potentially be much higher. I first got interested after seeing it correct a lot from IPO price and reading news around IPO time was helpful. Of course, there are other corporate governance issues but I see traction after new CEO assumed office.

“In the next four years by the end of FY27, 30% of the volume will be coming in from the area we have in southern India, Namakkal and Trichy and around 30-35% will be coming from Banaskantha and around 40% will be coming from the Fatehgarh Sahib GA.“

2 Likes

Update on investor relations response after multiple follow-ups and adding info@irmenergy.com to mail chain.

In respect of Licence fees issue- Our Board is seized to the issue and will take suitable action as appropriate time as deemed.

Pilot Project Updates- This is ongoing process

Investor Conference Calls- Will update you through Stock exchange announcement

I believe, one way to make management oblige with more details is bit of investor activism. ![]()

Update since I can’t post more than 3 consecutive replies per VP rules ! ![]()

IRM Energy inaugurates its 100th CNG station.

Which happens to be 47th at Banaskantha - good to see company changing gears to next level.

7 Likes

The two long term contracts signed recently with Shell and GSPL add up to 500 mmscm (174 + 326) of LNG (for a period of 5 years).

The current production volume is about 25 mmscm per Quarter of CNG and about the same for PNG (from investor presentation).

Now,

1 mmscm LNG = 1.63 mmscm of CNG, and

1 mmscm LNG = 3.6 mmscm of PNG

So at the current rate of production, they will produce 500 mmscm of CNG (25 x 4 x 5) and the same volume of PNG in the next 5 years.

The above production will need

(500/1.63) + (500/3.6) of LNG

i.e., 306 + 138 = 444 mmscm of LNG over the next 5 years

…but as per management the production will double by FY26

So the current contacts fall well short of their future needs.

2 Likes

Hi apurva sir can you please explain more bcos i am not able to understand that company will need 444 mmscm of LNG over the next 5 years & the 2 contracts give 500 mmscm then how the current contacts will fall well short of their future needs ? If you can explain,

Secondly if you can also explain the below line

…but as per management the production will double by FY26

Sir is it like the company would require similar amount of lng (500) more due to IRM’s expansion by fy 26 & that’s why the requirement is more or requirement is just double & that’s why it falls short ?

Thanks

.

1 Like

Yes, 500 mmscm (thru recent contracts) suffices if they keep the production at the current level. At the current production level my estimate says they need 444 mmscm over the next 5 years (which is < 500 of contracted volume)

However, we know from the management commentary that production will likely double in the next 12 to 24 months. So if that be true then they definitely need more than 500 mmscm of LNG over the next 5 years (it will be more than 444 and less than 888 because production ramp up will take time).

What I said above is very theoretical – I am sure they will find a way to get into new contracts and even buy at spot price to meet the demand.

3 Likes

is there any connection between MIT holdings in India Inc. and Kenneth Andrade? (WRT your note : Lastly, MIT (Kenneth Andrade) )

Finally some media presence and public appearance by CEO.

Good summary

2 Likes

Hello everyone,

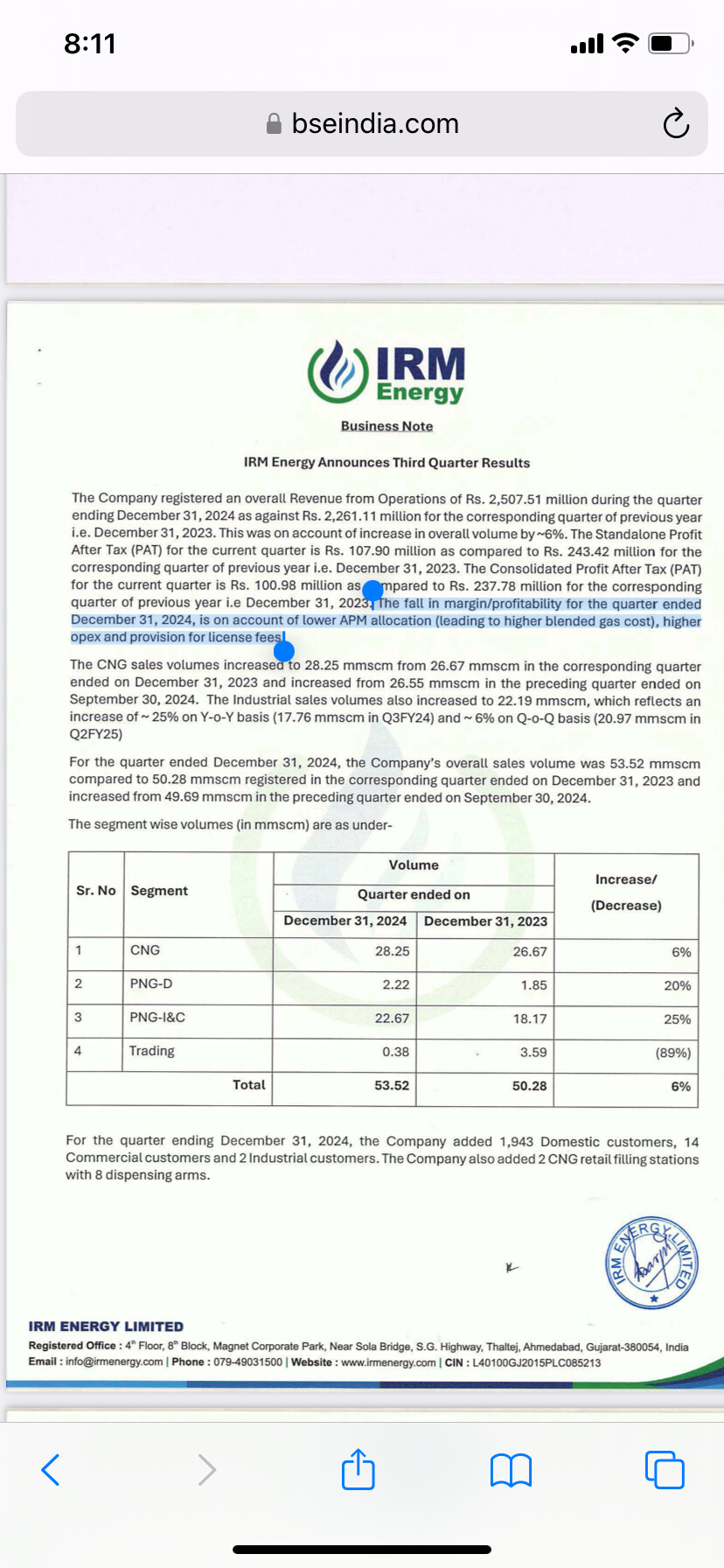

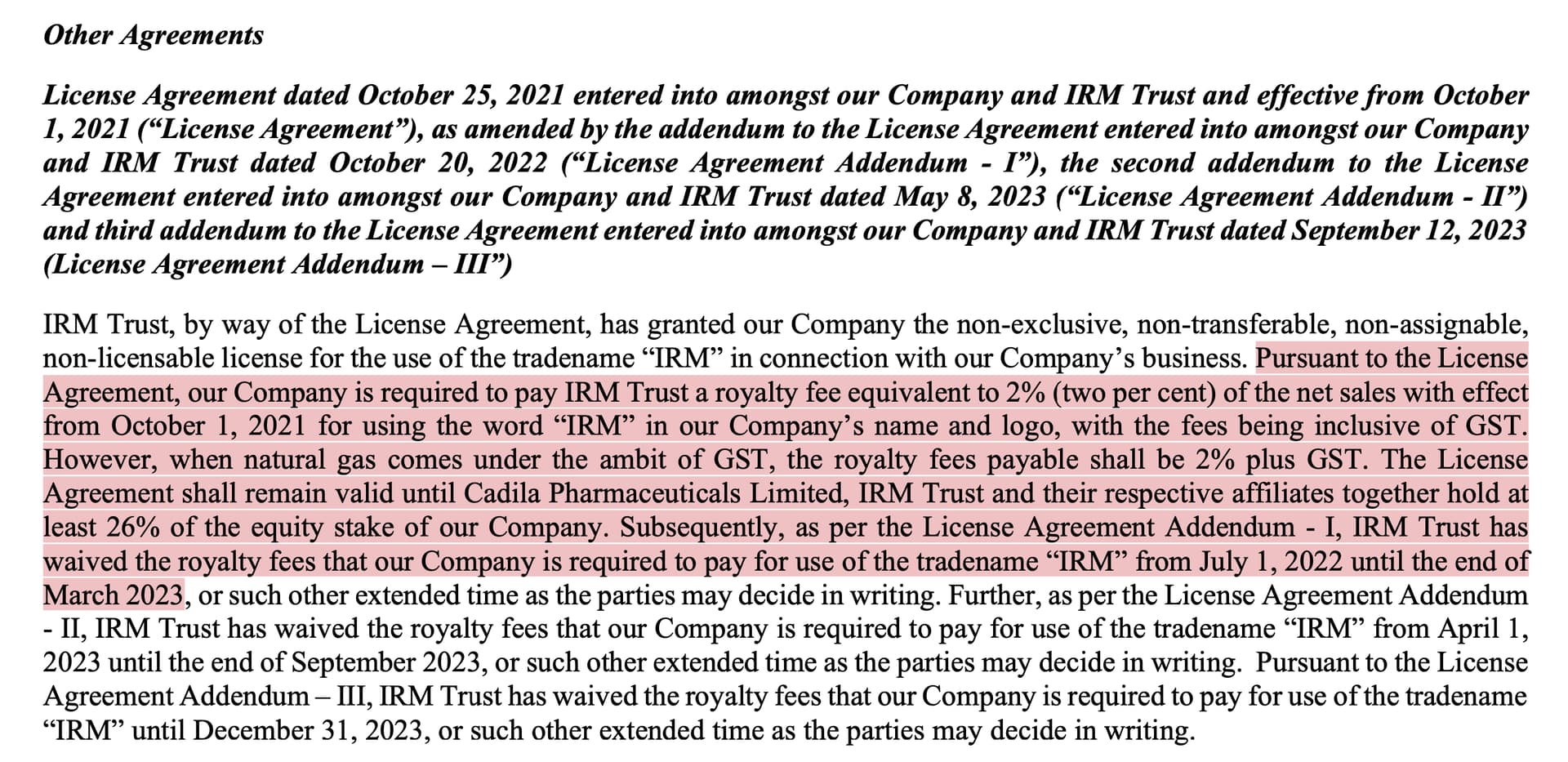

I have a question. Wasn’t the royalty fee disclosed by the company in the RHP? Please see the screenshot below from Page 238 of the RHP. The company disclosed that a royalty fee of 2% of revenues would have to be paid till the time the promoters hold 26% equity stake. It also mentioned that fee had been waived till end of September 2023. And they seem to have actually acted as per this disclosure. What am I missing?

2 Likes

IRM Energy Ltd has entered into a three-way partnership with GAIL (India) Ltd and IAV Biogas Pvt Ltd to support the distribution of Compressed Bio-Gas (CBG) in Tamil Nadu’s Namakkal and Tiruchirappalli districts. Signed on April 17, the agreement is part of the government’s CBG-CGD Synchronisation scheme, which aims to integrate cleaner bio-gas into India’s urban gas supply systems.

Under the terms of the agreement, IRM Energy will procure up to 3,000 standard cubic meters per day (SCMD) of Compressed Bio-Gas from IAV Biogas Pvt Ltd. This bio-fuel will be fed into IRM’s city gas distribution network across the two districts.

3 Likes

4QFY25:

Positives

- Capex-led growth continues on all fronts

Negatives:

- Management mum about royalty fee issue

- Operating leverage not seen playing out

4 Likes

Hello apurva & also other members who are tracking IRM energy, pardon me for asking naive Questions, want to understand the company

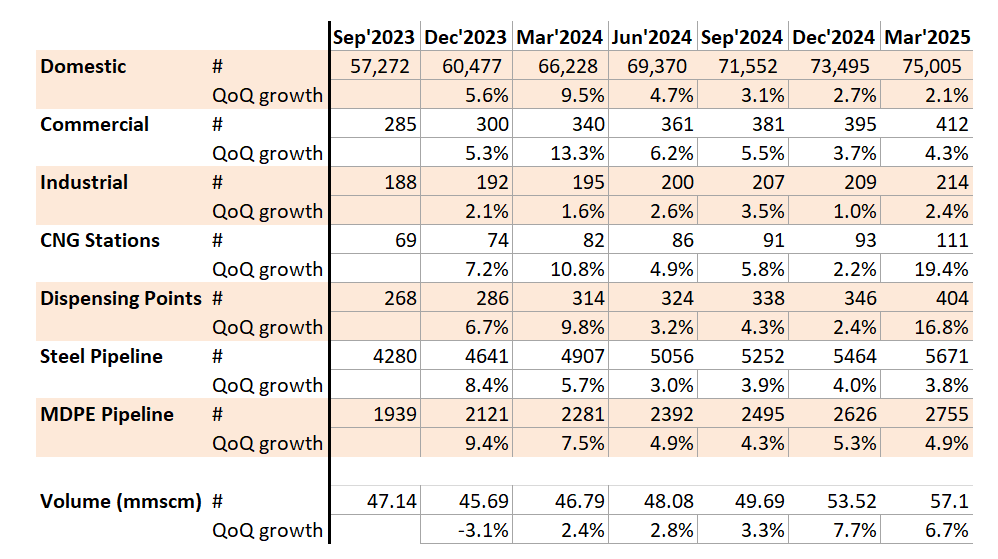

Q1) by which year this whole capex is estimated to reach final stage or how much it’s completed as of March 25 - -is it 50% complete ?

Q2) with increased cost of natural gas due to APM gas allocation reduction which led to reduction in margin & reduced overall profitability - what are your thoughts - should it be assumed that margins can remain in this range for next few Quarters

Q3) & finally considering the current margin profile & cash flows which metrics can be taken to value this company & compare & get sence how much it’s undervalued ?

Thanks

Divyansu K Taneja

1 Like

Regarding #1: looks like about 40-45% capex is done (based on planned, not sure about actual)

1 Like

Thanks apurva sir for your inputs - always very helpful,

i was trying to understand the overall picture & i have tried to write it below

What i understand sir - increase of sales not an issue most probably in coming 2-3 years they can easily increase sales by 50%-60% or even much much more, what i am not able to get hold on is margins profile, definitely this Quarter margin one of the lowest both due to reduction in apm & sourcing of high natural gas prices internationally , meanwhile from april internationally natural gas prices have decreased around 20% which can reflect in IRM next Quarter results(will it? Bcos i don’t know there procurement process, how many days before it is) but what about sustainable margins ? Bcos natural gas commodity in itself has been very volatile and definitely in 2024 it has increased a lot so can it be Around 8-9% margin profile or higher, definitely if environment will allow they have an option to increase selling price , but don’t think it can happen so early , coming to valuation if we take price to book metric then it’s cheap in comparison to other players ,also in terms of operating cash flow to price that is also okay when situationally cash flow will increase in coming years,

So in totallity the only problem is margins since it mainly depends upon international prices of natural gas, & can Russia Ukraine peace bring natural gas prices more lower ?

I am still trying to understand so please correct me members & add whatever possible

Thanks

Divyansu K Taneja

3 Likes